|

市場調查報告書

商品編碼

2061914

車床:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Lathe Machines - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

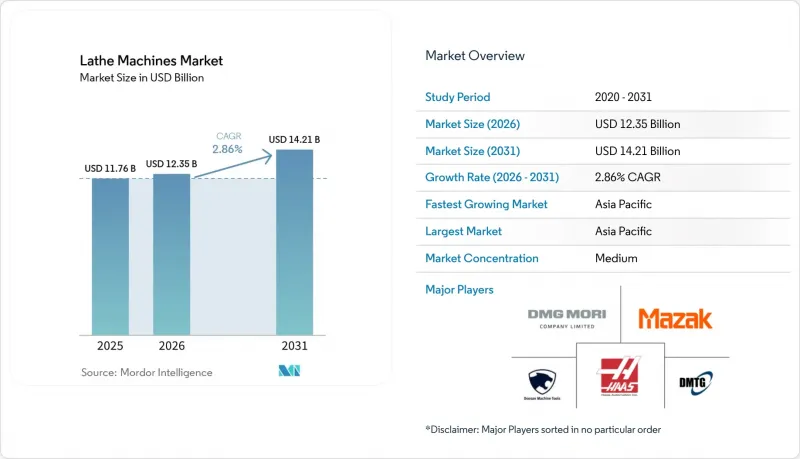

預計車床市場將從 2025 年的 117.6 億美元成長到 2026 年的 123.5 億美元,到 2031 年將達到 142.1 億美元,2026 年至 2031 年的複合年成長率為 2.86%。

本報告按產品類型(數控工具機、傳統工具機等)、工具機配置(水平、垂直等)、自動化程度(手動、半自動、全自動)、終端用戶產業(汽車、航太等)和地區(北美、南美、歐洲、亞太、中東和非洲)進行細分。市場預測(以金額為準,單位為十億美元)。

全球車床市場趨勢與洞察

航太零件製造需求不斷成長

受民航機產量增加、國防專案現代化以及太空經濟成長的推動,航太領域的需求為先進車削平台提供了結構性利好。近期產業分析預測,到2035年,該領域將實現顯著成長,其中民用航空將佔很大佔有率,而國防相關措施將增強整個商業週期的韌性。在英國,諸如全球作戰航空計畫(GCAP)等長期國防舉措預計將推動軍民兩用研發,並將成果延伸至精密製造和民用航太供應鏈。結合積層製造和減材製造流程的混合工作流程正成為許多飛行關鍵零件的標準配置,歐洲航空安全局(EASA)的指導方針強調,機械加工是實現認證介面和表面光潔度的重要後端工序。這些品質和認證標準正在推動對多軸車床、車銑複合機床以及支援小批量生產零缺陷的整合測量系統的需求。擴大折舊免稅額誘因的財政政策正在進一步加速主要航太供應商向自動化和數位化車床中心的升級。

汽車產業對引擎和變速箱零件的需求

儘管電氣化帶來了零件配置的變化,但汽車動力傳動系統加工仍然是CNC工具機和多軸車床的主要應用領域。在德國,預計2025年乘用車產量將達到415萬輛,比上年成長2%,但仍低於2019年的產量,預計到2026年初產量將趨於穩定。供應商不僅關注產量,也關注生產效率和加工複雜性。在美國,預計2025年汽車平均產量將達到1,018萬輛,其中輕型卡車佔比最大,這將維持對車軸、曲軸和傳動系統殼體的大量加工需求。電動車架構雖然減少了多級齒輪的數量,但卻對轉子軸、單速變速箱殼體和溫度控管部件產生了新的車削需求,改變了車床的工作負荷。這些變化有利於高度柔軟性的車銑複合機床和五軸平台,這些平台配備數位化加工循環,可在一次裝夾中完成齒輪切削、測量和研磨。隨著產品週期縮短和零件種類增多,車床市場正受益於資本向能夠適應設計變更而不延長前置作業時間的平台轉移。

