|

市場調查報告書

商品編碼

2062300

歐洲售後市場胎壓監測系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)Europe Aftermarket TPMS - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

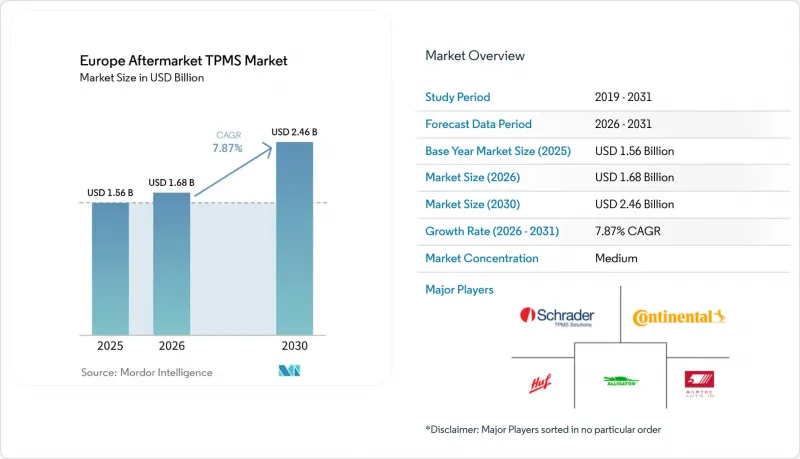

歐洲售後市場胎壓監測系統 (TPMS) 市場預計將從 2025 年的 15.6 億美元成長到 2026 年的 16.8 億美元,到 2031 年達到 24.6 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 7.87%。

本報告按類型(直接式胎壓監測系統和間接式胎壓監測系統)、技術整合(獨立式胎壓監測系統和智慧/連網式胎壓監測系統)、車輛類型(乘用車和商用車)、分銷管道(線下和線上)以及地區(德國、英國、法國、義大利、西班牙和其他歐洲國家)進行細分。市場預測以美元計價。

歐洲售後市場胎壓監測系統 (TPMS) 市場的趨勢與洞察

由於車輛老化,感知器更換的需求將會延長。

歐洲乘用車的平均車齡正在上升,部分地區甚至出現了車輛老化嚴重的現象。這一趨勢導致許多第一代直接式感測器的電池壽命超出正常範圍。為了降低維修成本,一些地區注重成本控制的維修店開始擴大使用通用可程式設計感測器。這種方法將滿足預計在可預見的未來將持續存在的更換需求。

根據歐盟法規 ECE 661/2009 促進更換週期

在德國、法國和荷蘭,胎壓監測系統(TPMS)故障現已被視為車輛在例行檢查中不合規,這使得該法規成為服務供應商和製造商可靠的收入來源。嚴格執行該法規可確保車輛符合安全標準,並刺激對TPMS維護和更換的需求。聯合國歐洲經濟委員會R141法規的適用範圍擴大至卡車和拖車,標誌著合規性的第二波浪潮,這將使能夠達到預警閾值的直接式TPMS系統受益。預計此舉將創造市場成長機會,因為車隊營運商和原始設備製造商(OEM)將合規性放在首位,以避免罰款並提高營運安全性。

學習/程式相關的高成本感測器和人事費用。

在波蘭,許多車主即使儀錶板上的警告燈亮起,也會推遲維修。主要原因是更換感測器成本高昂,尤其是考慮到人事費用和編程費用。此外,BMW和特斯拉系統的加密措施迫使維修店購買原廠配件或投資先進工具,這進一步推高了服務費用。

細分市場分析

到2025年,直接式胎壓監測系統(TPMS)將佔據歐洲售後市場74.38%的佔有率。這主要歸功於聯合國歐洲經濟委員會(UNECE)法規要求的即時、逐輪警報功能。同時,價格低40-50%的間接系統正以8.14%的複合年成長率成長,尤其是在南歐地區,因為2014年以前生產的廂型車業者正在尋求低成本的合規方案。

在預測期內,隨著演算法改善降低誤報率,歐盟售後市場間接式胎壓監測系統(TPMS)市場預計將加速成長。然而,絕對壓力測量精度方面的挑戰限制了其應用,目前僅限於注重成本的車隊。半導體技術的進步,例如恩智浦半導體(NXP)獲得AEC-Q100認證的NTM88K晶片,正在將直接式TPMS確立為重型車輛的長期標準,從而鞏固了直接式解決方案在歐洲售後TPMS市場的主導地位。

到2025年,獨立式閥門將佔據歐洲售後市場胎壓監測系統(TPMS)57.19%的佔有率。這主要是因為安裝人員更傾向於無需與遠端資訊處理閘道器配對的簡易重新學習流程。 Schrader和Huf提供的通用型產品降低了庫存成本,並維持了獨立維修店的支援。

受ESG主導的數據報告和預測性維護合約的推動,聯網胎壓監測系統(TPMS)的銷售額預計將以8.05%的複合年成長率成長。更實惠的車輛月度訂閱費用可望大幅提升連網套件在歐洲售後TPMS市場的佔有率。對於那些不願在中期更換感測器的車隊管理者而言,NXP的UWB架構能夠顯著延長電池壽命,因此可能頗具吸引力。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 由於車輛老化,感測器更換的需求週期越來越長。

