|

市場調查報告書

商品編碼

2062297

中國售後市場胎壓監測系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)China Aftermarket TPMS - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

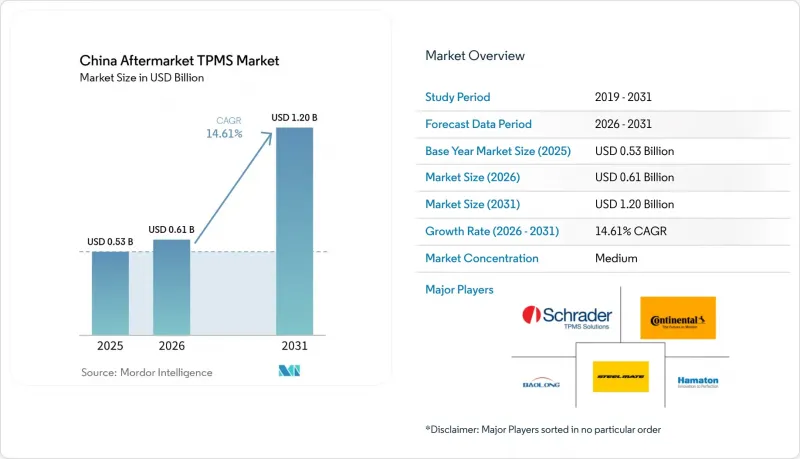

根據 Mordor Intelligence 預測,中國售後市場的胎壓監測系統 (TPMS) 市場規模預計將從 2025 年的 5.3 億美元成長到 2026 年的 6.1 億美元,到 2031 年將達到 12 億美元。

預計 2026 年至 2031 年的年複合成長率(CAGR)為 14.61%。

本報告按類型(直接式胎壓監測系統、間接式胎壓監測系統)、技術整合(獨立式胎壓監測系統、智慧/連網式胎壓監測系統)、車輛類型(乘用車、商用車)和通路(線下、線上)進行細分。市場預測以價值(美元)和銷售(輛)兩種形式呈現。

中國售後市場胎壓監測系統 (TPMS) 市場的趨勢與洞察

乘用車保有量增加和感知器更換週期

中國擁有龐大的乘用車保有量,並且每年持續成長。近年來銷售的汽車普遍配備密封式鋰電池,其使用壽命通常只有幾年。這將在未來引發大規模的更換需求,使售後市場每年新增數百萬個感測器。高周轉率的中型卡車進一步推動了商用車市場銷售的成長。由於這些電池不可修復,一旦某個電芯損壞,就需要更換整個感測器,這為供應商提供了穩定的收入來源。一線城市憑藉著完善的服務網路佔據主導地位,但隨著DIFM(直接安裝、維修和維護)基礎設施的完善,二、三線城市的需求也逐漸擴大。

新車強制安裝胎壓監測系統也影響了售後市場安裝的需求。

GB 26149-2017標準的實施顯著提高了乘用車胎壓監測系統(TPMS)的普及率。隨著原廠配備TPMS的二手車進入二手市場,原車主受惠於即時警報功能,老舊車輛的改裝也日益普及。 Steel Mate和Orange Electronics等品牌提供使用者可自行安裝的套件,以及需要輪胎店專業安裝的套件。儘管目前尚無針對貨車的正式強制要求,但商用車業者正積極採用這些系統,以應對未來的法規要求並減少因胎壓不足造成的燃油損失。在標準化管理委員會的持續監督下,改裝市場勢頭強勁,尤其是在東部沿海人口稠密的省份。

價格敏感度和假冒感應器

雖然標準型感測器在售後市場價格範圍內交易,但原廠配套感測器的價格卻高得多。這種價格差距刺激了對低成本替代品的需求,而其中一些已被證實是仿冒品產品。 Stellantis 和 Petromin 曝光了大規模出口企業,這些企業銷售仿冒的煞車和轉向零件,凸顯了中國品管的漏洞。假冒的胎壓監測系統 (TPMS) 常常因為密封不嚴或射頻不匹配而很快失效,損害了消費者的信心。貨運公司已經受到電動車價格競爭的嚴重衝擊,幾乎沒有餘力投資高價感測器,這進一步加劇了價格下行的壓力。雖然原廠配套品牌現在會在網路上顯著展示 ISO 和 CE 認證,並延長保固期,但由於監測系統分散在眾多工廠,這些措施難以全面落實。

