|

市場調查報告書

商品編碼

2044249

法國黏合劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)France Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

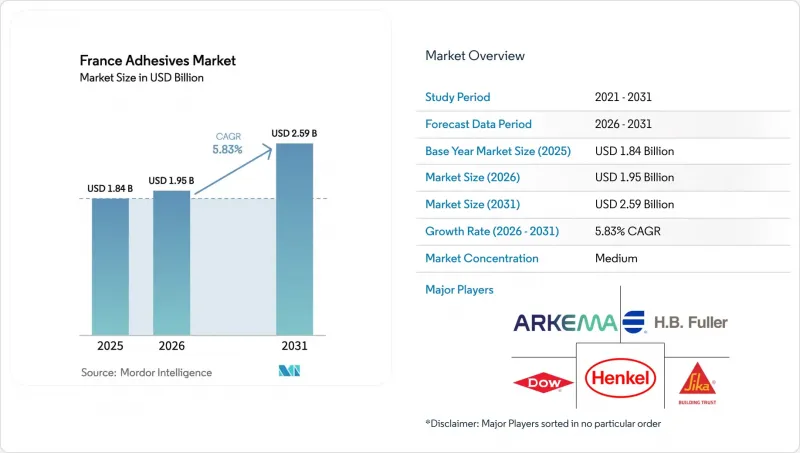

法國黏合劑市場預計到 2025 年將達到 18.4 億美元,到 2026 年將達到 19.5 億美元,到 2031 年將達到 25.9 億美元,2026 年至 2031 年的複合年成長率為 5.83%。

法國黏合劑市場正受益於維修主導的建築需求復甦,這在一定程度上緩解了該國60年來最低汽車產量水準的影響,同時加速了向符合REACH和RE2020法規要求的水性及生物基化學品的轉型。在法國價值322億歐元的節能維修計畫中,對隔熱膠帶、瓷磚黏合劑和結構玻璃密封膠的需求仍然強勁,但由於原料價格飆升,利潤率仍面臨挑戰,尤其是二氧化鈦的成本比2020年以前高出70%。同時,電動車組裝線上對高性能環氧樹脂和聚氨酯黏合劑的需求也在成長,這些黏合劑能夠減輕重量並延長電池續航里程。目前,每輛電動車在電池組和馬達連接處平均使用約8磅黏合劑和密封劑。隨著全球策略公司不斷進行收購,市場競爭日益激烈。阿科瑪於 2024 年 12 月收購了陶氏的包裝複合材料業務,漢高於 2026 年 1 月同意收購 ATP。此舉旨在確保產品系列,並更深入參與維修專案。

法國黏合劑市場趨勢與洞察

維修和節能建築需求

以「MaPrimeRenov」為核心的節能維修獎勵,在2023年為505,126個項目提供了19.5億歐元的資金,並在2020年至2024年中期累計創造了322億歐元的建築投資。這推動了對低VOC密封劑、氣密膠帶和生物基板材黏合劑的持續需求。 RE2020對建築內嵌碳排放的限制已從2022年的640公斤二氧化碳當量/平方米收緊至2031年的415公斤二氧化碳當量/平方米,迫使複合材料生產商從脲醛樹脂和酚醛樹脂轉向生物基替代品。採用160毫米礦棉的連續隔熱系統、預製CLT牆體和防潮層都依賴具有優異抗凍融穩定性和低排放的黏合劑。到2024年,透過節能證書(Certificates d'Economies d'Energie)獲得的資金將達到41.5億歐元,這將進一步加快維修工程的進度。工廠生產的零件已使現場廢棄物減少了約30%,並增加了對快速固化面板黏合劑的需求,從而保障了組裝的運作。

對更輕型汽車和電動車組裝的需求

在電動車 (EV) 專案中,能夠分散負載、粘合不同金屬和複合材料並承受 180–250 度C高溫烘烤的結構環氧樹脂和聚氨酯黏合劑至關重要。 Stellantis 已在都靈的電池技術中心投資超過 4,000 萬美元,目標是在 2030 年前將電池重量減半。這一目標與用黏合劑取代鉚釘和焊接直接相關,因為黏合劑可以防止脆性金屬間化合物的形成。結合黏合劑和鉚釘的混合黏合技術正成為實現電池外殼抗分層性和氣密性的新標準。儘管法國汽車產量在 2024 年跌至 60 年來的最低水平,但由於長期向電動車轉型,預計法國汽車產量將會回升。汽車裝飾和內裝黏合劑的短期低迷(2024 年下降 4.5%)掩蓋了高價值電池應用領域的結構性上升趨勢,這些趨勢有望在預測期內推動法國黏合劑市場的發展。

