|

市場調查報告書

商品編碼

2062093

無顆粒電工鋼板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Non Grain Electric Steel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

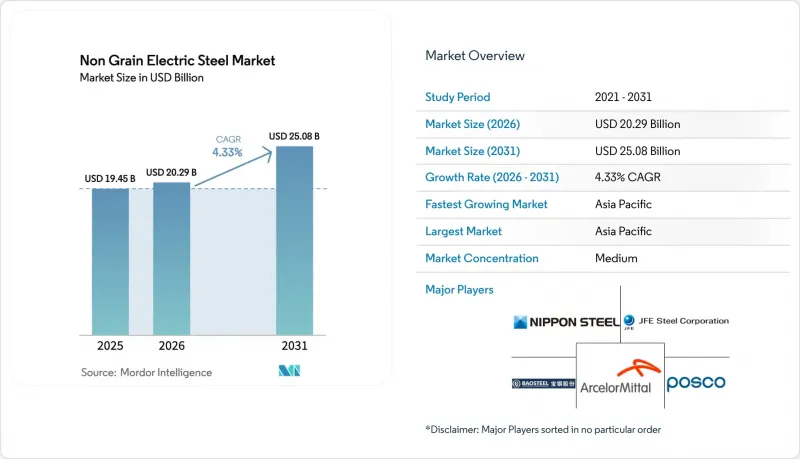

根據 Mordor Intelligence 預測,無顆粒電工鋼板的市場規模預計將從 2025 年的 194.5 億美元和 2026 年的 202.9 億美元成長到 2031 年的 250.8 億美元,2026 年至 2031 年的複合年成長率為 4.33%。

本報告按類型(成品和半成品)、應用(馬達、變壓器、電感器和電抗器等)、終端用戶產業(能源和公共產業、汽車和電動汽車、工業製造等)以及地區(亞太地區、北美地區、歐洲地區、南美地區以及中東和非洲地區)進行細分。市場預測以美元計價。

全球無粒電工鋼板市場趨勢及洞察

擴大電動車生產

2025年上半年,比亞迪電池式電動車(BEV)和插電式混合動力車(PHEV)的銷售量超過214.6萬輛,顯示驅動馬達的需求正在快速成長。在印度,2024年電動車銷量達到208萬輛,並計畫在2030年實現30%的市場滲透率,屆時將需要大量的充電站、變電站和配電變壓器,而這些設施都使用非晶粒電工鋼片(NGOES)鐵芯。中國於2025年4月實施的稀土礦出口限制將限制釹的供應,迫使汽車製造商轉向使用電工鋼片疊片而非永久磁鐵的電勵磁同步馬達。浦項鋼鐵(POSCO)的目標是到2030年每年生產750萬個馬達鐵芯,這表明整車製造商(OEM)正在尋求垂直整合以確保線圈供應。高速 800 伏特牽引馬達的運作頻率高於 1000 Hz,在這個頻率範圍內,鐵芯損耗與頻率的平方成正比,因此厚度為 0.20–0.27 毫米的鋼板不僅是一種選擇,而且是一種必需品。

可再生能源和風力發電機的擴張

2024年,全球新增風電裝置容量達114.3吉瓦。其中,中國貢獻了79.4吉瓦,佔全球總量的69.4%。 2024年,離岸風力發電機的額定功率平均接近10兆瓦,另有16-26兆瓦的平台進入商業競標,每個平台都需要使用數噸級的發電機鐵芯和變壓器組。由於電工鋼板供不應求,變壓器價格較2018年上漲了75%。這是因為鋼鐵廠的產能無法滿足全球整體待併網再生能源的需求,目前全球待併網可再生能源裝置容量已超過1,650吉瓦。不使用稀土元素的電勵磁發電機使得每台發電機使用的非晶態鋼板(NGOES)用量增加了20%,從而緩解了小型變壓器中非晶態鐵芯佔比下降的問題。在歐盟和亞太地區的政策支持下,資本持續流入離岸風力發電叢集,而這些集群不可避免地需要高品質的非政府組織級設施。

非晶態材料與奈米晶合金之間的競爭

2026年6月,日立金屬公司在南卡羅來納州康威市開始商業化生產其2605HB1M非晶帶材,該材料可將變壓器空載損耗降低至取向矽鋼的三分之一。 HB1M-LL牌號在1.42特斯拉、60赫茲的條件下,損耗可降低至0.19瓦/公斤,比傳統非晶產品提升20%至40%。日立目前已佔據非晶鐵芯市場57%的佔有率,該市場2024年價值8.65億美元,日立的目標是到2032年實現6.9%的複合年成長率。由於其脆性和較低的飽和磁通極限,這種帶材目前僅限於5兆伏安或以下的繞線鐵芯,但電力公司正在修改其配電變壓器的規格,以滿足美國能源局(DOE)更嚴格的能源效率標準。對於 NGOES 製造商而言,對旋轉機械的需求仍然強勁,但這正在削弱它們在低功率設備市場的佔有率。