對先進CNC車床的極高資本投入

資本密集是推廣應用的一大障礙,尤其對於訂單量不穩定、投資回收期短的中小型企業而言更是如此。入門級數控車床雖然能夠滿足基本需求,但高度監管的市場和高價值零件的加工則需要具備線性驅動、高剛性和整合測量獲利能力的高階多軸平台,這導致實施成本更高。刀具、工件夾持、整合和檢驗都會推高總擁有成本 (TCO),而推出初期人手不足造成的低運轉率也使投資決策更加複雜。隨著工廠從半自動化單元向全自動化單元擴展,包括應用工程和分階段自動化在內的供應商生態系統在論證投資合理性方面發揮核心作用。已公佈的先進加工平台價格範圍展現了投資概況,並強調了進行生命週期投資回報率 (ROI) 分析的必要性,該分析除了考慮表面加工週期時間外,還應涵蓋良率、運轉率和節能等因素。

細分市場分析

預計到2025年,CNC車床將佔據61.23%的市場佔有率,這反映了其在原型製作、多品種小批量生產以及對製程控制至關重要的受監管零件(確保認證供應)方面的多功能性。隨著買家尋求透過平行加工縮短複雜旋轉零件的加工週期,多軸平台預計也將實現6.23%的複合年成長率。先進的工具機以整合化為差異化優勢,將車削、銑削、齒輪加工、切削內測量和節能模式整合於一次裝夾中,從而縮短航太和醫療零件的前置作業時間。傳統引擎車床仍用於維修和維護,而立式轉塔車床則用於加工能源設備和重型機械中的大直徑、短長度工件。專用車床滿足特殊形狀和高度監管的細分市場需求,並透過客製化保持高價。在勞動力短缺以及加工流程簡化(除了金屬切削速度之外)價值日益成長的推動下,能夠消除二次加工的平台在車床市場正獲得越來越多的關注。

此外,混合型車銑床透過提供單一工件夾持路徑即可完成最終加工,並降低了因使用多個夾具而帶來的操作風險,從而模糊了不同工具機類別之間的界限。這種轉變與受監管行業的認證製造理念相契合,在這些行業中,可追溯性和進程內檢驗已成為必不可少的要求。買家不僅專注於主軸轉速,也重視全生命週期支援和應用專業知識。這種需求促使車床產業基於「功能叢集」對產品進行分類,這種分類方式比傳統的產品標籤更能準確地反映最終用戶的評價。因此,數控平台保持了其市場佔有率,而用於處理複雜零件組和縮短設計週期的多軸車床和混合系統的成長速度正在加快。

預計到2025年,臥式車床的市佔率將達到52.87%,主要得益於棒料送料生產和機器人工作負載處理應對力的提升。隨著買家整合生產系統以實現更嚴格的公差和縮短等待時間,多軸車床中心預計也將以5.41%的複合年成長率成長。對於法蘭、轉子和渦輪盤等大直徑工件,立式車床仍然至關重要,因為重力穩定性和堅固的工件夾持對於此類工件的加工至關重要。瑞士型車床正從傳統的細分市場擴展到醫療設備和精密緊固件等領域,這些領域普遍要求加工精度達到千分之一毫米以下,且外形規格較小。數位化循環和熱控制功能正成為高階機型的標配。因此,車床市場重視那些即使在長時間無人運作期間也能可靠地保持公差範圍的平台。

隨著供應商的角色不斷拓展,不僅要幫助原始設備製造商 (OEM) 解決產能過剩問題,還要支援新產品的快速上市,系統構成比正朝著更加靈活和整合化的方向發展。隨著零件設計迭代速度的加快,買家要求採用模擬、封閉回路型測量和預置加工循環等技術,以提高生產效率,同時保持品質和穩定的能耗。車削產業正持續向多軸解決方案轉型,這些方案能夠在不犧牲精度或主軸運作的前提下,適應零件形狀的變化。隨著數位化技術的進步和傳統程式設計障礙的減少,預計在預測期內,多軸解決方案在車削市場的佔有率將持續成長。

區域分析

預計到2025年,亞太地區將佔據全球車床市場48.12%的佔有率,並在2031年之前以6.91%的年均成長率持續成長,成為車床市場的區域驅動力。同時,多元化的製造業活動和政策支援正在推動汽車、電子和航太等行業供應商的產能擴張。日本和韓國持續出口先進的多軸和混合解決方案,樹立了性能標竿;而主要企業則在拓展產品系列,以適應製造業回流和供應商多元化的趨勢。東南亞精密產業叢集正在推動對棒料送料車削和小型精密零件的需求。預計該地區將在新設備部署方面保持主導地位,並在現有基礎設施建設和產能提升之間取得平衡。隨著資本配置跟隨電子和移動出行供應鏈的步伐,全部區域自動化和數位化工作流程的日益普及也帶動了車床市場的發展。

