|

市場調查報告書

商品編碼

2044250

英國黏合劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)United Kingdom Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

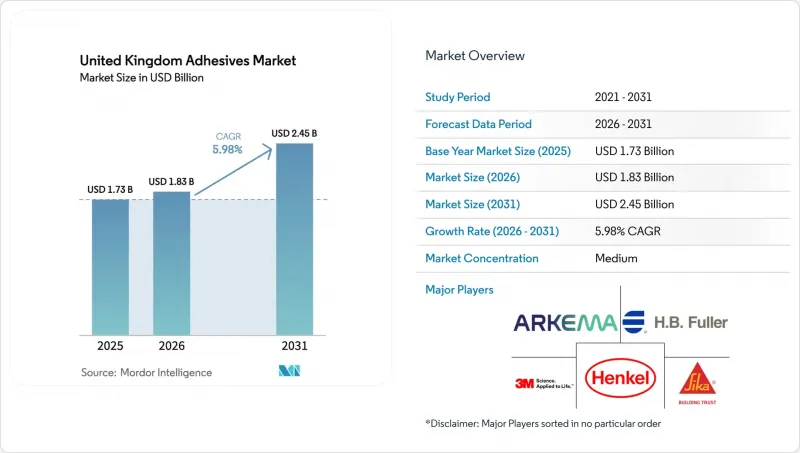

英國黏合劑市場預計到 2025 年將達到 17.3 億美元,到 2026 年將達到 18.3 億美元,到 2031 年將達到 24.5 億美元,2026 年至 2031 年的複合年成長率為 5.98%。

受歐盟高度關注物質 (SVHC) 法規更新、水性化學品快速普及以及輕質基材在交通運輸、建築和包裝領域日益廣泛的應用等因素的推動,黏合劑的角色正不斷轉變,從單純的通用材料轉變為性能增強組件。水性黏合劑在對法規要求嚴格的應用領域已佔據主導地位,而熱熔膠產品則正在搶佔電商包裝市場,因為該市場對固化時間的要求低於 60 秒。供應商正轉向反應型和生物基體系,以改進填料配方,同時兼顧原料價格波動和 VOC 法規的合規性。隨著被收購公司提供本地生產設施、技術服務團隊和區域分銷網路,全球巨頭之間的整合正在加速。

英國黏合劑市場趨勢與洞察

英國汽車製造業中輕質複合材料的應用日益廣泛

捷豹路虎斥資630萬英鎊(約831萬美元)的「SCALE-UP」計畫正朝著複合材料車門和再生碳纖維輪轂的大規模生產邁進,由此催生了對能夠粘合不同基材並承受電池式電動車熱負荷的黏合劑的需求。漢高於2026年簽署的對ATP黏合系統的收購協議,將為其帶來符合歐盟7排放標準可回收要求的低VOC特種膠帶。 SCALE-UP專案中的數位化建模能夠預測黏合線的性能,從而縮短供應商的開發週期。雖然聚氨酯和環氧樹脂化學品在結構連接領域仍佔據主導地位,但氰基丙烯酸酯和矽烷封端聚合物在需要60秒以下循環時間的領域逐漸獲得市場佔有率。預計複合材料的應用將使車輛減重35公斤,這將進一步鞏固結構性黏著劑作為機械緊固件替代品的長期需求。

模組化異地建造技術的普及推動了黏合劑的需求成長。

西卡英國銷售網路銷售聚氨酯和混合型系統,例如 SikaTack Panel 和 Sikaflex-545,這些系統可為異地製造商提供無需機械固定裝置即可實現氣密、抗振的接縫。工廠控制降低了固化時間的波動性,並允許使用更寬的捲材規格,從而廢棄物。多家供應商現已設立專門的模組化複合材料 (MMC) 部門,為生產線整合和操作人員培訓提供支援。據報道,使用 SikaForce 系統取代鉚釘可將夾芯板的生產速度提高 30%。混合型黏合劑±25% 的位移容許量可最大限度地減少模組運輸過程中的開裂,這對於正在大力推廣預製構件以緩解人手不足的住宅建築商而言是一項顯著優勢。

