|

市場調查報告書

商品編碼

2063257

風力發電機:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Wind Turbine Generator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

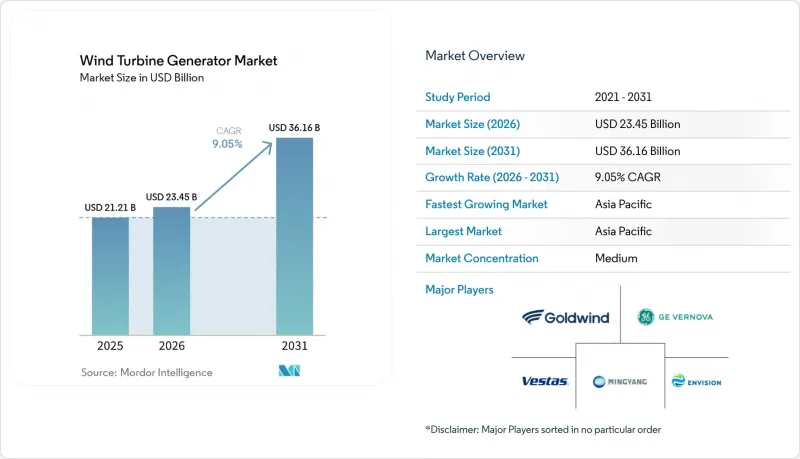

根據 Mordor Intelligence 預測,風力發電機渦輪機市場規模將從 2025 年的 212.1 億美元成長到 2026 年的 234.5 億美元,到 2031 年將達到 361.6 億美元,2026 年至 2031 年的複合年成長率為 9.05%。

本報告按發電機類型(永磁同步發電機、雙饋感應發電機、傳統同步發電機等)、額定輸出功率(小於2MW、2-5MW等)、應用領域(陸上、其他)、最終用戶(公共產業/獨立發電商、工業自用、商業/微電網)和地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。市場預測以美元計價。

全球風力發電機發電機市場趨勢及洞察

PMSG技術成本快速降低

隨著中歐製造商最佳化磁路並擴大自動化繞線生產線,永磁同步發電機(PMSG)系統價格在2024年至2026年初期間下降了22%。 2025年,回收硬碟提供的二次稀土元素供應量增加了4,200噸釹,抑制了先前一年飆升至每公斤160美元的現貨價格。金風科技和明陽科技利用其自有磁鐵工廠,以每兆瓦21萬美元的價格提供PMSG機艙,比歐洲報價低15%,並在2025年獲得了亞太地區68%的訂單。西門子歌美颯5.X平台採用的模組化定子將組裝時間縮短了30%,即使在重型起重機稀缺的市場也能實現直接驅動。隨著海上維修週期延長至18個月以上成為常態,無需昂貴頂升作業的無齒輪傳動PMSG機組正逐漸獲得優勢。

離岸風力發電目標的實現正在推動對直驅系統的需求。

歐盟計畫在2025年安裝22.5吉瓦的離岸風力發電,其中78%將採用額定功率12兆瓦或以上的直驅式永磁同步發電機(PMSG),以滿足其兩年一次的維護計畫。中國已對17兆瓦和20兆瓦的樣機進行了現場測試,消除了導致離岸風力發電停機時間三分之一的變速箱故障模式。維斯塔斯公司已獲得4.2吉瓦V236-15兆瓦機組的訂單,並在北海的一個試點項目中實現了94%的容量係數,比同類雙固定磁場(DFIG)風機高出8個百分點。 Highwind Tampen公司將機艙重量限制在120噸以內,這項標準由採用分段式無鐵芯轉子的緊湊型PMSG機組滿足。新的 IEC 61400-3-2浮體式標準強化了直驅式馬達的發展趨勢,直驅式馬達的旋轉部件更少,扭轉共振的風險更低。