北美市場前景仍然穩定,重點在於汽車、航太和醫療價值鏈中的高價值零件和全生命週期服務。預計2025年美國汽車產量將保持高位,其中輕型卡車尤為突出,這將為傳動系統和底盤零件的重型車床加工提供支撐。公私合營和政策現代化正在優先發展整合工廠技術和人才培養,從而推動中小企業對互聯車床平台和模組化自動化的需求。聯邦政府的人才培養舉措旨在擴大技術工人的供應,隨著勞動力短缺的緩解,這有望刺激潛在的設備需求。這些因素與提升車床市場運轉率和合規性的功能升級密切相關。

歐洲仍然是重要的生產中心,擁有領導企業、主要的航太製造商和醫療叢集。預計到2025年,德國將生產415萬輛乘用車,即使電氣化改變了零件的要求,也能支撐對動力傳動系統加工的核心需求。英國長期國防計畫的投資支撐著一個精密製造生態系統,並惠及民用航太供應商及其加工合作夥伴。義大利和西班牙保持著大型車削和立式車削的生產能力,而北歐國家則在船舶和能源相關零件領域擁有獨特的優勢。在世界其他地區,中東的工業化計劃和南美的選擇性擴張正在創造進一步的成長機會。這些趨勢共同支撐著車削市場,歐洲市場專注於高價值細分市場和全生命週期支持,而其他地區則正在推動大規模應用。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 航太零件製造需求不斷成長

- 汽車產業對引擎和變速箱零件的需求

- 通用工程和合約製造業務的擴張

- 醫療設備製造業務成長

- 石油和天然氣設備的製造要求

- 擴大多軸加工中心與車銑複合機床的引進規模。

- 市場限制因素

- 對先進CNC車床的極高資本投入

- 熟練車床操作員和CNC編程人員嚴重短缺

- 客製化機器配置的前置作業時間較長

- 高黴菌和維護成本結構

- 價值供應鏈分析

- 技術展望

- 監理情勢

- 產業吸引力—五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 依產品類型

- CNC車床

- 傳統(機動)車床

- 多軸車床

- 立式轉塔車床(VTL)

- 專用車床

- 其他-轉塔式車床、桌上型車床、高速車床

- 透過機器配置

- 臥式車床

- 高架車床

- 多軸車床

- 瑞士型/走心式車床

- 按自動化級別

- 手動的

- 半自動

- 全自動

- 按最終用戶行業分類

- 車

- 航太/國防

- 通用機械製造

- 電子與電機工程

- 醫療器材

- 石油和天然氣

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 秘魯

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 比荷盧經濟聯盟(比利時、荷蘭、盧森堡)

- 北歐國家(丹麥、芬蘭、冰島、挪威、瑞典)

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東協(印尼、泰國、菲律賓、馬來西亞、越南)

- 其他亞太國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 科威特

- 土耳其

- 埃及

- 南非

- 奈及利亞

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- DMG Mori Co., Ltd.

- Yamazaki Mazak Corporation

- Haas Automation, Inc.

- Doosan Machine Tools Co., Ltd.

- Dalian Machine Tool Group Co., Ltd.

- Okuma Corporation

- Hyundai WIA Corporation

- JTEKT Corporation

- Hardinge Inc.

- Emco Group

- INDEX-Traub

- Citizen Machinery

- Spinner Maschinenbau

- Ace Micromatic Group

- Victor Taichung Machinery

- Hartford Machining Centres

- Maschinenfabrik Berthold Hermle

- Gildemeister Italiana

- Beijing Jingdiao Group

- Arrow Machine Tools

第7章 市場機會與未來展望

According to Mordor Intelligence, the lathe machines market size is expected to grow from USD 11.76 billion in 2025 to USD 12.35 billion in 2026 and is forecast to reach USD 14.21 billion by 2031 at 2.86% CAGR over 2026-2031.

This report is Segmented by Product Type (CNC, Conventional, and More), by Machine Configuration (Horizontal, Vertical, and More), by Automation Level (Manual, Semi-Automatic, Fully Automatic), by End-User Industry (Automotive, Aerospace, and More), and by Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). Market Forecasts in Value (USD Billion).

