|

市場調查報告書

商品編碼

2062454

播出自動化 CiaB:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Playout Automation And Channel-In-A-Box - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

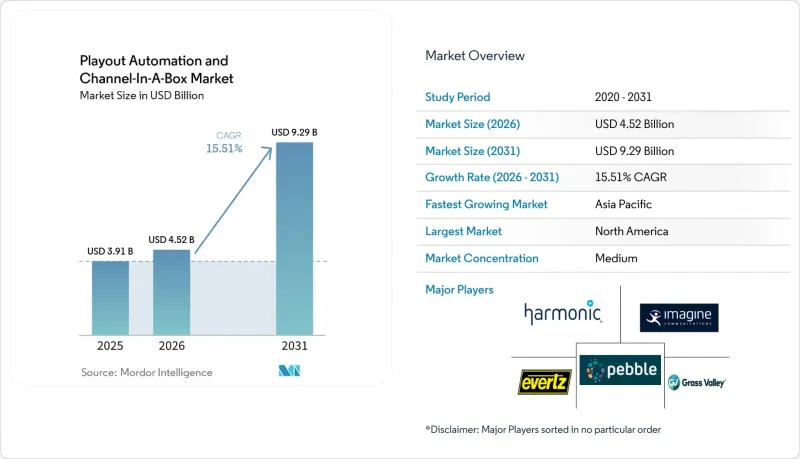

根據 Mordor Intelligence 預測,播出自動化和 CiaB 市場將從 2025 年的 39.1 億美元和 2026 年的 45.2 億美元成長到 2031 年的 92.9 億美元,2026 年至 2031 年的複合年成長率為 15.51%。

本報告按組件(硬體、軟體、服務)、部署模式(本地部署、雲端部署、混合部署)、最終用戶產業(地面電波和衛星廣播公司、有線電視網路營運商、OTT/串流平台等)、通道類型(單通道自動化、多通道自動化)和地區進行細分。市場預測以美元計價。

全球播出自動化與CiaB市場趨勢及洞察

向基於 IP 的播出基礎設施遷移

廣播公司正逐步淘汰SDI主控室,轉而採用SMPTE ST 2110 IP工作流程,以實現遠端製作、靈活路由以及應對大規模活動的雲端突發傳輸能力。 PBS在其連接170多家廣播公司的整個MPLS骨幹網路上,用Ateme TITAN Edge取代了衛星鏈路,從而降低了50%的傳輸成本,並為ATSC 3.0在該地區推廣鋪平了道路。 BBC世界服務使用Encompass Altitude Connect和Zixi傳輸完成了IP遷移,向全球廣播電視合作夥伴證明了其可靠性。雖然IP路由減少了佈線和硬體,但封包遺失管理和幀完美同步對於體育賽事轉播仍然至關重要,而亞太地區的人員短缺正在延緩IP的全面應用。

OTT和FAST頻道激增

隨著廣告商轉向程式化廣告位,觀眾也越來越傾向廣告支援的串流服務,OTT和FAST服務供應商正經歷最快的成長。 Amagi在其CLOUDPORT平台上實現了21%的影片觀看長度同比成長,其中大部分成長來自新推出的FAST頻道。 AIS PLAY透過新增六台PlayBox Neo「盒中頻道」設備,使其泰國足球聯賽的轉播量加倍,凸顯了該地區對低成本、快速推出的需求。雲端播放節省了50萬美元的硬體成本,並允許創建季節性的臨時頻道,但由於各地廣告揭露規則的差異,合規性問題也隨之而來。

硬體升級需要較高的初始資金投入。

小規模的廣播公司難以籌集約50萬美元的主控系統升級資金,這延緩了IP技術的普及,並使其成長率下降了2.1個百分點。儘管雲端模式採用付費使用制,但轉型仍需要網路升級和平行營運。當德國天空電視台(Sky Deutschland)將沃達豐的有線電視分發系統遷移到IP時,用Sky Q硬體替換機上盒的高昂成本凸顯了下游流程資本支出所受到的影響。

