|

市場調查報告書

商品編碼

2019089

熱噴塗設備市場商機、成長要素、產業趨勢分析及2026-2034年預測。Thermal Spray Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2034 |

||||||

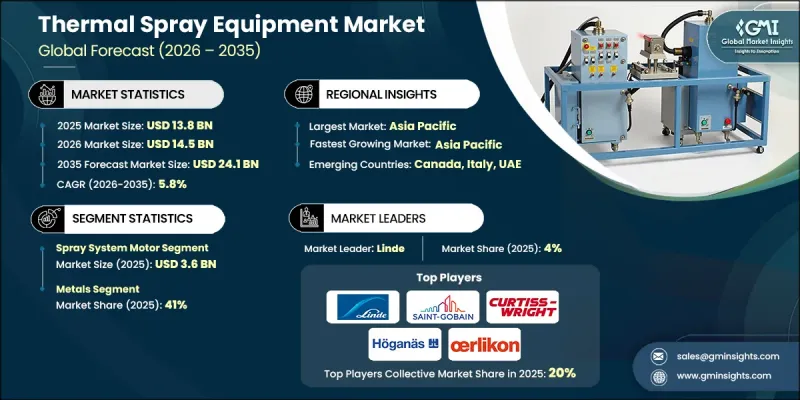

全球熱噴塗設備市場預計到 2025 年將達到 138 億美元,預計到 2035 年將以 5.8% 的複合年成長率成長至 241 億美元。

市場擴張的驅動力在於各行業尋求先進解決方案以提高零件耐久性和運作效率。熱噴塗技術正日益廣泛應用於航太、汽車、能源、重工業和製造業等產業,用於保護暴露於極端溫度、腐蝕性環境和高摩擦條件下的表面。對高性能塗層的日益依賴源自於延長設備壽命、降低維護成本和提升產品性能的需求。材料科學的進步和創新熱噴塗技術的出現,正在為電子、生物醫學設備和可再生能源等領域開闢新的應用,提供更強大的保護和功能優勢。製造商目前正利用自動化、機器人噴塗系統和精密控制技術,在最大限度地提高附著力、密度和耐磨性的同時,以實現塗層品質的一致性。這些進步使各行業能夠提高永續性、減少材料廢棄物並遵守環境法規,從而支持全球市場的穩定成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 138億美元 |

| 預測金額 | 241億美元 |

| 複合年成長率 | 5.8% |

預計2025年,噴塗系統馬達市場規模將達36億美元。噴塗系統由四個主要部件組成:噴槍、送料器、能源供應系統和控制系統。這些部件利用燃燒、等離子或電能產生高速加熱的物料流,形成緊密結合的塗層。這些系統能夠提高工業零件的耐磨性、耐腐蝕性和耐熱性,從而延長運作並提升各行業的性能。

到2025年,金屬塗層將佔據41%的市場佔有率,成為塗層材料的主要類別。金屬塗層,包括合金、鋁、鎳和不銹鋼塗層,具有卓越的強度、耐久性和耐腐蝕性。這些塗層廣泛應用於各個行業,以提高承受機械應力、化學腐蝕和極端溫度的零件的可靠性和效率。憑藉其多功能性和優異的性能,金屬塗層已成為高要求工業應用中不可或缺的材料。

北美熱噴塗設備市場佔89%的佔有率,預計2025年市場規模將達33億美元。美國市場成長的主要驅動力來自先進的航太、國防、汽車和能源產業,這些產業需要高性能塗層來維持零件的效率。美國擁有完善的製造業生態系統,能夠快速採用機器人噴塗系統、數位化監控和先進材料整合技術。此外,對永續性、法規遵循和最佳化維護的重視也進一步推動了北美對先進熱噴塗設備的需求。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 工業應用拓展

- 表面保護的需求日益成長

- 技術進步

- 產業潛在風險與挑戰

- 高初始投資

- 技術純熟勞工短缺

- 機會

- 自動化和機器人技術

- 高性能塗層材料的發展

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 透過裝置

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依設備類型分類,2022-2035年

- 噴霧系統

- 電漿

- 雙弧

- 火焰噴霧

- HVOF

- 粉末火焰噴霧

- 其他(例如真空)