加強REACH法規對異氰酸酯和溶劑的規定

自2023年8月24日起,工業應用中游離二異氰酸酯含量超過0.1%的聚氨酯黏合劑,其認證工人必須接受強制性培訓、提交相關文件並定期更新。小規模加工商由於需要維修生產線並調整配方以達到「低排放」等級,因此承擔了不成比例的合規成本。配方調整通常需要長達一年的時間,導致產品上市延遲並佔用研發預算。該法規適用於結構、地板材料和軟包裝領域的MDI、TDI、HDI和IPDI。儘管歐洲化學品管理局(ECHA)預測每年氣喘病例將減少3000例,但在豁免混合物廣泛應用之前,法國黏合劑市場的銷售成長預計將受到短期干擾的抑制。

細分市場分析

由於水性膠合劑符合VOC法規,且與瓷磚黏合劑和紙張層壓板中的水泥基材相容,預計到2025年,水性膠合劑仍將保持其在法國黏合劑市場44.68%的最大佔有率。熱熔膠系統預計將以6.74%的複合年成長率成長,並隨著包裝生產線投資於可縮短夾緊時間和降低能耗的快速固化壓敏黏著劑,其在法國黏合劑市場的佔有率也將不斷擴大。超低單體聚氨酯熱熔膠在柔軟性食品領域需求旺盛,因為它們無需等待固化即可滿足0.1%的異氰酸酯閾值。在通用產品領域,水性丙烯酸黏合劑合適用於書籍裝訂、標籤和室內人造板等需要E0排放標準的應用。反應型環氧樹脂和聚氨酯則用於電動車電池組、風力發電機葉片和飛機內裝等結構性細分市場,其20-35 MPa的搭接剪切強度使其價格較高。

熱熔膠供應商正加強與設備OEM製造商的垂直整合,使加工商運作生產線。這對於瓦楞紙板工廠至關重要,因為歐盟電子委員會正在升級其按需生產單元。水性樹脂混煉商正在投資高固態分散技術,該技術可在不顯著增加黏度的情況下將固態含量提高到65%,從而提高應用成本的經濟性。紫外光固化膠合劑雖然仍屬於小眾市場,但在電子和醫療設備產業正經歷兩位數的成長,其價值在於能夠在不到一秒的時間內固化,從而避免熱應力。隨著加工商逐步淘汰鞋類和家俱生產線上的甲苯基載體,溶劑型黏合劑的使用量持續下降。這些技術變革共同推動了法國黏合劑市場的中期復甦,儘管市場仍有週期性波動。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 維修和節能建築需求

- 汽車輕量化和電動車組裝的需求

- 對水性/低VOC系統的需求日益成長

- 歐盟綠色分類法對生物基製劑的獎勵

- 為迎接2024年巴黎奧運會,對歷史建築維修和修復工作。

- 市場限制因素

- 加強REACH法規對異氰酸酯和溶劑的規定

- 中小加工商合規成本不斷增加

- 某些汽車零件中雷射焊接的替代方案

- 價值鏈分析

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 透過技術

- 水溶液

- 溶劑型

- 反應性

- 熱熔膠

- 紫外光固化黏合劑

- 依樹脂類型

- 聚氨酯

- 環氧樹脂

- 丙烯酸纖維

- 氰基丙烯酸酯

- VAE/EVA

- 矽酮

- 其他樹脂

- 按最終用戶行業分類

- 建築/施工

- 包裝

- 車

- 航太

- 木工和細木工

- 鞋類

- 衛生保健

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- 3M

- Arkema

- Avery Dennison Corporation

- Bolton Adhesives

- Dow

- HB Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- MAPEI SpA

- Sika AG

- ADERIS Specialities

- ITW Performance Polymers

- Wacker Chemie AG

- BASF SE

- Dymax Corporation

- Parker Hannifin Corp

- KLEIBERIT SE & CO. KG

- RAMSA France

- Pidilite Industries Ltd.

第7章 市場機會與未來展望

The France Adhesives Market size is projected to be USD 1.84 billion in 2025, USD 1.95 billion in 2026, and reach USD 2.59 billion by 2031, growing at a CAGR of 5.83% from 2026 to 2031. The France adhesives market is riding a renovation-led construction rebound, accelerating substitution toward water-borne and bio-based chemistries that comply with REACH and RE2020 mandates while buffering the hit from a 60-year low in domestic vehicle production. Volume growth is strongest in thermal-insulation tapes, tile adhesives, and structural glazing sealants used in the nation's EUR 32.2 billion energy-retrofit pipeline, yet raw-material inflation and titanium-dioxide costs remain 70% higher than pre-2020, keeping margins tight. At the same time, electric-vehicle (EV) assembly lines are pulling demand toward high-performance epoxy and polyurethane bonds that cut weight and extend battery range, with an average EV already using nearly 8 lb of adhesives and sealants in its battery pack and motor interfaces. Competitive intensity is rising as global strategics execute bolt-on deals. Arkema bought Dow's packaging-lamination line in December 2024, and Henkel signed to acquire ATP in January 2026, to lock in low-VOC portfolios and deeper access to renovation projects.

