|

市場調查報告書

商品編碼

2061963

基於代理的AI在向量資料庫中的應用:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031年)Agentic AI Applications In Vector Database - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

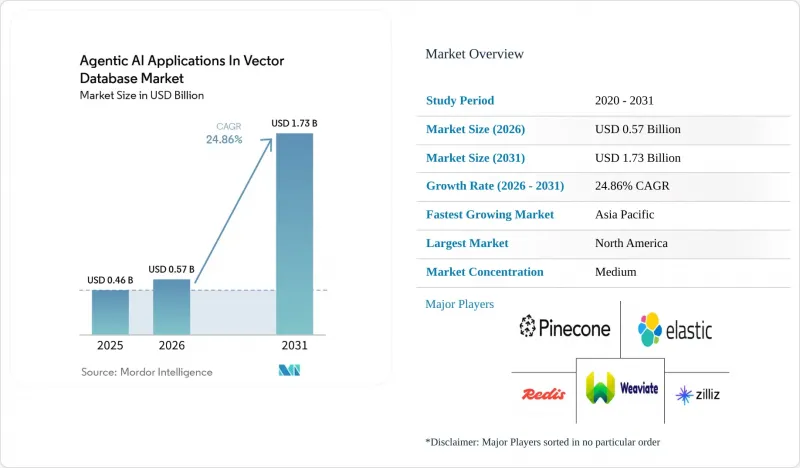

根據 Mordor Intelligence 預測,基於代理的 AI 應用在向量資料庫中的市場規模預計將從 2025 年的 4.6 億美元成長到 2026 年的 5.7 億美元,然後從 2026 年到 2031 年以 24.86% 的複合年成長率,到 2031 年達到 17.31 年達到 17.31 年達到 17.31 年。

本報告按部署模式(例如,雲端管理)、向量資料庫類型(例如,專用向量資料庫)、應用程式(例如,互動式人工智慧和搜尋增強產生)、最終用戶產業(例如,IT和電信、銀行、金融服務和保險、醫療保健和生命科學、零售和電子商務)以及地區進行細分。市場預測以價值(美元)表示。

基於代理的AI應用市場在向量資料庫領域的全球趨勢與洞察

大規模語言模式的普及推動了高維度搜尋的發展。

向量資料庫中基於代理人的AI應用市場正受益於大規模語言模型(LLM)從實驗性基礎設施轉向生產基礎設施的轉變。每個公司都將LLM推理與內部即時數據結合的流程,都需要能夠處理大量嵌入式資料並提供低延遲、穩定搜尋效能的向量索引。隨著許多組織不再標準化使用單一模型,而是支持在不同嵌入空間中運行的多個模型,這種壓力日益增大。這需要維護多個索引,從而增加了對同一環境中儲存、編配和計算的需求。 2026年1月,MongoDB推出了五種Voyage 4嵌入模型,其中包含多模態具有影片功能的多模態模型,並將它們整合到Atlas Vector Search中,以減少對外部嵌入呼叫的依賴。這些整合表明,向量資料庫中基於代理的AI應用市場正在隨著模型多樣化而擴展,而不是依賴單一的搜尋模式。

基於代理的人工智慧架構的興起增加了對持久性記憶體的需求。

向量資料庫中基於代理的AI應用市場也受到跨多個會話進行規劃、搜尋、推理和執行操作的代理系統的驅動。這些工作負載與靜態RAG(隨機可用性群組)不同,因為它們可以針對單一任務執行數千次向量搜尋,並且可以在任務執行期間將新記憶體寫回系統。 Qdrant在2026年4月指出,雖然生產環境中的代理循環每個工作流程會產生數千個查詢,但傳統的RAG工作負載仍然要輕得多。企業還要求完全可觀測性、審計追蹤和存取控制,因為代理的每個操作都必須能夠向其內部管治團隊解釋。 Amazon Bedrock AgentCore於2025年10月正式發布,透過引入持久記憶體、語意搜尋和原生OpenTelemetry可觀測性,提高了企業採用的標準。因此,向量資料庫中基於代理的AI應用市場更青睞那些不僅提供搜尋速度,而且兼顧效能和管治的供應商。