稀土元素供應波動推高了PMSG成本。

受中國對磁合金出口限制的影響,預計到2025年初,釹的價格將上漲至每公斤160美元,將使永磁同步發電機(PMSG)的組件成本增加每兆瓦8萬美元。歐洲和北美超過90%的稀土元素需求依賴進口,這使得專案極易受到外匯波動和政治風險的影響。雖然回收利用提供了一定的緩衝,但去年二次供應僅佔全球磁鐵需求的12%。輕型高溫超導發電機不使用磁體,但其低溫系統成本仍高。在澳洲、加拿大和坦尚尼亞的多個礦場於2028年後全面運作之前,永磁同步發電機價格的不不確定性將給競標預算帶來壓力。

細分市場分析

目前,採用高溫超導性(HTS)單元的風力發電機發電機市場規模較小,但預計到2031年將以15.6%的複合年成長率成長,因為浮體式電開發商致力於將機艙重量控制在每兆瓦8噸以下。截至2025年,雙饋感應發電機(DFIG)系統憑藉其低廉的資本成本和廣泛的服務網路,維持了54.9%的市場佔有率。永磁同步發電機(PMSG)的應用正在迅速擴展,尤其是在容量超過12兆瓦的離岸風力發電機中。這些發電機無需齒輪箱,從而減少了維護需求並延長了檢修週期。傳統同步發電機在系統建置中扮演著較為特殊的角色,而開關磁阻技術仍處於實用化前的階段。

高溫超導(HTS)原型機,例如3.6兆瓦的EcoSwing發電機,實現了每兆瓦11噸的重量比,並通過省去稀土元素磁體,使每台機組的材料成本降低了6.5萬美元。然而,隨著雙饋感應發電機(DFIG)升級以滿足更嚴格的低電壓穿越標準,這種成本優勢正在逐漸消失。在5-10兆瓦功率範圍內,直驅式永磁同步發電機(PMSG)佔據主導地位,其分段式定子設計便於在公共道路上運輸和現場組裝。傳統同步發電機仍用於需要黑啟動功能的微電網,但隨著電池儲能的普及,其優勢正在減弱。開關磁阻發電機的噪音問題(超過80分貝)限制了其在住宅附近的部署,並減緩了其廣泛應用。

2-5兆瓦級機組預計在2025年佔裝置總量的64.5%,並繼續滿足大多數陸上作業現場800噸級移動式起重機的承載能力限制。 5-10兆瓦級機組預計將從2026年起以12.0%的複合年成長率成長,因為改造計劃傾向於選擇單台機組數量較少但單台發電量增加三倍、土建工程量減少一半的機組。由於開發商追求超過50%的產能利用率,去年10兆瓦以上的機組佔海上訂單的14%。

自升降式鑽機近27萬美元的每日平均成本促使人們採用15兆瓦級機組,與三台小型風機相比,此機組可將船舶運作縮短40%。模組化機艙設計使得7兆瓦陸上風機可以透過卡車運輸六個定子段來滿足道路重量法規的要求。颱風多發地區的保險賠償限額為每颱風機1800萬美元,阻礙了東亞地區部署超過15兆瓦的單颱風機。在配電法規限制「用戶側」風電裝置容量為2兆瓦的地區,或因景觀保護原因需要降低輪轂高度的地區,2兆瓦以下的風機仍佔主導地位。

區域分析

亞太地區預計到2025年將佔風力發電機發電機市場收入的42.8%,並預計到2031年將以9.7%的複合年成長率成長。中國每年超過100吉瓦的新增裝置容量以及17兆瓦浮體式機組原型機的投產,鞏固了該地區的主導地位。印度由於快速推進9吉瓦電網升級項目,預計到2025年將新增6.3吉瓦裝置容量,儘管拉賈斯坦邦二期工程仍有訂單積壓。在日本和韓國,為滿足保險公司在颱風導致軸承故障後提出的要求,必須使用T級認證的風力發電機。越南和菲律賓已在易受颶風侵襲的地區簽署了2.8吉瓦的風力發電機項目契約,所有契約均指定使用具備即時狀態監測功能的永磁同步發電機(PMSG)。