細分市場分析

到2025年,服務業將以16.11%的複合年成長率(CAGR)實現最高成長,而硬體產業則佔據播出自動化和內容整合與廣播(CiaB)市場最大的佔有率,達到45.89%。託管播出服務提供者整合了內容創作、編碼、監控和分發,使內容擁有者無需在控制室安排人員24小時值守。康卡斯特技術解決方案公司展示了集中監控如何透過將多個客戶訊號整合到單一的IP廣播營運中心來降低人員和設施成本。在資料主權受到嚴格限制的市場中,硬體仍然至關重要,因為本地部署的設備可以滿足小型資料庫需求。基於訂閱的軟體維護模式將一次性資本支出轉化為經常性收入,使供應商能夠穩定現金流並持續提供功能更新。在整個預測期內,隨著廣播公司將資本支出轉向內容獲取而非基礎設施維護,播出自動化和CiaB市場的服務規模將不斷擴大。

對整合支援合約的需求也推動了業務收益的成長,PlayBox Neo 的全天候應用支援管理 (ASM) 和技術服務 (TS) 計劃確保了軟體升級和遠端故障排除。在北美和歐洲,成熟的生態系統優先考慮可預測的營運成本 (OPEX),從而推動了產品的普及。同時,在亞太和中東地區,硬體導向仍然強勁,但頻寬和延遲仍然是體育賽事直播面臨的挑戰。一種將現場採集硬體與雲端協作編排相結合的混合方案正在興起,成為一種過渡橋樑,有助於加強與供應商的關係,並確保多年服務等級協定 (SLA) 的收入來源。

隨著廣播公司優先考慮加快產品上市速度和提高擴展靈活性,預計到 2025 年,雲端服務將佔其收入的 41.36%,年平均成長率達 16.17%。 Amagi CLOUDPORT 提供多區域冗餘、AES-128 加密和基於角色的存取控制,使客戶能夠在幾天內建立全球高速網路。隨著廣播公司無需部署新的本地硬體即可提供季節性快訊或添加語言版本,雲端服務在播出自動化和內容整合與廣播 (CiaB) 市場的佔有率正在不斷擴大。混合模式仍然很受歡迎,因為它們透過在本地保持常規播出,並在大型會議期間將流量激增至 AWS 或 Azure,從而平衡了延遲和可擴展性。

在受主權法律約束的國內網路以及依賴衛星基礎設施 (SDI) 進行分發的網路中,本地部署系統仍然發揮著至關重要的作用。 Arqiva 提供多種部署選項,從單一區域雲端到客戶自有的租用戶環境,使工程師能夠精確控制地理容錯移轉。儘管網路安全風險正在削弱人們對雲端運算的熱情,但供應商正透過符合 ISO 27001 標準和即時威脅監控來應對這項挑戰。隨著網路骨幹網路容量的提升,雲端運算的成本效益將不斷提高,預計到 2031 年,其市場佔有率將超過本地部署解決方案。

區域分析

北美在2025年仍維持32.84%的市場佔有率,這得益於SMPTE ST 2110標準的早期應用以及強大的託管服務生態系統。 PBS透過向地面電波IP分發轉型,將衛星通訊成本降低了50%,證明了公共廣播公司的商業性可行性。康卡斯特的Dry Creek Hub集中了廣播和串流媒體品牌的播出,凸顯了規模經濟效益。儘管由於遍遠地區頻寬有限,加拿大和墨西哥的普及速度較慢,但兩國都利用了位於美國的跨境服務站。 FCC強制要求ATSC 1.0和3.0並行輸出的規定,正在推動對支援多標準播放的「頻道一體機」設備的需求。

亞太地區以16.51%的複合年成長率領先。印度、日本和東南亞正在從SDI轉向IP,以滿足本地語言的傳輸需求,而OTT業者則努力吸引行動優先的消費者。紐西蘭天空電視台部署AMPP技術凸顯了混合雲端的強勁發展勢頭。泰國AIS PLAY透過PlayBox Neo設備將其體育頻道數量加倍,反映出本地廣播權協議正在推動容量的成長。日本嚴格的ARIB UHD標準正在加速硬體更新換代,而中國和印度則是出於主權原因依賴本地部署設備。韓國和澳洲則透過在正常情況下進行本地播出,並在實況活動時將內容快速上傳至雲端,以平衡成本和效能。

在歐洲,雖然普及網路存取是公共服務義務,但預算限制促使工程師們轉向IP技術以降低衛星和有線電視的成本,從而推動了IP技術的穩定發展。 BBC世界服務已在歐洲全面完成IP轉型,德國天空電視台也已將沃達豐有線電視用戶遷移到IPTV,在增加互動功能的同時降低了前端費用。瑞典BoxerTV退出地面電波廣播活性化了關於地面電波頻段價值的討論,促使政策制定者支持OTT(網路電視)服務。在南美、中東和非洲,由於網路連線和進口關稅的差異,IPTV的普及速度較為緩慢,但託管服務供應商正透過營運成本(OPEX)模式吸引廣播公司,將資本支出(CAPEX)轉化為訂閱費,IPTV的普及正在逐步推進。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 向基於 IP 的播出基礎設施遷移

