|

市場調查報告書

商品編碼

1639413

熱噴塗材料:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)Thermal Spray Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

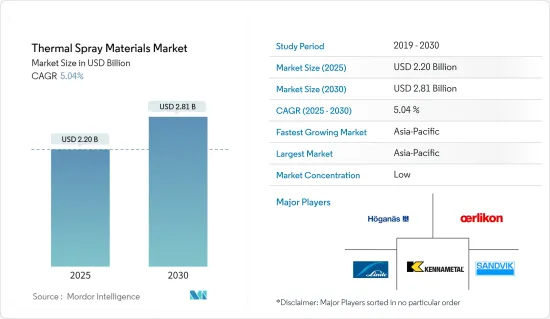

預計2025年熱噴塗材料市場規模為22億美元,預計2030年將達到28.1億美元,預測期間(2025-2030年)的複合年成長率為5.04%。

新冠疫情對2020年和2021年上半年的市場產生了負面影響。為了遏制病毒傳播,所有製造和其他活動都被關閉,這對市場造成了不利影響。然而,疫情過後,由於製造業的成長和目前已幾乎全面運作的終端用戶產業需求的復甦,預計市場將實現強勁成長。

主要亮點

- 市場發展的促進因素包括醫療設備製造中熱噴塗塗層的使用日益增多、熱噴塗陶瓷塗層的日益普及、防腐應用中的廣泛使用以及亞太地區風力發電行業的不斷發展。

- 然而,替代品的出現預計會阻礙市場的成長。

- 金屬陶瓷溶液前驅物等離子噴塗、噴塗材料回收、環境屏障塗層 (EBC) 噴塗粉末工業規模生產以及石油和天然氣行業的成長前景等進展,是預計推動市場的關鍵機會。

- 由於中國和印度等經濟的顯著成長,預計亞太地區將在預測期內佔據市場主導地位。

熱噴塗材料的市場趨勢

航太工業佔市場主導地位

- 熱噴塗材料在航太工業中有著廣泛的應用。熱噴塗材料用於生產飛機內各部件的塗層。這些塗層可延長零件的使用壽命、降低維護成本並提高燃油經濟性。

- 氧化鋯、鋁青銅、鈷鉬等熱噴塗材料分別用於塗層火箭燃燒室、壓縮機氣封及高壓噴嘴。

- 航空引擎容易因磨損、高溫腐蝕、微動磨損、顆粒侵蝕等原因而出現各種劣化問題。在較高溫度下,這種劣化會加速。熱噴塗材料賦予引擎零件所需的表面狀況,以延長其使用壽命。

- 全球軍事和航太製造市場包括波音、洛克希德和諾斯羅普·格魯曼等主要企業。國際民航組織發布的報告顯示,得益於經濟開放,後疫情期間商業航空公司的收益大幅成長。預計 2021 年將達到 4.72 億美元,到 2022年終將達到 6.58 億美元,增幅高達 39%。

- 航太領域的成長,特別是新興國家的民航領域的成長,預計將推動市場成長,這得益於對航太基礎設施建設和新計畫推出的大量支出。例如,在印度,2021 年 3 月,政府根據民航部的 UDAN-RCS 提交了一份在烏賈因大壩開發水上機場計劃的提案。

- 因此,由於上述優點,熱噴塗材料的採用預計會增加,從而推動其在航太工業的需求。

亞太地區佔市場主導地位

- 熱噴塗材料在航太工業中用作保護塗層。中國是最大的飛機製造國之一,也是最大的國內航空旅客市場之一。

- 龐大的市場規模、不斷增加的政府支持以及在線預訂電動車的能力等因素可能會推動該國對電動車的需求。

- 中國航太業預計將在先前大幅下滑後於2022年恢復獲利。此外,中國民航局估計,國內航空運輸量將恢復到疫情前的85%左右。

- 此外,中國航空公司計劃在未來20年內購買約7,690架新飛機,價值約1.2兆美元,預計將推動熱噴塗材料的需求。根據波音公司《2021-2040年商業展望》,到2040年中國將交付約8,700架新飛機,市場服務價值將達到1.8兆美元。

