|

市場調查報告書

商品編碼

2044256

西班牙黏合劑:市場佔有率分析、產業趨勢和統計數據、成長預測(2026-2031)Spain Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

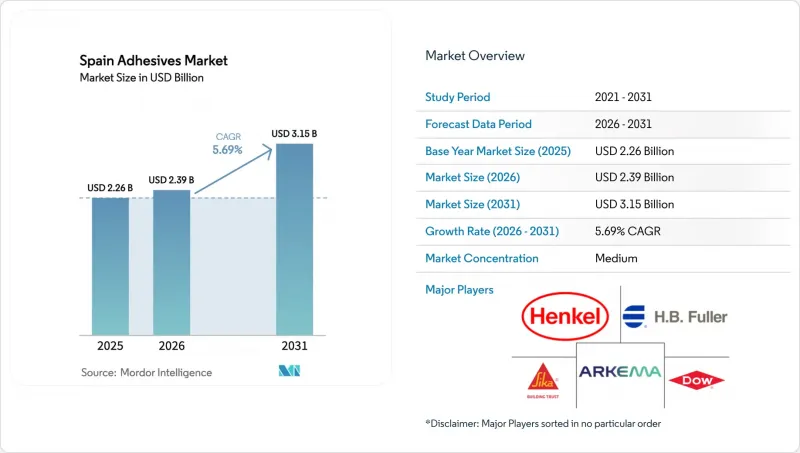

2025年西班牙黏合劑市場價值為22.6億美元,預計到2031年將達到31.5億美元,而2026年為23.9億美元,預測期(2026-2031年)複合年成長率為5.69%。

西班牙的建築維修項目、快速成長的電動車電池工廠以及歐盟廣泛的VOC法規正在推動對水性乳液、反應型混合膠和新一代熱熔膠的需求。建築公司對更厚的隔熱材料和氣密膜的需求促使他們需要透氣且耐用的黏合劑,這導致聚氨酯泡棉和MS聚合物密封劑的消耗量相對於溶劑型產品增加。汽車製造商正在轉向使用結構膠和熱膠來連接電池黏合劑和包裝單元,而包裝製造商則正在實現依賴低溫熱熔膠的無底紙貼標自動化。儘管跨國供應商佔據市場主導地位,但區域性專業供應商透過定製配方以適應西班牙多樣化的氣候和嚴格的維修保養週期,保持著自身的市場佔有率。儘管原料價格波動、結構膠粘劑行業勞動力短缺以及等離子粘合技術在鞋類行業的興起正在減緩長期前景,但西班牙整體黏合劑市場在2020年代中期仍將保持強勁的成長勢頭。

西班牙黏合劑市場趨勢與洞察

住宅維修增加和綠建築法規

西班牙的「PNRE 2026」藍圖要求到2030年,住宅初級能源消耗量比2020年水準降低16%,這將促使人們更多地使用透氣性MS聚合物和分散型黏合劑進行內保溫。在無法進行外保溫的歷史建築中,毛細作用系統目前更受青睞,這擴大了透氣型黏合劑的應用範圍。 「數位產品護照」將於2026年起逐步實施,要求提供批次級可追溯性和生命週期評估(LCA)數據,擁有ISO 14025 EPD認證的供應商將獲得優先待遇。此外,在發生多起外牆火災事故後,保險公司敦促減少易燃噴塗泡棉的使用,這進一步提高了人們對使用低VOC水性黏合劑固定的礦棉板的偏好。這些因素共同推動了西班牙住宅維修市場黏合劑市場的穩定成長。

汽車輕量化和向電動車的過渡

PowerCo在薩貢托建造的40GWh超級工廠將於2026年投產,為SEAT Martrel的電芯到電池包裝生產線供應標準化的棱柱形電芯。此生產線將以結構性黏著劑、導熱介面材料和灌封膠取代每個電池包裝中的100個緊固件。黏合劑配方必須兼具低揮發性、高導熱性和在無塵室環境下進行機器人應用的能力。漢高公司的人工智慧電池實驗室正在加速開發用於廢棄電池回收的脫模劑,以符合西班牙的循環經濟政策。 Stellantis和寧德時代建設計畫一座50GWh磷酸鐵鋰電池工廠,這將打造一個新的需求中心,並將西班牙黏合劑市場的商業機會集中在瓦倫西亞-薩拉戈薩走廊。

