|

市場調查報告書

商品編碼

2063247

太陽能電池:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)Solar Cell - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

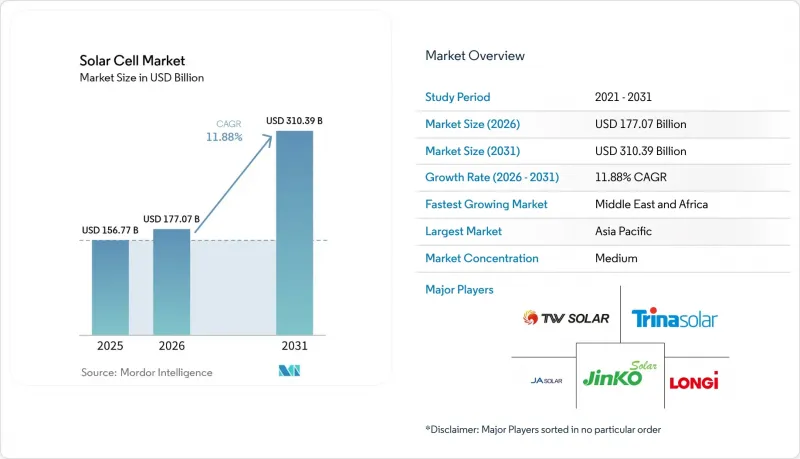

根據 Mordor Intelligence 預測,太陽能電池市場規模預計將在 2025 年達到 1,567.7 億美元,2026 年達到 1,770.7 億美元,到 2031 年達到 3,103.9 億美元,2026 年至 2031 年的複合年成長率為 11.88%。

本報告按類型(晶體矽、其他)、電池技術(P型PERC、N型TOPCon、HJT、IBC、BC、串聯)、應用(住宅、商業、工業、公用事業、浮體式太陽能、家用電子電器、汽車、航太、其他)和地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。市場預測以美元計價。

全球太陽能電池市場趨勢與洞察

降低平均電力成本(LCOE)

2024年,全球公用事業規模太陽能發電的平均平準化度電成本(LCOE)達到每千瓦時0.043美元,中國則為每千瓦時0.033美元,在90%的受訪市場中低於新建燃煤和燃氣電廠的成本。印度2024年的競標價格創下每千瓦時0.026美元的歷史新低,成交容量達3.9吉瓦,這預示著火電峰值負荷將迎來結構性轉折點。巴西2024年的採購價格定為每兆瓦時24美元,顯示太陽能發電也被視為拉丁美洲電網中成本最低的能源。雖然美國計畫的平均成本仍維持在每千瓦時0.070美元,但由於組件價格下降以及追蹤演算法的改進,發電效率的提升正在縮小差距。結合太陽能和儲能的混合系統正在重塑ERCOT和CAISO的容量市場經濟格局,並奪取了曾經由燃氣渦輪機主導的輔助服務收入。

全球脫碳目標與獎勵

美國《通膨降低法案》第45X條規定的稅額扣抵促使國內新增發電裝置容量公告數量激增,達到15吉瓦,這使得First Solar公司將2026年藍圖提高至25吉瓦。歐洲的碳邊境調節機制將高碳進口產品的進口成本提高了每瓦0.02至0.04美元,推動採購轉向本地資源。中國的「十四五」規劃設定了到2030年風能和太陽能發電裝置容量達到1200吉瓦的目標,而印度24億美元的生產連結獎勵計畫計畫(PLI)則鼓勵電池製造商在政府的「合格型號製造商名單」上註冊。海灣國家政府主導的人工智慧資料中心部署計畫正在創造對雙面和低劣化組件的高階需求,這表明政策的應用範圍已擴展到電力市場之外。

