|

市場調查報告書

商品編碼

2062298

印度售後市場胎壓監測系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)India Aftermarket TPMS - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

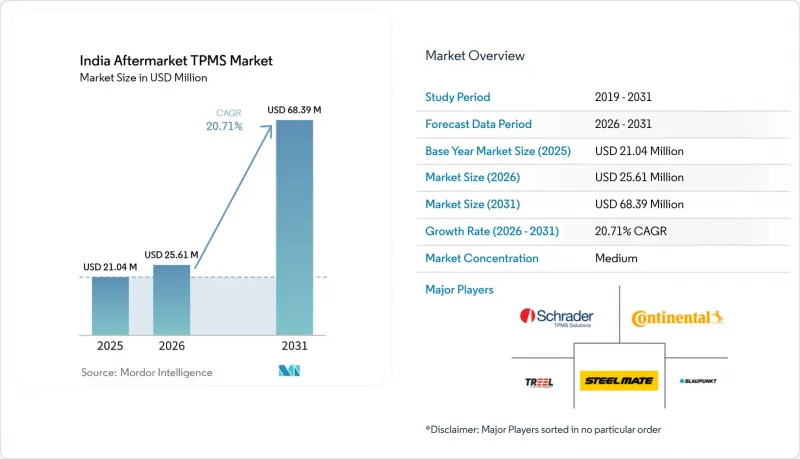

印度售後市場胎壓監測系統 (TPMS) 市場預計將從 2025 年的 2,104 萬美元成長到 2026 年的 2,561 萬美元,到 2031 年達到 6,839 萬美元。

預計 2026 年至 2031 年的年複合成長率(CAGR)為 20.71%。

本報告按類型(直接式胎壓監測系統和間接式胎壓監測系統)、技術整合(獨立式胎壓監測系統和智慧/連網式胎壓監測系統)、車輛類型(乘用車和商用車)以及分銷管道(線下和線上)進行細分。市場預測以美元計價。

印度售後市場胎壓監測系統 (TPMS) 市場的趨勢與洞察

對 N2、N3、M2 和 M3 類 AIS-151 第二階段進行強制性修改。

AIS-151第二階段標準的實施將強制要求在印度境內運作的中型和重型車輛安裝胎壓監測系統(TPMS)。由於合規性檢查與年度車輛檢驗掛鉤,因此安裝TPMS將成為車隊預算中的強制性成本。供應商將能夠獲得多年需求預測,從而更好地規劃本地生產、庫存管理和最後一公里物流。此外,該法規的有效執行將改善國內感測器製造商的資金籌措前景,並促進產能擴張。泰米爾納德邦、卡納塔克邦和馬哈拉斯特拉邦的早期實施將作為案例研究,加速鄰近市場的推廣。雖然該法規並非強制要求,但它將使輕型商用車車隊安裝TPMS的情況更加普遍。

電子商務的發展與DIY輪胎保養文化的興起

隨著15至35歲的年輕男性消費者越來越傾向於避開實體店,Flipkart和亞馬遜等線上市場平台的胎壓監測系統(TPMS)套件銷售量實現了兩位數成長。透明的價格、用戶評價和逐步安裝影片消除了資訊不對稱,降低了首次購買者的風險。二、三線城市的獨立維修店也開始大量線上訂購感應器,以縮短前置作業時間並豐富產品種類。車主技術素養的提高催生了DIY精神,他們用自己的時間取代了人事費用,從而擴大了潛在客戶群。這些因素正促使價值獲取從實體經銷商轉向提供支付、保固和物流等一站式服務的數位平台。

價格敏感型消費者的心理

胎壓監測系統(TPMS)套件的價格通常在5000至10000印度盧比(約54至108美元)之間,這是一筆不小的開支,尤其是在許多車主已經推遲日常保養的情況下。調查顯示,在經濟情勢不明朗的時期,68%的駕駛會延後非必要的車輛升級。收入較低的農村和郊區家庭往往更傾向於選擇車載資訊娛樂系統等顯眼的配件,而不是隱藏的安全電子設備。每5至7年更換一次電池會增加持續的維護成本,並降低購買意願。雖然在收入較高的南部和西部各邦,TPMS的購買率更高,但持續的價格促銷和融資方案對於在全國推廣仍然至關重要。

