|

市場調查報告書

商品編碼

2038377

2026 年至 2035 年電工鋼板塗層市場的商業機會、成長要素、產業趨勢分析與預測。Electrical Steel Coatings Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

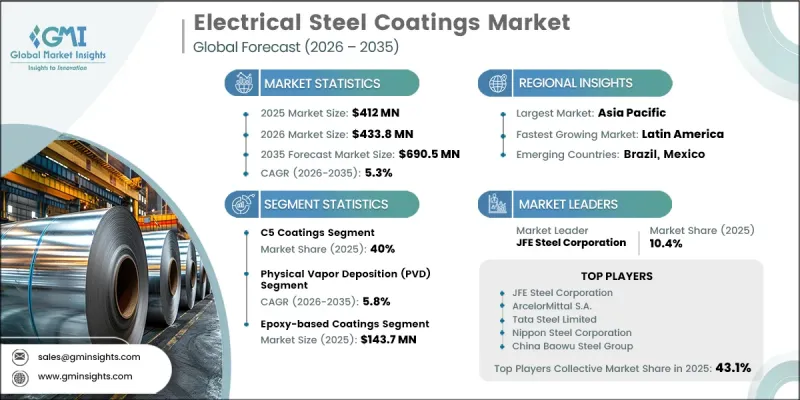

2025 年全球電工鋼板塗層市場價值為 4.12 億美元,預計到 2035 年將以 5.3% 的複合年成長率成長至 6.905 億美元。

在全球電氣化轉型、永續性目標以及塗層技術不斷進步的推動下,電工鋼板市場正經歷快速發展。汽車電氣化、可再生能源系統和工業機械日益成長的需求,進一步推動了對高性能電工鋼板塗層的需求,以提高效率並減少能源損耗。製造商越來越重視符合環保標準的解決方案,包括無鉻和無甲醛配方,以滿足更嚴格的環境標準和永續性。技術進步正在重塑生產方式;無電電鍍因其成本效益而被廣泛應用,而物理氣相沉積 (PVD) 和化學氣相沉積 (CVD) 則擴大應用於高精度、高性能領域。材料創新也在加速發展,環氧樹脂和聚酯塗層因其介電強度高且價格實惠而佔據主導地位,而對鉻基塗層的需求則持續下降。陶瓷、氧化鎂和混合塗層系統的新發展正在提高耐久性、熱穩定性和環境性能。從鋼材類型來看,取向電工鋼(GOES)因其優異的磁效率,仍然是變壓器應用中不可或缺的材料;而非取向電工鋼(NOES)在電機應用領域,尤其是在電動車領域,正迅速普及。變壓器仍然佔據大部分需求,但電機,特別是電動車驅動系統,正在成為成長最快的領域。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 4.12億美元 |

| 預計金額 | 6.905億美元 |

| 複合年成長率 | 5.3% |

預計到2025年,C5塗層市佔率將達到40%,並在2035年之前以5.7%的複合年成長率成長。 C3和C5等塗層等級仍廣泛應用於馬達和變壓器的絕緣和抗沖壓性能要求。 C5A和C5AS等先進等級的塗層具有更高的附著力和更薄的塗層厚度,有助於提高電氣系統的運作效率。隨著電動車和小型化電氣設備的普及,對用於次世代應用程式的超薄塗層解決方案的需求正在顯著成長。

預計到2025年,取向矽鋼(GOES)市場規模將達到2.431億美元,並在2026年至2035年間以5.3%的複合年成長率成長。與其他鋼種相比,取向矽鋼具有優異的磁性能和較低的鐵損,因此在變壓器應用中繼續發揮重要作用。相較之下,非晶態矽鋼(NOES)由於其均勻的磁性和動態應用的適用性,在包括電動車系統在內的馬達領域得到了越來越廣泛的應用。

預計2026年至2035年,北美電工鋼板塗層市場將以6%的複合年成長率成長。這一區域成長主要得益於持續的電網現代化改造、可再生能源基礎設施投資的增加以及電動車的日益普及。對先進變壓器和馬達的強勁需求進一步推動了市場擴張,而日益嚴格的環境法規加速了環保塗層技術的轉型。持續的技術創新和成熟製造商的存在預計將進一步支持該地區市場的發展。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 市場機遇

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 按塗層類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:塗料類型,2022-2035年