石化原料價格波動劇烈

丙烯酸酯、苯乙烯、EVA 和聚氨酯多元醇的價格與布蘭特原油價格密切相關,預計到 2025 年布蘭特原油價格將以個位數低點上漲,並在 2026 年面臨上行風險。由於西班牙大部分中間體都依賴進口,因此其生產商極易受到歐元兌美元匯率波動和地中海地區煉油廠停產的影響。像 QS Adhesives 這樣的小型公司缺乏避險能力,被迫將成本轉嫁給鞋類和家具 OEM 製造商,而這些製造商本身就已在與亞洲競爭對手競爭。生物基物料平衡原料雖然可以降低風險,但價格溢價高達 10-20%,進一步壓縮了西班牙黏合劑市場的利潤空間。

細分市場分析

2025年,水性膠合劑在西班牙黏合劑市場佔有43.44%的佔有率,這主要得益於歐盟VOC法規對建築和包裝行業乳化的推廣。預計到2031年,熱熔膠黏劑的複合年成長率將達到6.26%,這反映了無底紙標籤自動化生產以及鞋類產業逐步淘汰溶劑型接觸黏合劑的趨勢。漢高公司投資2,000萬歐元對其位於博芬根的工廠進行維修,擴大了其永續聚烯熱熔膠黏劑的生產能力。此外,Ravenwood公司的Com500塗佈機僅使用專用的熱熔壓敏膠。如果目前的採購協議能夠維持目前的市場成長速度,到2031年,西班牙熱熔黏合劑市場規模可望超過9.2億美元。

在皇家法令第117/2003號規定的監管上限下,溶劑型黏合劑的市場佔有率持續萎縮,但反應型黏合劑(環氧樹脂、聚氨酯和氰基丙烯酸酯)在航太和電動車電池領域仍保持著高價值的細分市場。漢高位於蒙託內斯的新工廠為空中巴士供應結構環氧樹脂,而雙固化(紫外線/熱熔)系統在汽車內裝領域也越來越受歡迎。儘管紫外線固化黏合劑的出貨量仍然小規模,但在加泰隆尼亞的電子組裝上,其出貨量卻實現了兩位數的成長。這些技術變革共同鞏固了西班牙作為黏合劑市場環保化學技術示範基地的地位。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 住宅翻新和強制性綠建築規範的增加

- 汽車輕量化和向電動車的過渡

- 歐盟推廣低揮發性有機化合物、水性化學品。

- 阿拉貢和納瓦拉的風力發電機葉片製造群

- 對超級工廠的津貼正在推動電池組裝用黏合劑的需求。

- 市場限制因素

- 石化原料價格波動劇烈

- 溶劑型系統的VOC嚴格法規

- 結構性黏著劑熟練安裝人員短缺

- 價值鏈分析

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 透過技術

- 水溶液

- 溶劑型

- 反應型

- 熱熔膠

- 紫外光固化黏合劑

- 依樹脂類型

- 聚氨酯

- 環氧樹脂

- 丙烯酸纖維

- 氰基丙烯酸酯

- VAE/EVA

- 矽酮

- 其他樹脂

- 按最終用戶行業分類

- 建築/施工

- 包裝

- 車

- 航太

- 木工和細木工

- 鞋類

- 衛生保健

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- 3M

- AC Marca

- Arkema

- Avery Dennison Corporation

- Beardow Adams

- CEYS

- Dow

- Dymax

- HB Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- ITW Performance Polymers

- MAPEI SpA

- Nitto Denko Corporation

- Permabond

- Quilosa

- Sika AG

- Soudal NV

- Tesa tape SA

第7章 市場機會與未來展望

The Spain Adhesives Market size was valued at USD 2.26 billion in 2025 and is estimated to grow from USD 2.39 billion in 2026 to reach USD 3.15 billion by 2031, at a CAGR of 5.69% during the forecast period (2026-2031). Spain's construction retrofits, fast-growing EV battery plants, and sweeping EU VOC caps are steering demand toward water-borne emulsions, reactive hybrids, and next-generation hot melts. Builders specifying thicker insulation and airtight membranes need breathable yet durable bonding agents, lifting consumption of polyurethane foams and MS-polymer sealants relative to solvent systems. Automotive manufacturers are shifting to structural and thermal adhesives for cell-to-pack architecture, while packaging converters automate linerless labels that rely on low-temperature hot melts. Multinational suppliers dominate, but regional specialists defend share by customizing formulations for Spain's diverse climate zones and tight repair-and-maintenance cycles. Feedstock volatility, labor shortages in structural bonding, and the emergence of plasma bonding in footwear temper the long-term outlook, yet the overall Spain adhesives market retains healthy momentum toward mid-decade.