由於供應過剩,模組價格暴跌。

2025年,中國多晶矽產量將達277萬噸,而全球需求仍維持在180萬噸,導致現貨矽價格暴跌60%,至每公斤12美元。組件價格也隨之暴跌至每瓦0.10-0.12美元,迫使二級廠商運作了8吉瓦的產能。儘管垂直整合的巨頭企業透過內部價值創造維持了8-10%的EBITDA,但純組裝製造商卻面臨現金流緊張和被迫整合的風險。矛盾的是,此次經濟衰退反而加速了技術創新,企業紛紛投資拓普康(TOPCon)和華聯電子(HJT)等公司,以避免即使在低利潤環境下產品同質化。

細分市場分析

到2025年,晶體矽太陽能電池將佔84.6%的市場佔有率,單晶矽太陽能電池的效率將達到24-25%,晶圓成本將持續下降。 CIGS和非晶質等細分領域目前主要面向建築光伏一體化(BIPV)和輕量化電子產品,在這些領域,柔軟性比降低效率更為重要。

新興太陽能電池技術包括鈣鈦礦太陽能電池、有機光伏電池(OPV)、量子點太陽能電池和染料敏化太陽能電池(DSSC)。雖然晶體矽太陽能電池在2031年之前仍將主導公用事業規模和屋頂光伏裝置,但鈣鈦礦太陽能電池正瞄準高階市場,例如空間受限的商業設施和建築光伏一體化(BIPV)應用。鈣鈦礦組件的IEC 61215認證預計將於2027年獲得通過,為企劃案融資奠定基礎。有機光伏電池目前仍局限於超低功耗應用,量子點電池仍在研發中,而染料敏化太陽能電池則面臨來自高性能鈣鈦礦太陽能電池的競爭。目前,鈣鈦礦組件的IEC 61215認證草案正在製定中,如果獲得批准,將使大規模的企劃案融資資金籌措在2027年之後得以實現。同時,屋頂光伏和建築玻璃的應用將使領先參與企業能夠以更高的價格收回投資,儘管現場可靠性方面仍存在不確定性。

區域分析

2025年,中國擴大了多晶矽和組件生產線,使其總合超過400吉瓦,亞太地區維持了64.3%的銷售佔有率。印度24億美元的生產關聯激勵計畫(PLI)補貼和先進材料管理條例(ALMM)每年引導12吉瓦的訂單流向國內供應商,而日本和韓國則利用其技術優勢,專注於東南亞國協出口。越南和馬來西亞的產能均擴大至5吉瓦,並利用其貿易中立的位置,積極開拓美國和歐盟市場。預計到2031年,亞太太陽能電池市場規模將達2,100億美元。

中東和非洲地區正經歷最快成長,複合年成長率達23.2%,這主要得益於沙烏地阿拉伯NEOM計畫2.6吉瓦的裝置容量分配以及阿拉伯聯合大公國計畫到2030年在穆罕默德·本·拉希德公園實現5吉瓦裝置容量。埃及的本班綜合體和南非的再生能源獨立電力生產商採購計劃(REIPPPP)是多邊融資如何降低主權信用風險並支持重塑該地區負載曲線的大型專案的典型例證。海水淡化和綠色氫能與電網的整合正在推動額外的電力需求,並支持缺水國家太陽能電池市場的擴張。

美國《通貨膨脹控制法案》(IRA)提供的45倍稅額扣抵正在支持超過11吉瓦的美國國內碲化鎘(CdTe)叢集,而歐盟的《淨零排放產業法案》則為30吉瓦的產能遷回歐盟提供資金。加拿大各省正與聯邦政府的稅額扣抵保持一致,逐步淘汰煤炭。巴西的競標在全球範圍內處於較低水平,這表明巴西將成為公用事業規模太陽能發電計畫的新中心。美國《通貨膨脹控制法案》(IRA)提供的45倍稅額扣抵正在助力First Solar實現其到2026年達到25吉瓦產能的目標,此外,俄亥俄州和阿拉巴馬州還將貢獻6吉瓦。歐盟2024年《淨零排放產業法案》已撥款30億歐元,用於到2030年將30吉瓦的產能遷回歐盟,並為Meyer Berger和Enel等公司提供支援。加拿大的 5 吉瓦太陽能發電計畫正在取代燃煤發電廠,而巴西和阿根廷正在擴大其太陽能發電能力,並透過跨境聯網線路向智利出口電力。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 降低平均電力成本(LCOE)