細分市場分析

到2025年,全加工鋼捲將佔非晶態電工鋼板市場佔有率的56.11%,預計到2031年將以5.36%的複合年成長率成長,因為交付廠更傾向於無需額外退火即可沖壓的鋼捲。全加工非晶態電工鋼板的市場規模正在擴大,這反映了汽車製造商垂直整合的趨勢,例如比亞迪的自有疊片沖壓加工能力以及浦項製鐵移動解決方案公司750萬片鋼芯的目標。

在汽車牽引馬達、IE4/IE5工業驅動器和汽車充電器等領域,對厚度低至0.10毫米且具有認證鐵損的超薄鋼板的需求日益成長。新日鐵住金株式會社(Nippon Steel & Sumitomo Metal)的廣畑和瀨戶內生產線已投入運作,總投資達2130億日元;阪神和八幡生產線計劃於2027年前投產,這表明為保持競爭力,各公司需要進行必要的資本投資。在大型同步發電機中,半成品鋼片仍然很常見,因為這些設備需要在現場進行應力消除處理。

區域分析

預計到2025年,亞太地區將佔全球銷售額的47.11%,成為非晶態電工鋼板市場的主要驅動力,並有望在2031年之前維持5.49%的複合年成長率。中國2024年新增79.4吉瓦風電裝置容量以及印度不斷擴展的電動車生態系統,都將支撐該地區的需求。廣畑鋼鐵廠、瀨戶內鋼鐵廠以及浦項鋼鐵浦項移動生產線產能的提升,確保了豐田、現代和比亞迪等汽車項目的本地化供應。

在北美,由於第 48C 條款稅額扣抵和「購買美國貨」條款,需求正在轉向克利夫蘭克利夫斯、紐柯和安賽樂米塔爾的鋼鐵廠,而日立金屬的康威帶狀工廠則將該地區定位為非晶態核心基地。

歐洲的需求主要受歐盟生態設計IE4法規和REPower EU採購規則的驅動。蒂森克虜伯的「Bluemint」和福斯鋼聯的「Greentech」鋼材正在助力該地區向低碳冶金轉型,而根特和林伍德則為大眾汽車和Stellantis的動力總成項目提供鋼材。

在南美、中東和非洲,國內軋延線短缺、外匯波動、對進口的依賴是主要障礙。然而,巴西工業的電氣化和沙烏地阿拉伯的NEOM大型企劃正在為能夠獲得ESG認證的出口商創造一些機會。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 擴大電動車生產

- 可再生能源和風力發電設施的開發

- 用於高速馬達的薄壁奈米管

- 關於變壓器鐵心國內採購價格的規定

- 利用數位雙胞胎進行升級

- 市場限制因素

- 非晶態材料與奈米晶合金之間的競爭

- 向「綠色」鋼鐵替代品轉型,受環境、社會和治理(ESG)驅動。

- 下一代驅動系統中的氫脆風險

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 完全加工產品

- 半成品

- 透過使用

- 引擎

- 用於推進(電動車/軌道運輸)

- 工業(IE4/IE5、HVAC)

- 變壓器

- 電源

- 電力分配和電動汽車

- 發電機

- 電感器和電抗器

- 感測器和其他

- 引擎

- 按最終用戶行業分類

- 能源與公共產業

- 汽車和電動旅行

- 工業製造

- 電器產品

- 航太和電動垂直起降飛行器

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Ansteel Group Corporation Limited

- ArcelorMittal

- Baoshan Iron & Steel Co. Ltd.

- Cleveland-Cliffs Inc.

- Gerdau S/A

- JFE Steel Corporation

- JSW

- LIBERTY Steel Group

- NIPPON STEEL CORPORATION

- NLMK

- POSCO

- Shandong Iron and Steel Group Co., Ltd.

- Shougang Group

- Tata Steel

- thyssenkrupp AG

- United States Steel Corporation

- voestalpine Stahl GmbH

第7章 市場機會與未來展望

According to Mordor Intelligence, the non grain electric steel market size is projected to expand from USD 19.45 billion in 2025 and USD 20.29 billion in 2026 to USD 25.08 billion by 2031, registering a CAGR of 4.33% between 2026 to 2031.