對於包含數十億筆記錄的索引,運算和儲存成本很高。

隨著部署規模從數百萬向量擴展到數十億向量,基於代理的向量資料庫中的人工智慧應用市場正面臨切實的成本限制。 HNSW索引仍然是記憶體密集型的,即使在對1536維、10億向量的資料集進行量化之前,也需要大量的RAM。這推高了託管雲端的成本,可能使中型企業以及同時測試多個代理商工作流程的企業難以負擔。 Qdrant重點介紹了二元量化技術,該技術可以將記憶體使用量降低到1/32,同時保持95%以上的召回率,但其優缺點仍取決於工作負載設計和對搜尋結果偏差的接受度。與靜態搜尋系統相比,頻繁的寫入操作會增加重建頻率和基礎設施負載,因此基於代理的記憶體系統面臨的壓力更為嚴峻。根據騰訊雲端預測,到2025年,其企業級向量資料庫每天將處理超過8,500億次騰訊內部營運的搜尋請求。這表明,擴展效率仍然集中在最大的幾家供應商手中。

細分市場分析

在基於向量資料庫代理的人工智慧應用市場,預計到2025年,雲端託管配置將佔據62.31%的市場佔有率。這主要歸功於買家對彈性、可控可用性和低基礎設施開銷的優先考慮。雲端託管服務透過在平台內處理索引、擴展、容錯移轉和計劃維護等工作,縮短了人工智慧團隊的部署時間。這種模式也符合企業的採購行為,因為向量搜尋擴大被整合到更廣泛的人工智慧訂閱服務中,而不是作為獨立系統購買。 Amazon Bedrock AgentCore 透過將持久記憶體和語義搜尋整合到託管服務堆疊中,進一步鞏固了這一趨勢。

在基於向量資料庫代理的AI應用市場中,自託管配置在醫療保健、政府和高度監管的企業環境中仍然至關重要,因為資料儲存和管理仍然至關重要。隨著企業尋求類似雲端的營運模式,同時又不失去對自身執行環境的控制,混合配置預計到2031年將以24.81%的複合年成長率成長。 Zilliz透過其BYOC-I和BYOC Azure選項直接滿足了這一需求,這些選項允許客戶將引擎保留在自己的租用戶中,同時保持廠商支援和託管更新。這進一步鞏固了混合部署在面向多區域企業的基於向量資料庫代理的AI應用市場中作為預設架構的地位,而非一種妥協方案。

在向量資料庫市場,專為高維度相似性搜尋而建立的專用向量資料庫預計到 2025 年將佔基於代理的 AI 應用的 55.73%。它們的價值在延遲要求嚴格、索引規模龐大且即使在生產負載下也必須保持穩定搜尋品質的場景中尤為顯著。 Qdrant 報告顯示,對於 768 維的 100 萬個向量,p50查詢延遲為 3 毫秒,p99 延遲為 14 毫秒,這表明專用引擎對於核心工作負載仍然具有吸引力。支援向量的關係型和文件型儲存也依然重要,因為它們允許企業在不引入新的基礎架構層的情況下,為現有應用資料庫添加語義搜尋功能。

在基於代理的AI應用領域,面向向量資料庫的嵌入式和邊緣向量儲存預計將以28.33%的複合年成長率成長至2031年,因為AI推理正變得越來越接近實際應用場景。 2025年7月,Qdrant發布了行動裝置、機器人和資源受限硬體的進程內向量庫「Qdrant Edge」。隨後,在2026年4月,Actian發布了從Raspberry Pi系統到企業邊緣伺服器等各種環境的「VectorAI DB」。由於該細分市場能夠透過本地搜尋降低延遲、支援離線執行並滿足資料最小化要求,因此在基於代理的AI應用領域,面向向量資料庫的這一細分市場正蓬勃發展。