- 全球脫碳目標與獎勵

- 企業清潔能源購電協議數量激增

- n型TOPCon和HJT細胞的商業化

- 鈣鈦礦矽串聯中試生產線(2026年起)

- 強制使用系統互連用逆變器以支援高效能電池

- 市場限制因素

- 由於供應過剩,模組價格暴跌。

- 電網連接瓶頸

- 白銀和銦即將面臨供應緊張局面

- 貿易壁壘(反傾銷/反補貼稅、關稅減讓)的不確定性

- 供應鏈分析

- 原料(多晶矽、銀、玻璃)分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按類型

- 晶體矽太陽能電池

- 單晶矽

- 多晶矽

- 薄膜太陽能電池

- 碲化鎘(CdTe)

- 非晶質(a-Si)

- 銅銦鎵硒(CIGS)

- 新興技術

- 鈣鈦礦太陽能電池

- 有機太陽能電池(OPV)

- 量子點太陽能電池

- 染料敏化太陽能電池(DSSC)

- 晶體矽太陽能電池

- 細胞技術

- P型PERC

- n型TOPCon

- 雜合子(HJT)

- 叉指背接觸(IBC)

- 背部接觸(BC)

- 串聯(鈣鈦礦-矽,III-V族)

- 透過使用

- 住宅- 屋頂

- 商業

- 產業

- 地面安裝公用設施

- 浮體式太陽能發電

- 家用電子產品

- 汽車和運輸業

- 航太/國防

- 其他(農光互補、穿戴裝置、離網等)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 北歐國家

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- LONGi Green Energy Technology Co., Ltd.

- Tongwei Solar Co., Ltd.

- JA Solar Technology Co., Ltd.

- Trina Solar Co., Ltd.

- JinkoSolar Holding Co., Ltd.

- First Solar, Inc.

- Canadian Solar Inc.

- Hanwha Q CELLS Co., Ltd.

- Risen Energy Co., Ltd.

- SunPower Corporation

- Maxeon Solar Technologies

- REC Group

- Yingli Green Energy Holding Co. Ltd.

- Panasonic Holdings Corporation

- Sharp Corporation

- Aiko Solar(Jiangxi)Co., Ltd.

- Runergy(Jiangsu)Co., Ltd.

- Astronergy(Chint)

- Huasun Energy Co., Ltd.

- Meyer Burger Technology AG

- Oxford PV Ltd.

- Heliatek GmbH

- Solaria Corporation

- Suntech Power Co., Ltd.

- Emeren Group Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the solar cell market size is projected to be USD 156.77 billion in 2025, USD 177.07 billion in 2026, and reach USD 310.39 billion by 2031, growing at a CAGR of 11.88% from 2026 to 2031.

This report is Segmented by Type (Crystalline-Silicon, Others), Cell Technology (P-Type PERC, N-Type TOPCon, HJT, IBC, BC, Tandem), Application (Residential, Commercial, Industrial, Utility, Floating PV, Consumer Electronics, Automotive, Aerospace, Others), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Solar Cell Market Trends and Insights

Declining Levelized Cost of Electricity (LCOE)

Utility solar reached a global average LCOE of USD 0.043 kWh in 2024, with China at USD 0.033 kWh, undercutting new coal and gas in 90% of tracked markets. Record-low tariffs of USD 0.026 kWh were achieved for 3.9 GW of Indian capacity in 2024 auctions, signaling a structural reset for thermal peaker plants. In Brazil, 2024 procurements cleared at USD 24 MWh, proving Latin American grids also view solar as the least-cost supply. U.S. projects still average USD 0.070 kWh, yet the gap is narrowing as module prices fall and tracker algorithms boost specific yield. Solar-plus-storage hybrids now capture ancillary-service income once reserved for combustion turbines, redefining capacity-market economics in ERCOT and CAISO.