- 截至2021年12月,中國計劃在未來15年內建造至少150座新核子反應爐,投資4,400億美元。中國擁有大量核子反應爐: 19座在建,43座等待核子反應爐,166座已宣佈建設。這228台機組的總合裝置容量為246GW。

- 印度政府將根據重工業部下屬的生產連結獎勵計畫計劃,向汽車及汽車零件產業提供 78 億美元資金。因此,預計在預測期內,由於汽車產量增加而導致的汽車產業擴張將推動市場成長。

- 由於這些發展,預計亞太地區將在預測期內佔據市場主導地位。

熱噴塗材料產業概況

從本質上來說,熱噴塗材料市場是部分分散的。市場的主要企業(不分先後順序)包括 Hoganas AB、OC Oerlikon Management AG、Kennametal Inc.、Sandvik AB 和 Linde PLC。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 擴大熱噴塗塗層在醫療設備製造的應用

- 熱噴塗陶瓷塗層的需求不斷增加

- 防腐應用中的廣泛使用

- 亞太地區風電產業的發展

- 限制因素

- 替代品的出現

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第 5 章 市場區隔(以金額為準的市場規模)

- 依產品類型

- 塗層材料

- 粉末

- 陶瓷

- 陶瓷氧化物

- 氧化鋁

- 二氧化鈦

- 鋯石

- 氧化鉻和其他陶瓷氧化物

- 硬質合金(包括金屬陶瓷)

- 碳化鉻

- 碳化鎢

- 金屬

- 純金屬和合金

- 貴金屬

- MCrAlY

- 聚合物和其他塗層材料

- 線材/棒材

- 其他塗料(液體)

- 次要材料(輔助材料)

- 塗層材料

- 依工藝類型

- 燃燒

- 電能

- 按最終用戶產業

- 航太

- 工業用燃氣渦輪機

- 車

- 電子產品

- 石油和天然氣

- 醫療設備

- 能源和電力

- 其他最終用戶產業

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭格局

- 併購、合資、合作與協議

- 市場排名分析

- 主要企業策略

- 公司簡介

- Aisher APM LLC

- Ametek Inc.

- Aimtek Inc.

- C&M Technologies GmbH

- Castolin Eutectic

- CenterLine(Windsor)Limited

- CRS Holdings Inc.

- Fisher Barton

- Global Tungsten & Powders Corp.

- HAI Inc.

- HC Starck GmbH

- Hoganas AB

- Hunter Chemical LLC

- Kennametal Stellite

- Linde PLC

- LSN Diffusion Ltd

- Metallisation Limited

- Metallizing Equipment Co. Pvt. Ltd

- OC Oerlikon Management AG

- Polymet Corporation

- Powder Alloy Corporation

- Saint-Gobain

- Sandvik AB

- Thermion

第7章 市場機會與未來趨勢

- 金屬陶瓷溶液前驅物等離子體噴塗的最新發展。

- 熱噴塗材料的回收利用

- 環境屏障塗層 (EBC) 熱噴塗粉末的工業規模生產

- 石油和天然氣產業的成長前景

The Thermal Spray Materials Market size is estimated at USD 2.20 billion in 2025, and is expected to reach USD 2.81 billion by 2030, at a CAGR of 5.04% during the forecast period (2025-2030).

COVID-19 negatively impacted the market in 2020 and the first half of 2021. All the manufacturing and other activities were put on hold to curb the spreading of the virus, thereby negatively affecting the market. However, the market is projected to grow steadily post the retraction of the pandemic, owing to increased manufacturing and reinstating demand from the end-user industries, which have become operational at almost full scale.

Key Highlights

- The studied market's significant factors include the increasing usage of thermal spray coating in medical device manufacturing, the rising popularity of thermal spray ceramic coatings, extensive consumption in anti-corrosion applications, and evolution in the Asia-Pacific wind power sector.

- On the other hand, the emergence of alternate substitutes is expected to hinder the market's growth.

- The ongoing progress in solution precursor plasma spraying of cermets, recycling of thermal spray processing materials, industrial-scale production of environmental barrier coatings (EBC) thermal spray powders, and growth prospects in the oil and gas industry are the significant opportunities expected to drive the market in the future.

