|

市場調查報告書

商品編碼

2044254

德國黏合劑:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Germany Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

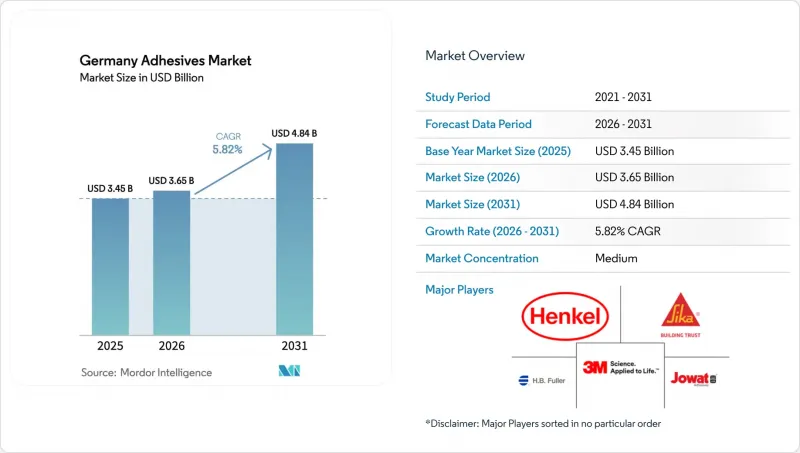

德國黏合劑市場預計將從 2025 年的 34.5 億美元成長到 2026 年的 36.5 億美元,到 2031 年達到 48.4 億美元。

預計2026年至2031年,市場將以5.82%的複合年成長率成長。這一成長主要受維修改造主導的建築需求、電動車產量增加以及包裝監管改革的推動,後者要求加工商改用低揮發性有機化合物(VOC)和可剝離化學品。由於能源價格仍比美國高出兩到三倍,且累積監管成本已接近附加價值的13%,國內市場的利潤率面臨壓力,因此國內複合材料生產商正日益關注出口。水基技術仍保持優勢,這得益於歐盟將於2026年中期實施的VOC上限規定,但隨著自動化和生物基技術的加速發展,熱熔技術也正在獲得發展動力。同時,全球企業正透過大規模收購來鞏固其在細分領域的地位,而中小企業則透過客製化和增強服務來捍衛其區域細分市場。

德國黏合劑市場趨勢與洞察

建築業的維修熱潮

節能改造佔據了很大一部分需求,因為1990年以前建造的建築需要多層保溫、氣密窗和外牆覆層,才能達到聯邦政府在2030年排放55%的目標。儘管2024年建築黏合劑的出貨量增加了15.4%,但木材和紙張的終端市場卻有所萎縮。這反映出維修工程中每平方公尺黏合劑用量的增加。諸如維修 VAE粉末之類的配方,使得CEM II瓷磚系統能夠在不影響其抗凍融耐久性的前提下,降低水泥熟料含量。由於技術純熟勞工短缺和成本增加(尤其是在精密外牆黏合方面),專案執行仍然存在風險,導致工期延誤。

過渡到柔軟性且可回收的包裝

修訂後的《包裝方法》(VerpackDG)規定,到2029年,塑膠包裝的回收率必須達到90%,並鼓勵使用單一材料薄膜和可剝離黏合劑,以避免因生產者延伸責任制(EPR)而受到處罰。對於聚乙烯和聚丙烯結構,建議優先使用水性黏合劑和熱熔膠,以排放溶劑排放並實現機械回收。漢高公司於2025年4月推出的可清洗標籤,能夠維持PET碎片在瓶到瓶循環中的質量,且僅需六個月的客戶檢驗,從而加速市場推廣。

嚴格的VOC和REACH法規對溶劑的使用有明確規定。

2026年,歐盟將室內裝飾產品中揮發性有機化合物(VOC)的允許含量降至30克/公升,並將職場甲醛暴露限值設定為0.3ppm。這迫使中小企業花費200萬至500萬歐元用於配方調整和設備升級。過渡期內庫存翻倍加劇了企業的營運資金壓力,同時,水性化學品在航太領域以及汽車黏合劑在高溫環境下的表現仍面臨挑戰。