- 歐盟法規 ECE 661/2009更換需求

- 消費者對輪胎安全性和燃油效率的關注度日益提高

- 所有車輛的ESG報告都需要即時輪胎壓力數據。

- 具備OTA升級功能的連網胎壓監測系統套件可作為新的收入來源

- 電子商務組件銷售管道擴大了通用套件的取得途徑

- 市場限制因素

- 人事費用進行重新培訓和編程。

- 與專為電動車設計的高壓輪胎有相容性問題

- 間接式胎壓監測系統的精確度問題正在削弱其可靠性。

- 聯網感測器中的網路風險會增加召回責任。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 直接式胎壓監測系統

- 間接式胎壓監測系統

- 透過技術整合

- 獨立式胎壓監測系統

- 智慧型/連網胎壓監測系統

- 車輛類型

- 搭乘用車

- 掀背車

- 轎車

- 運動型多用途車(SUV)和多功能車(MUV)

- 商用車輛

- 輕型商用車

- 中型和大型商用車輛

- 巴士和長途汽車

- 搭乘用車

- 透過分銷管道

- 離線

- 線上

- 國家

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Continental AG

- Sensata Technologies Inc.-Schrader

- Huf Hulsbeck & Furst GmbH

- Alligator Ventilfabrik GmbH

- ATEQ TPMS Tools

- Bartec Auto ID

- Autel Intelligent Technology

- Cub Elecparts Inc.

- Orange Electronic Co.

- Denso Corporation

- Pacific Industrial Co.

- ZF TRW Automotive

- Valeo SA

- Haltec Corporation

- Infitronic Technology

- Steelmate Automotive

- NXP Semiconductors

- Maxwell Products(TPMS Warehouse)

- Ridecell Fleet-TPMS

- Pricol Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the european aftermarket market size is projected to grow from USD 1.56 billion in 2025 to USD 1.68 billion in 2026, and is forecast to reach USD 2.46 billion by 2031, growing at a CAGR of 7.87% from 2026 to 2031.

This report is Segmented by Type (Direct TPMS and Indirect TPMS), Technology Integration (Stand-Alone TPMS Units and Smart/Connected TPMS), Vehicle Type (Passenger Cars and Commercial Vehicles), Distribution Channel (Offline and Online), and Geography (Germany, United Kingdom, France, Italy, Spain, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

Europe Aftermarket TPMS Market Trends and Insights

Aging Vehicle Parc Prolongs Sensor Replacement Demand

The average age of passenger cars in Europe has increased, with some regions reporting significantly older vehicles. This trend has led many first-generation direct sensors to exceed their typical battery life. To maintain affordability in repairs, workshops in cost-sensitive areas are increasingly using universal programmable sensors. This approach supports a sustained replacement trend expected to continue for the foreseeable future.

EU Regulation ECE 661/2009 Replacement-Cycle Pull

In Germany, France, and the Netherlands, periodic inspections now treat non-functional TPMS as failures, turning regulation into a reliable revenue source for service providers and manufacturers. This regulatory enforcement ensures that vehicles comply with safety standards, driving demand for TPMS maintenance and replacement. The extension of UNECE R141 to trucks and trailers signals a second compliance wave, benefiting direct TPMS that can meet the alert threshold. This development is expected to create growth opportunities in the market as fleet operators and OEMs prioritize compliance to avoid penalties and enhance operational safety.

High Sensor and Labor Cost for Relearn/Programming

In Poland, many customers delay repairs even when dashboard warnings signal issues, primarily because replacing sensors is costly, especially when labor and programming are factored in. Additionally, encryption on BMW and Tesla systems compels workshops to either purchase OEM parts or invest in advanced tools, further driving up service bills.

Other drivers and restraints analyzed in the detailed report include:

- Rising Consumer Focus on Tire Safety and Fuel Economy

- OTA-upgradeable Connected TPMS Kits

- EV-Specific High-Pressure Tires Create Compatibility Gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Direct TPMS commanded 74.38% of the European aftermarket market share in 2025, owing to real-time, wheel-specific alerts demanded by UNECE rules. Indirect systems priced 40-50% lower are growing at an 8.14% CAGR as operators of pre-2014 vans seek low-cost compliance, particularly in Southern Europe.

Over the forecast period, the EU TPMS aftermarket market for indirect TPMS is projected to accelerate as algorithm refinements reduce false positives. Yet, gaps in absolute-pressure measurement limit uptake to cost-sensitive fleets. Semiconductor advances, such as NXP's AEC-Q100-qualified NTM88K, are cementing direct TPMS as the long-term default across heavy-duty vehicles, reinforcing the leadership position of direct solutions in the European aftermarket market.

Stand-alone valves held 57.19% of the European aftermarket TPMS market size in 2025 as installers favored simpler re-learn processes that do not require pairing with telematics gateways. Universal-fit SKUs from Schrader and Huf keep inventory overhead low, sustaining loyalty among independent workshops.