Global Decarbonization Targets and Incentives

The U.S. Inflation Reduction Act's Section 45X credits triggered 15 GW of new domestic capacity announcements, lifting First Solar's roadmap to 25 GW by 2026. Europe's Carbon Border Adjustment Mechanism raises the landed cost of high-carbon imports by USD 0.02-0.04 W, redirecting procurement toward regional lines. China's 14th Five-Year Plan locks in 1,200 GW of wind and solar by 2030, while India's USD 2.4 billion PLI incentives push cell makers onto the government's Approved List of Models and Manufacturers. Sovereign AI-datacenter mandates in the Gulf add premium demand for bifacial and low-degradation modules, illustrating the policy's widening scope beyond power markets.

Oversupply-Driven Module Price Crash

China's polysilicon output rose to 2.77 million tonnes in 2025, versus global demand of 1.8 million tonnes, causing spot silicon prices 60% to USD 12 kg. Module prices followed, touching USD 0.10-0.12 W and pushing eight gigawatts of tier-2 capacity offline. Vertically integrated giants preserve 8-10% EBITDA by internalizing value capture, whereas pure-play assemblers see cash-flow stress and potential forced consolidation. The downturn is paradoxically accelerating technology upgrades, as firms invest in TOPCon and HJT to escape commoditization even while margins remain thin.

Other drivers and restraints analyzed in the detailed report include:

- Corporate Clean-Energy PPAs Boom

- Commercialization of N-Type TOPCon & HJT Cells

- Grid-Connection Bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Crystalline-silicon designs controlled 84.6% of the solar cell market in 2025, with monocrystalline variants delivering 24-25% efficiencies and falling wafer costs. Niche avenues such as CIGS and amorphous silicon now target BIPV or lightweight electronics where flexibility overshadows efficiency sacrifice.

Emerging solar technologies include perovskite, organic photovoltaic (OPV), quantum-dot, and dye-sensitized solar cells (DSSC). Crystalline silicon will dominate utility-scale and rooftop installations through 2031, while perovskite tandems target premium segments like space-constrained commercial and BIPV applications. IEC 61215 certification for perovskite modules is expected by 2027, enabling project financing. OPVs remain limited to ultra-low-power uses, quantum-dot cells are in development, and DSSCs face competition from higher-performing perovskites. IEC 61215 certification drafts for perovskite modules are in process, and approval could unlock larger project-finance pools post-2027. In the interim, rooftop and architectural-glass applications allow early movers to recoup higher price points despite field-reliability unknowns.

Geography Analysis

Asia-Pacific retained 64.3% revenue share in 2025 as China ramped polysilicon and module lines exceeding 400 GW of combined capacity. India's USD 2.4 billion PLI subsidies and ALMM rules rerouted 12 GW of annual orders to domestic suppliers, while Japan and South Korea leveraged technology leadership to serve ASEAN imports. Vietnam and Malaysia expanded output to 5 GW each, using trade-neutral positioning to reach U.S. and EU buyers. The solar cell market size across Asia-Pacific is projected to reach USD 210 billion by 2031.

The Middle East and Africa post the fastest growth at 23.2% CAGR, anchored by Saudi Arabia's 2.6 GW NEOM allocation and the UAE's march to 5 GW at its Mohammed bin Rashid park by 2030. Egypt's Benban complex and South Africa's REIPPPP illustrate how multilateral finance de-risks sovereign credit, unlocking scale projects that reshape regional load curves. Grid-integrated desalination and green hydrogen drive additional off-take, supporting a widening solar cell market in water-stressed states.