區域分析

在基於代理的向量資料庫人工智慧應用市場,預計到2025年,北美將佔據41.11%的市場佔有率,並繼續保持最大的區域收入基礎。這主要歸功於企業人工智慧在北美的大規模應用和生產部署速度遠超其他大多數地區。美國透過在金融服務、醫療保健和企業軟體領域的大規模部署,推動了區域支出成長;加拿大則透過研究叢集和新創企業生態系統加強了支持力度。墨西哥也透過拓展近岸技術服務以及在區域交付中心推廣人工智慧驅動的客戶參與平台做出了貢獻。該地區的監管要求也影響了產品設計,託管供應商已經開始添加針對醫療保健行業的合規功能,以支援在美國的部署。

在基於代理的AI應用資料庫,亞太地區是成長最快的地區,預計到2031年市場規模將以23.97%的複合年成長率成長。中國是主要的需求中心,這得益於國內AI基礎設施投資的不斷成長。騰訊雲端宣布,到2025年,其企業級向量資料庫在騰訊營運範圍內每天將處理超過8,500億次搜尋請求。日本透過知識管理和合規性搜尋等大型企業應用情境創造了需求,儘管部署數量較少,但合約金額很高。印度擁有大規模的開發者群體和IT服務產業,為市場成長提供了支持,並且正在加強對公共和企業級RAG(紅黃綠)計畫中向量平台的評估。韓國正在加強其在嵌入式部署方面的作用,因為製造商正在使用基於代理的AI進行品管和供應鏈工作流程,而這些都依賴於本地向量儲存。

歐洲在基於代理的向量資料庫人工智慧應用市場中扮演著獨特的角色。這是因為GDPR和歐盟人工智慧法規促使買家優先考慮本地部署基礎設施和更強大的管治功能。 2026年3月,Zilliz正式發布了BYOC Azure,該方案使用客戶管理的加密金鑰,直接滿足了客戶管理環境中的主權要求。雖然南美洲的規模仍然較小,但隨著雲端投資在全部區域不斷擴大,巴西已成為一個重要的樞紐。在中東和非洲,主權人工智慧計畫正在推動相關領域的發展,阿布達比的「Stargate UAE」計畫正在建造一個1吉瓦的運算基礎設施,預計首批200兆瓦將於2026年第二季投入運作。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 大規模語言模式的普及推動了高維度搜尋的發展。

- 基於代理的人工智慧架構的興起,增加了對持久性記憶體的需求。

- 將原生向量功能整合到其人工智慧堆疊中的雲端供應商

- 利用開放原始碼向量引擎降低整體擁有成本

- 邊緣人工智慧的普及正在推動對嵌入式向量儲存的需求。

- 創業投資的湧入正在加速產品創新。

- 市場限制因素

- 缺乏標準化基準和互通性

- 對於包含數十億筆記錄的索引,運算和儲存成本很高。

- 資料主權法規限制跨境載體共用

- 熟練的向量相似性工程師短缺

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 部署模式

- 雲端管理

- 自託管

- 混合

- 按向量資料庫類型

- 專用向量資料資料庫

- 支援向量的關係/文檔存儲

- 嵌入式/邊緣向量存儲

- 透過使用

- 互動式人工智慧與搜尋增強生成

- 自主代理與工作流程編配

- 語義搜尋和建議

- 詐欺檢測和異常分析

- 生物資訊學和科學計算

- 按最終用戶行業分類

- 資訊科技/通訊

- BFSI

- 醫療保健和生命科學

- 零售與電子商務

- 媒體與娛樂

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Pinecone Systems Inc.

- Zilliz Inc.

- Semi Technologies BV(Weaviate)

- Elastic NV

- Redis Ltd.

- Chroma Inc.

- Qdrant GmbH

- Oracle Corporation

- MongoDB Inc.

- Neo4j, Inc.

- Microsoft Corporation

- Amazon Web Services, Inc.

- Google LLC

- IBM Corporation

- Databricks Inc.

- Snowflake Inc.

- Couchbase, Inc.

