|

市場調查報告書

商品編碼

2062299

美國售後市場胎壓監測系統:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)United States Aftermarket TPMS - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

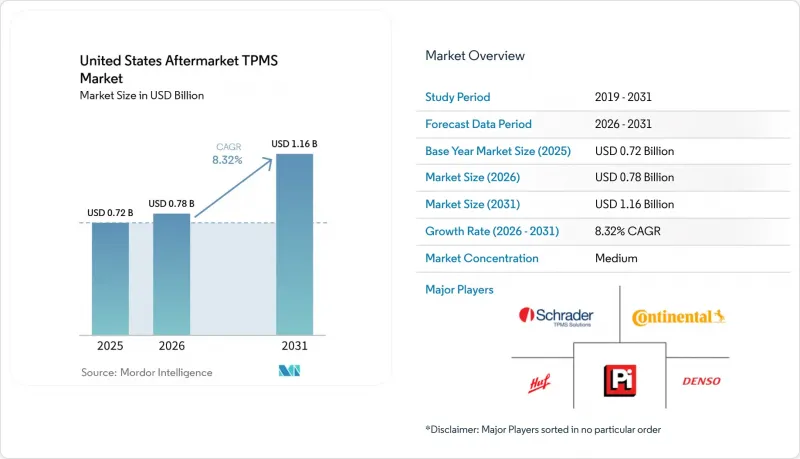

美國售後市場胎壓監測系統 (TPMS) 市場預計將從 2025 年的 7.2 億美元成長到 2026 年的 7.8 億美元,到 2031 年達到 11.6 億美元,在預測期(2026-2031 年)內複合年成長率為 8.32%。

本報告按類型(直接式胎壓監測系統和間接式胎壓監測系統)、技術整合(獨立式胎壓監測系統和智慧/連網式胎壓監測系統)、車輛類型(乘用車和商用車)以及銷售管道(線下和線上)進行細分。市場預測以美元計價。

美國售後市場胎壓監測系統 (TPMS) 市場的趨勢與洞察

FMVSS 138實施與感測器更換週期

FMVSS 138 標準規定,如果輪胎氣壓顯著低於指示值,每個車輪都必須發出警告,這鞏固了直接式胎壓監測系統 (TPMS) 在新車中的優勢。第一代感光元件內建的鋰電池壽命即將耗盡,由此產生的更換需求與常規輪胎維護無關。近期特斯拉 Model 3 和 Model Y 的召回事件凸顯了合規性監管的加強,並促使車主檢查感測器。在紐約州、賓州和德克薩斯等州,車輛偵測程序會自動偵測故障的 TPMS,導致違規產品的售後市場銷售激增。立法者正在根據《快速通道法案》(FAST Act) 的授權,探索防篡改架構,並展望未來可能重新定義服務協議的法規。

DIY胎壓監測感測器和診斷工具的電子商務拓展

亞馬遜平台上的維修工具和通用汽車相容感測器銷售量激增,凸顯了線上市場的快速滲透。像Alligator的Sens.it RS+這樣的通用感測器幾乎相容於所有車型。這些感測器可以透過連網工具進行韌體更新,使維修店能夠大幅減少原廠專用庫存。雖然這些成本節省對消費者來說很有吸引力,但最低限度標準意味著許多小包裹將繞過聯邦檢查,從而增加了仿冒品的風險。這也是美國海關關注的問題。這種情況既為安裝商帶來了成長機會,也帶來了品管的挑戰。

感測器平均售價(ASP)的下降給安裝商的利潤率帶來了壓力。

售後感測器價格已大幅下降。曾經價格昂貴的原廠配件如今以可程式設計單元和廉價通用產品的形式出現,價格大幅降低。對於設定產業平均服務費用的安裝商而言,扣除零件和人事費用後,維持獲利變得十分困難。而價格親民的DIY學習工具的普及,使得具備一定知識的車主無需專業人員協助即可完成安裝,這進一步加劇了這項挑戰。同時,大規模輪胎連鎖店正利用其採購優勢,透過交叉銷售輪胎來彌補感測器利潤率的下降,但單體門市的利潤空間則更加捉襟見肘。