The U.S. IRA's 45X credit supports a domestic CdTe cluster exceeding 11 GW, while the EU's Net-Zero Industry Act funds 30 GW of reshored capacity. Canadian provinces align with federal tax credits to phase out coal, and Brazil's auctions clear at world-class low tariffs, signaling new poles of utility-scale buildout. The U.S. Inflation Reduction Act's 45X credit drives First Solar's 25 GW capacity target by 2026, with 6 GW added in Ohio and Alabama. The EU's 2024 Net-Zero Industry Act allocates EUR 3 billion to reshore 30 GW by 2030, aiding Meyer Burger and Enel. Canada's 5 GW solar pipeline replaces coal, while Brazil and Argentina expand solar capacity, exporting electricity to Chile via cross-border interconnections.

- LONGi Green Energy Technology Co., Ltd.

- Tongwei Solar Co., Ltd.

- JA Solar Technology Co., Ltd.

- Trina Solar Co., Ltd.

- JinkoSolar Holding Co., Ltd.

- First Solar, Inc.

- Canadian Solar Inc.

- Hanwha Q CELLS Co., Ltd.

- Risen Energy Co., Ltd.

- SunPower Corporation

- Maxeon Solar Technologies

- REC Group

- Yingli Green Energy Holding Co. Ltd.

- Panasonic Holdings Corporation

- Sharp Corporation

- Aiko Solar (Jiangxi) Co., Ltd.

- Runergy (Jiangsu) Co., Ltd.

- Astronergy (Chint)

- Huasun Energy Co., Ltd.

- Meyer Burger Technology AG

- Oxford PV Ltd.

- Heliatek GmbH

- Solaria Corporation

- Suntech Power Co., Ltd.

- Emeren Group Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Declining levelised cost of electricity (LCOE)

- 4.2.2 Global decarbonisation targets & incentives

- 4.2.3 Corporate clean-energy PPAs boom

- 4.2.4 Commercialisation of n-type TOPCon & HJT cells

- 4.2.5 Perovskite-silicon tandem pilot lines (2026+)

- 4.2.6 Grid-forming-inverter mandates favouring high-efficiency cells

- 4.3 Market Restraints

- 4.3.1 Oversupply-driven module price crash

- 4.3.2 Grid-connection bottlenecks

- 4.3.3 Looming silver & indium supply constraints

- 4.3.4 Trade-barrier uncertainty (AD/CVD, CBAM)

- 4.4 Supply-Chain Analysis

- 4.5 Raw-Material (Polysilicon, Silver, Glass) Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Crystalline-Silicon Solar Cells

- 5.1.1.1 Monocrystalline Silicon

- 5.1.1.2 Polycrystalline Silicon

- 5.1.2 Thin-Film Solar Cells

- 5.1.2.1 Cadmium Telluride (CdTe)

- 5.1.2.2 Amorphous Silicon (a-Si)

- 5.1.2.3 Copper Indium Gallium Selenide (CIGS)

- 5.1.3 Emerging Technologies

- 5.1.3.1 Perovskite Solar Cells

- 5.1.3.2 Organic Photovoltaic (OPV) Cells

- 5.1.3.3 Quantum-Dot Solar Cells

- 5.1.3.4 Dye-Sensitised Solar Cells (DSSC)

- 5.1.1 Crystalline-Silicon Solar Cells

- 5.2 By Cell Technology

- 5.2.1 P-type PERC

- 5.2.2 n-type TOPCon

- 5.2.3 Heterojunction (HJT)

- 5.2.4 Interdigitated Back-Contact (IBC)

- 5.2.5 Back-Contact (BC)

- 5.2.6 Tandem (Perovskite-Si, III-V)

- 5.3 By Application

- 5.3.1 Residential - Rooftop

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.3.4 Ground-Mounted Utility

- 5.3.5 Floating PV

- 5.3.6 Consumer Electronics

- 5.3.7 Automotive and Transportation

- 5.3.8 Aerospace and Defense

- 5.3.9 Others (Agrivoltaic, Wearables, Off-grid, etc.)