在歐洲,根據歐盟再生能源計畫(REPowerEU),已安裝了22.5吉瓦的離岸風力發電,該計畫的目標是到2030年達到120吉瓦。德國已對680兆瓦的陸上風電場進行了改造,在不增加新的電網節點的情況下,使每個站點的兆瓦密度提高了兩倍。英國一項10吉瓦的浮體式海上風電租賃協議規定,機艙質量必須小於每兆瓦8噸,這一標準正在加速高溫超導(HTS)發電機的普及。斯堪的納維亞半島的輸電網聯網線路使得海上剩餘電力得以出口,在完全受風力影響的北海風電場,其容量係數維持在近94%。在法國,布列塔尼和諾曼第正在建造的項目(總裝置容量3.2吉瓦)採用15兆瓦的直驅發電機,以最大限度地減少對景觀的影響。

在北美,儘管併網等待容量高達2600吉瓦,美國仍新增了11.2吉瓦的裝置容量,並寄希望於聯邦能源監管委員會(FERC)2023號指令能在2028年前釋放38吉瓦的容量。加拿大已簽署了2.4吉瓦的裝機契約,主要位於亞伯達和薩斯喀徹爾,這兩個省份的5兆瓦及以上發電機組正在減少維護時間。巴西的828兆瓦Dom Inocencio風電場和阿根廷的230兆瓦Esquina do Vento風電場均已簽署長期購電協議(PPA),利用了40%的容量係數。在中東和非洲,沙烏地阿拉伯的3吉瓦巨型風電場創下了每千瓦時1.33美分的銷售價格紀錄,並選擇了一台7.7兆瓦的永磁同步發電機(PMSG)來應對沙漠高溫。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- PMSG技術成本快速降低

- 離岸風力發電的目標正在推動對大容量直驅風力渦輪機的需求。

- 修訂電網標準,強制引進先進的變速發電機

- 企業購電協議 (PPA) 正在加速公用事業規模電廠的部署。

- 透過電力改造計畫創造維修需求

- 先導計畫浮體式海上發電試點計畫正在推動輕型發電機的設計。

- 市場限制因素

- 稀土元素供應的波動推高了PMSG的成本。

- 輸電網連接延遲

- 由於起重機重量限制,大型陸基設備受到限制。

- 颱風多發地區軸承故障風險增加,導致保險費上漲。

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按生成器類型

- 永磁同步發電機(PMSG)

- 雙饋型感應發電機(DFIG)

- 傳統同步發電機

- 傳統感應發電機

- 開關磁阻發電機

- 按額定容量

- 小於2兆瓦

- 2~5 MW

- 5~10 MW

- 10兆瓦或以上

- 透過使用

- 陸上

- 離岸(固定)

- 浮體式海上

- 最終用戶

- 公共產業及獨立電力生產商(IPP)

- 工業專屬式

- 商業和微電網

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 北歐國家

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Siemens Gamesa Renewable Energy

- Vestas Wind Systems A/S

- GE Vernova

- Nordex Group

- Mitsubishi Heavy Industries

- Suzlon Energy Ltd.

- Enercon GmbH

- Goldwind

- Envision Energy

- Ming Yang Smart Energy

- Dongfang Electric Corporation

- CSIC Haizhuang Wind Power

- Senvion GmbH

- Doosan Enerbility

- Hitachi Ltd.

- ABB Ltd.

- Siemens Energy AG

- Lagerwey(Enercon Group)

- Bergey WindPower Co.

- Inox Wind Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the wind turbine generator market size is expected to grow from USD 21.21 billion in 2025 to USD 23.45 billion in 2026 and is forecast to reach USD 36.16 billion by 2031 at 9.05% CAGR over 2026-2031.