Spain Adhesives Market Trends and Insights

Rising Residential Renovation and Green-Build Mandates

Spain's PNRE 2026 roadmap obliges residential buildings to trim primary energy use 16% below 2020 levels by 2030, triggering an upswing in internal insulation bonded with vapor-open MS-polymer and dispersion adhesives. Heritage properties that cannot receive external insulation now favor capillary-active systems, widening the addressable base for breathable adhesive chemistries. Digital Product Passports, phased in from 2026, demand batch-level traceability and LCA data, rewarding suppliers with ISO 14025 EPD credentials. Insurers are discouraging combustible spray foams after facade fire incidents, further tilting preference toward mineral-wool panels fixed with low-VOC water-borne adhesives. Together, these forces underpin steady growth for the Spain adhesives market in residential retrofits.

Automotive Lightweighting and EV Shift

PowerCo's 40 GWh gigafactory in Sagunto will start output in 2026 and feed unified prismatic cells to SEAT Martorell's cell-to-pack lines, where structural adhesives, thermal interface materials, and potting compounds replace 100 fasteners per pack. Adhesive formulations must combine low outgassing, high thermal conductivity, and robotic dispensability under clean-room protocols. Henkel's AI-assisted battery labs shorten debonding-solution development for end-of-life recovery, aligning with Spain's circular-economy policies. The Stellantis/CATL plan for a 50 GWh LFP plant in Zaragoza adds a second demand node, concentrating Spain adhesives market opportunities along the Valencia-Zaragoza corridor.

Volatile Petrochemical Feedstock Prices

Acrylates, styrene, EVA, and polyurethane polyols track Brent crude, which climbed in the low single digits during 2025 and faces upside risk in 2026. Spain imports most intermediates, exposing formulators to EUR/USD swings and Mediterranean refinery outages. Smaller firms such as QS Adhesives lack hedging muscle and must pass costs to footwear and furniture OEMs that already battle Asian competition. Bio-based mass-balance inputs cushion exposure but carry 10-20% premiums, squeezing margins across the Spain adhesives market.

Other drivers and restraints analyzed in the detailed report include:

- EU Push Toward Low-VOC, Water-Borne Chemistries

- Wind-Turbine Blade Clusters in Aragon and Navarre

- Stringent VOC Limits for Solvent-Borne Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Water-borne systems accounted for 43.44% of the Spain adhesives market in 2025 as EU VOC rules favored emulsions in construction and packaging. Hot melts are projected to register a 6.26% CAGR to 2031, reflecting linerless label automation and footwear's pivot from solvent contact cements. Henkel's EUR 20 million Bopfingen upgrade adds capacity for sustainable polyolefin hot melts, and Ravenwood's Com500 coaters rely exclusively on dedicated hot-melt PSAs. The Spain adhesives market size for hot melts could exceed USD 920 million by 2031 if adoption rates match current purchase commitments.

Solvent-borne share keeps eroding under Royal Decree 117/2003 caps, while reactive adhesives - epoxy, polyurethane, cyanoacrylate - retain high-value niches in aerospace and EV batteries. Henkel's new Montornes hub supplies structural epoxies to Airbus, and dual-cure UV/hot-melt systems gain traction in interior automotive trim. UV-cure volumes remain small but double-digit growth is visible in electronics assembly lines in Catalonia. Collectively, technology shifts reinforce the Spain adhesives market as a testbed for greener chemistries.

The Spain Adhesives Market Report is Segmented by Technology (Water-Borne, Solvent-Borne, Reactive, Hot Melt, and UV Cured Adhesives), Resin (Polyurethane, Epoxy, Acrylic, Cyanoacrylate, VAE/EVA, Silicone, and Other Resins), and End-User Industry (Building and Construction, Packaging, Automotive, Aerospace, Woodworking and Joinery, Footwear, and More). Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 3M

- AC Marca

- Arkema

- Avery Dennison Corporation

- Beardow Adams

- CEYS

- Dow

- Dymax

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- ITW Performance Polymers

- MAPEI S.p.A.