由於石化供應鏈中斷,原物料價格出現波動。

漢高預計2026年異氰酸酯、環氧樹脂和壓克力單體的成本漲幅將維持在個位數低位,但部分原物料的季度現貨價格波動仍普遍在15%至25%之間。佔區域供應主體的中小型混煉企業避險能力有限,往往必須承受較低的利潤率或延後產能擴張。英國REACH滾動行動計畫對PFAS和阻燃劑的監管力度加大,進一步加劇了不確定性。大型企業正透過增加配方中礦物填料的比例來應對,但這種策略受到黏度和應用限制。最終,成本波動更有利於擁有槓桿期貨採購和全球供應鏈的跨國公司。

細分市場分析

預計到2025年,水性產品將佔英國黏合劑市場佔有率的43.44%,英國更嚴格的VOC法規以及出口商必須滿足歐盟PPWR回收標準的要求,將進一步鞏固其主導地位。儘管熱熔膠市場規模較小,但隨著英國黏合劑市場與電子商務同步成長,預計其複合年成長率將達到6.26%,這主要得益於自動化小包裹處理線和紙質緩衝材料的日益普及。

溶劑型產品面臨合規成本上升和目標細分市場萎縮的雙重困境,但在某些需要深度滲透基材的地板材料和外牆細木工應用中,其需求依然強勁。反應型聚氨酯和環氧樹脂系統對於複合材料和模組化建築的結構黏合仍然至關重要。BASF與西卡共同推出的Baxxodur EC 151固化劑,其VOC排放量降低了90%,標誌著市場正向低排放量反應型產品轉型。雖然紫外光固化產品的市場佔有率較小,但它們在醫療設備和電子組裝領域的應用正在不斷擴展,以實現快速固化和零排放的工廠環境。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 英國汽車製造業中輕質複合材料的應用日益廣泛

- 模組化異地建造技術的普及推動了黏合劑。

- 英國永續性法規推動了生物基黏合劑的日益普及。

- 對高性能黏合劑的需求量正在增加。

- 英國區域機場周邊的小眾航太維修、修理和大修 (MRO) 活動激增

- 市場限制因素

- 由於石化供應鏈中斷,原物料價格出現波動。

- 英國REACH 法規對 VOC排放的嚴格限制增加了合規成本。

- 高技能黏合劑應用技術人員短缺

- 價值鏈分析

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 透過技術

- 水溶液

- 溶劑型

- 反應性

- 熱熔膠

- 紫外光固化黏合劑

- 依樹脂類型

- 聚氨酯

- 環氧樹脂

- 丙烯酸纖維

- 氰基丙烯酸酯

- VAE/EVA

- 矽酮

- 其他樹脂

- 按最終用戶行業分類

- 建築/施工

- 包裝

- 車

- 航太

- 木工和細木工

- 鞋類

- 衛生保健

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- 3M

- Arkema

- Avery Dennison Corporation

- BASF

- Beardow Adams

- Dow

- Dymax Corporation

- Follmann Chemie GmbH

- HB Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- Jowat SE

- Momentive Performance Materials

- PARKER HANNIFIN CORP

- Scapa

- Sika AG

- Wacker Chemie AG

第7章 市場機會與未來展望

The United Kingdom Adhesives Market size is projected to be USD 1.73 billion in 2025, USD 1.83 billion in 2026, and reach USD 2.45 billion by 2031, growing at a CAGR of 5.98% from 2026 to 2031. Regulatory realignment with EU SVHC updates, rapid uptake of water-borne chemistries, and heavier use of lightweight substrates in mobility, construction, and packaging continue to redefine adhesives from commodity inputs to performance-enabling materials. Water-borne grades already dominate regulatory-sensitive applications, while hot-melt lines capture e-commerce packaging runs that demand sub-60-second set times. Suppliers are improving filler loading and shifting to reactive or bio-based systems to balance raw-material volatility and VOC compliance. Consolidation among global majors is intensifying as acquisition targets supply local production footprints, technical service teams, and regional distribution depth.