- 展位

- 除塵系統

- 冷卻器

- 噴槍和噴嘴

- 供應系統

- 瓦斯系統

- 其他(氣體檢測系統等)

第6章 市場估算與預測:依表面類型分類,2022-2035年

- 金屬

- 陶瓷

- 聚合物

- 複合材料

- 其他(例如,碳化物、氧化物)

第7章 市場估計與預測:依營運方式分類,2022-2035年

- 自動的

- 半自動

- 手動的

第8章 市場估算與預測:依最終用途產業分類,2022-2035年

- 航太

- 車

- 電子學

- 生物醫學

- 製造業

- 石油和天然氣

- 能源與電力

- 其他(醫療設備等)

第9章 市場估價與預測:依通路分類,2022-2035年

- 直接地

- 間接

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- A&A Thermal Spray Coatings

- Ador Fontech

- Aimtek

- Alloy Metal Surface Technologies

- Bodycote

- Brycoat

- Curtiss-Wright

- Hannecard Roller Coatings

- Hoganas

- Kennametal

- Lincoln Electric

- Linde

- Oerlikon

- Saint Gobain

- Wall Colmonoy

The Global Thermal Spray Equipment Market was valued at USD 13.8 billion in 2025 and is estimated to grow at a CAGR of 5.8% to reach USD 24.1 billion by 2035.

The market's expansion is fueled by industries seeking advanced solutions to enhance component durability and operational efficiency. Thermal spray technology is increasingly adopted across aerospace, automotive, energy, heavy engineering, and manufacturing sectors to protect surfaces exposed to extreme temperatures, corrosive environments, and high-friction conditions. The growing reliance on high-performance coatings is driven by the need to extend equipment life, reduce maintenance costs, and improve product performance. Material science advancements and innovative spray techniques have opened new applications in electronics, biomedical devices, and renewable energy, providing additional protective and functional benefits. Manufacturers are now leveraging automation, robotic spray systems, and precise control technologies to achieve consistent coating quality and maximize adhesion, density, and resistance. These developments enable industries to improve sustainability, reduce material waste, and maintain compliance with environmental regulations, supporting steady market growth globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $13.8 Billion |

| Forecast Value | $24.1 Billion |

| CAGR | 5.8% |

In 2025, the spray system motor segment reached USD 3.6 billion. Spray systems consist of four core components: the spray gun, feedstock delivery unit, energy supply, and control systems. They operate using combustion, plasma, or electrical energy to create high-velocity, heated material streams that produce tightly bonded coatings. These systems enhance the wear, corrosion, and temperature resistance of industrial components, ensuring longer operational life and improved performance across sectors.

The metals segment accounted for 41% share in 2025, making it the dominant coating material category. Metallic coatings, including alloys, aluminum, nickel, and stainless steel, provide superior strength, durability, and corrosion resistance. These coatings are widely applied across industries to enhance the reliability and efficiency of components subjected to mechanical stress, chemical exposure, and thermal extremes. Their versatility and performance benefits make metal coatings essential for high-demand industrial applications.

North America Thermal Spray Equipment Market held 89% share, generating USD 3.3 billion in 2025. Market growth in the U.S. is supported by advanced aerospace, defense, automotive, and energy sectors that demand high-performance coatings to maintain component efficiency. The country's established manufacturing ecosystem enables rapid adoption of robotic spray systems, digital monitoring, and advanced material integration. Focus on sustainability, regulatory compliance, and maintenance optimization further boosts demand for sophisticated thermal spray equipment in North America.

