|

市場調查報告書

商品編碼

2060418

歐洲熱噴塗市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)Europe Thermal Spray - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

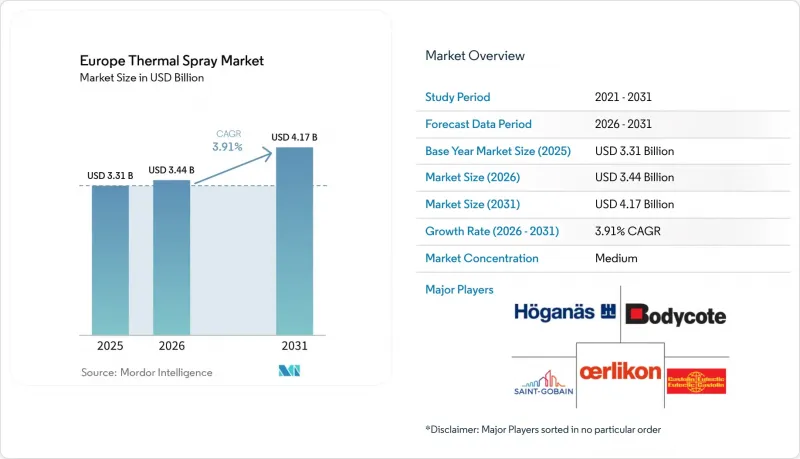

據 Mordor Intelligence 稱,2025 年歐洲熱噴塗市場價值為 33.1 億美元,預計到 2031 年將從 2026 年的 34.4 億美元成長至 41.7 億美元,預測期(2026-2031 年)複合年成長率為 3.91%。

本報告按產品類型(塗料、材料、設備)、製程類型(燃燒、電能)、終端用戶產業(航太、工業用燃氣渦輪機、汽車、電子、石油天然氣、醫療設備、能源電力、鋼鐵製造、紡織、印刷造紙)和地區(德國、英國、法國、義大利等)進行細分。市場預測以美元計價。

歐洲熱噴塗市場趨勢與洞察

用於植入的醫用級Ti-HA塗層

預計到2030年,歐洲65歲及以上人口將佔總人口的近三分之一,因此,整形外科和人工植牙製造商正在擴大等離子噴塗鈦(Ti)和羥基磷灰石(HA)塗層的應用。這些技術進步顯著縮短了癒合時間,並減少了再次手術的需求。懸浮等離子噴塗技術的進步使得亞微米級HA粉末的精細加工成為可能。這種粉末與天然骨礦物質非常相似,並符合嚴格的ISO 13779-2認證標準。雖然由於將植入耐久性與醫院支付掛鉤的製度改革,市場需求不斷成長,但一個令人擔憂的趨勢也正在出現。超過一半的鈦粉仍然來自北美僅有的兩家供應商,這加劇了供應鏈的脆弱性。

歐盟對渦輪機和鍋爐的脫碳義務

根據歐盟《清潔工業公約》,營運商必須在2030年前大幅減少排放。為實現這一目標,營運商正在對燃氣渦輪機進行改造,加裝钆和鋯酸鑭熱障塗層(TBC)。這些塗層旨在承受一定濃度的氫氣混合物。在荷蘭一家聯合循環發電廠進行的初步測試表明,其耐久性顯著提高。此外,強調鍋爐高效率的《建築指令》正在加速MCrAlY黏結層的更換。

機器人整合噴塗單元的高資本支出 (CAPEX)

對於小規模工廠而言,自動化單位往往價格高昂,難以負擔,因為它們無法將成本分攤到足夠的銷售收入中。租賃提供了一種解決方案,可以將高額的前期成本(資本支出:CAPEX)轉化為負擔較輕的持續成本(營運支出:OPEX)。然而,這種便利性是有補償的:使用者需要依賴昂貴的耗材,以擠壓利潤空間。除了財務風險外,從冷噴塗系統到更新的HVAF技術的過渡週期很短(僅用了幾年時間),這進一步加劇了設備快速過時的風險。

細分市場分析

至2025年,塗料將主導歐洲熱噴塗市場,佔77.13%的市場。這一主導地位凸顯了塗料的消耗性以及航太領域頻繁的檢修週期。同時,設備領域也呈現上升趨勢,預計在2026年至2031年的預測期內將以3.95%的複合年成長率成長。這一成長主要得益於原始設備製造商(OEM)推動噴塗單元的數位化和即時診斷技術的整合。歐瑞康的預測性維護模組有望為歐洲熱噴塗市場的設備領域帶來好處。這些先進的模組不僅能夠實現備件的自動訂購,還有助於提升售後市場收入。介於塗料和設備之間的材料領域也正在蓬勃發展,部分原因是霍根哈斯公司近期推出了「Amperit 678」和「685」兩種新型塗料。這些新材料符合產業在 REACH 法規的推動下減少鎳和鈷用量的趨勢。