This report is Segmented by Type (Fully-Processed and Semi-Processed), Application (Motors, Transformers, Inductors and Reactors, and More), End-User Industry (Energy and Utilities, Automotive and E-Mobility, Industrial Manufacturing, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Non Grain Electric Steel Market Trends and Insights

Electric Vehicle Production Expansion

Battery-electric and plug-in hybrid sales surpassed 2.146 million units at BYD in the first half of 2025, illustrating how rapidly traction-motor demand is compounding. India's 2.08 million EV sales in 2024 and a 30% penetration goal by 2030 will require large numbers of charging stations, substations, and distribution transformers, all of which use NGOES cores. China's April 2025 export controls on rare-earth minerals restrict neodymium supplies and push automakers toward electrically excited synchronous motors that replace permanent magnets with extra electrical-steel laminations. POSCO's target of 7.5 million motor cores a year by 2030 showcases vertical integration as OEMs safeguard coil supply. High-speed 800-volt traction motors operate above 1,000 hertz, where core loss scales with frequency squared, making 0.20-0.27 millimeter gauges a necessity rather than an option.

Renewable and Wind-Turbine Build-Out

Global wind additions reached 114.3 gigawatts in 2024, driven by China's 79.4 gigawatt build that alone accounted for 69.4% of the total. Offshore turbine ratings climbed toward 10 megawatts on average in 2024, with 16-26 megawatt platforms entering commercial tenders, each using multi-ton generator cores and transformer banks. Electrical-steel shortages lifted transformer prices 75% over 2018 levels as mill capacity lags renewable interconnection queues that now top 1,650 gigawatts worldwide. Electrically excited generators that sidestep rare-earth magnets boost NGOES content per turbine by up to 20%, cushioning the loss of share to amorphous cores in small transformers. Policy support in the EU and APAC continues to funnel capital toward offshore wind clusters that are, by necessity, hungry for premium NGOES grades.

Competition from Amorphous and Nano-Crystalline Alloys

Hitachi Metals started commercial output of 2605HB1M amorphous ribbons at Conway, South Carolina in June 2026, delivering no-load transformer losses barely one-third of grain-oriented silicon steel. The HB1M-LL grade pushes loss down to 0.19 W/kg at 1.42 Tesla and 60 Hz, a 20-40% improvement on earlier amorphous products. Hitachi already controlled 57% of the amorphous-core segment worth USD 865 million in 2024 and aims for 6.9% CAGR through 2032. Although brittleness and low saturation flux limit ribbons to wound cores under 5 MVA, utilities chasing tighter DOE efficiency standards are shifting distribution-transformer specifications accordingly. For NGOES producers this erodes share in small-power units even as rotating-machine demand stays intact.

Other drivers and restraints analyzed in the detailed report include:

- Thin-Gauge NGOES for High-Speed Motors

- Domestic-Content Rules for Transformer Cores

- ESG-Driven Shift to "Green" Steel Alternatives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fully processed grades held 56.11% of non grain electric steel market share in 2025 and are projected to grow at 5.36% CAGR to 2031 as OEMs favor coils that arrive ready for punching without extra annealing. The non-grain electric steel market size for fully processed, reflecting automaker vertical-integration moves such as BYD's in-house lamination stamping and POSCO Mobility Solution's 7.5 million-core goal.

Automotive traction motors, IE4/IE5 industrial drives, and on-board chargers increasingly demand ultra-thin gauges down to 0.10 mm with certified core loss. Investments totaling JPY 213 billion brought Nippon Steel's Hirohata and Setouchi lines online and will add Hanshin and Yawata by 2027, showing the capex race needed to stay relevant. Semi-processed grades remain common in large synchronous generators that undergo site-specific stress relief.

Geography Analysis

Asia-Pacific dominated the non grain electric steel market with 47.11% revenue in 2025 and will log a 5.49% CAGR to 2031. China's 79.4 GW of new wind in 2024 and India's expanding EV ecosystem underpin the region's appetite. Capacity additions at Hirohata, Setouchi, and POSCO's Pohang mobility line ensure local supply for Toyota, Hyundai, and BYD programs.

In North America, Section 48C credits and Buy America clauses redirect demand to Cleveland-Cliffs, Nucor, and ArcelorMittal mills, while Hitachi Metals' Conway ribbon plant positions the region as an amorphous-core hub.

Europe's demand is by Ecodesign IE4 mandates and REPowerEU sourcing rules. Thyssenkrupp's Bluemint and Voestalpine's Greentec steel reinforce the bloc's push toward low-carbon metallurgy, while Gent and Ringwood supply Volkswagen and Stellantis traction programs.