Major players in the Global Thermal Spray Equipment Industry include Oerlikon, Hannecard Roller Coatings, Alloy Metal Surface Technologies, Lincoln Electric, Saint Gobain, Curtiss-Wright, Brycoat, Bodycote, Kennametal, Linde, Wall Colmonoy, Aimtek, Ador Fontech, and A&A Thermal Spray Coatings. Companies in the Thermal Spray Equipment Market pursue strategies such as technological innovation, strategic partnerships, and service differentiation to strengthen their market foothold. Firms invest heavily in R&D to improve robotic systems, plasma and combustion spray technologies, and real-time digital monitoring capabilities. Strategic alliances with industrial manufacturers and material suppliers allow companies to expand applications across diverse sectors. Emphasis on maintenance services, training programs, and turnkey solutions enhances customer loyalty. Geographic expansion into emerging markets, product portfolio diversification, and sustainability-focused innovations support long-term growth. Competitive differentiation is achieved through high-precision coating solutions, durability improvements, and advanced energy-efficient systems that meet industry-specific operational requirements.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment type

- 2.2.3 Surface type

- 2.2.4 Operation

- 2.2.5 End use industry

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing industrial application

- 3.2.1.2 Growing demand for surface protection

- 3.2.1.3 Technological advancements

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment

- 3.2.2.2 Skilled labor shortages

- 3.2.3 Opportunities

- 3.2.3.1 Automation & robotics

- 3.2.3.2 Growth in high-performance coating materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By equipment type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Equipment Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Spray system

- 5.2.1 Plasma

- 5.2.2 Twin arc

- 5.2.3 Flame spray

- 5.2.4 HVOF

- 5.2.5 Powder flame spray

- 5.2.6 Others (vacuum, etc.)

- 5.3 Booths

- 5.4 Dust collection systems

- 5.5 Chillers

- 5.6 Spray guns and nozzles

- 5.7 Feeder systems

- 5.8 Gas systems

- 5.9 Others (gas detection systems, etc.)

Chapter 6 Market Estimates and Forecast, By Surface Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Metals

- 6.3 Ceramics

- 6.4 Polymers

- 6.5 Composites

- 6.6 Others (e.g., carbides, oxides)

Chapter 7 Market Estimates and Forecast, By Operation, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Automatic

- 7.3 Semi-automatic

- 7.4 Manual

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Aerospace

- 8.3 Automotive

- 8.4 Electronics

- 8.5 Biomedical

- 8.6 Manufacturing

- 8.7 Oil and gas

- 8.8 Energy and power

- 8.9 Others (medical devices, etc.)

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 A&A Thermal Spray Coatings

- 11.2 Ador Fontech

- 11.3 Aimtek

- 11.4 Alloy Metal Surface Technologies

- 11.5 Bodycote

- 11.6 Brycoat

- 11.7 Curtiss-Wright

- 11.8 Hannecard Roller Coatings

- 11.9 Hoganas

- 11.10 Kennametal

- 11.11 Lincoln Electric

- 11.12 Linde

- 11.13 Oerlikon

- 11.14 Saint Gobain

- 11.15 Wall Colmonoy

歐洲熱噴塗市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

歐洲熱噴塗市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) 熱噴塗設備市場:2026-2032年全球市場預測(依製程、材料、設備類型、最終用途產業及應用分類)基於氧化釔的等離子噴塗粉末市場:按產品類型、製程類型、氧化釔含量範圍、塗層厚度和最終用途產業分類,全球預測(2026-2032年)熱感噴塗:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

熱噴塗設備市場:2026-2032年全球市場預測(依製程、材料、設備類型、最終用途產業及應用分類)基於氧化釔的等離子噴塗粉末市場:按產品類型、製程類型、氧化釔含量範圍、塗層厚度和最終用途產業分類,全球預測(2026-2032年)熱感噴塗:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球熱感噴塗市場報告

2026年全球熱感噴塗市場報告 全球熱噴塗材料市場熱噴塗設備:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

全球熱噴塗材料市場熱噴塗設備:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 熱噴塗市場規模、佔有率和成長分析(按材料、技術、應用和地區)- 產業預測 2025-2032熱噴塗材料:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

熱噴塗市場規模、佔有率和成長分析(按材料、技術、應用和地區)- 產業預測 2025-2032熱噴塗材料:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 全球熱噴塗材料市場(2024-2028)

全球熱噴塗材料市場(2024-2028)