歐洲熱噴塗產業的價格趨勢有明顯差異。航太級熱障塗層粉末價格高昂,而工業級碳化鎢的價格則相對較低。此外,除塵系統和重力式給料機已從輔助工具發展成為符合標準所需的設備。這種轉變主要歸功於ISO 45001標準的實施,該標準強調對亞微米顆粒的捕集。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 用於植入的醫用級鈦(Ti)和羥磷石灰(HA)塗層。

- 歐盟對渦輪機和鍋爐的脫碳義務

- 快速採用HVOF陶瓷塗層技術開發電動車轉子塗層

- AI最佳化的噴塗路徑演算法減少了廢料。

- 歐盟對風力發電機維修工程中耐磨塗層的需求正在激增。

- 市場限制因素

- 機器人整合噴塗單元需要高資本投入

- YSZ和稀土元素氧化物供應短缺。

- 受 ESG(環境、社會和治理)因素的驅動,噴漆房逐步淘汰甲烷燃料。

- 價值鏈分析

- 波特五力模型

第5章:預測市場規模與成長率

- 依產品類型

- 塗層

- 材料

- 塗層材料

- 粉末

- 陶瓷

- 金屬

- 聚合物

- 其他塗層材料

- 粉末

- 線材/棒材

- 其他材料

- 塗層材料

- 熱噴塗裝置

- 熱噴塗系統

- 除塵器

- 噴槍噴嘴

- 送料裝置

- 備用零件

- 隔音機殼

- 其他熱噴塗設備

- 依工藝類型

- 燃燒類型

- 電能類型

- 按最終用戶行業分類

- 航太

- 工業用燃氣渦輪機

- 車

- 電子設備

- 石油和天然氣

- 醫療設備

- 能源與電力

- 煉鋼

- 纖維

- 印刷和造紙

- 按地區

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 俄羅斯

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 生產熱噴塗用粉末的公司

- Air Products and Chemicals, Inc.

- AMETEK

- C&M Technologies GmbH

- CASTOLIN EUTECTIC

- CRS Holdings Inc.

- Diffusion Engineers Limited

- Fujimi Corporation

- Global Tungsten & Powders

- HC Starck

- HAI Inc

- Hoganas AB

- Kennametl Stellite

- Linde plc

- Metallisation Limited

- OC Oerlikon Management AG

- Saint-Gobain

- Sandvik AB

- The Fisher Barton Group

- Treibacher Industrie AG

- 專門從事熱噴塗塗層的公司

- APS Materials, Inc.

- ARC International

- Bodycote

- CASTOLIN EUTECTIC

- Chromalloy Gas Turbine LLC

- Fujimi Corporation

- Kennametl Stellite

- Linde plc

- Metallisation Limited

- OC Oerlikon Management AG

- Pamarco

- Surface Dynamics

- The Fisher Barton Group

- 熱噴塗設備公司

- Air Products and Chemicals, Inc.

- Camfil Air Pollution Control

- CASTOLIN EUTECTIC

- Donaldson Company Inc.

- Flame Spray Technologies BV

- GTV-wear GmbH

- HAI Inc

- Kennametl Stellite

- Kurt J. Lesker Company

- Linde plc

- Metallisation Limited

- OC Oerlikon Management AG

- Saint-Gobain

- The Lincoln Electric Company

- 生產熱噴塗用粉末的公司

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe thermal spray market size was valued at USD 3.31 billion in 2025 and is estimated to grow from USD 3.44 billion in 2026 to reach USD 4.17 billion by 2031, at a CAGR of 3.91% during the forecast period (2026-2031).

This report is Segmented by Product Type (Coatings, Materials, and Equipment), Process Type (Combustion and Electric Energy), End-User Industry (Aerospace, Industrial Gas Turbines, Automotive, Electronics, Oil and Gas, Medical Devices, Energy and Power, Steel Making, Textile, and Printing and Paper), and Geography (Germany, UK, France, Italy, and More). Market Forecasts are Provided in Value (USD).