細分市場分析

預計到2025年,水性膠合劑將佔據德國黏合劑市場41.15%的佔有率。這主要得益於木工、包裝和建築業的使用者轉向低溶劑型膠合劑,以回應歐盟將室內排放(VOC)排放量限制在30克/公升的法規。水性膠合劑在德國黏合劑市場的主導地位反映了其成熟的生產基礎設施以及VAE共聚物性能的提升,這些共聚物的VOC含量低於1克/公升,生物基原料含量高達50%。然而,由於包裝生產線對即時黏性的需求,熱熔膠預計將保持最高的成長率,到2031年複合年成長率將達到6.67%。此外,BioRUHM的生物反應型熱熔膠的應用範圍正在從瓦楞紙板擴展到汽車的木材和金屬結構。

儘管溶劑型產品的產量持續下降,但在水性系統因吸水性、固化速度慢或高溫穩定性等原因無法使用的領域,溶劑型產品仍發揮至關重要的作用,尤其是在航太內裝領域。反應型化學品(環氧樹脂、聚氨酯和氰基丙烯酸酯)是航太複合材料、醫療設備和電子設備的基礎材料,其高搭接剪切強度和精確的固化特性確保了高利潤率。紫外光固化和混合反應型熱熔膠結合了即時操作和最終交聯的優點,這種融合有望重新定義產品類別,並提升德國黏合劑市場的競爭力。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 建設產業的維修熱潮

- 過渡到柔軟性且可回收的包裝

- 醫療保健和醫療設備黏合劑市場的成長

- 德國生物經濟戰略支持的生物基黏合劑

- 用於電動汽車電池的導熱黏合劑

- 市場限制因素

- 嚴格的VOC和REACH法規對溶劑的使用有明確規定。

- 特種聚合物供應鏈中斷

- 精密黏合劑應用領域技術純熟勞工短缺

- 價值鏈分析

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 透過技術

- 水溶液

- 溶劑型

- 反應性

- 熱熔膠

- 紫外光固化黏合劑

- 依樹脂類型

- 聚氨酯

- 環氧樹脂

- 丙烯酸纖維

- 氰基丙烯酸酯

- VAE/EVA

- 矽酮

- 其他樹脂

- 按最終用戶行業分類

- 建築/施工

- 包裝

- 車

- 航太

- 木工和細木工

- 鞋類

- 衛生保健

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- 3M

- Arkema

- Avery Dennison Corporation

- DELO Industrie Klebstoffe GmbH & Co. KGaA

- Dow

- Dymax

- HB Fuller Company

- Henkel AG & Co. KGaA

- Hexion Inc.

- ITW Performance Polymers

- Jowat SE

- Klebchemie MG Becker GmbH & Co. KG

- Lohmann GmbH & Co. KG

- Permabond

- Rampf Holding GmbH & Co. KG

- Sika AG

- Wacker Chemie AG

- Wevo-Chemie GmbH

第7章 市場機會與未來展望

The Germany Adhesives Market size is projected to grow from USD 3.45 billion in 2025 to USD 3.65 billion in 2026, and reach USD 4.84 billion by 2031, growing at a CAGR of 5.82% from 2026 to 2031. Growth stems from renovation-led construction demand, rising electric-vehicle output, and packaging reforms that oblige converters to switch to low-VOC and debondable chemistries. Domestic formulators sharpen export focus because energy prices remain two to three times U.S. levels and cumulative regulation costs approach 13% of value-added, eroding home-market margins. Water-borne technology maintains a lead on the back of EU mid-2026 VOC caps, while hot melts gain traction as automation and bio-based initiatives accelerate. Meanwhile, global players consolidate specialty niches through large acquisitions, leaving small and medium-sized enterprises (SMEs) to defend regional pockets through customization and service intensity.