Global Lathe Machines Market Trends and Insights

Growing Aerospace Component Manufacturing Demand

Aerospace demand is a structural tailwind for advanced turning platforms, supported by rising commercial aviation output, defense program modernization, and a growing space economy. Recent industry analysis highlights substantial growth potential through 2035, with commercial aviation taking the larger share and defense initiatives adding resilience across cycles. In the United Kingdom, long-horizon defense initiatives such as the Global Combat Air Program are expected to stimulate precision manufacturing and dual-use R&D that spills into civilian aerospace supply chains. Additive to subtractive hybrid workflows have become standard for many flight-critical parts, with EASA guidance underscoring machining as a required post-process to achieve certified interfaces and finishes. These quality and certification norms reinforce demand for multi-axis lathes, turn mill centers, and integrated metrology that support zero defect execution at small batch sizes. Fiscal policies that improve capital allowances further catalyze upgrades to automation-ready, digitally enabled turning centers among aerospace suppliers in key markets.

Automotive Industry Demand for Engine and Transmission Components

Automotive powertrain machining remains a key use case for CNC and multi-spindle lathes, even as electrification reshapes component mixes. Germany produced 4.15 million passenger cars in 2025, which was a 2% year over year increase, though still below 2019 volumes, and early 2026 readings point to a near flat trajectory that keeps suppliers focused on productivity and complexity rather than volume alone. In the United States, motor vehicle assemblies averaged 10.18 million units in 2025, with light trucks comprising the bulk, which sustains heavy-duty turning for axles, crankshafts, and drivetrain housings. EV architectures change the lathe workload by reducing multi-speed gear counts while adding new turning needs such as rotor shafts, single-speed gearbox housings, and thermal management components. These shifts favor flexible turn mill centers and 5-axis capable platforms with digital cycles that integrate gear cutting, measuring, and grinding in the same setup. As model cycles shorten and part variety rises, the lathe machines market benefits from capital that moves toward platforms able to absorb design churn without extending lead times.

Extremely High Capital Investment for Advanced CNC Lathes

Capital intensity impedes adoption, especially for small and mid sized firms that face uneven order books and short payback thresholds. Entry level CNC turning can meet basic needs, yet regulated markets and high value parts push buyers toward premium multi axis platforms with linear drives, higher rigidity, and integrated measurement that raise acquisition costs. Tooling, workholding, integration, and validation add to the total cost of ownership, which complicates the business case when labor constraints reduce attainable utilization in the early ramp period. Supplier ecosystems that include application engineering and phased automation are now central to justify spend as shops scale from semi automatic to lights out cells. Published pricing ranges for advanced machining platforms illustrate the investment profile and reinforce the need for lifecycle ROI analysis that captures yield, uptime, and energy savings in addition to headline cycle time.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of General Engineering and Job Shop Operations

- Medical Device Manufacturing Growth

- Critical Shortage of Skilled Lathe Operators and CNC Programmers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

CNC lathes held 61.23% of 2025, reflecting their versatility for prototypes, high mix batches, and regulated parts where process control is critical to qualified supply, and multi spindle platforms are projected to record a 6.23% CAGR as buyers chase cycle time reduction on complex rotational parts through parallel operations. Integration is the differentiator as advanced machines combine turning, milling, gear cutting, in cut measurement, and energy saving modes within a single setup to compress lead times for aerospace and medical components. Conventional engine lathes persist in repair and maintenance, while vertical turret lathes serve large diameter, short length work in energy and heavy equipment. Special purpose lathes address outlier geometries and regulated niches that can sustain customization premiums. The lathe machines market favors platforms that can remove secondary steps because workforce scarcity elevates the value of process elimination in addition to raw metal removal rate.

The category lines are also blurring as turn mill hybrids present a single workholding path to final geometry and reduce handling risks tied to multiple fixtures. This shift aligns with validated manufacturing in regulated sectors, where traceability and in process confirmation are now table stakes. Buyers prioritize lifecycle support and application expertise rather than peak spindle ratings alone. These demands help the lathe machine industry segment its offerings by capability clusters, which more closely mirror end user evaluations than traditional product labels. The result is continued share for CNC platforms and faster growth for multi spindle and hybrid systems that align with complex part families and shorter design cycles.