細分市場分析

預計2025年,直接式胎壓監測系統將佔據中國胎壓監測系統售後70.33%的佔有率。這主要得益於GB 26149-2017標準的實施,該標準規定,當胎壓低於建議值的75%時,必須發出精確的單輪胎壓警報。直接式感測器能夠提供溫度數據和單輪統計數據,這些數據對於特斯拉和蔚來等汽車製造商採用的ADAS平台至關重要。同時,間接式胎壓監測技術預計將以15.04%的複合年成長率成長。這是因為基於ABS的軟體更新使其能夠在不為2019年之前生產的車輛添加新硬體的情況下,作為基本的預警系統運作。然而,間接式胎壓監測系統在車隊市場吸引力不足,因為它無法檢測過量充氣或緩慢洩漏,無法識別故障輪,也無法在每次更換輪胎後重新校準。

國內晶片廠商正在縮小成本差距。 AutoChips的單晶片AC5111已將直觸式感測器的平均價格降至一定閾值以下,緩解了先前的價格挑戰。寶龍正大力投資研發,以提升電池續航力並整合藍牙連接功能,旨在進軍OTA生態系統。儘管監管部門更傾向於直觸式警報,但分析師預測,即使間接式感測器逐漸滲透到對價格敏感的市場,直觸式感測器在總出貨量方面仍將超越間接式感測器。

預計到2025年,獨立式胎壓監測系統(TPMS)設備將佔據中國售後市場TPMS市場71.46%的佔有率,並繼續成為二手車售後市場的主力產品,因為在這些市場中,簡單的儀錶板顯示器即可滿足需求。整合BLE、NFC和OTA更新功能的智慧或連網平台預計將以17.11%的複合年成長率成長,這主要得益於智慧型手機的普及和車載資訊服務需求的推動。借助RF-Star的BLE套件,駕駛員可以透過應用程式監控輪胎壓力、溫度和感測器電池電量,並且無需拆卸車輪即可進行更新。鴻河科技透過加密的OTA軟體套件實現了極低的故障率,從而增強了用戶對現場韌體升級的信心。

車隊營運商正在部署雲端連接系統,透過 LoRa 閘道傳輸輪胎數據,從而減少路肩停工時間,而路肩停工時間通常會對每次商業事故造成高昂的成本。對於個人駕駛員而言,NFC可程式設計型號無需診斷工具,即可實現快速的 DIY 輪胎更換。雖然獨立設備預計在短期內仍將主導低價市場,但軟體定義感測器正透過進階分析和遠端診斷,為訂閱收入打開大門。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 乘用車保有量增加和感知器更換週期

- 新車強制安裝胎壓監測系統(TPMS)帶動了售後市場對TPMS安裝的需求。

- 電氣化正在加速商用車輛輪胎的磨損。

- 電子商務組件管道的擴展

- 消費者安全意識日益增強

- 國產用於胎壓監測系統的單晶片半導體顯著降低了套件價格。

- 市場限制因素

- 價格敏感度和假冒感應器

- 老舊車輛安裝的複雜性

- 非標準頻率和電池服務成本

- 人們對連網胎壓監測系統的資料隱私問題感到擔憂。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 直接式胎壓監測系統

- 間接式胎壓監測系統

- 透過技術整合

- 獨立式胎壓監測系統

- 智慧型/連網胎壓監測系統

- 車輛類型

- 搭乘用車

- 掀背車

- 轎車

- 運動型多用途車(SUV)和多功能車(MUV)

- 商用車輛

- 輕型商用車

- 中型和大型商用車輛

- 巴士和長途汽車

- 搭乘用車

- 透過分銷管道

- 線下通路(零件商店、專賣店、服務中心)

- 線上(OEM網站/應用程式、電子商務平台)

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Sensata Technologies(Schrader)

- Continental AG

- Shanghai Baolong Automotive

- Steelmate Automotive

- Hamaton Automotive Technology

- Shenzhen Careud Security Equipment

- Kysonix Automotive Electronics

- Shenzhen TireMagic Electronic Tech

- AutoChips Inc.

- Hangzhou Huf Hulsbeck & Furst

- Pacific Industrial Co. Ltd.

- Denso Corporation

- ZF Friedrichshafen(WABCO)

- Orange Electronic

- Ningbo Delin Auto Parts

- ATEQ China

- Promata Sinotek

- Shenzhen EGQ Cloud Technology

第7章 市場機會與未來展望

According to Mordor Intelligence, the china aftermarket TPMS market size is projected to grow from USD 0.53 billion in 2025 to USD 0.61 billion in 2026, and is forecast to reach USD 1.20 billion by 2031, growing at a CAGR of 14.61% from 2026 to 2031.