Germany Adhesives Market Trends and Insights

Construction-Sector Renovation Boom

Energy-efficiency retrofits dominate demand as pre-1990 structures require multilayer insulation, window sealing, and facade cladding to meet the federal 55% emissions-reduction target by 2030. Construction adhesives volume rose 15.4% in 2024 while wood and paper end-markets shrank, reflecting higher adhesive intensity per square meter in renovation projects. Formulations such as VINNAPAS VAE powders enable lower-clinker CEM II tile systems without sacrificing freeze-thaw durability. Project execution risk remains as skilled-labor shortages delay installations and lift costs, particularly for precision facade bonding.

Shift Toward Flexible and Recyclable Packaging

The amended Packaging Act (VerpackDG) forces 90% recyclability of plastic packs by 2029, incentivizing mono-material films and debondable adhesives to avoid extended producer responsibility penalties. Water-borne and hot-melt systems are preferred for polyethylene and polypropylene structures because they remove solvent emissions and allow mechanical recycling. Henkel's wash-off labels, launched in April 2025, preserve PET flake quality during bottle-to-bottle loops and require only six months of customer validation, accelerating market uptake.

Stringent VOC and REACH Regulations on Solvents

The EU slashed allowable VOC content to 30 g/L for interior products in 2026 and imposed workplace formaldehyde exposure limits of 0.3 ppm, forcing SMEs to spend EUR 2-5 million on reformulation and equipment upgrades. Dual inventories during the transition squeeze working capital, while water-borne chemistries still face performance gaps in aerospace and high-temperature automotive bonding.

Other drivers and restraints analyzed in the detailed report include:

- Thermal-Conductive Adhesives for EV Battery Cells

- Bio-Based Adhesives Backed by German Bioeconomy Strategy

- Specialty-Polymer Supply-Chain Disruptions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Water-borne systems captured 41.15% of Germany adhesives market share in 2025 on the strength of EU VOC limits that cap interior emissions at 30 g/L, steering woodworking, packaging, and construction users toward low-solvent options. Their dominance in Germany adhesives market size reflects mature production infrastructure and improved VAE copolymer performance, including less than or equal to 1 g/L VOC content and up to 50% bio input. Yet hot melts post the fastest 6.67% CAGR to 2031 as packaging lines demand instant tack, and BioRUHM's bio-reactive grades broaden application reach beyond cartons into automotive wood-metal structures.

Solvent-borne volumes continue to shrink but retain critical roles where water uptake, slow cure, or high-temperature stability preclude aqueous systems, particularly in aerospace interiors. Reactive chemistries - epoxies, polyurethanes, cyanoacrylates - anchor aerospace composites, medical devices, and electronics, commanding premium margins because of high lap-shear strength and precise cure profiles. UV-cure and hybrid reactive hot melts blend instant handling with final cross-linking, a convergence likely to redefine category boundaries and sharpen Germany adhesives market competitiveness.

The Germany Adhesives Market Report is Segmented by Technology (Water-Borne, Solvent-Borne, Reactive, Hot Melt, and UV Cured), Resin (Polyurethane, Epoxy, Acrylic, Cyanoacrylate, VAE/EVA, Silicone, and Other Resins), and End-User Industry (Building and Construction, Packaging, Automotive, Aerospace, Woodworking and Joinery, Footwear, Healthcare, and Other End-User Industries). Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 3M

- Arkema

- Avery Dennison Corporation

- DELO Industrie Klebstoffe GmbH & Co. KGaA

- Dow

- Dymax

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Hexion Inc.