- Asia-Pacific region is expected to dominate the market in the forecast period because of vastly growing economies such as China and India.

Thermal Spray Materials Market Trends

Aerospace Industry to Dominate the Market

- Thermal spray materials are extensively used in the aerospace sector. They are used in manufacturing coatings, which are applied to various parts throughout the aircraft. These coatings offer component longevity, thus, reducing maintenance costs and increasing fuel efficiency.

- Thermal spray materials, such as zirconium oxide, aluminum bronze, and cobalt-molybdenum, are used for coating purposes in rocket combustion chambers, compressor air seals, and high-pressure nozzles, respectively.

- Various degradation problems exist in aircraft engines due to wear, hot corrosion, fretting, particle erosion, and many more. This degradation is accelerated when high temperatures are involved. Thermal spray material imparts the surface conditions required to increase engine components' service life.

- The global military and aerospace manufacturing market include dominant players such as Boeing, Lockheed, and Northrop Grumman. As per the report published by International Civil Aviation Organisation, commercial airlines' revenue grew significantly during the post-pandemic period because of the opening up of economies. It reached up to USD 472 million in 2021 and is forecasted to gain a whopping 39% standing at USD 658 million by the end of 2022.

- Growth in the aerospace sector, especially in civil aviation in emerging economies, on account of high expenditure on aerospace infrastructural construction and commissioning new projects, is expected to drive the market's growth. For instance, in India, in March 2021, the government submitted a proposal to develop a water aerodrome project at the Ujjain Dam under the Ministry of Civil Aviation's UDAN-RCS.

- Thus, increasing the adoption of thermal spray material due to its advantages mentioned above is expected to boost its demand in the aerospace industry.

Asia-Pacific to Dominate the Market

- Thermal spray materials are used in the aerospace industry as protective coating. China is one of the largest aircraft manufacturers and one of the largest markets for domestic air passengers.

- Factors such as large market size, increasing government support, and the ability to book electric vehicles online are likely to fuel the demand for electric vehicles in the country.

- China's aerospace industry is projected to return to profitability in 2022 after facing a significant decline in the previous years. In addition, the Civil Aviation Administration of China (CAAC) has estimated the aviation sector to recover domestic traffic to around 85% of pre-pandemic levels.

- Moreover, Chinese airline companies are planning to purchase about 7,690 new aircraft in the next 20 years, valued at approximately USD 1.2 trillion, expected to drive the demand for thermal spray materials. According to the Boeing Commercial Outlook 2021-2040, around 8,700 new deliveries will be made in China by 2040, with a market service value of USD 1,800 billion.

- In December 2021, China planned to build at least 150 new nuclear reactors in the next 15 years with an investment of USD 440 billion. The country has 19 reactors under construction, 43 reactors awaiting permits, and a massive 166 reactors that have been announced. The combined capacity of these 228 reactors is 246GW.

- The Government of India has planned to give USD 7.8 billion to the automobile and auto components sector in production-linked incentive schemes under the Department of Heavy Industries. Thus, the expansion of the automotive sector with the growing production of automobiles is anticipated to drive the market's growth over the forecast period.

- Owing to these developments, Asia-Pacific is expected to dominate the market over the forecast period.

Thermal Spray Materials Industry Overview

The thermal spray materials market is partially fragmented in nature. Some of the major players in the market (in no particular order) include Hoganas AB, OC Oerlikon Management AG, Kennametal Inc., Sandvik AB, and Linde PLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Usage of Thermal Spray Coating in Medical Device Manufacturing

- 4.1.2 Rising Demand of Thermal Spray Ceramic Coatings

- 4.1.3 Extensive Consumption in Anti-corrosion Applications

- 4.1.4 Evolution in the Asia-Pacific Wind Power Sector

- 4.2 Restraints

- 4.2.1 Emergence of Alternate Substitutes

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Product Type

- 5.1.1 Coating Materials

- 5.1.1.1 Powders

- 5.1.1.1.1 Ceramics

- 5.1.1.1.1.1 Ceramic Oxides

- 5.1.1.1.1.1.1 Alumina

- 5.1.1.1.1.1.2 Titania

- 5.1.1.1.1.1.3 Zirconia

- 5.1.1.1.1.1.4 Chromia and Other Ceramic Oxides

- 5.1.1.1.1.2 Carbides (including Cermets)