- Nitto Denko Corporation

- Permabond

- Quilosa

- Sika AG

- Soudal N.V.

- Tesa tape S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising residential renovation and green-build mandates

- 4.2.2 Automotive lightweighting and EV shift

- 4.2.3 EU push toward low-VOC, water-borne chemistries

- 4.2.4 Wind-turbine blade manufacturing clusters in Aragon and Navarre

- 4.2.5 Gigafactory subsidies driving battery-assembly adhesive demand

- 4.3 Market Restraints

- 4.3.1 Volatile petrochemical feed-stock prices

- 4.3.2 Stringent VOC limits for solvent-borne systems

- 4.3.3 Shortage of skilled applicators for structural bonding

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Technology

- 5.1.1 Water-borne

- 5.1.2 Solvent-borne

- 5.1.3 Reactive

- 5.1.4 Hot Melt

- 5.1.5 UV Cured Adhesives

- 5.2 By Resin

- 5.2.1 Polyurethane

- 5.2.2 Epoxy

- 5.2.3 Acrylic

- 5.2.4 Cyanoacrylate

- 5.2.5 VAE/EVA

- 5.2.6 Silicone

- 5.2.7 Other Resins

- 5.3 By End-User Industry

- 5.3.1 Building and Construction

- 5.3.2 Packaging

- 5.3.3 Automotive

- 5.3.4 Aerospace

- 5.3.5 Woodworking and Joinery

- 5.3.6 Footwear

- 5.3.7 Healthcare

- 5.3.8 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 AC Marca

- 6.4.3 Arkema

- 6.4.4 Avery Dennison Corporation

- 6.4.5 Beardow Adams

- 6.4.6 CEYS

- 6.4.7 Dow

- 6.4.8 Dymax

- 6.4.9 H.B. Fuller Company

- 6.4.10 Henkel AG & Co. KGaA

- 6.4.11 Huntsman International LLC

- 6.4.12 ITW Performance Polymers

- 6.4.13 MAPEI S.p.A.

- 6.4.14 Nitto Denko Corporation

- 6.4.15 Permabond

- 6.4.16 Quilosa

- 6.4.17 Sika AG

- 6.4.18 Soudal N.V.

- 6.4.19 Tesa tape S.A.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

眼科黏合劑市場規模、佔有率和成長分析:按產品類型、應用、適應症、最終用戶和地區分類-2026-2033年產業預測

眼科黏合劑市場規模、佔有率和成長分析:按產品類型、應用、適應症、最終用戶和地區分類-2026-2033年產業預測 2026-2030年全球黏合劑市場

2026-2030年全球黏合劑市場 丙烯酸樹脂黏合劑市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、分銷方式、地區和競爭格局分類,2021-2031年智慧黏合劑市場-全球產業規模、佔有率、趨勢、機會、預測:按技術、應用、地區和競爭格局分類,2021-2031年

丙烯酸樹脂黏合劑市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、分銷方式、地區和競爭格局分類,2021-2031年智慧黏合劑市場-全球產業規模、佔有率、趨勢、機會、預測:按技術、應用、地區和競爭格局分類,2021-2031年 織物黏合劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)

織物黏合劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031) 電子產業PUR黏合劑市場規模、佔有率和成長分析:按功能/類型、應用、終端用戶產業、包裝、分銷管道和地區分類-2026-2033年產業預測亞太地區EVA黏合劑:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

電子產業PUR黏合劑市場規模、佔有率和成長分析:按功能/類型、應用、終端用戶產業、包裝、分銷管道和地區分類-2026-2033年產業預測亞太地區EVA黏合劑:市佔率分析、產業趨勢與統計及成長預測(2026-2031年) 北美基材黏合劑市場規模、佔有率和趨勢分析報告:按樹脂類型、技術、應用、國家和細分市場預測(2026-2033 年)

北美基材黏合劑市場規模、佔有率和趨勢分析報告:按樹脂類型、技術、應用、國家和細分市場預測(2026-2033 年) 全球冷封黏合劑市場:依應用、類型、材料相容性及地區分類-市場規模、產業趨勢、機會分析及2026-2035年預測

全球冷封黏合劑市場:依應用、類型、材料相容性及地區分類-市場規模、產業趨勢、機會分析及2026-2035年預測 電子黏合劑市場:按材料、產品類型、應用和地區分類

電子黏合劑市場:按材料、產品類型、應用和地區分類