This report is Segmented by Generator Type (PMSG, DFIG, Conventional Synchronous, and More), Capacity Rating (Below 2 MW, 2-5 MW, and More), Application (Onshore, and More), End-User (Utilities & IPPs, Industrial Captive, Commercial & Micro-Grids), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Wind Turbine Generator Market Trends and Insights

Rapid Cost Reductions in PMSG Technology

PMSG system prices fell 22% between 2024 and early 2026 as Chinese and European manufacturers optimized magnet circuits and scaled automated winding lines. Secondary rare-earth supply from recycled hard-disk drives added 4,200 tonnes of neodymium in 2025, softening spot prices that had spiked to USD 160 per kilogram a year earlier . Goldwind and Ming Yang leveraged captive magnet plants to offer PMSG nacelles at USD 210,000 per megawatt, undercutting European quotes by 15% and winning 68% of Asia-Pacific orders in 2025. Modular stators on Siemens Gamesa's 5. X platform trimmed assembly labor 30%, making direct-drive viable in markets that lack heavy-lift cranes . Longer offshore service intervals now exceeding 18 months favor gearless PMSG machines that avoid costly jack-up interventions.

Offshore Wind Targets Boosting Direct-Drive Demand

The European Union installed 22.5 GW offshore in 2025, with 78% using direct-drive PMSGs rated above 12 MW to meet two-year maintenance windows . China field-tested 17 MW and 20 MW prototypes that retired gearbox failure modes responsible for one-third of offshore downtime. Vestas booked 4.2 GW of V236-15 MW orders that achieved 94% capacity factors in North Sea pilots, eight points above comparable DFIG fleets. Hywind Tampen capped nacelle mass at 120 tonnes, a threshold met by compact PMSG units with segmented ironless rotors. New IEC 61400-3-2 floating rules reinforce preference for direct-drive models with fewer rotating parts and lower torsional resonance risk.

Rare-Earth Supply Volatility Inflating PMSG Costs

Neodymium prices climbed to USD 160 per kilogram in early 2025 after export curbs on Chinese magnet alloys, boosting PMSG bills of material by USD 80,000 per megawatt. Europe and North America rely on imports for more than 90% of rare-earth needs, exposing projects to currency swings and political risk. Recycling added a temporary buffer, yet the secondary supply covered only 12% of global magnet demand last year. Lighter High-Temperature Superconducting generators avoid magnets but remain cost-intensive due to cryogenic systems. Until diversified mines in Australia, Canada, and Tanzania are fully commissioned after 2028, PMSG price uncertainty will pressure tender budgets.

Other drivers and restraints analyzed in the detailed report include:

- Grid-Code Revisions Requiring Variable-Speed Operation

- Corporate PPAs Driving Utility-Scale Rollouts

- Transmission Interconnection Delays

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The wind turbine generator market size for High-Temperature Superconducting (HTS) units is small today, yet it will expand at a 15.6% CAGR through 2031 as floating developers chase nacelle mass below 8 tonnes per megawatt. DFIG systems retained 54.9% market share in 2025 thanks to lower capital cost and extensive service networks. The adoption of Permanent Magnet Synchronous Generators (PMSG) is growing rapidly, especially in offshore turbines with capacities exceeding 12 MW. The removal of the gearbox in these turbines reduces maintenance needs and extends service intervals. Conventional synchronous units satisfy niche grid-forming roles, and switched-reluctance concepts remain pre-commercial.

HTS prototypes like the 3.6 MW EcoSwing generator achieved an 11-tonne-per-megawatt ratio and removed rare-earth magnets, cutting material exposure by USD 65,000 per machine. DFIG upgrades are now needed to meet stricter low-voltage ride-through codes, eroding their cost edge. PMSG direct-drive units dominate the 5-10 MW bracket, where segmented stators allow road-legal transport and on-site assembly. Conventional synchronous machines still equip micro-grids that need black-start capability, but batteries are narrowing that advantage. Switched-reluctance noise issues above 80 decibels limit deployment near communities, delaying broader uptake.

The 2 to 5 MW class represented 64.5% of 2025 installations and continues to align with 800-tonne mobile crane limits on most onshore sites. The 5 to 10 MW segment will grow at 12.0% CAGR after 2026 as repowering programs favor fewer units that triple energy output per foundation and cut civil works in half. Machines above 10 MW grabbed 14% of offshore orders last year as developers chase capacity factors beyond 50%.

