|

市場調查報告書

商品編碼

2062431

亞太地區線上生鮮市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)Asia-Pacific Online Grocery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

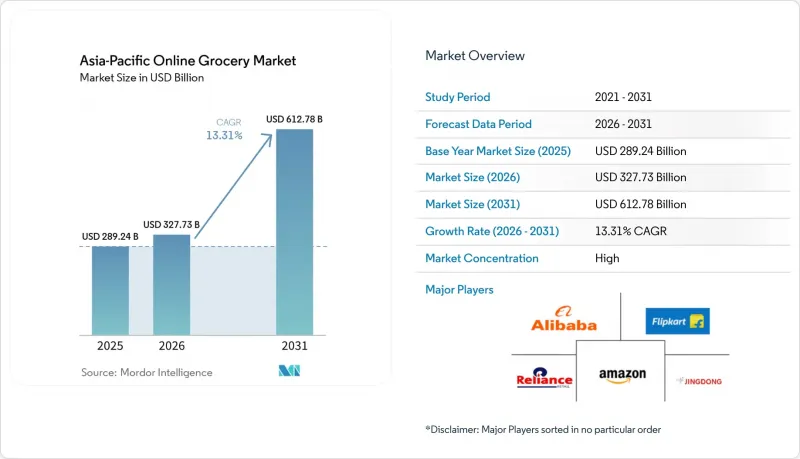

根據 Mordor Intelligence 預測,亞太地區線上雜貨配送市場規模預計將從 2025 年的 2,892.4 億美元成長到 2026 年的 3,277.3 億美元,到 2031 年將達到 6,127.8 億美元,2026 年至 2031 年的複合年成長率為 13.31%。

本報告按產品類別(生鮮食品、加工食品、飲料等)、配送速度(即時/當日送達、預約/隔日送達)、履約模式(電商平台/聚合平台、零售商自營暗店等)、訂單頻率計劃(按需訂購、訂閱/自動補貨)和地區(中國、印度等)進行細分。市場預測以美元計價。

亞太地區線上食品雜貨市場的趨勢和洞察。

在線使用在生鮮和易腐食品領域不斷擴展

生鮮食品是該平台的主要驅動力,這得益於溫控物流和自動化揀選技術的進步,這些技術提高了訂單準確率並最大限度地減少了廢棄物。雪梨和墨爾本的自動化客戶履約中心透過提高處理能力和維持新鮮度,擴大了2小時以內的配送窗口,增強了消費者對在線上購買生鮮食品的信心。低溫運輸挑戰在一些市場依然存在,例如印度由於從農場到餐桌的基礎設施不足以及過度依賴單一產品,導致果蔬採後損失率高達5%至15%。雖然區域低溫運輸專案和現代化物流系統正在應對這些挑戰,但東南亞仍需進一步投資於倉儲設施、節能營運以及數位化倉庫管理系統(WMS)和運輸管理系統(TMS)。

智慧型手機的普及正在推動「行動優先」的食品雜貨購物行為。

在全部區域,行動裝置已成為存取數位商務的主要管道,智慧型手機的普及正在改變消費者發現、訂購和支付食品雜貨的方式。年輕的人口結構和高都市區密度推動了頻繁的訂單,而即時庫存可見性和路線最佳化則縮短了配送時間。在日本,電子商務生態系統整合了履約中心、忠誠度計畫和支付系統,以增強消費者在日常食品雜貨購物中的參與。東協地區關於數位身分和跨境資料流動的區域政策旨在減輕行動優先交易的支付流程和合規負擔。在印度,跨帳戶支付和極低的交易成本消除了現金處理的低效之處,實現了快速的大規模交易,並促進了行動食品雜貨購物的廣泛普及。

挑戰包括最後一公里配送成本高和都市區交通擁擠。

都市區擁擠和配送密度波動導致最後一公里配送成本居高不下,影響了30分鐘以內配送的單次獲利能力。平台正透過路線整合、批量揀貨和動態人員配置來應對這些挑戰,但一天中不同時段和天氣造成的訂單需求波動加劇了配送成本的不確定性。如果能有效控制食品變質,高比例生鮮食品的購物籃可以提高利潤率,但溫控處理和退貨管理成本高昂,需要擴大規模才能抵銷這些成本。零售商自有門市網路可以透過利用倉庫和路邊取貨來平衡尖峰時段需求並縮短配送距離,從而降低最後一公里配送的複雜性。城市關於路邊空間、配送時間和配送人員安全的政策會影響運能規劃,需要在遵守政策的同時維持配送速度。