- OTT和FAST頻道的普及

- 對具有成本效益的多通路營運的需求

- 推動高清和超高清廣播的監管

- 在播出鏈中引入基於機器學習的自動化品管(QC)

- 災害復原對臨時通路的需求日益成長

- 市場限制因素

- 硬體升級需要大量初始投資

- 與傳統自動化系統進行複雜整合

- SMPTE ST 2110 工作流程的技能短缺

- 基於雲端的播放中的網路安全問題

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 硬體

- 軟體

- 服務

- 按部署模式

- 現場

- 雲

- 混合

- 按最終用戶行業分類

- 地面電波和衛星廣播公司

- 有線電視網路營運商

- OTT/串流平台

- 其他終端用戶產業

- 按頻道類型

- 單通道自動化

- 多通道自動化

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Grass Valley Canada Holdings Limited

- Imagine Communications Corp.

- Harmonic Inc.

- Evertz Microsystems Ltd.

- Pebble Beach Systems Group plc

- Dalet SA

- PlayBox Neo Ltd.

- BroadStream Solutions Inc.

- Florical Systems, Inc.

- Aveco sro

- Cinegy GmbH

- Rohde and Schwarz GmbH and Co KG

- Ross Video Ltd.

- Amagi Corporation

- Hexaglobe SAS(SGT)

- Pixel Power Ltd.

- ENCO Systems Inc.

- Switch Media Pty Ltd.

- Logitek Electronic Systems Inc.

- Crispin Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the playout automation and channel-in-a-box market size is projected to expand from USD 3.91 billion in 2025 and USD 4.52 billion in 2026 to USD 9.29 billion by 2031, registering a 15.51% CAGR between 2026 and 2031.

This report is Segmented by Component (Hardware, Software, and Services), Deployment Model (On-Premise, Cloud, and Hybrid), End-User Industry (Terrestrial and Satellite Broadcasters, Cable Network Operators, OTT/Streaming Platforms, and More), Channel Type (Single-Channel Automation, and Multi-Channel Automation), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Playout Automation And Channel-In-A-Box Market Trends and Insights

Shift Toward IP-Based Playout Infrastructure

Broadcasters are retiring SDI master-control rooms in favor of SMPTE ST 2110 IP workflows that enable remote production, flexible routing, and cloud-burst capacity for major events. PBS replaced satellite links with Ateme TITAN Edge across its MPLS backbone connecting more than 170 stations, reducing distribution cost by 50% and paving the way for ATSC 3.0 regional rollout. BBC World Service completed an IP migration using Encompass Altitude Connect with Zixi transport, proving reliability for global radio and TV partners. While IP routing trims cabling and hardware, packet loss management and frame-accurate sync remain critical for live sports, and skill shortages in Asia-Pacific delay full adoption.

Proliferation of OTT and FAST Channels

OTT and FAST operators expand quickest as advertisers pivot to programmatic inventory and viewers favor ad-supported streaming. Amagi processed 21% more video hours year over year on its CLOUDPORT platform, with most new channels classed as FAST. AIS PLAY doubled Thai League football feeds after adding six PlayBox Neo channel-in-a-box units, underscoring regional demand for low-cost rapid launch. Cloud playout eliminates USD 500 000 hardware spends and allows seasonal pop-up channels, though fragmented advertising-disclosure rules create compliance complexity across jurisdictions.

High Upfront Capital Expenditure for Hardware Refresh

Smaller broadcasters struggle to finance USD 500 000 master-control overhauls, delaying IP adoption and subtracting 2.1 percentage points from growth. Although cloud models offer pay-as-you-go pricing, migration still incurs network upgrades and dual-run periods. Sky Deutschland's shift of Vodafone cable feeds to IP required costly set-top box swaps to Sky Q hardware, demonstrating downstream capital impacts.