Horizontal lathes accounted for 52.87% in 2025 on the strength of bar-fed production and compatibility with robotic loading, and multi-axis turning centers are forecast to grow at 5.41% CAGR as buyers consolidate operations for tighter tolerances and shorter queues. Vertical configurations remain essential for large diameter workpieces such as flanges, rotors, and turbine disks, where gravity-assisted stability and rigid workholding are critical. Swiss-type lathes are expanding beyond legacy niches to serve medical devices and precision fasteners where sub-thousandth tolerances and small form factors dominate. Digital cycles and thermal control additions are now standard expectations in the upper tier. As a result, the lathe machines market rewards platforms that can reliably hold tolerance bands through long unattended runs.

The configuration mix is shifting toward flexible and integrated systems because supplier roles have broadened to cover overflow capacity and rapid new product introduction support for OEMs. As part designs iterate faster, buyers require simulation, closed-loop measurement, and pre-built machining cycles that preserve quality while pushing throughput at stable energy draw. The lathe machine industry continues to move toward multi-axis solutions that accept volatility in part mix without giving up accuracy or spindle uptime. This tilt helps multi-axis solutions lift their share of the lathe machines market over the forecast period as digital adoption lowers historical programming barriers.

Geography Analysis

Asia Pacific accounted for 48.12% in 2025 and is projected to grow at 6.91% through 2031, making it the regional engine of the lathe machines market, while diversified manufacturing and policy support reinforce capacity expansion across automotive, electronics, and aerospace suppliers. Japan and South Korea continue to export advanced multi-axis and hybrid solutions that set performance benchmarks, and domestic champions in India expand their portfolios to address reshoring and vendor diversification. Precision clusters in Southeast Asia add demand for bar-fed turning and small-form precision parts. The region's balance of installed base and capability upgrades positions it to continue leading new equipment placements. As capital allocation follows electronics and mobility supply chains, the lathe machines market gains from the broader adoption of automation and digital workflows across APAC.

North America's outlook is stable as automotive, aerospace, and medical supply chains prioritize higher value parts and lifecycle service depth. U.S. motor vehicle assemblies remained elevated in 2025, with a light truck skew that supports heavy-duty turning for drivetrain and chassis components. Public-private programs and policy modernization emphasize integrated factory technologies and workforce development, which raise the appeal of connected turning platforms and modular automation among small and mid-sized firms. Federal workforce initiatives aim to expand the skilled trade pipeline, which can unlock latent equipment demand as staffing constraints ease. These drivers keep the lathe machines market tied to capability upgrades that enhance utilization and compliance.

Europe retains a significant base anchored by automotive leaders, aerospace primes, and medical clusters. Germany produced 4.15 million passenger cars in 2025, which sustained core demand for powertrain machining even as electrification changes part requirements. The United Kingdom's long-run defense program investment supports precision manufacturing ecosystems that ripple across civil aerospace suppliers and their machining partners. Italy and Spain maintain production strengths in heavy-duty and vertical turning, while the Nordics contribute niche capabilities in marine and energy parts. Across the rest of the world, industrialization agendas in the Middle East and selective expansions in South America provide incremental growth opportunities. Together, these trends support a lathe machines market where Europe emphasizes high-value segments and lifecycle support, while other regions drive volume placements.

- DMG Mori Co., Ltd.

- Yamazaki Mazak Corporation

- Haas Automation, Inc.

- Doosan Machine Tools Co., Ltd.

- Dalian Machine Tool Group Co., Ltd.

- Okuma Corporation

- Hyundai WIA Corporation

- JTEKT Corporation

- Hardinge Inc.

- Emco Group

- INDEX-Traub

- Citizen Machinery

- Spinner Maschinenbau

- Ace Micromatic Group

- Victor Taichung Machinery

- Hartford Machining Centres

- Maschinenfabrik Berthold Hermle

- Gildemeister Italiana

- Beijing Jingdiao Group

- Arrow Machine Tools

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Aerospace Component Manufacturing Demand