This report is Segmented by Type (Direct TPMS, Indirect TPMS), Technology Integration (Stand-Alone TPMS Units, Smart/Connected TPMS), Vehicle Type (Passenger Cars, Commercial Vehicles), and Distribution Channel (Offline, Online). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

China Aftermarket TPMS Market Trends and Insights

Growing Passenger-Car Parc and Sensor-Replacement Cycle

China has a significant passenger-car parc and continues to add vehicles annually. Cars sold in recent years are equipped with sealed lithium batteries, which typically last several years. This will lead to a substantial replacement wave in the future, adding millions of sensors to the annual aftermarket demand. Medium-duty trucks, with a faster turnover rate, further contribute to increased volumes in the commercial segment. Since these batteries are non-serviceable, a dead cell requires complete sensor replacement, ensuring consistent revenue for suppliers. Tier-1 cities are leading due to their established service networks, while tier-2 and tier-3 regions are gradually advancing as their DIFM infrastructure develops.

Mandatory TPMS Fitment on New Vehicles Spills Over to Retrofit Demand

The implementation of GB 26149-2017 significantly increased the adoption of TPMS in passenger cars . With factory-equipped used cars now entering the secondary market, first-time owners are benefiting from real-time alerts and are also retrofitting older vehicles. Brands like Steel Mate and Orange Electronics offer both internal and external kits that can be self-installed or professionally installed at tire shops. Even without formal truck mandates, commercial operators are proactively installing these systems to prepare for future regulations and reduce fuel losses from underinflation. The Standardization Administration's continuous scrutiny ensures that retrofit momentum remains strong, particularly in the densely populated provinces along the east coast.

Price Sensitivity and Counterfeit Sensors

Standard units fetch aftermarket prices within a certain range, while OEM-equivalent sensors are significantly more expensive. This price disparity fuels demand for low-cost substitutes, some of which turn out to be counterfeit. Stellantis and Petromin exposed a significant export ring dealing in imitation brake and steering parts, highlighting vulnerabilities in China's quality oversight. Counterfeit Tire Pressure Monitoring Systems (TPMS) often malfunction quickly, attributed to inadequate sealing and misaligned radio frequencies, eroding consumer trust. Freight operators, already feeling the pinch from electric-vehicle price wars, find little leeway for premium sensors, intensifying downward pressure on prices. While genuine brands are now prominently showcasing ISO and CE certifications online and extending warranties, enforcement of these measures is hindered by fragmented policing across numerous factories.

Other drivers and restraints analyzed in the detailed report include:

- Electrification Accelerating Tire-Wear on CV Fleets

- Expansion of E-Commerce Parts Channels

- Installation Complexity for Legacy Vehicles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Direct systems captured 70.33% of the Chinese aftermarket TPMS market in 2025 because GB 26149-2017 requires precise, per-wheel pressure alarms below 75% of recommended levels. Direct sensors provide temperature data and tire-level statistics prized by ADAS platforms from automakers such as Tesla and NIO. Indirect technology, however, is projected to advance at a 15.04% CAGR because an ABS-based software update can turn any pre-2019 vehicle into a basic alert system without new hardware. Yet indirect options cannot flag over-inflation or slow leaks, identify which wheel is failing, or be calibrated after every rotation, reducing fleet appeal.

Domestic chip makers are closing the cost gap: AutoChips' single-die AC5111 has pushed average direct-sensor prices below a certain threshold, easing past price challenges. Baolong is investing significantly in R&D to enhance battery life and integrate Bluetooth connectivity, positioning itself for OTA ecosystems. Despite regulations favoring direct alerts, analysts predict direct sensors will surpass indirect units in total volume, even as indirect units penetrate price-sensitive markets.

Stand-alone TPMS devices held 71.46% of the Chinese aftermarket TPMS market in 2025 and remain staples for the used-car aftermarket, where a simple dash display suffices. Smart or connected platforms integrating BLE, NFC, and OTA updates are forecast to post a 17.11% CAGR, driven by smartphone ubiquity and telematics demand. RF-Star's BLE kit allows drivers to monitor tire pressure, temperature, and sensor battery life via an app, and to push updates without removing the wheels. Honghe Technology demonstrated that encrypted OTA packages can achieve extremely low failure rates, enhancing confidence in field firmware upgrades.

Fleet operators are adopting cloud-linked systems that transmit tire data through LoRa gateways, reducing roadside downtime, which typically incurs high costs per commercial incident. For individual drivers, NFC-programmable models eliminate the need for a diagnostic tool, enabling a DIY tire swap in a short time. While stand-alone units are expected to dominate low-ticket sales for the foreseeable future, software-defined sensors are paving the way for subscription revenue through advanced analytics and remote diagnostics.

List of Companies Covered in this Report:

- Sensata Technologies (Schrader)

- Continental AG

- Shanghai Baolong Automotive

- Steelmate Automotive

- Hamaton Automotive Technology

- Shenzhen Careud Security Equipment

- Kysonix Automotive Electronics

- Shenzhen TireMagic Electronic Tech

- AutoChips Inc.