South America, and Middle-East and Africa are hampered by scarce domestic rolling lines, currency swings, and import dependence. Nevertheless, Brazil's industrial electrification and Saudi Arabia's NEOM megaproject offer selective upside for exporters able to certify ESG credentials.

- Ansteel Group Corporation Limited

- ArcelorMittal

- Baoshan Iron & Steel Co. Ltd.

- Cleveland-Cliffs Inc.

- Gerdau S/A

- JFE Steel Corporation

- JSW

- LIBERTY Steel Group

- NIPPON STEEL CORPORATION

- NLMK

- POSCO

- Shandong Iron and Steel Group Co., Ltd.

- Shougang Group

- Tata Steel

- thyssenkrupp AG

- United States Steel Corporation

- voestalpine Stahl GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Electric Vehicle production expansion

- 4.2.2 Renewable and wind-turbine build-out

- 4.2.3 Thin-gauge NGOES for high-speed motors

- 4.2.4 Domestic-content rules for transformer cores

- 4.2.5 Digital-twin-driven grade upgrades

- 4.3 Market Restraints

- 4.3.1 Competition from amorphous and nano-crystalline alloys

- 4.3.2 ESG-driven shift to "green" steel alternatives

- 4.3.3 Hydrogen-embrittlement risk in next-gen drives

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Fully-processed

- 5.1.2 Semi-processed

- 5.2 By Application

- 5.2.1 Motors

- 5.2.1.1 Traction (EV/rail)

- 5.2.1.2 Industrial (IE4/IE5, HVAC)

- 5.2.2 Transformers

- 5.2.2.1 Power

- 5.2.2.2 Distribution and EV on-board

- 5.2.3 Generators

- 5.2.4 Inductors and Reactors

- 5.2.5 Sensors and Miscellaneous

- 5.2.1 Motors

- 5.3 By End-user Industry

- 5.3.1 Energy and Utilities

- 5.3.2 Automotive and E-mobility

- 5.3.3 Industrial Manufacturing

- 5.3.4 Consumer Appliances

- 5.3.5 Aerospace and eVTOL

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Ansteel Group Corporation Limited

- 6.4.2 ArcelorMittal

- 6.4.3 Baoshan Iron & Steel Co. Ltd.

- 6.4.4 Cleveland-Cliffs Inc.

- 6.4.5 Gerdau S/A

- 6.4.6 JFE Steel Corporation

- 6.4.7 JSW

- 6.4.8 LIBERTY Steel Group

- 6.4.9 NIPPON STEEL CORPORATION

- 6.4.10 NLMK

- 6.4.11 POSCO

- 6.4.12 Shandong Iron and Steel Group Co., Ltd.

- 6.4.13 Shougang Group

- 6.4.14 Tata Steel

- 6.4.15 thyssenkrupp AG

- 6.4.16 United States Steel Corporation

- 6.4.17 voestalpine Stahl GmbH

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

電工鋼:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

電工鋼:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 電工鋼板市場:依材質、產品類型、厚度範圍、表面絕緣系統和應用分類-2026-2032年全球市場預測無取向電工鋼板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

電工鋼板市場:依材質、產品類型、厚度範圍、表面絕緣系統和應用分類-2026-2032年全球市場預測無取向電工鋼板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) 全球電工鋼板市場規模、佔有率、趨勢及成長分析報告(2026-2034年)

全球電工鋼板市場規模、佔有率、趨勢及成長分析報告(2026-2034年) 全球電工鋼市場:按類型、應用、終端用戶產業和地區分類-預測至2031年

全球電工鋼市場:按類型、應用、終端用戶產業和地區分類-預測至2031年 非光學電氣鋼板(NOES)市場預測至2034年-按類型、厚度、應用、最終用戶和地區分類的全球分析

非光學電氣鋼板(NOES)市場預測至2034年-按類型、厚度、應用、最終用戶和地區分類的全球分析 電工鋼板市場:按類型、應用和地區分類

電工鋼板市場:按類型、應用和地區分類 2026 年至 2035 年電工鋼板塗層市場的商業機會、成長要素、產業趨勢分析與預測。

2026 年至 2035 年電工鋼板塗層市場的商業機會、成長要素、產業趨勢分析與預測。 電工鋼板市場規模、佔有率、趨勢和預測:按類型、應用、最終用途行業和地區分類,2026-2034年2026-2034年全球取向矽鋼片市場規模、佔有率、趨勢與成長分析報告

電工鋼板市場規模、佔有率、趨勢和預測:按類型、應用、最終用途行業和地區分類,2026-2034年2026-2034年全球取向矽鋼片市場規模、佔有率、趨勢與成長分析報告