- Alibaba Cloud(Alibaba Group)

- Tencent Cloud

- Vespa.ai

第7章 市場機會與未來展望

According to Mordor Intelligence, the agentic AI applications market size in the vector database market is expected to grow from USD 0.46 billion in 2025 to USD 0.57 billion in 2026, and is forecast to reach USD 1.73 billion by 2031 at a 24.86% CAGR over 2026-2031.

This report is Segmented by Deployment Mode (Cloud-Managed, and More), Vector DB Type (Purpose-Built Vector Databases, and More), Application (Conversational AI and Retrieval-Augmented Generation, and More), End-User Industry (IT and Telecom, BFSI, Healthcare and Life Sciences, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Agentic AI Applications In Vector Database Market Trends and Insights

Proliferation Of Large Language Models Driving High-Dimensional Retrieval

Agentic AI applications in the vector database market are benefiting from the shift of large language models from experimentation to production infrastructure. Each enterprise pipeline that combines LLM inference with live internal data requires a vector index that can handle large embedding volumes with low, stable retrieval latency. The pressure is increasing because many organizations are no longer standardizing on a single model and are instead supporting several models that operate in different embedding spaces. That forces them to maintain multiple indexes and raises storage, orchestration, and compute demand inside the same environment. MongoDB introduced 5 Voyage 4 embedding models in January 2026, including a multimodal option with video capability, and integrated them into Atlas Vector Search to reduce dependence on external embedding calls. That kind of integration shows how the agentic AI applications in the vector database market are expanding alongside model diversity rather than around a single retrieval pattern.

Rise of Agentic AI Architectures Necessitating Persistent Memory Stores

The agentic AI applications in the vector database market are also being pushed forward by agentic systems that plan, retrieve, reason, and act across multiple sessions. These workloads differ from static RAG because they can execute thousands of vector lookups for one task and also write new memory back into the system while the task is still active. Qdrant stated in April 2026 that production agent loops generate multi-thousand queries per workflow, while traditional RAG workloads remain much lighter. Enterprises also expect full observability, audit trails, and access controls because every agent action must be explainable to internal governance teams. Amazon Bedrock AgentCore reached general availability in October 2025, introducing persistent memory, semantic retrieval, and native OpenTelemetry observability, raising the baseline for enterprise deployments. As a result, the agentic AI applications in the vector database market are favoring providers that combine performance with governance rather than solely on retrieval speed.

High Compute And Storage Costs For Billion-Scale Indexes

Agentic AI applications in the vector database market face a real cost ceiling as deployments move from millions of vectors to billions. HNSW indexes remain memory-intensive, and a 1-billion-vector dataset with 1,536 dimensions requires substantial RAM before quantization is even applied. That pushes managed cloud spending to levels that can weaken the business case for mid-market users and for enterprises testing multiple agent workflows simultaneously. Qdrant highlights binary quantization that cuts memory use by 32x while preserving more than 95% recall, but the tradeoff still depends on workload design and tolerance for retrieval drift. The pressure is sharper for agent memory systems because frequent writes increase rebuild frequency and infrastructure load compared with static retrieval systems. Tencent Cloud said its enterprise vector database handled more than 850 billion daily retrieval requests across internal Tencent businesses in 2025, which shows how scale efficiency remains concentrated among the largest operators.

Other drivers and restraints analyzed in the detailed report include:

- Cloud Providers Embedding Native Vector Capabilities Into AI Stacks

- Open-Source Vector Engines Lowering Total Cost of Ownership

- Lack of Standardized Benchmarks And Interoperability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Within the agentic AI applications market for vector databases, cloud-managed deployments held a 62.31% share in 2025, as buyers favored elasticity, managed availability, and low infrastructure overhead. Cloud-managed services shorten deployment time for AI teams by handling indexing, scaling, failover, and routine maintenance within the platform. The model also fits enterprise buying behavior because vector retrieval is increasingly bundled into broader AI subscriptions rather than purchased as a separate system. Amazon Bedrock AgentCore reinforced that pattern in 2025 by combining persistent memory and semantic retrieval inside a managed service stack.