United Kingdom Adhesives Market Trends and Insights

Growing Adoption of Lightweight Composites in UK Automotive Manufacturing

Jaguar Land Rover's GBP 6.3 million (USD 8.31 million) SCALE-UP program is scaling composite doors and recycled carbon-fiber wheels, creating demand for adhesives that bond mixed substrates and survive battery-electric vehicle thermal loads. Henkel's 2026 agreement to acquire ATP Adhesive Systems adds low-VOC specialty tapes that align with Euro 7 recyclability goals. Digital modelling within SCALE-UP now predicts bond-line performance, shrinking development cycles for suppliers. Polyurethane and epoxy chemistries still dominate structural joints, but cyanoacrylate and silane-terminated polymer options are gaining share where sub-60-second takt times matter. Composite adoption is forecast to trim vehicle mass by 35 kg, reinforcing long-term pull for structural adhesives over mechanical fasteners.

Increase in Modular Off-Site Construction Techniques Boosting Adhesive Demand

Sika's UK network sells polyurethane and hybrid systems such as SikaTack Panel and Sikaflex-545 that give off-site builders airtight, vibration-tolerant joints without mechanical fixings. Factory controls cut cure-time variance and allow wider roll formats, reducing waste by roughly 30%. Dedicated MMC divisions at several suppliers now offer line-integration support and operator training. Sandwich-panel production speeds reportedly rise 30% when SikaForce systems replace rivets. Hybrid adhesives' +-25% movement capability minimizes cracking during module transport, a key benefit as housebuilders boost prefabrication to ease labor shortages.

Volatility in Raw-Material Prices Linked to Petrochemical Supply-Chain Disruptions

Henkel projects low single-digit cost inflation for isocyanates, epoxies, and acrylic monomers in 2026, yet 15-25% quarterly spot swings remain common for some feedstocks. SME formulators, which dominate local supply, lack hedging power and often absorb margin hits or delay capacity upgrades. PFAS and flame-retardant scrutiny within the UK REACH Rolling Action Plan adds further uncertainty. Larger players are countering by boosting mineral-filler loading, but viscosity and application limits cap this tactic. Cost turbulence ultimately favors integrated multinationals with forward-buying leverage and global supply webs.

Other drivers and restraints analyzed in the detailed report include:

- Rising Use of Bio-Based Adhesive Formulations Driven by UK Sustainability Mandates

- Expansion of E-Commerce Packaging Volumes Requiring High-Performance Adhesives

- Stringent VOC-Emission Limits Under UK REACH Regulations Increasing Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Water-borne chemistries accounted for 43.44% of the United Kingdom adhesives market share in 2025, a lead reinforced by the UK's tighter VOC trajectory and by exporters' need to satisfy EU PPWR recyclability criteria. Hot-melt products, while smaller in base, are on track for a 6.26% CAGR as the UK adhesives market size tied to e-commerce grows in step with automated parcel lines and paper-based void-fill adoption.

Solvent-borne products confront rising compliance costs and shrinking target niches, though they still win select flooring and exterior joinery work that demands deep substrate wetting. Reactive polyurethane and epoxy systems remain indispensable for structural bonding in composites and modular construction; BASF and Sika's Baxxodur EC 151 hardener, with 90% lower VOC release, exemplifies the pivot toward low-emission reactive grades. UV-cure lines, though a small slice, are expanding in medical and electronics assembly for instant curing and zero-emission factory floors.

The United Kingdom Adhesives Market Report is Segmented by Technology (Water-Borne, Solvent-Borne, Reactive, Hot Melt, and UV Cured Adhesives), Resin (Polyurethane, Epoxy, Acrylic, Cyanoacrylate, VAE/EVA, Silicone, and Other Resins), and End-User Industry (Building and Construction, Packaging, Automotive, Aerospace, Woodworking and Joinery, Footwear, Healthcare, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 3M

- Arkema

- Avery Dennison Corporation

- BASF

- Beardow Adams

- Dow

- Dymax Corporation

- Follmann Chemie GmbH

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- Jowat SE

- Momentive Performance Materials

- PARKER HANNIFIN CORP

- Scapa

- Sika AG

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing adoption of lightweight composites in UK automotive manufacturing