細分市場分析

預計到2025年,當日達和隔日達服務將佔據53.48%的市場佔有率,而30分鐘內超快速配送服務預計到2031年將以18.74%的複合年成長率成長。高密度網路和自動化履約系統正在改變都市區獲取日常必需品的方式。亞太地區的線上生鮮配送市場正朝著更短的配送時間方向發展,在小訂單快捷郵件配送和大訂單定時配送之間取得平衡,從而最佳化車輛運轉率和勞動生產力。澳洲的自動化客戶履約中心正提高高需求商品的處理能力與準確性,提升大都會圈2小時送達率,並增強消費者對生鮮食品配送服務的信心。在中國,與線上商品庫相連的連網倉庫實現了人口密集地區30分鐘送達,並輔以部分實體店提供即時配送服務。

路線最佳化、庫存視覺化和城市物流技術的進步正在減少訂單取消和替換,從而提升短途配送服務的客戶體驗。超過24小時的定時配送對於郊區的大量補貨仍然至關重要,因此,較長配送時段的價值得以維持。微型倉配的引進縮短了揀貨到出貨的時間,並擴大了當日達的覆蓋範圍。諸如線上訂購線下取貨之類的混合模式降低了最後一公里配送成本,並改善了郊區的取貨選擇。平台正在利用時限的訂單資料來最佳化商品種類和定價,從而提高轉換率。市場趨勢正朝著縮短交貨週期、同時維持處理大訂單能力的方向發展,從而緩解需求高峰,確保新鮮商品的供應。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 擴大線上銷售在生鮮和短保存期限食品領域的應用。

- 智慧型手機的普及正在推動行動優先的食品雜貨購物行為。

- 為滿足即時交付的需求,快速商業迅速發展。

- 快速消費品產業在應用程式內廣告和促銷的支出增加

- 訂閱模式的擴展(在日常必需品領域)

- 政府支持引入數位基礎設施和電子商務

- 市場限制因素

- 不斷上漲的最後一公里配送成本和都市區交通堵塞帶來的挑戰。

- 二、三線城市低溫運輸基礎設施不足。

- 都市區倉儲成本不斷上漲,正在影響快速零售的利潤率。

- 激烈的競爭持續對利潤率構成壓力。

- 消費行為分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按配送速度

- 30分鐘內

- 當天(2-12小時)/隔天

- 預定送貨時間(24 小時或以上)

- 依產品類型

- 生鮮食品

- 乳製品和烘焙食品

- 肉類、魚貝類

- 日用品和包裝商品

- 飲料

- 冷凍食品

- 其他產品類型

- 透過分銷管道

- 直接面對消費者 (D2C)

- 聚合平台

- 按地區

- 中國

- 印度

- 日本

- 澳洲

- 印尼

- 韓國

- 泰國

- 新加坡

- 越南

- 菲律賓

- 其他亞太國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Alibaba Group

- JD.com

- Amazon

- Reliance Retail

- Flipkart

- Zomato

- Swiggy

- Zepto

- Dingdong Maicai

- Meituan Maicai

- Pinduoduo

- Woolworths Group

- Coles Group

- NTUC FairPrice

- Lazada

- Rakuten

- Coupang

- Grab

- Foodpanda

- Ocado

第7章 市場機會與未來趨勢

According to Mordor Intelligence, the asia-Pacific online grocery delivery market is expected to grow from USD 289.24 billion in 2025 to USD 327.73 billion in 2026 and is forecast to reach USD 612.78 billion by 2031 at a CAGR of 13.31% over 2026-2031.

This report is Segmented by Product Category (Fresh Produce, Packaged Foods, Beverages, and More), Delivery Speed (Instant/Same Day, Scheduled/Next Day), Fulfilment Model (Marketplace Aggregator, Retailer-Owned Dark and More), Order-Frequency Plan (On-Demand, Subscription Auto-Replenish), and Geography (China, India, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Online Grocery Market Trends and Insights

Rising Online Adoption of Fresh and Perishable Grocery Categories

Fresh produce has become a key growth driver for platforms, supported by advancements in temperature-controlled logistics and automated picking, which enhance order accuracy and minimize waste. Automated customer fulfillment centers in Sydney and Melbourne have increased throughput and improved freshness, enabling scalable two-hour delivery windows and strengthening consumer trust in online purchases of perishables. Cold chain gaps persist in several markets, with India experiencing post-harvest losses of 5-15% for fruits and vegetables due to inadequate farmgate infrastructure and a focus on single commodities. Regional cold chain projects and modernized logistics systems are addressing these challenges, while Southeast Asia requires further investment in storage, energy-efficient operations, and digital WMS and TMS.