In the agentic AI applications market for vector databases, self-hosted deployments remain relevant in healthcare, government, and heavily regulated enterprise environments where residency and control remain central. Hybrid deployments are projected to expand at a 24.81% CAGR through 2031 as organizations seek cloud-like operations without losing control of the execution environment. Zilliz positioned directly into that demand with BYOC-I and BYOC Azure options that let customers keep the engine inside their own tenant while retaining vendor support and managed updates. That makes hybrid less of a compromise and more of a default architecture for the agentic AI applications in the vector database market across multi-region enterprises.

Within the vector database market, purpose-built vector databases captured 55.73% of the agentic AI applications share in 2025 because they are designed from the ground up for high-dimensional similarity search. Their value is strongest where latency targets are tight, index sizes are large, and retrieval quality must remain stable under production load. Qdrant reported p50 query latency of 3 milliseconds and p99 latency of 14 milliseconds for 1 million vectors at 768 dimensions, which illustrates why purpose-built engines remain attractive for core workloads. Vector-enabled relational and document stores still matter because they let enterprises add semantic retrieval to existing application databases without introducing another infrastructure layer.

In the agentic AI applications market for vector databases, embedded and edge vector stores are forecast to grow at a 28.33% CAGR through 2031 as AI inference moves closer to the point of action. Qdrant launched Qdrant Edge in July 2025 as an in-process vector library for mobile devices, robots, and resource-constrained hardware. Actian followed in April 2026 with VectorAI DB, aimed at environments ranging from Raspberry Pi systems to enterprise edge servers. This segment is gaining ground in the agentic AI applications market for the vector databases because local search reduces latency, supports offline execution, and meets data minimization requirements.

Geography Analysis

Within the agentic AI applications market for vector databases, North America held a 41.11% share in 2025 and remained the leading regional revenue base, as enterprise AI deployments moved into production earlier than in most other regions. The United States led regional spending through large rollouts across financial services, healthcare, and enterprise software, while Canada added support through its research clusters and startup ecosystem. Mexico also contributed through the expansion of nearshore technology services and the wider use of AI-enabled customer engagement platforms in regional delivery centers. The region's regulatory demands are also shaping product design, and managed vendors have already added healthcare-focused compliance features to support U.S. adoption.

Within the agentic AI applications in the vector database market, Asia-Pacific is the fastest-growing region, and the market size in the region is projected to grow at a 23.97% CAGR through 2031. China is a major demand center because domestic AI infrastructure investment is growing, and Tencent Cloud said its enterprise vector database handled more than 850 billion daily retrieval requests across internal Tencent businesses in 2025. Japan is building demand through large-enterprise knowledge management and compliance retrieval use cases that carry high contract value even when deployment counts remain lower. India is supporting growth through its large developer base and IT services sector, which is increasingly evaluating vector platforms for public and enterprise RAG programs. South Korea is strengthening the region's role in embedded deployment because manufacturers are using agentic AI for quality control and supply chain workflows that depend on local vector stores.

Europe has a distinct role in the agentic AI applications market for vector databases because GDPR and the EU AI Act are pushing buyers toward resident infrastructure and stronger governance features. Zilliz made BYOC Azure with customer-managed encryption keys generally available in March 2026, directly addressing those sovereignty requirements within customer-controlled environments. South America remains smaller, with Brazil as the main node, as cloud investment expands across the region. Th Middle East and Africa are gaining momentum through sovereign AI programs, and the Stargate UAE project in Abu Dhabi is building a 1-gigawatt compute base,e with an initial 200 MW phase expected to be operational in Q2 2026.

- Pinecone Systems Inc.

- Zilliz Inc.

- Semi Technologies B.V. (Weaviate)

- Elastic N.V.

- Redis Ltd.

- Chroma Inc.

- Qdrant GmbH

- Oracle Corporation

- MongoDB Inc.

- Neo4j, Inc.

- Microsoft Corporation

- Amazon Web Services, Inc.

- Google LLC

- IBM Corporation

- Databricks Inc.