細分市場分析

預計到2025年,直接式感測器將佔據印度售後市場胎壓監測系統(TPMS)市場佔有率的68.17%,這主要得益於車隊對±1 PSI精度的偏好,以滿足保險公司的資料登錄要求。這進一步鞏固了閥式感測器技術在印度售後市場TPMS市場的佔有率優勢。大陸集團位於班加羅爾的工廠目前正在交付第二代產品,其電池壽命長達7-10年,從而降低了終身服務成本。然而,由於掀背車和轎車車主為了將安裝成本閾值在5000印度盧比(約合54美元)以下而選擇基於ABS的感應式系統,預計到2031年,間接式平台將以21.17%的複合年成長率成長,從而擴大印度售後市場TPMS市場中首次購車者的佔有率。

Martti Suzuki 2026車型系列將進一步鞏固間接式胎壓監測系統的應用,該系列所有中檔車型都將配備基於車輪速度的胎壓監測警報功能。然而,由於精度有限,且更換輪胎後需要手動重置,其在長途貨車上的實用性受到限制。因此,直接式胎壓監測系統仍然是預測性維護合約的基礎,並在印度售後市場商用車胎壓監測系統中保持領先地位。

預計到2025年,獨立式顯示器將佔據印度售後市場胎壓監測系統(TPMS)58.83%的市場佔有率,這顯示市場對低初始成本的需求旺盛,且部署大規模。同時,智慧型TPMS平台正以21.42%的複合年成長率成長,透過將資料傳送到雲端儀錶板,實現節油分析。這一趨勢使得聯網感測器成為印度售後市場TPMS中成長最快的組件。

Shriram General Insurance公司為那些在95%的運作時間內將輪胎氣壓保持在可接受範圍內的車隊提供10-15%的保費折扣,這充分體現了遠端資訊處理合約的成本效益。隨著5G網路覆蓋範圍的擴大、延遲的降低以及無線韌體更新的普及,印度的售後胎壓監測系統(TPMS)產業正從硬體利潤率轉向數據驅動型服務。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- AIS-151 第二階段 N2、N3、M2 和 M3 類別的合規性要求。

- 電子商務的發展與DIY輪胎保養文化的興起

- 電動車和天然氣汽車重量的增加引發了人們對輪胎安全性的擔憂。

- 透過捆綁式智慧胎壓監測系統擴展有組織的售後服務鏈。

- 中小企業車隊數位轉型,降低輪胎相關營運成本(OPEX)

- 配備胎壓監測系統 (TPMS) 的車輛可享有保險遠端資訊處理折扣。

- 市場限制因素

- 價格敏感型消費者的心理

- 大量低成本假冒感測器的湧入正在破壞信任。

- 缺乏熟練的TPMS直接校準技術人員

- 與原廠資訊娛樂系統互通性問題。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 直接式胎壓監測系統

- 間接式胎壓監測系統

- 透過技術整合

- 獨立式胎壓監測系統

- 智慧型/連網胎壓監測系統

- 車輛類型

- 搭乘用車

- 掀背車

- 轎車

- 運動型多用途車(SUV)和多功能車(MUV)

- 商用車輛

- 輕型商用車

- 中型和大型商用車輛

- 巴士和長途汽車

- 搭乘用車

- 透過分銷管道

- 離線

- 線上

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Sensata Technologies(Schrader)

- Continental AG

- Treel Mobility(JK Tyre)

- Steelmate Co Ltd

- Blaupunkt India

- Alligator Ventilfabrik GmbH

- CUB Elecparts Inc.

- Hamaton Automotive

- Dill Air Controls

- Bartec Auto ID

- TyreSense(Transense)

- SensAiry(Tymtix)

- Goodyear SightLine

- Bridgestone Webfleet TPMS

- CEAT Smart Tyre

- Michelin TPMS Solutions

- Manatec Electronics

- JK Automotive Sensors

- Autel Intelligent TPMS

第7章 市場機會與未來展望

According to Mordor Intelligence, the indian aftermarket TPMS market is projected to grow from USD 21.04 million in 2025 to USD 25.61 million in 2026 and is forecast to reach USD 68.39 million by 2031, growing at a CAGR of 20.71% from 2026 to 2031.

This report is Segmented by Type (Direct TPMS and Indirect TPMS), Technology Integration (Stand-Alone TPMS Units and Smart/Connected TPMS), Vehicle Type (Passenger Cars and Commercial Vehicles), and Distribution Channel (Offline and Online). The Market Forecasts are Provided in Terms of Value (USD).