Jack-up day rates near USD 270,000 incentivize 15 MW units that cut vessel time 40% compared with three smaller turbines. Modular nacelle splits let 7 MW onshore models meet road-weight regulations by trucking six stator sections. Insurance limits in typhoon zones cap coverage at USD 18 million per turbine, which discourages single-unit capacities above 15 MW in East Asia. Sub-2 MW turbines persist where distribution-utility rules cap behind-the-meter wind at 2 MW and where community aesthetics drive demand for lower hub heights.

Geography Analysis

Asia-Pacific held 42.8% of the 2025 wind turbine generator market revenue and is forecast to expand at 9.7% CAGR to 2031. China's >100 GW annual installation run rate and its prototype 17 MW floating units underpin regional leadership. India added 6.3 GW in 2025 after fast-tracking 9 GW of grid upgrades, though a second-tier backlog in Rajasthan persists. Japan and South Korea now mandate Class T certified turbines to satisfy insurers after typhoon-related bearing failures. Vietnam and the Philippines signed 2.8 GW of contracts in cyclone zones, all specifying PMSGs with real-time condition monitoring.

Europe is installing 22.5 GW offshore under the REPowerEU policy that targets 120 GW by 2030. Germany repowered 680 MW of onshore capacity, tripling megawatt density per site without adding new grid nodes. The United Kingdom's 10 GW floating offshore leases stipulate nacelle mass below 8 tonnes per megawatt, a criterion that accelerates HTS generator adoption. Nordic interconnectors enable export of surplus offshore power and sustain capacity factors near 94% on fully exposed North Sea arrays. France advanced 3.2 GW of Brittany and Normandy projects that adopt 15 MW direct-drive machines to minimize visual impact.

In North America, the U.S. added 11.2 GW despite the 2,600 GW interconnection queue and is banking on FERC Order 2023 to unlock 38 GW by 2028. Canada closed 2.4 GW of contracts centered in Alberta and Saskatchewan, where 5 MW-plus machines lower service person-hours. Brazil's 828 MW Dom Inocencio wind farm and Argentina's 230 MW Esquina do Vento leveraged 40% capacity factors to win long-dated PPAs. In the Middle East and Africa, Saudi Arabia's 3 GW mega-farm set a record 1.33 cents per kilowatt-hour tariff and selected 7.7 MW PMSG turbines that withstand desert heat.

- Siemens Gamesa Renewable Energy

- Vestas Wind Systems A/S

- GE Vernova

- Nordex Group

- Mitsubishi Heavy Industries

- Suzlon Energy Ltd.

- Enercon GmbH

- Goldwind

- Envision Energy

- Ming Yang Smart Energy

- Dongfang Electric Corporation

- CSIC Haizhuang Wind Power

- Senvion GmbH

- Doosan Enerbility

- Hitachi Ltd.

- ABB Ltd.

- Siemens Energy AG

- Lagerwey (Enercon Group)

- Bergey WindPower Co.

- Inox Wind Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid cost reductions in PMSG technology

- 4.2.2 Offshore wind targets boosting high-capacity direct-drive demand

- 4.2.3 Grid-code revisions mandating advanced variable-speed generators

- 4.2.4 Corporate PPAs accelerating utility-scale installations

- 4.2.5 Repowering schemes creating retrofit demand

- 4.2.6 Floating offshore pilots driving lightweight generator designs

- 4.3 Market Restraints

- 4.3.1 Rare-earth supply volatility inflating PMSG costs

- 4.3.2 Transmission interconnection delays

- 4.3.3 Crane weight limits restricting large onshore units

- 4.3.4 Insurance premium hikes from bearing-failure risk in typhoon zones

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Generator Type

- 5.1.1 Permanent-Magnet Synchronous Generator (PMSG)

- 5.1.2 Doubly-Fed Induction Generator (DFIG)