France Adhesives Market Trends and Insights

Renovation and Energy-Efficiency Construction Demand

Energy-retrofit incentives, led by MaPrimeRenov', disbursed EUR 1.95 billion to 505,126 projects in 2023 and generated EUR 32.2 billion of cumulative works between 2020 and mid-2024, driving sustained pull for low-VOC sealants, airtightness tapes, and bio-based panel adhesives. Embodied-carbon caps under RE2020 are tightening from 640 kg CO2e/m2 in 2022 to 415 kg CO2e/m2 by 2031, pushing formulators to swap UF and phenolic resins for bio-sourced alternatives. Continuous-insulation systems using 160 mm mineral wool, prefabricated CLT walls, and vapor-barrier membranes all rely on adhesives with superior freeze-thaw stability and low emissions. Funding from Certificats d'Economies d'Energie hit EUR 4.15 billion in 2024, further accelerating retrofit activity. Factory-built elements already cut on-site waste by roughly 30%, increasing demand for fast-curing panel bonds that keep assembly lines moving.

Automotive Lightweighting and EV Assembly Needs

Electric-vehicle programs depend on structural epoxy and polyurethane adhesives that distribute loads, bond dissimilar metals to composites, and survive 180-250°C paint-bake cycles. Stellantis invested over USD 40 million in a Turin battery technology center aiming to halve battery weight by 2030, a goal linked directly to replacing rivets and welds with adhesives that avoid brittle intermetallics. Hybrid joints, adhesive plus rivet, are becoming the new norm in battery housings, providing peel resistance plus sealing. Although France's vehicle output slumped to a six-decade low in 2024, the long-run shift to EVs is expected to restore volume. Short-run softness in automotive trim and interior adhesives, down 4.5% in 2024, masks a structural upswing in high-value battery applications primed to lift the France Adhesives market over the forecast horizon.

REACH Tightening on Isocyanates and Solvents

Since August 24, 2023, industrial use of polyurethane adhesives with more than 0.1% free diisocyanate requires certified worker training, documentation, and periodic renewals. Small converters shoulder disproportionate compliance costs as they retrofit lines or reformulate into "micro-emission" grades. Reformulations often span a full year, delaying product launches and tying up research and development budgets. The rule covers MDI, TDI, HDI, and IPDI across structural, flooring, and flexible-packaging segments. Although ECHA forecasts 3,000 fewer asthma cases annually, near-term disruption clips volume growth in the France Adhesives market until exempt blends gain scale.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Water-Borne/Low-VOC Systems

- EU Green-Taxonomy Incentives for Bio-Based Formulas

- Escalating Compliance Cost for SME Converters

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Water-borne platforms retained the largest 44.68% France adhesives market share in 2025 due to their compliance with VOC legislation and compatibility with cementitious substrates in tile adhesives and paper lamination. Hot-melt systems are forecast to expand at a 6.74% CAGR, lifting their slice of the France Adhesives market size as packaging lines invest in fast-setting, pressure-sensitive grades that reduce clamp time and energy use. Demand for ultra-low-monomer polyurethane hot melts is rising in flexible food packaging because they meet 0.1% isocyanate thresholds without curing delays. On the commodity end, water-borne acrylics cover bookbinding, labeling, and interior wood panels where E0 emissions rules apply. Reactive epoxies and polyurethanes occupy structural niches, EV battery packs, wind turbine blades, and aircraft interiors, where lap-shear strengths of 20-35 MPa justify premium pricing.

Hot-melt suppliers are deepening vertical ties with equipment OEMs so converters can run at line speeds above 400 m/min, critical for e-commerce corrugated plants upgrading box-on-demand cells. Water-borne formulators invest in high-solid dispersion tech that boosts solids to 65% without viscosity spikes, improving coat-weight economics. UV-cured volumes, though niche, post double-digit growth in electronics and medical devices where sub-second cure avoids thermal stress. Solvent-borne usage continues to shrink as converters phase out toluene carriers in shoe and furniture lines. Combined, technology shifts underpin medium-term upswing in the France adhesives market despite cyclical bumps.

