|

市場調查報告書

商品編碼

2063272

亞太地區政府和教育物流:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Asia-Pacific Government And Education Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

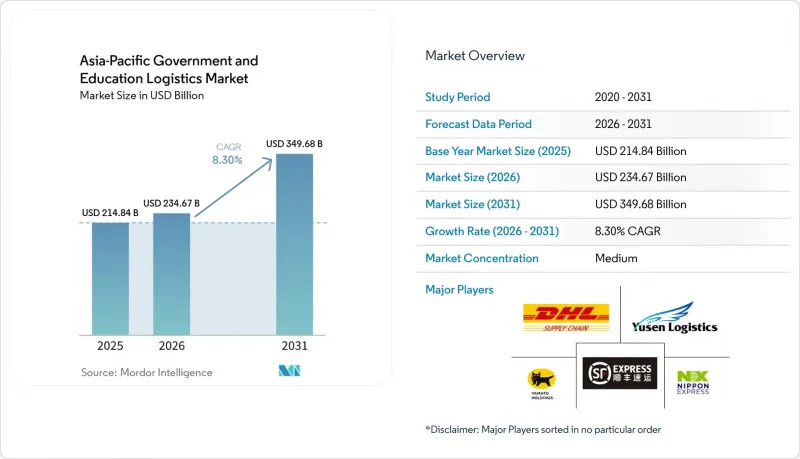

根據 Mordor Intelligence 預測,亞太地區政府和教育物流市場規模預計將從 2025 年的 2,148.4 億美元成長到 2026 年的 2,346.7 億美元,到 2031 年將達到 3,496.8 億美元,2026 年至 2031 年的複合年成長率為 20318.30%。

這一成長軌跡反映了國防自主能力的增強、大規模數位化學習的普及以及公私合作外包框架的建立,該框架正在重塑全部區域供應鏈的問責制。報告按服務類型(包括陸路、鐵路、航空和海運)、最終用戶(中央/聯邦政府、州政府和地方政府)以及地區(中國、印度、日本、韓國、澳洲、印尼、泰國、越南、馬來西亞和其他亞太國家)進行細分。市場預測以美元計價。

亞太地區政府和教育物流市場的趨勢和見解。

大規模電子政府和智慧基礎設施經濟措施

各國數位政府計畫透過資助硬體部署、雲端遷移計畫和資料中心建設,持續推動物流需求。印度的「數位印度」舉措已撥款300億美元用於數位基礎建設,確保25萬個政府機構和150萬所學校的物資供應暢通無阻。印尼耗資320億美元的「努桑塔拉」智慧首都計畫也需要協調多個機構之間的貨運。越南的「工業4.0框架」要求所有部會在2027年前採用雲端服務,這增加了對關鍵資訊通訊技術設備安全運輸的需求。菲律賓的資訊通訊技術指南評估競標的網路安全能力,並要求第三方供應商取得ISO 27001系統認證。雖然這些項目為供應商提供了多年發展前景,但也加劇了國家和地方政府採購流程的零碎化。

區域國防採購(AUKUS、QUAD)的擴大正在推動對安全可靠的第三方物流的需求。

隨著國防現代化進程的推進,必須符合嚴格清關和倉儲管理標準的貨物流動速度正在加快。澳洲耗資3,680億美元的「海鷗」(AUKUS)潛艦計畫需要核能推進零件的物流,而這些零件只能由經過審查的承包商處理。四方安全對話(QUAD)供應鏈韌性舉措正在澳洲、印度、日本和美國之間統一安全程序,並為兩用物項建立指定的運輸路線。日本計劃在2027年將國防支出提高到GDP的2%,這將對彈藥和高價值系統產生新的倉儲和運輸需求。韓國大力推廣國產平台,也增加了逆向物流的複雜度。因此,現有的國防認證供應商可以收取高價,而新進業者則面臨很高的進入門檻。

亞太地區卡車駕駛人老化和日益短缺。

在日本,47%的駕駛人超過50歲,不斷加速的退休率加劇了運輸能力的短缺。在澳大利亞,預計到2024年將出現2.6萬個工作崗位的缺口,而國防和安全審查的障礙進一步惡化了這一局面。儘管韓國的薪資年增了18%,但由於職業訓練學校數量有限,泰國在本地線路的駕駛人短缺問題上舉步維艱。營運商正透過提供合約獎金、模擬器和提前進行自動駕駛測試等方式來應對,但監管方面的延誤阻礙了政府貨運全面採用自動駕駛運輸的進程。