細分市場分析

受 FMVSS 138 逐輪精度要求的驅動,直接式系統預計到 2025 年將在美國售後市場胎壓監測系統 (TPMS) 市場佔據最大的市場佔有率,達到 83.26%。而依賴 ABS 車輪速度比較的間接式解決方案將佔 16.74% 的市場佔有率,但在對成本較為敏感的輕型商用車車隊市場中,預計到 2031 年將以 8.56% 的複合年成長率成長。

在直接式技術方面,低功耗藍牙和遠端韌體更新的普及應用正在不斷推進,收入來源也正從硬體設備轉向軟體訂閱。由於間接式解決方案無法在靜止狀態下同時檢測氣壓下降或漏氣,因此在合規性環境中,它們僅作為直接式感測器的補充手段。

截至2025年,獨立式配置占美國售後市場胎壓監測系統(TPMS)市場佔有率的64.15%,但隨著車隊採用符合ISO 15638-23標準的互聯平台,這一佔有率正在逐漸下降。預計到2031年,智慧解決方案的複合年成長率將達到8.37%,超過整體市場成長率。

物流公司正在利用雲端分析來管理維修計劃,並報告意外輪胎故障顯著減少。增強型加密技術解決了學術研究中提出的隱私問題,使連網胎壓監測系統 (TPMS) 更容易被保險公司和企業合規團隊接受。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 根據 NHTSA 第 563 部分規定,胎壓監測系統 (TPMS) 的更換義務期限為 2025 年。

- DIY胎壓監測感測器和工具的電商交易量激增

- 輕型商用車營運商對車隊遠端資訊處理系統的改造升級日益增多

- 輪胎服務連鎖店ADAS調整套件銷售增加

- 引入聯網胎壓監測系統可享保險折扣。

- 無鋰MEMS壓力感測器的技術進步

- 市場限制因素

- 感測器平均售價(ASP)的下降給安裝商的利潤率帶來了壓力。

- 來自中國低成本仿冒品的競爭加劇。

- 獨立維修店技術水平的差異

- 採用自充氣技術的電動車用固態輪胎

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 直接式胎壓監測系統

- 間接式胎壓監測系統

- 透過技術整合

- 獨立式胎壓監測系統

- 智慧型/連網胎壓監測系統

- 車輛類型

- 搭乘用車

- 掀背車

- 轎車

- 運動型多用途車(SUV)和多功能車(MUV)

- 商用車輛

- 輕型商用車

- 中型和大型商用車輛

- 巴士和長途汽車

- 搭乘用車

- 透過分銷管道

- 離線

- 線上

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Sensata Technologies(Schrader)

- Continental AG

- Huf Hulsbeck & Furst

- Pacific Industrial

- DENSO Corp

- Alligator Ventilfabrik

- Dill Air Controls

- Standard Motor Products

- Autel Intelligent Tech.

- Bartec USA

- ATEQ TPMS Tools

- Orange Electronic

- Steelmate

- Haltec Corporation

- Myers Tire Supply

- Cub Elecparts

- Nonda Inc.

- PressurePro

- BorgWarner(Servoflex)

第7章 市場機會與未來展望

According to Mordor Intelligence, the united states aftermarket TPMS market size is expected to grow from USD 0.72 billion in 2025 to USD 0.78 billion in 2026 and is forecast to reach USD 1.16 billion by 2031, at a CAGR of 8.32% during the forecast period (2026-2031).

This report is Segmented by Type (Direct TPMS and Indirect TPMS), Technology Integration (Stand-Alone TPMS Units and Smart/Connected TPMS), Vehicle Type (Passenger Cars and Commercial Vehicles), and Distribution Channel (Offline and Online). The Market Forecasts are Provided in Terms of Value (USD).