- Hangzhou Huf Hulsbeck & Furst

- Pacific Industrial Co. Ltd.

- Denso Corporation

- ZF Friedrichshafen (WABCO)

- Orange Electronic

- Ningbo Delin Auto Parts

- ATEQ China

- Promata Sinotek

- Shenzhen EGQ Cloud Technology

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Passenger-Car Parc and Sensor-Replacement Cycle

- 4.2.2 Mandatory TPMS Fitment on New Vehicles Spills Over to Retrofit Demand

- 4.2.3 Electrification Accelerating Tire-Wear on CV Fleets

- 4.2.4 Expansion of E-Commerce Parts Channels

- 4.2.5 Heightened Consumer Safety Awareness

- 4.2.6 Domestic One-Chip TPMS Silicon Slashes Kit Prices

- 4.3 Market Restraints

- 4.3.1 Price Sensitivity and Counterfeit Sensors

- 4.3.2 Installation Complexity for Legacy Vehicles

- 4.3.3 Non-Standard Frequencies and Battery-Service Costs

- 4.3.4 Data-Privacy Worries Around Connected TPMS

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size and Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Type

- 5.1.1 Direct TPMS

- 5.1.2 Indirect TPMS

- 5.2 By Technology Integration

- 5.2.1 Stand-alone TPMS Units

- 5.2.2 Smart/Connected TPMS

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.1.1 Hatchbacks

- 5.3.1.2 Sedans

- 5.3.1.3 Sports Utility Vehicles (SUVs) and Multi-Utility Vehicles (MUVs)

- 5.3.2 Commercial Vehicles

- 5.3.2.1 Light Commercial Vehicles

- 5.3.2.2 Medium and Heavy Commercial Vehicles

- 5.3.2.3 Buses and Coaches

- 5.3.1 Passenger Cars

- 5.4 By Distribution Channel

- 5.4.1 Offline (Parts Stores, Specialty Shops, Service Centers)

- 5.4.2 Online (OEM Sites/Apps, E-commerce Platforms)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Sensata Technologies (Schrader)

- 6.4.2 Continental AG

- 6.4.3 Shanghai Baolong Automotive

- 6.4.4 Steelmate Automotive

- 6.4.5 Hamaton Automotive Technology

- 6.4.6 Shenzhen Careud Security Equipment

- 6.4.7 Kysonix Automotive Electronics

- 6.4.8 Shenzhen TireMagic Electronic Tech

- 6.4.9 AutoChips Inc.

- 6.4.10 Hangzhou Huf Hulsbeck & Furst

- 6.4.11 Pacific Industrial Co. Ltd.

- 6.4.12 Denso Corporation

- 6.4.13 ZF Friedrichshafen (WABCO)

- 6.4.14 Orange Electronic

- 6.4.15 Ningbo Delin Auto Parts

- 6.4.16 ATEQ China

- 6.4.17 Promata Sinotek

- 6.4.18 Shenzhen EGQ Cloud Technology

7 Market Opportunities & Future Outlook

歐洲售後市場胎壓監測系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)印度售後市場胎壓監測系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國售後市場胎壓監測系統:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

歐洲售後市場胎壓監測系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)印度售後市場胎壓監測系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國售後市場胎壓監測系統:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 2026年全球智慧拖車輪胎壓力監測系統(TMPS)和遠端資訊處理市場報告

2026年全球智慧拖車輪胎壓力監測系統(TMPS)和遠端資訊處理市場報告 輪胎壓力監測系統市場:2026年至2032年全球市場預測(依產品類型、組件、銷售管道、最終用戶及車輛類型分類)

輪胎壓力監測系統市場:2026年至2032年全球市場預測(依產品類型、組件、銷售管道、最終用戶及車輛類型分類) 輪胎壓力監測系統市場報告:按類型、技術、車輛類型、銷售管道和地區分類(2026-2034 年)

輪胎壓力監測系統市場報告:按類型、技術、車輛類型、銷售管道和地區分類(2026-2034 年) 汽車輪胎壓力監測系統市場:依產品類型、車輛類型、銷售管道和地區分類2026年全球先進胎壓監測系統市場報告2026年全球汽車輪胎壓力監測系統市場報告2026年全球高壓熔斷器監測模組市場報告

汽車輪胎壓力監測系統市場:依產品類型、車輛類型、銷售管道和地區分類2026年全球先進胎壓監測系統市場報告2026年全球汽車輪胎壓力監測系統市場報告2026年全球高壓熔斷器監測模組市場報告