細分市場分析

到了2031年,附加價值服務維持了9.30%的複合年成長率,顯著超過亞太地區交通運輸領域政府和教育物流的整體市場佔有率。 2025年,交通運輸領域仍將佔59.89%的市場佔有率,凸顯了基礎貨運需求的規模。然而,商品化、司機短缺以及日益嚴格的碳排放法規限制了貨運價格上漲的空間,迫使營運商將海關手續、基於區塊鏈的認證和ESG(環境、社會和治理)儀錶板等服務打包在一起。鐵路走廊,特別是印度的專用貨運線路,正在將標準前置作業時間縮短30-40%,並降低對柴油燃料的依賴。空運仍然局限於一些特定領域,例如官方文件和緊急救援物資的運輸,但高價位可以彌補低噸位的損失。海運和內河航運仍然是向島嶼地區運送貨物的關鍵,但燃油風險正在轉移到長期租船人身上。倉儲業正受惠於各項升級改造,這些改造提高了倉儲產業應對氣候變遷的能力,高架貨架和雙電源系統現在已成為泰國和越南的標準配置。

校園內微型倉配中心數量不斷增加,對節省空間、自動化設備以及與學生入口網站的API整合提出了更高的要求。因此,能夠將這些要素整合到一張發票中的供應商可以獲得更高的利潤率並提高客戶留存率。市場領導者透過ISO 27001認證的資料中心、零知識證明加密模組和現場報關服務台來脫穎而出。而那些缺乏網路安全認證的落後貨運代理則面臨被降級為分包商的風險,從而失去定價權和戰略影響力。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 大規模電子政府與智慧基礎設施經濟刺激方案

- 該地區國防採購的擴張(AUKUS、QUAD)正在推動對安全可靠的第三方物流的需求。

- 政府部門和大學透過官民合作關係(PPP)模式開展外包的浪潮

- 強制實施具有氣候適應能力的冗餘倉庫設施,以應對 2023 年洪水造成的破壞。

- 利用區塊鏈技術對教育內容進行認證,以遏制偽造教科書的行為

- 大學校園內提供按需學習工具包的微型倉配中心

- 市場限制因素

- 亞太地區卡車駕駛人老化和短缺問題日益嚴重。

- 燃油額外費用較大,對教育船舶運輸的固定預算造成了沉重負擔。

- 強制採用零知識加密來限制國防貨物的資料可見度。

- ESG一級審計要求增加了中小型承包商的合規成本。

- 波特五力模型

- 價值供應鏈分析

- 產業的技術創新

- 政府法規和政策

- 地緣政治事件對市場的影響

第5章 市場規模與成長預測

- 按服務類型

- 運輸

- 路

- 鐵路

- 航空

- 海路和內河航道

- 倉儲/物流

- 附加價值服務

- 運輸

- 最終用戶

- 中央政府/聯邦政府

- 州和地方政府

- 國防組織

- 公共教育(幼稚園至12年級)

- 高等教育機構

- 其他

- 國家

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 印尼

- 泰國

- 越南

- 馬來西亞

- 其他亞太國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- DHL Supply Chain & Global Forwarding

- Nippon Express Holdings

- Yamato Holdings

- Yusen Logistics

- SF Express(Group)Co., Ltd.

- DSV

- Kuehne+Nagel

- CEVA Logistics

- CJ Logistics

- Kerry Logistics Network

- Sinotrans Limited

- Toll Group

- Sagawa Express

- Gati Ltd

- Allcargo Logistics

- Linfox

- AIT Worldwide Logistics

- Rhenus Logistics

- JD Logistics

- Kintetsu World Express

- Delhivery

第7章 市場機會與未來展望

According to Mordor Intelligence, the asia-Pacific government and education logistics market size is expected to grow from USD 214.84 billion in 2025 to USD 234.67 billion in 2026 and is forecast to reach USD 349.68 billion by 2031 at an 8.30% CAGR over 2026-2031.