Smartphone Penetration Driving Mobile-First Grocery Shopping Behavior

Mobile devices dominate digital commerce access across Asia-Pacific, with smartphone adoption shaping how consumers discover, order, and pay for groceries. Younger demographics and urban density drive frequent orders, while real-time inventory visibility and route optimization reduce delivery times. In Japan, e-commerce ecosystems integrate fulfillment centers, loyalty programs, and payment systems, enhancing engagement for routine grocery purchases. Regional policies on digital identity and cross-border data flows aim to ease checkout and compliance for mobile-first transactions across ASEAN. In India, account-to-account payments and minimal transaction costs eliminate cash-handling inefficiencies, enabling quick, low-value transactions and supporting mobile grocery adoption at scale.

High Last-Mile Delivery Costs and Urban Congestion Challenges

Urban congestion and delivery density variability keep last-mile costs high, impacting unit economics for under-30-minute delivery. Platforms address these challenges through route clustering, batched picking, and dynamic labor allocation, but demand fluctuations driven by time of day and weather drive cost-to-serve variability. Perishable-heavy baskets can improve margins if spoilage is controlled, though temperature-controlled handling and returns management add costs requiring scale to offset. Retailer-owned store networks mitigate last-mile complexities by using backrooms and curbside pickup to smooth peak-hour demand and reduce delivery distances. Urban policies on curb space, delivery windows, and rider safety influence capacity planning, requiring compliance while maintaining delivery speed.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Growth of Quick-Commerce for Instant Delivery Needs

- Government Support for Digital Infrastructure and E-Commerce Adoption

- Inadequate Cold Chain Infrastructure in Tier-2 and Tier-3 Cities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Same-day and next-day services are projected to account for 53.48% of the market in 2025, with ultra-fast delivery within 30 minutes growing at a CAGR of 18.74% through 2031. Dense networks and automated fulfillment systems are transforming access to daily essentials across cities. The Asia-Pacific online grocery delivery market is shifting toward shorter delivery windows, balancing express deliveries for smaller orders with scheduled deliveries for larger baskets to optimize vehicle utilization and labor productivity. Automated customer fulfillment centers in Australia enhance throughput and accuracy for high-demand items, increasing two-hour delivery rates in metropolitan areas and strengthening trust in fresh delivery services. In China, networked warehouses integrated with online assortments enable 30-minute delivery in dense areas, supported by selective offline locations for instant delivery.

Advancements in routing, inventory visibility, and city logistics reduce cancellations and substitutions, improving customer experience in fast-delivery formats. Scheduled deliveries beyond 24 hours remain vital for bulk restocking in suburban areas, ensuring the relevance of longer delivery windows. Micro-fulfillment adoption compresses pick-to-ship times, expanding same-day delivery coverage. Hybrid models like click-and-collect lower last-mile costs and improve suburban pickup options. Platforms use short-window order data to refine assortments and pricing, enhancing conversion rates. The market trends toward shorter timelines while maintaining capacity for larger orders, mitigating peak demand and ensuring fresh product availability.

List of Companies Covered in this Report:

- Alibaba Group

- JD.com

- Amazon

- Reliance Retail

- Flipkart

- Zomato

- Swiggy

- Zepto

- Dingdong Maicai

- Meituan Maicai

- Pinduoduo

- Woolworths Group

- Coles Group

- NTUC FairPrice

- Lazada

- Rakuten

- Coupang

- Grab

- Foodpanda

- Ocado

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising online adoption of fresh and perishable grocery categories