- Snowflake Inc.

- Couchbase, Inc.

- Alibaba Cloud (Alibaba Group)

- Tencent Cloud

- Vespa.ai

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of Large Language Models Driving High-Dimensional Retrieval

- 4.2.2 Rise of Agentic AI Architectures Necessitating Persistent Memory Stores

- 4.2.3 Cloud Providers Embedding Native Vector Capabilities into AI Stacks

- 4.2.4 Open-Source Vector Engines Lowering Total Cost of Ownership

- 4.2.5 Edge AI Adoption Spurring Demand for Embedded Vector Stores

- 4.2.6 Venture Capital Influx Accelerating Product Innovation

- 4.3 Market Restraints

- 4.3.1 Lack of Standardized Benchmarks and Interoperability

- 4.3.2 High Compute and Storage Costs for Billion-Scale Indexes

- 4.3.3 Data-Sovereignty Regulations Restricting Cross-Border Vector Sharing

- 4.3.4 Scarcity of Skilled Vector Similarity Engineers

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intenssity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-Managed

- 5.1.2 Self-Hosted

- 5.1.3 Hybrid

- 5.2 By Vector Database Type

- 5.2.1 Purpose-Built Vector Databases

- 5.2.2 Vector-Enabled Relational/Document Stores

- 5.2.3 Embedded/Edge Vector Stores

- 5.3 By Application

- 5.3.1 Conversational AI and Retrieval-Augmented Generation

- 5.3.2 Autonomous Agents and Workflow Orchestration

- 5.3.3 Semantic Search and Recommendation

- 5.3.4 Fraud Detection and Anomaly Analytics

- 5.3.5 Bioinformatics and Scientific Computing

- 5.4 By End-User Industry

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Retail and E-Commerce

- 5.4.5 Media and Entertainment

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Pinecone Systems Inc.

- 6.4.2 Zilliz Inc.

- 6.4.3 Semi Technologies B.V. (Weaviate)

- 6.4.4 Elastic N.V.

- 6.4.5 Redis Ltd.

- 6.4.6 Chroma Inc.

- 6.4.7 Qdrant GmbH

- 6.4.8 Oracle Corporation

- 6.4.9 MongoDB Inc.

- 6.4.10 Neo4j, Inc.

- 6.4.11 Microsoft Corporation

- 6.4.12 Amazon Web Services, Inc.

- 6.4.13 Google LLC

- 6.4.14 IBM Corporation

- 6.4.15 Databricks Inc.

- 6.4.16 Snowflake Inc.

- 6.4.17 Couchbase, Inc.

- 6.4.18 Alibaba Cloud (Alibaba Group)

- 6.4.19 Tencent Cloud

- 6.4.20 Vespa.ai

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026年全球對抗性學習市場報告

2026年全球對抗性學習市場報告 全球醫療、法律和監管 (MLR) 審查軟體市場:按組件、部署模式、組織規模、功能和審查內容類型分類-市場規模、產業趨勢、機會分析及 2026 年至 2035 年預測

全球醫療、法律和監管 (MLR) 審查軟體市場:按組件、部署模式、組織規模、功能和審查內容類型分類-市場規模、產業趨勢、機會分析及 2026 年至 2035 年預測 2026-2030年全球機械客戶市場

2026-2030年全球機械客戶市場 GPU加速卡:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)機器學習維運(MLops):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)人工智慧和機器學習:雲端人工智慧人工智慧與機器學習:雲端人工智慧市場數據概覽:2026年第二季度人工智慧和機器學習:邊緣人工智慧人工智慧與機器學習:邊緣人工智慧-市場數據概覽(2026 年第二季)AI和機器學習:TinyML

GPU加速卡:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)機器學習維運(MLops):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)人工智慧和機器學習:雲端人工智慧人工智慧與機器學習:雲端人工智慧市場數據概覽:2026年第二季度人工智慧和機器學習:邊緣人工智慧人工智慧與機器學習:邊緣人工智慧-市場數據概覽(2026 年第二季)AI和機器學習:TinyML