The France Adhesives Market Report is Segmented by Technology (Water-Borne, Solvent-Borne, Reactive, Hot Melt, and UV Cured Adhesives), Resin (Polyurethane, Epoxy, Acrylic, Cyanoacrylate, VAE/EVA, Silicone, and Other Resins), and End-User Industry (Building and Construction, Packaging, Automotive, Aerospace, Woodworking and Joinery, Footwear, Healthcare, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 3M

- Arkema

- Avery Dennison Corporation

- Bolton Adhesives

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- MAPEI S.p.A.

- Sika AG

- ADERIS Specialities

- ITW Performance Polymers

- Wacker Chemie AG

- BASF SE

- Dymax Corporation

- Parker Hannifin Corp

- KLEIBERIT SE & CO. KG

- RAMSA France

- Pidilite Industries Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Renovation and energy-efficiency construction demand

- 4.2.2 Automotive lightweighting and EV assembly needs

- 4.2.3 Rising demand for water-borne/low-VOC systems

- 4.2.4 EU green-taxonomy incentives for bio-based formulas

- 4.2.5 Paris-2024 retrofits and heritage-building restorations

- 4.3 Market Restraints

- 4.3.1 REACH tightening on isocyanates and solvents

- 4.3.2 Escalating compliance cost for SME converters

- 4.3.3 Laser-welding substitution in selected auto parts

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Technology

- 5.1.1 Water-borne

- 5.1.2 Solvent-borne

- 5.1.3 Reactive

- 5.1.4 Hot Melt

- 5.1.5 UV Cured Adhesives

- 5.2 By Resin

- 5.2.1 Polyurethane

- 5.2.2 Epoxy

- 5.2.3 Acrylic

- 5.2.4 Cyanoacrylate

- 5.2.5 VAE/EVA

- 5.2.6 Silicone

- 5.2.7 Other Resins

- 5.3 By End-user Industry

- 5.3.1 Building and Construction

- 5.3.2 Packaging

- 5.3.3 Automotive

- 5.3.4 Aerospace

- 5.3.5 Woodworking and Joinery

- 5.3.6 Footwear

- 5.3.7 Healthcare

- 5.3.8 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Avery Dennison Corporation

- 6.4.4 Bolton Adhesives

- 6.4.5 Dow

- 6.4.6 H.B. Fuller Company

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 Huntsman International LLC

- 6.4.9 MAPEI S.p.A.

- 6.4.10 Sika AG

- 6.4.11 ADERIS Specialities

- 6.4.12 ITW Performance Polymers

- 6.4.13 Wacker Chemie AG

- 6.4.14 BASF SE

- 6.4.15 Dymax Corporation

- 6.4.16 Parker Hannifin Corp

- 6.4.17 KLEIBERIT SE & CO. KG

- 6.4.18 RAMSA France

- 6.4.19 Pidilite Industries Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

丙烯酸樹脂黏合劑市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、分銷方式、地區和競爭格局分類,2021-2031年智慧黏合劑市場-全球產業規模、佔有率、趨勢、機會、預測:按技術、應用、地區和競爭格局分類,2021-2031年

丙烯酸樹脂黏合劑市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、分銷方式、地區和競爭格局分類,2021-2031年智慧黏合劑市場-全球產業規模、佔有率、趨勢、機會、預測:按技術、應用、地區和競爭格局分類,2021-2031年 電子產業PUR黏合劑市場規模、佔有率和成長分析:按功能/類型、應用、終端用戶產業、包裝、分銷管道和地區分類-2026-2033年產業預測

電子產業PUR黏合劑市場規模、佔有率和成長分析:按功能/類型、應用、終端用戶產業、包裝、分銷管道和地區分類-2026-2033年產業預測 北美基材黏合劑市場規模、佔有率和趨勢分析報告:按樹脂類型、技術、應用、國家和細分市場預測(2026-2033 年)

北美基材黏合劑市場規模、佔有率和趨勢分析報告:按樹脂類型、技術、應用、國家和細分市場預測(2026-2033 年) 全球冷封黏合劑市場:依應用、類型、材料相容性及地區分類-市場規模、產業趨勢、機會分析及2026-2035年預測

全球冷封黏合劑市場:依應用、類型、材料相容性及地區分類-市場規模、產業趨勢、機會分析及2026-2035年預測 2026年全球磁磚黏合劑市場報告

2026年全球磁磚黏合劑市場報告 英國黏合劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

英國黏合劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 2026-2034年全球衛生黏合劑市場規模、佔有率、趨勢和成長分析報告PUR黏合劑全球市場規模、佔有率、趨勢和成長分析報告(2026-2034年)德國黏合劑:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

2026-2034年全球衛生黏合劑市場規模、佔有率、趨勢和成長分析報告PUR黏合劑全球市場規模、佔有率、趨勢和成長分析報告(2026-2034年)德國黏合劑:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)