- 4.2.2 Increase in modular off-site construction techniques boosting adhesive demand

- 4.2.3 Rising use of bio-based adhesive formulations driven by UK sustainability mandates

- 4.2.4 Expansion of e-commerce packaging volumes requiring high-performance adhesives

- 4.2.5 Surge in niche aerospace MRO activities around UK regional airports

- 4.3 Market Restraints

- 4.3.1 Volatility in raw-material prices linked to petrochemical supply-chain disruptions

- 4.3.2 Stringent VOC-emission limits under UK REACH regulations increasing compliance costs

- 4.3.3 Skills shortage in advanced adhesive-application technicians

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Technology

- 5.1.1 Water-borne

- 5.1.2 Solvent-borne

- 5.1.3 Reactive

- 5.1.4 Hot Melt

- 5.1.5 UV Cured Adhesives

- 5.2 By Resin

- 5.2.1 Polyurethane

- 5.2.2 Epoxy

- 5.2.3 Acrylic

- 5.2.4 Cyanoacrylate

- 5.2.5 VAE/EVA

- 5.2.6 Silicone

- 5.2.7 Other Resins

- 5.3 By End-user Industry

- 5.3.1 Building and Construction

- 5.3.2 Packaging

- 5.3.3 Automotive

- 5.3.4 Aerospace

- 5.3.5 Woodworking and Joinery

- 5.3.6 Footwear

- 5.3.7 Healthcare

- 5.3.8 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Avery Dennison Corporation

- 6.4.4 BASF

- 6.4.5 Beardow Adams

- 6.4.6 Dow

- 6.4.7 Dymax Corporation

- 6.4.8 Follmann Chemie GmbH

- 6.4.9 H.B. Fuller Company

- 6.4.10 Henkel AG & Co. KGaA

- 6.4.11 Huntsman International LLC

- 6.4.12 Jowat SE

- 6.4.13 Momentive Performance Materials

- 6.4.14 PARKER HANNIFIN CORP

- 6.4.15 Scapa

- 6.4.16 Sika AG

- 6.4.17 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment

丙烯酸樹脂黏合劑市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、分銷方式、地區和競爭格局分類,2021-2031年智慧黏合劑市場-全球產業規模、佔有率、趨勢、機會、預測:按技術、應用、地區和競爭格局分類,2021-2031年

丙烯酸樹脂黏合劑市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、分銷方式、地區和競爭格局分類,2021-2031年智慧黏合劑市場-全球產業規模、佔有率、趨勢、機會、預測:按技術、應用、地區和競爭格局分類,2021-2031年 電子產業PUR黏合劑市場規模、佔有率和成長分析:按功能/類型、應用、終端用戶產業、包裝、分銷管道和地區分類-2026-2033年產業預測

電子產業PUR黏合劑市場規模、佔有率和成長分析:按功能/類型、應用、終端用戶產業、包裝、分銷管道和地區分類-2026-2033年產業預測 北美基材黏合劑市場規模、佔有率和趨勢分析報告:按樹脂類型、技術、應用、國家和細分市場預測(2026-2033 年)

北美基材黏合劑市場規模、佔有率和趨勢分析報告:按樹脂類型、技術、應用、國家和細分市場預測(2026-2033 年) 全球冷封黏合劑市場:依應用、類型、材料相容性及地區分類-市場規模、產業趨勢、機會分析及2026-2035年預測

全球冷封黏合劑市場:依應用、類型、材料相容性及地區分類-市場規模、產業趨勢、機會分析及2026-2035年預測 2026年全球磁磚黏合劑市場報告

2026年全球磁磚黏合劑市場報告 2026-2034年全球衛生黏合劑市場規模、佔有率、趨勢和成長分析報告PUR黏合劑全球市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

2026-2034年全球衛生黏合劑市場規模、佔有率、趨勢和成長分析報告PUR黏合劑全球市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 德國黏合劑:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)法國黏合劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)

德國黏合劑:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)法國黏合劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)