- ITW Performance Polymers

- Jowat SE

- Klebchemie M.G. Becker GmbH & Co. KG

- Lohmann GmbH & Co. KG

- Permabond

- Rampf Holding GmbH & Co. KG

- Sika AG

- Wacker Chemie AG

- Wevo-Chemie GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Construction-sector renovation boom

- 4.2.2 Shift toward flexible and recyclable packaging

- 4.2.3 Healthcare and medical-device bonding growth

- 4.2.4 Bio-based adhesives backed by German Bioeconomy Strategy

- 4.2.5 Thermal-conductive adhesives for EV battery cells

- 4.3 Market Restraints

- 4.3.1 Stringent VOC and REACH regulations on solvents

- 4.3.2 Specialty-polymer supply-chain disruptions

- 4.3.3 Skilled-labor gap in precision adhesive application

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Technology

- 5.1.1 Water-borne

- 5.1.2 Solvent-borne

- 5.1.3 Reactive

- 5.1.4 Hot Melt

- 5.1.5 UV Cured Adhesives

- 5.2 By Resin

- 5.2.1 Polyurethane

- 5.2.2 Epoxy

- 5.2.3 Acrylic

- 5.2.4 Cyanoacrylate

- 5.2.5 VAE/EVA

- 5.2.6 Silicone

- 5.2.7 Other Resins

- 5.3 By End-User Industry

- 5.3.1 Building and Construction

- 5.3.2 Packaging

- 5.3.3 Automotive

- 5.3.4 Aerospace

- 5.3.5 Woodworking and Joinery

- 5.3.6 Footwear

- 5.3.7 Healthcare

- 5.3.8 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Avery Dennison Corporation

- 6.4.4 DELO Industrie Klebstoffe GmbH & Co. KGaA

- 6.4.5 Dow

- 6.4.6 Dymax

- 6.4.7 H.B. Fuller Company

- 6.4.8 Henkel AG & Co. KGaA

- 6.4.9 Hexion Inc.

- 6.4.10 ITW Performance Polymers

- 6.4.11 Jowat SE

- 6.4.12 Klebchemie M.G. Becker GmbH & Co. KG

- 6.4.13 Lohmann GmbH & Co. KG

- 6.4.14 Permabond

- 6.4.15 Rampf Holding GmbH & Co. KG

- 6.4.16 Sika AG

- 6.4.17 Wacker Chemie AG

- 6.4.18 Wevo-Chemie GmbH

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

丙烯酸樹脂黏合劑市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、分銷方式、地區和競爭格局分類,2021-2031年智慧黏合劑市場-全球產業規模、佔有率、趨勢、機會、預測:按技術、應用、地區和競爭格局分類,2021-2031年

丙烯酸樹脂黏合劑市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、分銷方式、地區和競爭格局分類,2021-2031年智慧黏合劑市場-全球產業規模、佔有率、趨勢、機會、預測:按技術、應用、地區和競爭格局分類,2021-2031年 電子產業PUR黏合劑市場規模、佔有率和成長分析:按功能/類型、應用、終端用戶產業、包裝、分銷管道和地區分類-2026-2033年產業預測

電子產業PUR黏合劑市場規模、佔有率和成長分析:按功能/類型、應用、終端用戶產業、包裝、分銷管道和地區分類-2026-2033年產業預測 北美基材黏合劑市場規模、佔有率和趨勢分析報告:按樹脂類型、技術、應用、國家和細分市場預測(2026-2033 年)

北美基材黏合劑市場規模、佔有率和趨勢分析報告:按樹脂類型、技術、應用、國家和細分市場預測(2026-2033 年) 全球冷封黏合劑市場:依應用、類型、材料相容性及地區分類-市場規模、產業趨勢、機會分析及2026-2035年預測

全球冷封黏合劑市場:依應用、類型、材料相容性及地區分類-市場規模、產業趨勢、機會分析及2026-2035年預測 2026年全球磁磚黏合劑市場報告

2026年全球磁磚黏合劑市場報告 英國黏合劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

英國黏合劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 2026-2034年全球衛生黏合劑市場規模、佔有率、趨勢和成長分析報告PUR黏合劑全球市場規模、佔有率、趨勢和成長分析報告(2026-2034年)法國黏合劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)

2026-2034年全球衛生黏合劑市場規模、佔有率、趨勢和成長分析報告PUR黏合劑全球市場規模、佔有率、趨勢和成長分析報告(2026-2034年)法國黏合劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)