|

市場調查報告書

商品編碼

2044105

北美資料中心冷卻:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)North America Data Center Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

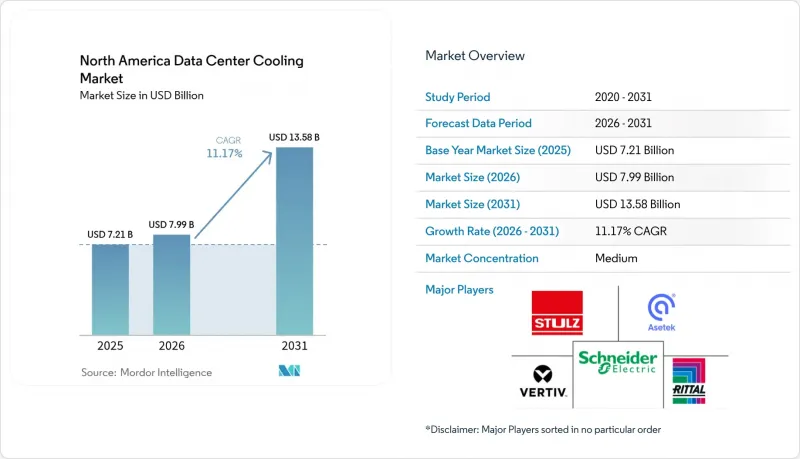

預計北美資料中心冷卻市場規模將在 2025 年達到 72.1 億美元,2026 年達到 79.9 億美元,2031 年達到 135.8 億美元,2026 年至 2031 年的複合年成長率為 11.17%。

隨著機架密度超過 40 千瓦,營運商被迫從傳統的風冷系統轉向液冷架構,後者可直接從處理器中排出熱量。推動這一轉變的因素是聯邦法規,該法規將租賃續約與電源使用效率 (PUE) 基準掛鉤。 《通貨膨脹削減法案》提供的稅額扣抵抵免(最高可覆蓋符合條件的設備成本的 30%)正在加速淘汰高全球暖化潛勢 (GWP) 的冷卻器,而沙漠地區的州用水限制則推動了對封閉回路型乾式冷卻器的需求。儘管大型暖通空調公司正在更新其冷卻器產品線,但由於液冷專家透過確保晶片溫度低於 25°C 來贏得設計訂單,競爭仍然激烈。開發商還面臨北維吉尼亞電網的限制以及與乾旱相關的保險附加費,這些因素都會影響選址和整體擁有成本。

北美資料中心冷卻市場趨勢與洞察

根據美國政府關於永續性。

聯邦機構必須證明,到2027會計年度,新建設施的PUE值低於1.4,現有設施低於1.5,這實際上排除了依賴周邊空氣處理機的傳統架空地板設計。更新後的租賃法規要求房東共用分錶計量的製冷能耗數據,如果未能滿足能源效率合約條款,租戶有權終止合約。承包商正轉向採用配備變速壓縮機的模組化冷卻器機組,此機組可將PUE值降低高達0.20個百分點。即使是曾經偏好空氣間隙安全系統的國防相關工作負載,也擴大採用後門式熱交換器來減輕中央空調系統的負荷。商業租戶也在回應聯邦政府的要求,敦促多租戶服務提供者保證類似的能源效率標準。

超大規模資料中心機架密度快速成長

用於訓練尖端人工智慧模型的叢集通常每個機架的功耗超過 40kW,而由於高頻寬記憶體和多晶片封裝會產生集中的熱量,某些 GPU 配置的功耗甚至接近 80kW。在如此高的負載下,如果沒有大量安裝高能耗風扇,僅靠空氣系統很難將進氣溫度維持在 27 度C以下。超大規模資料中心業者正在轉向「晶片級」冷板,這種冷板可以阻擋 70% 到 90% 的處理器熱量,防止其進入室內空氣,從而降低空調系統的負荷。這種高密度化也改變了位置標準,營運商紛紛遷往電力成本更低、氣候條件更有利於長時間自然冷卻的地區。傳統的空調基礎設施正被重新用於密度較低的儲存陣列,最大限度地利用閒置投資,同時液冷系統則負責保護運算核心。

電力網路限制導致維吉尼亞北部的新建設延期。

截至2026年1月,Dominion Energy的併網申請已超過7吉瓦,需要新建變電站的專案平均等待時間為36個月。 500千伏輸電線路投資不足以及當地對新建輸電線路的反對阻礙了輸電容量的擴張,迫使開發商考慮建造備用發電設施或將項目遷至俄亥俄州或北卡羅來納州。氫燃料電池等過渡方案需要大量資本投入,並需接受額外的空氣污染排放許可審查。一些營運商正在縮減設施規模,以適應現有饋線的可用容量,這使得原本以大型專案為導向的投資計畫變得分散。此外,由於貸款機構將延誤因素計入所需的收益率,擁塞風險也推高了資金籌措成本。

細分市場分析

預計到2031年,液冷解決方案將以12.54%的複合年成長率成長,顯著超過風冷。風冷在2025年仍將佔59.64%的市佔率。在北美資料中心冷卻市場,隨著超大規模資料中心業者資料中心維修其運算單元以容納目前每個機架功耗高達40-80kW的GPU,液冷解決方案的規模正在擴大。邊緣節點的浸沒式冷卻器解決了空間和噪音方面的限制,而直接冷卻板(DTC)則在大規模訓練叢集中佔據主導地位。後門熱交換器起到橋樑作用,延長了風冷機房的使用壽命並降低了資本支出。暖通空調供應商報告稱,液冷撬裝設備的訂單增加了數百倍,這表明這是長期趨勢,而非小眾嘗試。監管機構要求使用低全球暖化潛值(GWP)冷媒,這進一步促使營運商完全淘汰冷卻器,轉而依賴熱水循環系統,並透過乾式冷卻器排放熱量。