United States Aftermarket TPMS Market Trends and Insights

FMVSS 138 Enforcement and Sensor Replacement Cycles

FMVSS 138 mandates a per-wheel warning when tire pressure drops significantly below placard levels, solidifying the dominance of direct TPMS in new vehicles. Sensors from the first wave are now outlasting their sealed lithium batteries, leading to a replacement demand that's independent of regular tire service events. A recent recall affecting Tesla's Model 3 and Y underscores the compliance scrutiny nudging owners to promptly service sensors. In states like New York, Pennsylvania, and Texas, inspection programs automatically flag non-functional TPMS, turning regulatory non-compliance into instant aftermarket sales. Legislators, under the FAST Act mandate, are delving into tamper-resistant architectures, eyeing potential rulemaking that could redefine future service protocols.

E-commerce Expansion for DIY TPMS Sensors and Diagnostic Tools

Amazon's marketplace highlights a surge in online sales for a relearn tool and GM-compatible sensors, underscoring rapid online penetration . Universal sensors, like Alligator's Sens.it RS+, cover nearly all vehicles. These sensors receive firmware updates through web-connected tools, allowing repair shops to significantly reduce their OEM-specific inventory. While these cost savings attract consumers, the de minimis threshold means many small parcels can skip federal inspection, heightening the risk of counterfeits, a concern noted by U.S. Customs. This dynamic presents both growth opportunities and quality-control hurdles for installers.

Declining Sensor ASPs Squeezing Installer Margins

Aftermarket sensor prices have decreased significantly. Once priced higher at OEMs, they now include programmable units and budget generics at much lower costs. Installers, with an industry-average service ticket, find it challenging to maintain profits after accounting for parts and labor. This challenge is further intensified by the availability of affordable DIY relearn tools, which enable savvy owners to bypass professional assistance. While high-volume tire chains utilize their purchasing power and cross-sell tires to counteract shrinking sensor margins, single-location shops face tighter profit margins.

Other drivers and restraints analyzed in the detailed report include:

- Fleet Telematics Retrofits Among Light Commercial Vehicle Operators

- Insurance-Linked Discounts for Connected-TPMS Adoption

- Technical Skill Gap at Independent Repair Shops

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Direct systems captured 83.26% of the United States aftermarket TPMS market share in 2025, owing to FMVSS 138's per-wheel accuracy requirements, securing the largest share of the United States aftermarket TPMS market. Indirect solutions, reliant on ABS wheel-speed comparisons, held 16.74% yet may grow 8.56% CAGR through 2031 among cost-sensitive light-commercial fleets.

Direct technology continues to adopt Bluetooth LE and remote firmware updates, shifting revenue emphasis from hardware units to software subscriptions. Indirect options remain limited by their inability to detect simultaneous pressure loss or stationary leaks, relegating them to a secondary role to direct sensors in compliance-driven environments.

Stand-alone configurations accounted for 64.15% of the United States aftermarket TPMS market share in 2025, but are now in gradual decline as fleets adopt connected platforms aligned with ISO 15638-23. Smart solutions are projected to outpace overall growth with an 8.37% CAGR through 2031.

Logistics operators harness cloud analytics for maintenance scheduling, reporting a significant drop in unplanned tire failures. Upgraded encryption addresses privacy issues highlighted in academic studies, rendering connected TPMS (Tire Pressure Monitoring Systems) more palatable for insurance underwriting and corporate compliance teams.

List of Companies Covered in this Report:

- Sensata Technologies (Schrader)

- Continental AG

- Huf Hulsbeck & Furst

- Pacific Industrial

- DENSO Corp

- Alligator Ventilfabrik

- Dill Air Controls

- Standard Motor Products

- Autel Intelligent Tech.

- Bartec USA

- ATEQ TPMS Tools

- Orange Electronic

- Steelmate

- Haltec Corporation

- Myers Tire Supply

- Cub Elecparts

- Nonda Inc.