Other drivers and restraints analyzed in the detailed report include:

- Need for Cost-Effective Multi-Channel Operations

- Regulatory Push Toward HD and UHD Broadcasting

- Complex Integration with Legacy Automation Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services recorded the fastest 16.11% CAGR while hardware held the largest 45.89% share of the playout automation and channel-in-a-box market in 2025. Managed playout providers bundle origination, encoding, monitoring, and distribution so content owners avoid staffing 24-hour control rooms. Comcast Technology Solutions consolidated multiple client feeds into a single IP Broadcast Operations Center, illustrating how centralized oversight trims personnel and facility expense. Hardware remains critical in markets enforcing data-sovereignty, where on-premise appliances satisfy local storage mandates. Subscription-based software maintenance converts one-time capital sales into recurring revenue, letting vendors smooth cash flow and continuously push feature updates. Over the forecast period, the playout automation and channel-in-a-box market size for services is widening as broadcasters reallocate capex toward content acquisition rather than infrastructure upkeep.

Demand for integrated support contracts also lifts service revenue, with PlayBox Neo's 24-hour ASM and TS programs guaranteeing software upgrades and remote troubleshooting. North America and Europe drive adoption because mature ecosystems value predictable opex. Asia-Pacific and the Middle East lean toward hardware while wide-area bandwidth and latency remain concerns for live sports. Hybrid engagements that place ingest hardware on site but route schedules to cloud orchestration are emerging as a transitional bridge, anchoring vendor relationships and locking in multiyear SLA revenue streams.

Cloud captured 41.36% revenue in 2025, growing 16.17% annually as broadcasters prioritize time-to-market and elastic scaling. Amagi CLOUDPORT provisions multi-region redundancy with AES-128 encryption and role-based permissions, allowing clients to stand up global FAST networks in days. The playout automation and channel-in-a-box market share for cloud rises when operators spin seasonal pop-up feeds or add language variants without new on-premise hardware. Hybrid models remain popular where baseline playout stays local but surges burst to AWS or Azure during major tournaments, balancing latency and scalability.

On-premise systems stay relevant for national networks bound by sovereignty laws or reliant on SDI contribution. Arqiva offers deployment choices from single-region cloud to customer-owned tenancy, giving engineers precise control over geographic failover. Cybersecurity risk tempers cloud enthusiasm, but vendors respond with ISO 27001 compliance and real-time threat monitoring. As internet backbone capacity improves, cloud's unit economics strengthen, positioning it to eclipse on-premise share before 2031.

Geography Analysis

North America retained 32.84% market share in 2025, supported by early SMPTE ST 2110 adoption and robust managed-service ecosystems. PBS's conversion to IP terrestrial distribution cut satellite spend by 50%, proving commercial viability for public broadcasters. Comcast's Dry Creek hub centralizes playout for broadcast and streaming brands, highlighting scale economics. Canadian and Mexican uptake is slower due to rural bandwidth gaps, yet both leverage cross-border service bureaus housed in the United States. FCC rules mandating parallel ATSC 1.0 and 3.0 outputs elevate demand for channel-in-a-box appliances capable of multi-standard playout.

Asia-Pacific records the fastest 16.51% CAGR. India, Japan, and Southeast Asia replace SDI with IP to support regional language feeds, while OTT operators chase mobile-first consumers. Sky New Zealand's AMPP deployment underscores hybrid cloud momentum. Thailand's AIS PLAY doubled sports channels via PlayBox Neo appliances, reflecting how local rights deals drive incremental capacity. Japan's stringent ARIB UHD specifications quicken hardware refresh cycles, whereas China and India lean on on-premise gear for sovereignty reasons. South Korea and Australia run baseline playout locally then burst to cloud during live events, balancing cost and performance.

Europe demonstrates steady growth as public-service mandates require universal access yet budgets push engineers toward IP to curtail satellite and cable costs. BBC World Service completed a full IP handoff across the continent, and Sky Deutschland shifted Vodafone cable customers to IPTV, reducing head-end fees while adding interactive features. Sweden's BoxerTV exit from DTT catalyzes debate over terrestrial spectrum value, nudging policymakers toward OTT support. South America, the Middle East, and Africa trail due to connectivity gaps and import tariffs, but managed-service vendors entice broadcasters with opex models that convert capex into subscription fees, stimulating gradual adoption.

- Grass Valley Canada Holdings Limited

- Imagine Communications Corp.

- Harmonic Inc.

- Evertz Microsystems Ltd.

- Pebble Beach Systems Group plc

- Dalet S.A.

- PlayBox Neo Ltd.

- BroadStream Solutions Inc.

- Florical Systems, Inc.

- Aveco s.r.o.

- Cinegy GmbH

- Rohde and Schwarz GmbH and Co KG

- Ross Video Ltd.