- C5塗層

- C6塗層

- C4塗層

- C3塗層

- C2塗層

- 其他塗層

第6章 市場估算與預測:依塗層技術分類,2022-2035年

- 物理氣相沉積(PVD)

- 化學氣相沉積(CVD)

- 無電電鍍

第7章 市場估計與預測:依材料成分分類,2022-2035年

- 環氧樹脂漆

- 含鉻塗料

- 聚酯基塗料

- 無鉻塗料

- 酚醛塗料

- 無甲醛塗料

- 氧化鎂基塗料

- 其他材料類型

第8章 市場估算與預測:依電工鋼板類型分類,2022-2035年

- 取向電工鋼板(GOES)

- 無取向電工鋼板(NOES)

- 矽鋼

第9章 市場估計與預測:依應用領域分類,2022-2035年

- 變壓器

- 電動機

- 發電機

- 電感器

- 其他用途

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第11章:公司簡介

- JFE Steel Corporation

- ArcelorMittal SA

- Tata Steel Limited

- Nippon Steel Corporation

- China Baowu Steel Group

- POSCO Holdings Inc.

- Voestalpine AG

- Axalta Coating Systems

- Dorf Ketal Chemicals

- Chemetall GmbH(BASF)

The Global Electrical Steel Coatings Market was valued at USD 412 million in 2025 and is estimated to grow at a CAGR of 5.3% to reach USD 690.5 million by 2035.

The market is evolving rapidly, supported by the global push toward electrification, sustainability goals, and continuous advancements in coating technologies. Increasing demand from automotive electrification, renewable energy systems, and industrial machinery is reinforcing the need for high-performance electrical steel coatings that enhance efficiency and reduce energy losses. Manufacturers are increasingly prioritizing environmentally compliant solutions, including chrome-free and formaldehyde-free formulations, in response to stricter environmental standards and sustainability commitments. Technological advancements are reshaping production methods, with electroless plating continuing to be widely used due to cost efficiency, while physical vapor deposition and chemical vapor deposition are gaining adoption in high-precision and high-performance applications. Material innovation is also accelerating, with epoxy and polyester coatings leading due to their dielectric strength and affordability, while demand for chrome-based solutions continues to decline. Emerging developments in ceramic-based, magnesium oxide, and hybrid coating systems are improving durability, thermal stability, and environmental performance. From a steel type perspective, grain-oriented electrical steel (GOES) remains essential for transformer applications due to its superior magnetic efficiency, whereas non-grain-oriented electrical steel (NOES) is gaining strong traction in electric motor applications, particularly in electrified mobility. Transformers continue to dominate application demand, while electric motors, especially EV traction systems, are emerging as the fastest-growing segment.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $412 Million |

| Forecast Value | $690.5 Million |

| CAGR | 5.3% |

The C5 coatings segment accounted for 40% share in 2025 and is projected to grow at a CAGR of 5.7% through 2035. Coating classifications such as C3 and C5 remain widely adopted for insulation and punchability requirements in motors and transformers. Advanced variants such as C5A and C5AS offer improved anti-stick performance and reduced coating thickness, supporting higher operational efficiency in electrical systems. The growing shift toward electric mobility and compact electrical equipment is significantly boosting demand for ultra-thin coating solutions used in next-generation applications.

The grain-oriented electrical steel (GOES) segment accounted for USD 243.1 million in 2025 and is expected to grow at a CAGR of 5.3% between 2026 and 2035. GOES continues to play a critical role in transformer applications due to its superior magnetic properties and lower core losses compared to alternative steel types. In contrast, non-grain-oriented electrical steel (NOES) is increasingly being adopted in electric motors, including EV systems, due to its uniform magnetic characteristics and suitability for dynamic applications.

North America Electrical Steel Coatings Market is projected to grow at a CAGR of 6% during 2026-2035. Growth in the region is driven by ongoing grid modernization initiatives, rising investments in renewable energy infrastructure, and increasing adoption of electric vehicles. Strong demand for advanced transformers and electric motors is further strengthening market expansion, while stricter environmental regulations are accelerating the transition toward eco-friendly coating technologies. Continuous technological innovation and the presence of established manufacturers are expected to further support regional market development.