- 4.2.2 Smartphone penetration driving mobile-first grocery shopping behavior

- 4.2.3 Rapid growth of quick-commerce for instant delivery needs

- 4.2.4 Increasing FMCG spending on in-app advertising and promotions

- 4.2.5 Expansion of subscription-based models for recurring essentials

- 4.2.6 Government support for digital infrastructure and e-commerce adoption

- 4.3 Market Restraints

- 4.3.1 High last-mile delivery costs and urban congestion challenges

- 4.3.2 Inadequate cold chain infrastructure in Tier-2 and Tier-3 cities

- 4.3.3 Rising urban warehousing costs impacting quick-commerce margins

- 4.3.4 Intense competition leading to sustained margin pressure

- 4.4 Consumer Behevaior Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Delivery Speed

- 5.1.1 <=30 Minutes

- 5.1.2 Same-Day (2-12 h) and Next Day

- 5.1.3 Scheduled (more than 24 h)

- 5.2 By Product Type

- 5.2.1 Fresh Produce

- 5.2.2 Dairy and Bakery

- 5.2.3 Meat, Fish, and Seafood

- 5.2.4 Staples and Packaged Goods

- 5.2.5 Beverages

- 5.2.6 Frozen Foods

- 5.2.7 Other Product Type

- 5.3 By Delivery Channel

- 5.3.1 Direct-to-Consumer (D2C)

- 5.3.2 Aggregator Platforms

- 5.4 By Geography

- 5.4.1 China

- 5.4.2 India

- 5.4.3 Japan

- 5.4.4 Australia

- 5.4.5 Indonesia

- 5.4.6 South Korea

- 5.4.7 Thailand

- 5.4.8 Singapore

- 5.4.10 Vietnam

- 5.4.11 Philippines

- 5.4.12 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Alibaba Group

- 6.4.2 JD.com

- 6.4.3 Amazon

- 6.4.4 Reliance Retail

- 6.4.5 Flipkart

- 6.4.6 Zomato

- 6.4.7 Swiggy

- 6.4.8 Zepto

- 6.4.9 Dingdong Maicai

- 6.4.10 Meituan Maicai

- 6.4.11 Pinduoduo

- 6.4.12 Woolworths Group

- 6.4.13 Coles Group

- 6.4.14 NTUC FairPrice

- 6.4.15 Lazada

- 6.4.16 Rakuten

- 6.4.17 Coupang

- 6.4.18 Grab

- 6.4.19 Foodpanda

- 6.4.20 Ocado

7 Market Opportunities and Future Trends

線上雜貨市場:2026-2032年全球市場預測(按產品類型、履約方式、配送速度、訂購管道和最終用戶分類)

線上雜貨市場:2026-2032年全球市場預測(按產品類型、履約方式、配送速度、訂購管道和最終用戶分類) 線上食品市場:按產品類型、購買方式和地區分類

線上食品市場:按產品類型、購買方式和地區分類 2026年全球線上雜貨市場報告

2026年全球線上雜貨市場報告 全球線上雜貨市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球線上雜貨市場規模、佔有率、趨勢和成長分析報告(2026-2034) B2B線上雜貨市場-全球產業規模、佔有率、趨勢、機會及預測(產品類型、支付方式、地區及競爭格局分類,2021-2031年)線上雜貨市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、配送類型、地區和競爭格局分類,2021-2031年

B2B線上雜貨市場-全球產業規模、佔有率、趨勢、機會及預測(產品類型、支付方式、地區及競爭格局分類,2021-2031年)線上雜貨市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、配送類型、地區和競爭格局分類,2021-2031年 全球線上雜貨市場:依產品、配送方式及地區劃分-市場規模、產業動態、機會分析及預測(2026-2035 年)

全球線上雜貨市場:依產品、配送方式及地區劃分-市場規模、產業動態、機會分析及預測(2026-2035 年) 日本線上雜貨市場報告:按產品類型、經營模式、平台、購買方式和地區分類(2026-2034年)

日本線上雜貨市場報告:按產品類型、經營模式、平台、購買方式和地區分類(2026-2034年) 線上雜貨市場規模、佔有率和成長分析(按產品類型、配送類型、支付方式、最終用戶和地區分類)-2026-2033年產業預測

線上雜貨市場規模、佔有率和成長分析(按產品類型、配送類型、支付方式、最終用戶和地區分類)-2026-2033年產業預測 即時生鮮配送生態系市場預測至2032年:依產品、支付方式、平台類型、技術、最終用戶及地區分類的全球分析

即時生鮮配送生態系市場預測至2032年:依產品、支付方式、平台類型、技術、最終用戶及地區分類的全球分析