- 5.1.1.1.1.2.1 Chromium Carbides

- 5.1.1.1.1.2.2 Tungsten Carbides

- 5.1.1.1.2 Metals

- 5.1.1.1.2.1 Pure Metal and Alloys

- 5.1.1.1.2.2 Precious Metals

- 5.1.1.1.2.3 MCrAlY

- 5.1.1.1.3 Polymer and Other Coating Materials

- 5.1.1.2 Wires/Rods

- 5.1.1.3 Other Coating Materials (Liquid)

- 5.1.2 Supplementary Materials (Auxiliary Materials)

- 5.1.1 Coating Materials

- 5.2 Process Type

- 5.2.1 Combustion

- 5.2.2 Electric Energy

- 5.3 End-user Industry

- 5.3.1 Aerospace

- 5.3.2 Industrial Gas Turbines

- 5.3.3 Automotive

- 5.3.4 Electronics

- 5.3.5 Oil and Gas

- 5.3.6 Medical Devices

- 5.3.7 Energy and Power

- 5.3.8 Other End-user Industries

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Aisher APM LLC

- 6.4.2 Ametek Inc.

- 6.4.3 Aimtek Inc.

- 6.4.4 C&M Technologies GmbH

- 6.4.5 Castolin Eutectic

- 6.4.6 CenterLine (Windsor) Limited

- 6.4.7 CRS Holdings Inc.

- 6.4.8 Fisher Barton

- 6.4.9 Global Tungsten & Powders Corp.

- 6.4.10 HAI Inc.

- 6.4.11 HC Starck GmbH

- 6.4.12 Hoganas AB

- 6.4.13 Hunter Chemical LLC

- 6.4.14 Kennametal Stellite

- 6.4.15 Linde PLC

- 6.4.16 LSN Diffusion Ltd

- 6.4.17 Metallisation Limited

- 6.4.18 Metallizing Equipment Co. Pvt. Ltd

- 6.4.19 OC Oerlikon Management AG

- 6.4.20 Polymet Corporation

- 6.4.21 Powder Alloy Corporation

- 6.4.22 Saint-Gobain

- 6.4.23 Sandvik AB

- 6.4.24 Thermion

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Current Progress in Solution Precursor Plasma Spraying of Cermets

- 7.2 Recycling of Thermal Spray Processing Materials

- 7.3 Industrial Scale Production of Environmental Barrier Coatings (EBC) Thermal Spray Powders

- 7.4 Growth Prospects in the Oil and Gas Industry

歐洲熱噴塗市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

歐洲熱噴塗市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) 熱噴塗設備市場:2026-2032年全球市場預測(依製程、材料、設備類型、最終用途產業及應用分類)

熱噴塗設備市場:2026-2032年全球市場預測(依製程、材料、設備類型、最終用途產業及應用分類) 熱噴塗設備市場商機、成長要素、產業趨勢分析及2026-2034年預測。基於氧化釔的等離子噴塗粉末市場:按產品類型、製程類型、氧化釔含量範圍、塗層厚度和最終用途產業分類,全球預測(2026-2032年)熱感噴塗:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

熱噴塗設備市場商機、成長要素、產業趨勢分析及2026-2034年預測。基於氧化釔的等離子噴塗粉末市場:按產品類型、製程類型、氧化釔含量範圍、塗層厚度和最終用途產業分類,全球預測(2026-2032年)熱感噴塗:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球熱感噴塗市場報告

2026年全球熱感噴塗市場報告 全球熱噴塗材料市場熱噴塗設備:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

全球熱噴塗材料市場熱噴塗設備:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 熱噴塗市場規模、佔有率和成長分析(按材料、技術、應用和地區)- 產業預測 2025-2032

熱噴塗市場規模、佔有率和成長分析(按材料、技術、應用和地區)- 產業預測 2025-2032 全球熱噴塗材料市場(2024-2028)

全球熱噴塗材料市場(2024-2028)