- 4.2.2 Automotive Industry Demand for Engine and Transmission Components

- 4.2.3 Expansion of General Engineering and Job Shop Operations

- 4.2.4 Medical Device Manufacturing Growth

- 4.2.5 Oil and Gas Equipment Manufacturing Requirements

- 4.2.6 Rising Adoption of Multi-Axis and Turn-Mill Centers

- 4.3 Market Restraints

- 4.3.1 Extremely High Capital Investment for Advanced CNC Lathes

- 4.3.2 Critical Shortage of Skilled Lathe Operators and CNC Programmers

- 4.3.3 Long Lead Times for Custom Machine Configurations

- 4.3.4 High Tooling and Maintenance Cost Structure

- 4.4 Value / Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Industry Attractiveness - Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value-In USD Billion)

- 5.1 By Product Type

- 5.1.1 CNC Lathe Machines

- 5.1.2 Conventional (Engine) Lathes

- 5.1.3 Multi-Spindle Lathes

- 5.1.4 Vertical Turret / Turning Lathes (VTLs)

- 5.1.5 Special-Purpose Lathes

- 5.1.6 Others - Capstan & Turret Lathes, Bench & Speed Lathes

- 5.2 By Machine Configuration

- 5.2.1 Horizontal Lathes

- 5.2.2 Vertical Lathes

- 5.2.3 Multi-Axis Turning Centres

- 5.2.4 Swiss-Type / Sliding-Head Lathes

- 5.3 By Automation Level

- 5.3.1 Manual

- 5.3.2 Semi-Automatic

- 5.3.3 Fully Automatic

- 5.4 By End-User Industry

- 5.4.1 Automotive

- 5.4.2 Aerospace & Defence

- 5.4.3 General Machinery Manufacturing

- 5.4.4 Electronics & Electrical

- 5.4.5 Medical Devices

- 5.4.6 Oil & Gas

- 5.4.7 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Peru

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.5.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 Kuwait

- 5.5.5.5 Turkey

- 5.5.5.6 Egypt

- 5.5.5.7 South Africa

- 5.5.5.8 Nigeria

- 5.5.5.9 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 DMG Mori Co., Ltd.

- 6.4.2 Yamazaki Mazak Corporation

- 6.4.3 Haas Automation, Inc.

- 6.4.4 Doosan Machine Tools Co., Ltd.

- 6.4.5 Dalian Machine Tool Group Co., Ltd.

- 6.4.6 Okuma Corporation

- 6.4.7 Hyundai WIA Corporation

- 6.4.8 JTEKT Corporation

- 6.4.9 Hardinge Inc.

- 6.4.10 Emco Group

- 6.4.11 INDEX-Traub

- 6.4.12 Citizen Machinery

- 6.4.13 Spinner Maschinenbau

- 6.4.14 Ace Micromatic Group

- 6.4.15 Victor Taichung Machinery

- 6.4.16 Hartford Machining Centres

- 6.4.17 Maschinenfabrik Berthold Hermle

- 6.4.18 Gildemeister Italiana

- 6.4.19 Beijing Jingdiao Group

- 6.4.20 Arrow Machine Tools

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

全球車床市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球車床市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 車床市場報告:按類型、操作方式、負載、最終用戶和地區分類,2026-2034 年

車床市場報告:按類型、操作方式、負載、最終用戶和地區分類,2026-2034 年 自動車床市場:按工具機類型、控制方式、操作方式、軸數、銷售管道、應用與最終用戶分類-2026-2032年全球市場預測車床市場:2026-2032年全球市場預測(依工具機類型、主軸方向、結構類型及最終用途產業分類)

自動車床市場:按工具機類型、控制方式、操作方式、軸數、銷售管道、應用與最終用戶分類-2026-2032年全球市場預測車床市場:2026-2032年全球市場預測(依工具機類型、主軸方向、結構類型及最終用途產業分類) 2026年全球車床市場報告

2026年全球車床市場報告 印度車床市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

印度車床市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 車床市場規模、佔有率和成長分析(按類型、操作方式、產能、最終用戶和地區分類)-2026-2033年產業預測

車床市場規模、佔有率和成長分析(按類型、操作方式、產能、最終用戶和地區分類)-2026-2033年產業預測 2032 年車床市場預測:按產品類型、營運類型、營運模式、最終用戶和地區進行的全球分析

2032 年車床市場預測:按產品類型、營運類型、營運模式、最終用戶和地區進行的全球分析 氣舉閥工作筒市場報告:趨勢、預測和競爭分析(至 2030 年)

氣舉閥工作筒市場報告:趨勢、預測和競爭分析(至 2030 年)