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 NORDIC Countries

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 ASEAN Countries

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 LONGi Green Energy Technology Co., Ltd.

- 6.4.2 Tongwei Solar Co., Ltd.

- 6.4.3 JA Solar Technology Co., Ltd.

- 6.4.4 Trina Solar Co., Ltd.

- 6.4.5 JinkoSolar Holding Co., Ltd.

- 6.4.6 First Solar, Inc.

- 6.4.7 Canadian Solar Inc.

- 6.4.8 Hanwha Q CELLS Co., Ltd.

- 6.4.9 Risen Energy Co., Ltd.

- 6.4.10 SunPower Corporation

- 6.4.11 Maxeon Solar Technologies

- 6.4.12 REC Group

- 6.4.13 Yingli Green Energy Holding Co. Ltd.

- 6.4.14 Panasonic Holdings Corporation

- 6.4.15 Sharp Corporation

- 6.4.16 Aiko Solar (Jiangxi) Co., Ltd.

- 6.4.17 Runergy (Jiangsu) Co., Ltd.

- 6.4.18 Astronergy (Chint)

- 6.4.19 Huasun Energy Co., Ltd.

- 6.4.20 Meyer Burger Technology AG

- 6.4.21 Oxford PV Ltd.

- 6.4.22 Heliatek GmbH

- 6.4.23 Solaria Corporation

- 6.4.24 Suntech Power Co., Ltd.

- 6.4.25 Emeren Group Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

串聯太陽能電池市場預測至2034年—按電池結構、效率範圍、技術、應用、最終用戶和地區分類的全球分析有機太陽能電池(OPV)市場預測—全球材料、裝置結構、應用、終端用戶和地區分析—2034年

串聯太陽能電池市場預測至2034年—按電池結構、效率範圍、技術、應用、最終用戶和地區分類的全球分析有機太陽能電池(OPV)市場預測—全球材料、裝置結構、應用、終端用戶和地區分析—2034年 下一代太陽能電池市場規模、佔有率和成長分析:按技術、材料、應用、安裝類型、最終用戶、組件和地區分類-2026-2033年產業預測

下一代太陽能電池市場規模、佔有率和成長分析:按技術、材料、應用、安裝類型、最終用戶、組件和地區分類-2026-2033年產業預測 拓普康太陽能電池市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、安裝方式、最終用戶、地區和競爭格局分類,2021-2031年雙層異質結有機太陽能電池市場-全球產業規模、佔有率、趨勢、機會、預測:按材料、應用、實體尺寸、最終用戶、地區和競爭格局分類,2021-2031年

拓普康太陽能電池市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、安裝方式、最終用戶、地區和競爭格局分類,2021-2031年雙層異質結有機太陽能電池市場-全球產業規模、佔有率、趨勢、機會、預測:按材料、應用、實體尺寸、最終用戶、地區和競爭格局分類,2021-2031年 全球串聯太陽能電池市場(至2040年):按技術、結構、應用、地區、主要參與者、產業趨勢和預測分類生物混合機器人市場:產業趨勢與全球市場預測(至2035年)

全球串聯太陽能電池市場(至2040年):按技術、結構、應用、地區、主要參與者、產業趨勢和預測分類生物混合機器人市場:產業趨勢與全球市場預測(至2035年) 太陽能電池市場:全球市場按技術、安裝類型、應用和最終用戶分類的預測——2026-2032年下一代太陽能電池市場:按技術、材料、安裝類型和應用分類-2026-2032年全球市場預測

太陽能電池市場:全球市場按技術、安裝類型、應用和最終用戶分類的預測——2026-2032年下一代太陽能電池市場:按技術、材料、安裝類型和應用分類-2026-2032年全球市場預測 拓普康太陽能電池市場:按類型、安裝方式、應用和地區分類

拓普康太陽能電池市場:按類型、安裝方式、應用和地區分類