The growth path reflects rising defense self-sufficiency, large-scale digital-learning roll-outs, and public-private outsourcing frameworks that are redrawing supply-chain responsibilities across the region. This report is Segmented by Service Type (Transportation, Including Road, Rail, Air, Sea, and More), by End-User (Central/Federal Government, State and Local Government, and More), and by Geography (China, India, Japan, South Korea, Australia, Indonesia, Thailand, Vietnam, Malaysia, and Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Government And Education Logistics Market Trends and Insights

Large-Scale E-Governance & Smart-Infrastructure Stimulus Packages

National digital-government programs are injecting sustained logistics demand by funding hardware roll-outs, cloud-migration projects, and data-center construction. India's Digital India initiative allocated USD 30 billion to digital infrastructure, creating continuous freight flows to 250,000 offices and 1.5 million schools. Indonesia's USD 32 billion Nusantara smart-capital project similarly requires synchronized multi-agency freight coordination. Vietnam's Framework 4.0 mandates cloud-based services throughout ministries by 2027, amplifying the need for secure transportation of critical ICT equipment. Philippine ICT guidelines now score bidders on cybersecurity capacity, pushing third-party providers to certify ISO 27001 systems. Together, these programs provide multi-year visibility for providers but fragment tender cycles across national and provincial entities.

Escalating Regional Defense Procurement (AUKUS, QUAD) Fuelling Secure 3PL Demand

Defense modernization accelerates cargo streams that must meet stringent clearance and chain-of-custody standards. Australia's USD 368 billion AUKUS submarine program demands nuclear-propulsion component logistics that only vetted contractors can perform. The QUAD Supply Chain Resilience Initiative aligns security procedures across Australia, India, Japan, and the United States, creating designated corridors for dual-use items. Japan is lifting defense outlays to 2% of GDP by 2027, triggering new storage and transport needs for ammunition and high-value systems. South Korea's push for indigenous platforms adds reverse-logistics complexity. Providers with existing defense accreditations, therefore, capture premium pricing while newcomers face high entry barriers.

Aging Truck Driver Workforce & Widening Talent Gaps in APAC

Japan reports 47% of drivers above 50, with retirements accelerating capacity shortfalls. Australia recorded 26,000 vacancies in 2024, compounded by defense-security clearance hurdles. South Korea's wages jumped 18% year on year, while Thailand struggles to staff rural routes due to limited vocational schools. Providers respond with signing bonuses, simulators, and early autonomous trials, but regulatory lag slows full driverless deployment for government cargo.

Other drivers and restraints analyzed in the detailed report include:

- Public-Private Partnership Outsourcing Wave Across Ministries & Universities

- Climate-Resilient Redundant Warehousing Mandates After 2023 Flood Disruptions

- Volatile Bunker Fuel Surcharges Stressing Fixed-Budget Education Shipments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Value-added services secured a 9.30% CAGR through 2031, well above the broader Asia-Pacific government and education logistics market share for the transportation sector. In 2025, transportation preserved 59.89% share, underlining the scale of basic freight demand. Yet commoditization, driver shortages, and stricter carbon caps curb rate upside, pushing operators to bundle customs, blockchain stamping, and ESG dashboards. Rail corridors, especially India's dedicated freight routes, trim textbook lead-times by 30-40% and reduce diesel exposure. Air freight remains a niche for official documents and emergency relief, commanding premiums that offset low tonnage. Sea and inland waterways stay critical for archipelagic deliveries, though fuel risk shifts toward long-term charterers. Warehousing gains from climate-resilient upgrades, with elevated racks and dual-power systems now baseline specifications across Thailand and Vietnam.

Micro-fulfillment hubs multiply on campuses, requiring small-footprint automation and API links to student portals. Consequently, providers integrating these components into one invoice realize higher margins and deepen client lock-in. Market leaders differentiate through ISO 27001 data centers, zero-knowledge encryption modules, and on-site customs desks. Lagging freight forwarders that lack cybersecurity credentials risk relegation to subcontract status, losing pricing power and strategic influence.

List of Companies Covered in this Report:

- DHL Supply Chain & Global Forwarding

- Nippon Express Holdings

- Yamato Holdings

- Yusen Logistics

- SF Express (Group) Co., Ltd.