Connected TPMS revenue will advance at an 8.05% CAGR on the back of ESG-driven data reporting and predictive maintenance contracts. The European aftermarket TPMS market share for connected kits could grow significantly if subscription prices become more affordable per vehicle per month. Fleet managers, hesitant about mid-cycle sensor swaps, may find NXP's UWB architecture appealing, offering a notable improvement in battery life.

List of Companies Covered in this Report:

- Continental AG

- Sensata Technologies Inc.- Schrader

- Huf Hulsbeck & Furst GmbH

- Alligator Ventilfabrik GmbH

- ATEQ TPMS Tools

- Bartec Auto ID

- Autel Intelligent Technology

- Cub Elecparts Inc.

- Orange Electronic Co.

- Denso Corporation

- Pacific Industrial Co.

- ZF TRW Automotive

- Valeo SA

- Haltec Corporation

- Infitronic Technology

- Steelmate Automotive

- NXP Semiconductors

- Maxwell Products (TPMS Warehouse)

- Ridecell Fleet-TPMS

- Pricol Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging Vehicle Parc Prolongs Sensor Replacement Demand

- 4.2.2 EU Regulation ECE 661/2009 Replacement-Cycle Pull

- 4.2.3 Rising Consumer Focus on Tire Safety and Fuel-Economy

- 4.2.4 Fleet-Wide ESG Reporting Needs Real-Time Pressure Data

- 4.2.5 OTA-Upgradeable Connected TPMS Kits as New Revenue Stream

- 4.2.6 E-Commerce Parts Channels Widen Access to Universal Kits

- 4.3 Market Restraints

- 4.3.1 High Sensor and Labor Cost for Relearn/Programming

- 4.3.2 EV-Specific High-Pressure Tires Create Compatibility Gaps

- 4.3.3 Accuracy Issues with Indirect TPMS Erode Confidence

- 4.3.4 Cyber-Risks in Connected Sensors Raise Recall Liability

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Type

- 5.1.1 Direct TPMS

- 5.1.2 Indirect TPMS

- 5.2 By Technology Integration

- 5.2.1 Stand-alone TPMS Units

- 5.2.2 Smart/Connected TPMS

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.1.1 Hatchbacks

- 5.3.1.2 Sedans

- 5.3.1.3 Sports Utility Vehicles (SUVs) & Multi-Utility Vehicles (MUVs)

- 5.3.2 Commercial Vehicles

- 5.3.2.1 Light Commercial Vehicles

- 5.3.2.2 Medium and Heavy Commercial Vehicles

- 5.3.2.3 Buses and Coaches

- 5.3.1 Passenger Cars

- 5.4 By Distribution Channel

- 5.4.1 Offline

- 5.4.2 Online

- 5.5 By Country

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Continental AG

- 6.4.2 Sensata Technologies Inc.- Schrader

- 6.4.3 Huf Hulsbeck & Furst GmbH

- 6.4.4 Alligator Ventilfabrik GmbH

- 6.4.5 ATEQ TPMS Tools

- 6.4.6 Bartec Auto ID

- 6.4.7 Autel Intelligent Technology

- 6.4.8 Cub Elecparts Inc.

- 6.4.9 Orange Electronic Co.

- 6.4.10 Denso Corporation

- 6.4.11 Pacific Industrial Co.

- 6.4.12 ZF TRW Automotive

- 6.4.13 Valeo SA

- 6.4.14 Haltec Corporation

- 6.4.15 Infitronic Technology

- 6.4.16 Steelmate Automotive

- 6.4.17 NXP Semiconductors

- 6.4.18 Maxwell Products (TPMS Warehouse)

- 6.4.19 Ridecell Fleet-TPMS

- 6.4.20 Pricol Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet Need Assessment

印度售後市場胎壓監測系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國售後市場胎壓監測系統:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)中國售後市場胎壓監測系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

印度售後市場胎壓監測系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國售後市場胎壓監測系統:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)中國售後市場胎壓監測系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) 2026年全球智慧拖車輪胎壓力監測系統(TMPS)和遠端資訊處理市場報告

2026年全球智慧拖車輪胎壓力監測系統(TMPS)和遠端資訊處理市場報告 輪胎壓力監測系統市場:2026年至2032年全球市場預測(依產品類型、組件、銷售管道、最終用戶及車輛類型分類)

輪胎壓力監測系統市場:2026年至2032年全球市場預測(依產品類型、組件、銷售管道、最終用戶及車輛類型分類) 輪胎壓力監測系統市場報告:按類型、技術、車輛類型、銷售管道和地區分類(2026-2034 年)

輪胎壓力監測系統市場報告:按類型、技術、車輛類型、銷售管道和地區分類(2026-2034 年) 汽車輪胎壓力監測系統市場:依產品類型、車輛類型、銷售管道和地區分類2026年全球先進胎壓監測系統市場報告2026年全球汽車輪胎壓力監測系統市場報告2026年全球高壓熔斷器監測模組市場報告

汽車輪胎壓力監測系統市場:依產品類型、車輛類型、銷售管道和地區分類2026年全球先進胎壓監測系統市場報告2026年全球汽車輪胎壓力監測系統市場報告2026年全球高壓熔斷器監測模組市場報告