India Aftermarket TPMS Market Trends and Insights

AIS-151 Stage-II Mandate for Retrofitment Across N2, N3, M2, M3 Categories

Implementing AIS-151 Stage-II compels medium- and heavy-duty vehicles on Indian roads to install TPMS. Compliance inspection is linked to annual fitness certificates, making adoption a non-optional cost item for fleet budgets. Suppliers gain multi-year demand visibility and can plan localized manufacturing, inventory, and last-mile distribution. Enforcement certainty also improves financing prospects for domestic sensor makers, encouraging capacity expansion. Early adoption clusters in Tamil Nadu, Karnataka, and Maharashtra create reference customers that accelerate diffusion into adjacent markets. The regulation further normalizes TPMS fitment for light-commercial fleets, even though they are not legally required to do so.

Growth of E-commerce & DIY Tyre-Maintenance Culture

Online marketplaces like Flipkart and Amazon recorded double-digit growth in TPMS kit sales as younger male buyers aged 15-35 increasingly bypass brick-and-mortar stores. Transparent pricing, peer reviews, and step-by-step installation videos reduce information asymmetry and lower perceived risk for first-time buyers. Independent garages in Tier-2 and Tier-3 cities bulk-order sensors online to shorten lead times and widen SKU choices. Rising technical literacy among vehicle owners fosters a do-it-yourself ethos that substitutes labor cost with personal time, widening the addressable base. These factors shift value capture from physical dealers toward digital platforms that bundle payment, warranty, and logistics.

Price-Sensitive Consumer Mindset

A TPMS kit typically costs INR 5,000-10,000 (USD 54-108), a meaningful discretionary outlay when many owners already postpone routine maintenance. Surveys indicate 68% of drivers defer non-essential vehicle upgrades during economic uncertainty. Rural and semi-urban households, where disposable income is lower, often prioritize visible accessories such as infotainment over unseen safety electronics. Replacing the battery every 5-7 years adds a recurring cost, reinforcing hesitation. Southern and western states with higher per-capita incomes show better conversion rates, but sustained price promotions or financing schemes remain critical for nationwide diffusion.

Other drivers and restraints analyzed in the detailed report include:

- Heavier EV/CNG Vehicles Raising Tyre-Safety Sensitivity

- Expansion of Organised Service Chains Bundling Smart TPMS

- Counterfeit Low-Cost Sensor Influx Hurting Trust

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Direct sensors accounted for 68.17% of the Indian aftermarket TPMS market share in 2025, underscoring fleet preference for +-1 PSI accuracy that satisfies insurer data-logging requirements, thereby reinforcing the India aftermarket TPMS market share advantage for valve-mounted technology. Continental's Bengaluru line now ships second-generation units rated for 7-10 year battery endurance, lowering lifetime service costs. Yet, Indirect platforms are forecast to grow at a 21.17% CAGR through 2031 as hatchback and sedan owners adopt ABS-based inference to stay under the INR 5,000 (USD 54) installation threshold, expanding the India aftermarket TPMS market footprint among first-time buyers.

Indirect adoption is further normalized by Maruti Suzuki's 2026 range, which offers wheel-speed-based alerts across mid-tier trims. However, limited precision and the need for manual resets after rotations limit their utility for long-haul trucks, keeping Direct systems the backbone of predictive maintenance contracts and preserving the Indian aftermarket TPMS market's premium in commercial niches.

Stand-alone displays retained 58.83% of the Indian aftermarket TPMS market share in 2025, signaling a large installed base that values one-time outlays. Smart TPMS platforms, however, are growing at a 21.42% CAGR, exporting data to cloud dashboards that unlock fuel-savings analytics; this dynamic positions connected sensors as the fastest value compounder in the Indian aftermarket TPMS market.

Shriram General Insurance cuts premiums by 10-15% for fleets that maintain tire pressure within tolerance for 95% of operating hours, validating the payback on telematics subscriptions. As 5G coverage expands, latency falls, and over-the-air firmware updates become routine, the Indian aftermarket TPMS industry is moving toward data-driven services rather than hardware margins.

List of Companies Covered in this Report:

- Sensata Technologies (Schrader)

- Continental AG

- Treel Mobility (JK Tyre)

- Steelmate Co Ltd

- Blaupunkt India

- Alligator Ventilfabrik GmbH

- CUB Elecparts Inc.