Europe Thermal Spray Market Trends and Insights

Medical-Grade Ti and HA Coatings for Implants

With Europe's over-65 population set to reach nearly one-third by 2030, orthopedic and dental implant manufacturers are increasingly adopting plasma-sprayed titanium and hydroxyapatite layers. These advancements are notably shortening healing times and diminishing the necessity for revision surgeries. The evolution of suspension plasma spray now adeptly handles sub-micron HA powders, closely resembling natural bone minerals and adhering to the rigorous ISO 13779-2 certification standards. While reforms tying hospital payments to implant longevity have increased demand, a worrisome trend surfaces: over half of titanium powder is still procured from merely two North American suppliers, amplifying supply vulnerabilities.

EU Decarbonization Mandates for Turbines and Boilers

Operators, under the EU Clean Industrial Deal, face a 2030 deadline for significant emissions reductions. In response, they are retrofitting turbines with gadolinium- and lanthanum-zirconate thermal barrier coatings (TBCs), which are designed to withstand specific volumes of hydrogen blends. Early tests in Dutch combined-cycle plants have highlighted notable durability enhancements. Furthermore, the Energy Performance of Buildings Directive, which emphasizes high boiler efficiency, is accelerating the replacement cycle for MCrAlY bond coats.

High CAPEX of Robot-Integrated Spray Cells

Small shops often find automated cells prohibitively expensive, as they are unable to distribute the costs over sufficient sales. Leasing offers a solution, converting a significant upfront cost (capital expenditure - CAPEX) into a more digestible ongoing expense (operational expenditure - OPEX). However, this convenience comes at a price, as users become tethered to costly consumables, which squeeze their profit margins. Adding to the financial stakes, the swift transition from cold-spray systems to the newer HVAF technology, just a few years apart, amplifies the risks of rapid obsolescence.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Uptake of HVOF Ceramic Coatings for EV Rotors

- Surging Demand for Wear-Resistant Coatings in Wind-Turbine Rebuilds

- Supply Tightness of YSZ and Rare-Earth Oxides

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, coatings took center stage in the European thermal spray market, securing a dominant 77.13% share. This dominance highlights the consumable nature of coatings and the aerospace sector's regular overhaul cycles. Meanwhile, the equipment segment is on an upward trajectory, with projections indicating a 3.95% CAGR growth during the forecast period of 2026-2031. This anticipated growth is fueled by OEMs' initiatives to digitize spray cells and integrate real-time diagnostics. The equipment segment of Europe's thermal spray market is set to benefit from Oerlikon's predictive-maintenance modules. These advanced modules not only trigger automatic spare-part orders but also boost aftermarket revenue. Positioned between coatings and equipment, materials are gaining momentum, thanks in part to Hoganas' recent introductions of Amperit 678 and 685. These new materials resonate with the industry's pivot towards reducing nickel and cobalt, a shift driven by REACH mandates.

Price dynamics in the European thermal spray sector showcase a clear disparity. Aerospace TBC powders fetch premium prices, while industrial tungsten-carbide grades are priced more modestly. Additionally, dust-collection systems and gravimetric feeders have evolved from secondary tools to vital compliance instruments. This transformation is primarily attributed to ISO 45001 enforcement, which emphasizes the capture of sub-micron particulates.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Medical-grade Ti and HA coatings for implants

- 4.2.2 EU decarbonisation mandates for turbines and boilers

- 4.2.3 Rapid uptake of HVOF ceramic coatings for EV rotors

- 4.2.4 AI-optimised spray-path algorithms cut scrap

- 4.2.5 Surging demand for wear-resistant coatings in European Union wind-turbine rebuilds

- 4.3 Market Restraints

- 4.3.1 High CAPEX of robot-integrated spray cells

- 4.3.2 Supply tightness of YSZ and rare-earth oxides

- 4.3.3 ESG-driven phase-out of methane fuel in spray booths

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Coatings

- 5.1.2 Materials

- 5.1.2.1 Coating Materials

- 5.1.2.1.1 Powders

- 5.1.2.1.1.1 Ceramics

- 5.1.2.1.1.2 Metals

- 5.1.2.1.1.3 Polymer

- 5.1.2.1.1.4 Other Coating Materials

- 5.1.2.1.1 Powders

- 5.1.2.2 Wires/Rods

- 5.1.2.3 Other Materials

- 5.1.2.1 Coating Materials

- 5.1.3 Thermal-Spray Equipment

- 5.1.3.1 Thermal Spray Coating System

- 5.1.3.2 Dust Collection Equipment

- 5.1.3.3 Spray Gun and Nozzle

- 5.1.3.4 Feeder Equipment

- 5.1.3.5 Spare Parts

- 5.1.3.6 Noise-reducing Enclosure

- 5.1.3.7 Other Thermal Spray Equipment

- 5.2 By Process Type

- 5.2.1 Combustion

- 5.2.2 Electric Energy

- 5.3 By End-user Industry

- 5.3.1 Aerospace

- 5.3.2 Industrial Gas Turbines

- 5.3.3 Automotive

- 5.3.4 Electronics

- 5.3.5 Oil and Gas

- 5.3.6 Medical Devices

- 5.3.7 Energy and Power

- 5.3.8 Steel Making

- 5.3.9 Textile

- 5.3.10 Printing and Paper

- 5.4 By Geography

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 NORDICS Countries

- 5.4.7 Russia

- 5.4.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Thermal Spray Powder Companies

- 6.4.1.1 Air Products and Chemicals, Inc.