- Amagi Corporation

- Hexaglobe SAS (SGT)

- Pixel Power Ltd.

- ENCO Systems Inc.

- Switch Media Pty Ltd.

- Logitek Electronic Systems Inc.

- Crispin Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift Toward IP-Based Playout Infrastructure

- 4.2.2 Proliferation of OTT and FAST Channels

- 4.2.3 Need for Cost-Effective Multi-Channel Operations

- 4.2.4 Regulatory Push Toward HD and UHD Broadcasting

- 4.2.5 Adoption of ML-Driven Automated QC in Playout Chains

- 4.2.6 Rising Demand for Disaster-Recovery Pop-Up Channels

- 4.3 Market Restraints

- 4.3.1 High Upfront Capital Expenditure for Hardware Refresh

- 4.3.2 Complex Integration with Legacy Automation Systems

- 4.3.3 Skill Shortage in SMPTE ST 2110 Workflows

- 4.3.4 Cybersecurity Concerns for Cloud-Based Playout

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Deployment Model

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.3 By End-user Industry

- 5.3.1 Terrestrial and Satellite Broadcasters

- 5.3.2 Cable Network Operators

- 5.3.3 OTT / Streaming Platforms

- 5.3.4 Other End-User Inudustries

- 5.4 By Channel Type

- 5.4.1 Single-Channel Automation

- 5.4.2 Multi-Channel Automation

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Grass Valley Canada Holdings Limited

- 6.4.2 Imagine Communications Corp.

- 6.4.3 Harmonic Inc.

- 6.4.4 Evertz Microsystems Ltd.

- 6.4.5 Pebble Beach Systems Group plc

- 6.4.6 Dalet S.A.

- 6.4.7 PlayBox Neo Ltd.

- 6.4.8 BroadStream Solutions Inc.

- 6.4.9 Florical Systems, Inc.

- 6.4.10 Aveco s.r.o.

- 6.4.11 Cinegy GmbH

- 6.4.12 Rohde and Schwarz GmbH and Co KG

- 6.4.13 Ross Video Ltd.

- 6.4.14 Amagi Corporation

- 6.4.15 Hexaglobe SAS (SGT)

- 6.4.16 Pixel Power Ltd.

- 6.4.17 ENCO Systems Inc.

- 6.4.18 Switch Media Pty Ltd.

- 6.4.19 Logitek Electronic Systems Inc.

- 6.4.20 Crispin Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

廣播自動化和一體化頻道市場-全球產業規模、佔有率、趨勢、機會和預測:按最終用戶、頻道應用、地區和競爭對手分類,2021-2031年

廣播自動化和一體化頻道市場-全球產業規模、佔有率、趨勢、機會和預測:按最終用戶、頻道應用、地區和競爭對手分類,2021-2031年 播出自動化及CiaB(盒式頻道)市場分析:按組件、工作流程、應用、頻道類型、最終用戶和地區分類(2026-2034 年)

播出自動化及CiaB(盒式頻道)市場分析:按組件、工作流程、應用、頻道類型、最終用戶和地區分類(2026-2034 年) 2026年全球播出自動化市場報告

2026年全球播出自動化市場報告 播出自動化和機上盒頻道市場:按產品、部署、應用、最終用戶和分銷管道分類-2026年至2032年全球預測2026年全球播出自動化和一體化頻道市場報告

播出自動化和機上盒頻道市場:按產品、部署、應用、最終用戶和分銷管道分類-2026年至2032年全球預測2026年全球播出自動化和一體化頻道市場報告 播出解決方案市場分析及至2035年預測:按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和解決方案分類

播出解決方案市場分析及至2035年預測:按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和解決方案分類 全球播放解決方案市場

全球播放解決方案市場 2021-2031 年亞太地區播出自動化和 Channel-in-a-Box 市場報告(範圍、細分、動態和競爭分析)

2021-2031 年亞太地區播出自動化和 Channel-in-a-Box 市場報告(範圍、細分、動態和競爭分析) 2021-2031 年北美播出自動化和盒式頻道市場報告(範圍、細分、動態和競爭分析)

2021-2031 年北美播出自動化和盒式頻道市場報告(範圍、細分、動態和競爭分析) 2021-2031 年歐洲播放自動化和 Channel-in-a-Box 市場報告(範圍、細分、動態和競爭分析)

2021-2031 年歐洲播放自動化和 Channel-in-a-Box 市場報告(範圍、細分、動態和競爭分析)