- Hamaton Automotive

- Dill Air Controls

- Bartec Auto ID

- TyreSense (Transense)

- SensAiry (Tymtix)

- Goodyear SightLine

- Bridgestone Webfleet TPMS

- CEAT Smart Tyre

- Michelin TPMS Solutions

- Manatec Electronics

- JK Automotive Sensors

- Autel Intelligent TPMS

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AIS-151 Stage-II Mandate For Retro-Fitment Across N2, N3, M2, M3 Categories

- 4.2.2 Growth of E-commerce & DIY Tire Maintenance Culture

- 4.2.3 Heavier EV/CNG Vehicles Raising tire-Safety Sensitivity

- 4.2.4 Expansion of Organized Service Chains Bundling Smart TPMS

- 4.2.5 SME Fleet Digitization To Curb Tire-Related OPEX

- 4.2.6 Insurance Telematics Discounts For TPMS-Equipped Vehicles

- 4.3 Market Restraints

- 4.3.1 Price-Sensitive Consumer Mindset

- 4.3.2 Counterfeit Low-Cost Sensor Influx Hurting Trust

- 4.3.3 Shortage Of Trained Technicians For Direct-TPMS Calibration

- 4.3.4 Inter-Operability Issues With OE Infotainment Units

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Type

- 5.1.1 Direct TPMS

- 5.1.2 Indirect TPMS

- 5.2 By Technology Integration

- 5.2.1 Stand-alone TPMS Units

- 5.2.2 Smart / Connected TPMS

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.1.1 Hatchbacks

- 5.3.1.2 Sedans

- 5.3.1.3 Sport Utility Vehicles (SUVs) & Multi-Utility Vehicles (MUVs)

- 5.3.2 Commercial Vehicles

- 5.3.2.1 Light Commercial Vehicles

- 5.3.2.2 Medium & Heavy Commercial Vehicles

- 5.3.2.3 Buses & Coaches

- 5.3.1 Passenger Cars

- 5.4 By Distribution Channel

- 5.4.1 Offline

- 5.4.2 Online

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Sensata Technologies (Schrader)

- 6.4.2 Continental AG

- 6.4.3 Treel Mobility (JK Tyre)

- 6.4.4 Steelmate Co Ltd

- 6.4.5 Blaupunkt India

- 6.4.6 Alligator Ventilfabrik GmbH

- 6.4.7 CUB Elecparts Inc.

- 6.4.8 Hamaton Automotive

- 6.4.9 Dill Air Controls

- 6.4.10 Bartec Auto ID

- 6.4.11 TyreSense (Transense)

- 6.4.12 SensAiry (Tymtix)

- 6.4.13 Goodyear SightLine

- 6.4.14 Bridgestone Webfleet TPMS

- 6.4.15 CEAT Smart Tyre

- 6.4.16 Michelin TPMS Solutions

- 6.4.17 Manatec Electronics

- 6.4.18 JK Automotive Sensors

- 6.4.19 Autel Intelligent TPMS

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

歐洲售後市場胎壓監測系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)美國售後市場胎壓監測系統:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)中國售後市場胎壓監測系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

歐洲售後市場胎壓監測系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)美國售後市場胎壓監測系統:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)中國售後市場胎壓監測系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) 2026年全球智慧拖車輪胎壓力監測系統(TMPS)和遠端資訊處理市場報告

2026年全球智慧拖車輪胎壓力監測系統(TMPS)和遠端資訊處理市場報告 輪胎壓力監測系統市場:2026年至2032年全球市場預測(依產品類型、組件、銷售管道、最終用戶及車輛類型分類)

輪胎壓力監測系統市場:2026年至2032年全球市場預測(依產品類型、組件、銷售管道、最終用戶及車輛類型分類) 輪胎壓力監測系統市場報告:按類型、技術、車輛類型、銷售管道和地區分類(2026-2034 年)

輪胎壓力監測系統市場報告:按類型、技術、車輛類型、銷售管道和地區分類(2026-2034 年) 汽車輪胎壓力監測系統市場:依產品類型、車輛類型、銷售管道和地區分類2026年全球先進胎壓監測系統市場報告2026年全球汽車輪胎壓力監測系統市場報告2026年全球高壓熔斷器監測模組市場報告

汽車輪胎壓力監測系統市場:依產品類型、車輛類型、銷售管道和地區分類2026年全球先進胎壓監測系統市場報告2026年全球汽車輪胎壓力監測系統市場報告2026年全球高壓熔斷器監測模組市場報告