- 6.4.1.2 AMETEK

- 6.4.1.3 C&M Technologies GmbH

- 6.4.1.4 CASTOLIN EUTECTIC

- 6.4.1.5 CRS Holdings Inc.

- 6.4.1.6 Diffusion Engineers Limited

- 6.4.1.7 Fujimi Corporation

- 6.4.1.8 Global Tungsten & Powders

- 6.4.1.9 H.C. Starck

- 6.4.1.10 HAI Inc

- 6.4.1.11 Hoganas AB

- 6.4.1.12 Kennametl Stellite

- 6.4.1.13 Linde plc

- 6.4.1.14 Metallisation Limited

- 6.4.1.15 OC Oerlikon Management AG

- 6.4.1.16 Saint-Gobain

- 6.4.1.17 Sandvik AB

- 6.4.1.18 The Fisher Barton Group

- 6.4.1.19 Treibacher Industrie AG

- 6.4.2 Thermal Spray Coating Companies

- 6.4.2.1 APS Materials, Inc.

- 6.4.2.2 ARC International

- 6.4.2.3 Bodycote

- 6.4.2.4 CASTOLIN EUTECTIC

- 6.4.2.5 Chromalloy Gas Turbine LLC

- 6.4.2.6 Fujimi Corporation

- 6.4.2.7 Kennametl Stellite

- 6.4.2.8 Linde plc

- 6.4.2.9 Metallisation Limited

- 6.4.2.10 OC Oerlikon Management AG

- 6.4.2.11 Pamarco

- 6.4.2.12 Surface Dynamics

- 6.4.2.13 The Fisher Barton Group

- 6.4.3 Thermal Spray Equipment Companies

- 6.4.3.1 Air Products and Chemicals, Inc.

- 6.4.3.2 Camfil Air Pollution Control

- 6.4.3.3 CASTOLIN EUTECTIC

- 6.4.3.4 Donaldson Company Inc.

- 6.4.3.5 Flame Spray Technologies BV

- 6.4.3.6 GTV-wear GmbH

- 6.4.3.7 HAI Inc

- 6.4.3.8 Kennametl Stellite

- 6.4.3.9 Kurt J. Lesker Company

- 6.4.3.10 Linde plc

- 6.4.3.11 Metallisation Limited

- 6.4.3.12 OC Oerlikon Management AG

- 6.4.3.13 Saint-Gobain

- 6.4.3.14 The Lincoln Electric Company

- 6.4.1 Thermal Spray Powder Companies

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment

熱噴塗設備市場:2026-2032年全球市場預測(依製程、材料、設備類型、最終用途產業及應用分類)

熱噴塗設備市場:2026-2032年全球市場預測(依製程、材料、設備類型、最終用途產業及應用分類) 熱噴塗設備市場商機、成長要素、產業趨勢分析及2026-2034年預測。基於氧化釔的等離子噴塗粉末市場:按產品類型、製程類型、氧化釔含量範圍、塗層厚度和最終用途產業分類,全球預測(2026-2032年)

熱噴塗設備市場商機、成長要素、產業趨勢分析及2026-2034年預測。基於氧化釔的等離子噴塗粉末市場:按產品類型、製程類型、氧化釔含量範圍、塗層厚度和最終用途產業分類,全球預測(2026-2032年) 熱感噴塗:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

熱感噴塗:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球熱感噴塗市場報告

2026年全球熱感噴塗市場報告 全球熱噴塗材料市場熱噴塗設備:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

全球熱噴塗材料市場熱噴塗設備:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 熱噴塗市場規模、佔有率和成長分析(按材料、技術、應用和地區)- 產業預測 2025-2032熱噴塗材料:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

熱噴塗市場規模、佔有率和成長分析(按材料、技術、應用和地區)- 產業預測 2025-2032熱噴塗材料:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 全球熱噴塗材料市場(2024-2028)

全球熱噴塗材料市場(2024-2028)