Key players operating in the Electrical Steel Coatings Market include JFE Steel Corporation, ArcelorMittal S.A., Tata Steel Limited, Nippon Steel Corporation, China Baowu Steel Group, POSCO Holdings Inc., Voestalpine AG, Axalta Coating Systems, Dorf Ketal Chemicals, and Chemetall GmbH (BASF). Companies in the Electrical Steel Coatings Market are focusing on expanding their technological capabilities and developing environmentally compliant formulations to meet tightening global regulations. Significant investment is being directed toward chrome-free, energy-efficient, and high-performance coatings that enhance electrical efficiency and reduce losses. Market participants are strengthening R&D efforts to improve coating precision, durability, and thermal resistance while aligning EV and renewable energy requirements. Strategic partnerships with steel manufacturers and automotive OEMs are being used to secure long-term supply agreements and integrate coatings into next-generation platforms. Players are also expanding production capacities in high-growth regions, particularly Asia Pacific, to support large-scale industrial demand.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Coating Type

- 2.2.3 Coating Technique

- 2.2.4 Material Composition

- 2.2.5 Electrical Steel Type

- 2.2.6 Application

- 2.3 TAM Analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By coating type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 LATAM

- 4.2.6 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Coating Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 C5 Coatings

- 5.3 C6 Coatings

- 5.4 C4 Coatings

- 5.5 C3 Coatings

- 5.6 C2 Coatings

- 5.7 Other Coatings

Chapter 6 Market Estimates and Forecast, By Coating Technique, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Physical Vapor Deposition (PVD)

- 6.3 Chemical Vapor Deposition (CVD)

- 6.4 Electroless Plating

Chapter 7 Market Estimates and Forecast, By Material Composition, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Epoxy-Based Coatings

- 7.3 Chrome-Containing Coatings

- 7.4 Polyester-Based Coatings

- 7.5 Chrome-Free Coatings

- 7.6 Phenolic-Based Coatings

- 7.7 Formaldehyde-Free Coatings

- 7.8 MgO-Based Coatings

- 7.9 Other Material Types

Chapter 8 Market Estimates and Forecast, By Electrical Steel Type, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Grain-Oriented Electrical Steel (GOES)

- 8.3 Non-Grain-Oriented Electrical Steel (NOES)

- 8.4 Silicon Steel

Chapter 9 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 Transformers

- 9.3 Electric Motors

- 9.4 Generators

- 9.5 Inductors

- 9.6 Other Applications

Chapter 10 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 JFE Steel Corporation

- 11.2 ArcelorMittal S.A.

- 11.3 Tata Steel Limited

- 11.4 Nippon Steel Corporation

- 11.5 China Baowu Steel Group

- 11.6 POSCO Holdings Inc.

- 11.7 Voestalpine AG

- 11.8 Axalta Coating Systems

- 11.9 Dorf Ketal Chemicals

- 11.10 Chemetall GmbH (BASF)

電工鋼板市場:依材質、產品類型、厚度範圍、表面絕緣系統和應用分類-2026-2032年全球市場預測

電工鋼板市場:依材質、產品類型、厚度範圍、表面絕緣系統和應用分類-2026-2032年全球市場預測 全球電工鋼板市場規模、佔有率、趨勢及成長分析報告(2026-2034年)

全球電工鋼板市場規模、佔有率、趨勢及成長分析報告(2026-2034年) 全球電工鋼市場:按類型、應用、終端用戶產業和地區分類-預測至2031年

全球電工鋼市場:按類型、應用、終端用戶產業和地區分類-預測至2031年 非光學電氣鋼板(NOES)市場預測至2034年-按類型、厚度、應用、最終用戶和地區分類的全球分析

非光學電氣鋼板(NOES)市場預測至2034年-按類型、厚度、應用、最終用戶和地區分類的全球分析 電工鋼板市場:按類型、應用和地區分類

電工鋼板市場:按類型、應用和地區分類 無顆粒電工鋼板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

無顆粒電工鋼板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 電工鋼板市場規模、佔有率、趨勢和預測:按類型、應用、最終用途行業和地區分類,2026-2034年2026-2034年全球取向矽鋼片市場規模、佔有率、趨勢與成長分析報告

電工鋼板市場規模、佔有率、趨勢和預測:按類型、應用、最終用途行業和地區分類,2026-2034年2026-2034年全球取向矽鋼片市場規模、佔有率、趨勢與成長分析報告 2026年全球無取向電工鋼市場報告2026年全球電工鋼市場報告

2026年全球無取向電工鋼市場報告2026年全球電工鋼市場報告