- DSV

- Kuehne + Nagel

- CEVA Logistics

- CJ Logistics

- Kerry Logistics Network

- Sinotrans Limited

- Toll Group

- Sagawa Express

- Gati Ltd

- Allcargo Logistics

- Linfox

- AIT Worldwide Logistics

- Rhenus Logistics

- JD Logistics

- Kintetsu World Express

- Delhivery

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Large-Scale e-Governance & Smart-Infrastructure Stimulus Packages

- 4.2.2 Escalating Regional Defence Procurement (AUKUS, QUAD) Fuelling Secure 3PL Demand

- 4.2.3 Public-Private Partnership (PPP) Outsourcing Wave Across Ministries & Universities

- 4.2.4 Climate-Resilient Redundant Warehousing Mandates after 2023 Flood Disruptions

- 4.2.5 Blockchain Authentication of Educational Content to Curb Counterfeit Textbooks

- 4.2.6 Micro-Fulfilment Hubs on University Campuses for On-Demand Learning Kits

- 4.3 Market Restraints

- 4.3.1 Ageing Truck Driver Workforce & Widening Talent Gaps in APAC

- 4.3.2 Volatile Bunker Fuel Surcharges Stressing Fixed-Budget Education Shipments

- 4.3.3 Mandatory Zero-Knowledge Encryption for Defence Cargo Limiting Data Visibility

- 4.3.4 ESG Tier-1 Audit Requirements Adding Compliance Costs for SME Contractors

- 4.4 Porter's Five Forces

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Competitive Rivalry

- 4.5 Value / Supply-Chain Analysis

- 4.6 Technological Innovations in the Industry

- 4.7 Government Regulations and Policies

- 4.8 Impact of Geopolitical Events on the Market

5 Market Size and Growth Forecasts (Value, USD Billion)

- 5.1 By Service Type

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Rail

- 5.1.1.3 Air

- 5.1.1.4 Sea and Inland Waterway

- 5.1.2 Warehousing and Distribution

- 5.1.3 Value-Added Services

- 5.1.1 Transportation

- 5.2 By End-User

- 5.2.1 Central/Federal Government

- 5.2.2 State and Local Government

- 5.2.3 Defense Agencies

- 5.2.4 Public Education (K-12)

- 5.2.5 Higher Education Institutions

- 5.2.6 Others

- 5.3 By Country

- 5.3.1 China

- 5.3.2 India

- 5.3.3 Japan

- 5.3.4 South Korea

- 5.3.5 Australia

- 5.3.6 Indonesia

- 5.3.7 Thailand

- 5.3.8 Vietnam

- 5.3.9 Malaysia

- 5.3.10 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 DHL Supply Chain & Global Forwarding

- 6.4.2 Nippon Express Holdings

- 6.4.3 Yamato Holdings

- 6.4.4 Yusen Logistics

- 6.4.5 SF Express (Group) Co., Ltd.

- 6.4.6 DSV

- 6.4.7 Kuehne + Nagel

- 6.4.8 CEVA Logistics

- 6.4.9 CJ Logistics

- 6.4.10 Kerry Logistics Network

- 6.4.11 Sinotrans Limited

- 6.4.12 Toll Group

- 6.4.13 Sagawa Express

- 6.4.14 Gati Ltd

- 6.4.15 Allcargo Logistics

- 6.4.16 Linfox

- 6.4.17 AIT Worldwide Logistics

- 6.4.18 Rhenus Logistics

- 6.4.19 JD Logistics

- 6.4.20 Kintetsu World Express

- 6.4.21 Delhivery

7 Market Opportunities and Future Outlook

裝卸整平機市場規模、佔有率和成長分析:按操作方式、核心材料成分、最終用途產業、分銷管道和地區分類-2026-2033年產業預測

裝卸整平機市場規模、佔有率和成長分析:按操作方式、核心材料成分、最終用途產業、分銷管道和地區分類-2026-2033年產業預測 全球物流市場:市場規模、佔有率、趨勢和成長分析(2026-2034)

全球物流市場:市場規模、佔有率、趨勢和成長分析(2026-2034) 2026年全球智慧物流市場報告

2026年全球智慧物流市場報告 智慧物流自動化市場預測至2034年—全球解決方案、運輸方式、組件、技術、應用、最終用戶和區域分析

智慧物流自動化市場預測至2034年—全球解決方案、運輸方式、組件、技術、應用、最終用戶和區域分析 航運和海事資訊通訊技術:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

航運和海事資訊通訊技術:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 2026-2030年全球物流市場按需物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)政府與教育物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

2026-2030年全球物流市場按需物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)政府與教育物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年) 全球資料中心物流市場(2026 年)2026年貨櫃存放場即時定位系統(RTLS)全球市場報告

全球資料中心物流市場(2026 年)2026年貨櫃存放場即時定位系統(RTLS)全球市場報告