- 5.1.3 Conventional Synchronous Generator

- 5.1.4 Conventional Induction Generator

- 5.1.5 Switched Reluctance Generator

- 5.2 By Capacity Rating

- 5.2.1 Below 2 MW

- 5.2.2 2 to 5 MW

- 5.2.3 5 to 10 MW

- 5.2.4 Above 10 MW

- 5.3 By Application

- 5.3.1 Onshore

- 5.3.2 Offshore (Fixed-bottom)

- 5.3.3 Floating Offshore

- 5.4 By End-user

- 5.4.1 Utilities and IPPs

- 5.4.2 Industrial Captive

- 5.4.3 Commercial and Micro-grids

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 NORDIC Countries

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN Countries

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Siemens Gamesa Renewable Energy

- 6.4.2 Vestas Wind Systems A/S

- 6.4.3 GE Vernova

- 6.4.4 Nordex Group

- 6.4.5 Mitsubishi Heavy Industries

- 6.4.6 Suzlon Energy Ltd.

- 6.4.7 Enercon GmbH

- 6.4.8 Goldwind

- 6.4.9 Envision Energy

- 6.4.10 Ming Yang Smart Energy

- 6.4.11 Dongfang Electric Corporation

- 6.4.12 CSIC Haizhuang Wind Power

- 6.4.13 Senvion GmbH

- 6.4.14 Doosan Enerbility

- 6.4.15 Hitachi Ltd.

- 6.4.16 ABB Ltd.

- 6.4.17 Siemens Energy AG

- 6.4.18 Lagerwey (Enercon Group)

- 6.4.19 Bergey WindPower Co.

- 6.4.20 Inox Wind Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

無翼風力渦輪機市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、最終用戶、地區和競爭格局分類,2021-2031年陸域風力發電機葉輪市場-全球產業規模、佔有率、趨勢、機會、預測:依葉片材料、區域和競爭格局分類,2021-2031年風力發電機制動器市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、類型、運作模式、最終用戶、地區和競爭格局分類,2021-2031年風力發電機市場:全球產業規模、市場佔有率、趨勢、機會和預測(按發電機類型、驅動系統、轉速和地區分類)、競爭格局(2021-2031 年)

無翼風力渦輪機市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、最終用戶、地區和競爭格局分類,2021-2031年陸域風力發電機葉輪市場-全球產業規模、佔有率、趨勢、機會、預測:依葉片材料、區域和競爭格局分類,2021-2031年風力發電機制動器市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、類型、運作模式、最終用戶、地區和競爭格局分類,2021-2031年風力發電機市場:全球產業規模、市場佔有率、趨勢、機會和預測(按發電機類型、驅動系統、轉速和地區分類)、競爭格局(2021-2031 年) 南美洲風力發電機:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

南美洲風力發電機:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 風力發電機潤滑油市場預測至2034年-按產品類型、基礎油、渦輪機零件、換油週期、應用和地區分類的全球分析風力發電機鍛件市場預測至2034年:按類型、材質、零件、應用和地區分類的全球分析

風力發電機潤滑油市場預測至2034年-按產品類型、基礎油、渦輪機零件、換油週期、應用和地區分類的全球分析風力發電機鍛件市場預測至2034年:按類型、材質、零件、應用和地區分類的全球分析 風力發電機狀態監測市場分析與預測(至2035年):類型、產品類型、服務、技術、組件、應用、部署狀態、最終用戶、解決方案全球風力發電機市場預測至2034年:按組件、類型、容量、安裝類型、應用、最終用戶和地區分類

風力發電機狀態監測市場分析與預測(至2035年):類型、產品類型、服務、技術、組件、應用、部署狀態、最終用戶、解決方案全球風力發電機市場預測至2034年:按組件、類型、容量、安裝類型、應用、最終用戶和地區分類 風力發電機市場:按類型、組件、功率、安裝、應用和最終用戶分類-2026-2032年全球市場預測

風力發電機市場:按類型、組件、功率、安裝、應用和最終用戶分類-2026-2032年全球市場預測