- PressurePro

- BorgWarner (Servoflex)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandated TPMS Replacement Interval Under NHTSA Part 563 (2025)

- 4.2.2 Surging E-Commerce Volumes For DIY TPMS Sensors & Tools

- 4.2.3 Growing Fleet Telematics Retrofits Among LCV Operators

- 4.2.4 Rise in ADAS Recalibration Bundling At Tire-Service Chains

- 4.2.5 Insurance-Linked Discounts For Connected-TPMS Adoption

- 4.2.6 Lithium-Free MEMS Pressure-Sensor Breakthroughs

- 4.3 Market Restraints

- 4.3.1 Declining Sensor ASPs Squeezing Installer Margins

- 4.3.2 Increasing Competition From Low-Cost Chinese Clones

- 4.3.3 Technical Skill Gap At Independent Repair Shops

- 4.3.4 EV solid-State Tires With Embedded Self-Inflation Tech

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power - Suppliers

- 4.7.3 Bargaining Power - Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Type

- 5.1.1 Direct TPMS

- 5.1.2 Indirect TPMS

- 5.2 By Technology Integration

- 5.2.1 Stand-alone TPMS Units

- 5.2.2 Smart/Connected TPMS

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.1.1 Hatchbacks

- 5.3.1.2 Sedans

- 5.3.1.3 Sport Utility Vehicles (SUVs) & Multi-Utility Vehicles (MUVs)

- 5.3.2 Commercial Vehicles

- 5.3.2.1 Light Commercial Vehicles

- 5.3.2.2 Medium & Heavy Commercial Vehicles

- 5.3.2.3 Buses & Coaches

- 5.3.1 Passenger Cars

- 5.4 By Distribution Channel

- 5.4.1 Offline

- 5.4.2 Online

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Sensata Technologies (Schrader)

- 6.4.2 Continental AG

- 6.4.3 Huf Hulsbeck & Furst

- 6.4.4 Pacific Industrial

- 6.4.5 DENSO Corp

- 6.4.6 Alligator Ventilfabrik

- 6.4.7 Dill Air Controls

- 6.4.8 Standard Motor Products

- 6.4.9 Autel Intelligent Tech.

- 6.4.10 Bartec USA

- 6.4.11 ATEQ TPMS Tools

- 6.4.12 Orange Electronic

- 6.4.13 Steelmate

- 6.4.14 Haltec Corporation

- 6.4.15 Myers Tire Supply

- 6.4.16 Cub Elecparts

- 6.4.17 Nonda Inc.

- 6.4.18 PressurePro

- 6.4.19 BorgWarner (Servoflex)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

歐洲售後市場胎壓監測系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)印度售後市場胎壓監測系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國售後市場胎壓監測系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

歐洲售後市場胎壓監測系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)印度售後市場胎壓監測系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國售後市場胎壓監測系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) 2026年全球智慧拖車輪胎壓力監測系統(TMPS)和遠端資訊處理市場報告

2026年全球智慧拖車輪胎壓力監測系統(TMPS)和遠端資訊處理市場報告 輪胎壓力監測系統市場:2026年至2032年全球市場預測(依產品類型、組件、銷售管道、最終用戶及車輛類型分類)

輪胎壓力監測系統市場:2026年至2032年全球市場預測(依產品類型、組件、銷售管道、最終用戶及車輛類型分類) 輪胎壓力監測系統市場報告:按類型、技術、車輛類型、銷售管道和地區分類(2026-2034 年)

輪胎壓力監測系統市場報告:按類型、技術、車輛類型、銷售管道和地區分類(2026-2034 年) 汽車輪胎壓力監測系統市場:依產品類型、車輛類型、銷售管道和地區分類2026年全球先進胎壓監測系統市場報告2026年全球汽車輪胎壓力監測系統市場報告2026年全球高壓熔斷器監測模組市場報告

汽車輪胎壓力監測系統市場:依產品類型、車輛類型、銷售管道和地區分類2026年全球先進胎壓監測系統市場報告2026年全球汽車輪胎壓力監測系統市場報告2026年全球高壓熔斷器監測模組市場報告