這種混合趨勢意味著兩種技術將共存。營運商根據工作負載分類機房區域,為人工智慧設備分配液冷區域,而儲存和網路設備則採用風冷。這種靈活的方法既能幫助設施人員逐步提陞技能,又能保護過去的投資。供應商目前正在捆綁控制軟體,以協調兩種系統,並將工作負載轉移到散熱裕度最佳的機架上。隨著液冷技術的日益普及,對感測器、接頭和快速斷開連接器的售後市場需求正在湧現,從而開闢了輔助收入來源。在北美資料中心冷卻市場,評估兩相冷媒迴路的先導計畫仍在繼續,但商業化進程可能會推遲到目前的預測期之後。

到2025年,電腦室的空氣處理機組將佔40.72%的市場佔有率,這反映了全部區域高架機房的歷史基礎。然而,泵浦和閥門的年複合成長率預計將達到12.66%,這反映了流體技術的快速發展。現代迴路需要精確的流量控制;即使是輕微的不平衡也會導致葉尖溫度急劇上升,從而降低效能。製造商正在透過內建流量感測器的變速泵浦和能夠即時自動調節迴路平衡的智慧閥門來解決這個問題。冷卻器仍然是資本項目中最大的單項設備,但其用途正在向模組化方向轉變,以500kW為單位交付到現場,以適應分階段的IT部署。

控制軟體是產品差異化的關鍵因素,人工智慧驅動的平台能夠學習負載模式,並在推理處理高峰到來之前預先設定冷卻迴路。營運商將這些系統與工作負載調度器整合,使其成為計算和冷卻一體化的效率引擎。混合式乾式冷卻器可減少 60-70% 的用水量,有助於在用水量受限的地區遵守相關法規。隨著超大規模資料中心業者資料中心簽訂多年合約以確保供應連續性,上游供應商也因連鎖效應而受益,銷售額不斷成長。雖然預計傳統風冷組件在北美資料中心冷卻市場的佔有率將會萎縮,但由於維修需求,對替換過濾器、皮帶和節熱器套件的需求在長期內仍將保持強勁。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 根據美國政府關於永續性。

- 超大規模資料中心機架密度快速成長

- AI/ML工作負載中液冷技術的廣泛應用

- 加拿大各省的區域供熱採購協議

- 根據《通貨膨脹控制法案》,低全球暖化潛值冷媒冷卻器稅額扣抵。

- 各州層級的用水限制正加速朝封閉回路型系統的維修。

- 市場限制因素

- 由於氫氟碳化合物(HFCs)的逐步減少,冷媒價格出現波動。

- 電力網路限制是維吉尼亞北部新建設延期的一個因素。

- 浸沒式冷卻維護技術不足

- 乾旱地區水冷系統的保險費附加費。

- 產業供應鏈分析

- 監理情勢

- 宏觀經濟因素對市場的影響

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章:北美目前資料中心部署狀況分析

- 資料中心 IT 負載容量(兆瓦)和面積(平方英尺)分析(2019-2031 年)

- 北美主要資料中心集群分析

- 北美未來主要超大規模設施分析

第6章 市場規模與成長預測

- 按類型分類的冷卻技術

- 空冷式

- CRAH

- 冷卻器和節熱器

- 冷卻塔(直冷式、間接式、兩級式)

- 其他

- 液冷

- 浸沒式冷卻

- 直接冷卻至尖端

- 後門熱交換器

- 空冷式

- 透過冷卻部件

- 電腦房空調機組(CRAH/CRAC)

- 冷卻器和熱交換裝置

- 冷卻塔和乾式冷卻器

- 泵浦和閥門

- 控制和監控軟體

- 層級類型

- 一級和二級

- 三級

- 第四級

- 按資料中心規模

- 小規模資料中心

- 中型資料中心

- 大型資料中心

- 超大規模資料中心

- 依資料中心類型

- 託管資料中心

- 超大規模資料中心業者資料中心/雲端服務供應商

- 企業和邊緣資料中心

- 國家

- 美國

- 加拿大

- 墨西哥

第7章 競爭情勢

- 市佔率分析

- 公司簡介

- Vertiv Group Corp.

- Stulz GmbH

- Schneider Electric SE

- Rittal GmbH and Co. KG

- Asetek A/S

- Alfa Laval AB

- Iceotope Technologies Ltd.

- Green Revolution Cooling Inc.

- Chilldyne Inc.

- Airedale International Air-Conditioning Ltd.

- Nortek Air Solutions LLC

- Mitsubishi Electric Corporation

- Johnson Controls International plc

- Munters Group AB

- Delta Electronics Inc.

- Hewlett Packard Enterprise Company

- IBM Corporation

- Cisco Systems Inc.

- LiquidStack Inc.

- Submer Technologies, SL

- CoolIT Systems Inc.

- Trane Technologies plc

- Super Micro Computer Inc.

第8章 市場機會與未來展望

- 評估未開發的領域和未滿足的需求

The North America data center cooling market size is projected to be USD 7.21 billion in 2025, USD 7.99 billion in 2026, and reach USD 13.58 billion by 2031, growing at a CAGR of 11.17% from 2026 to 2031.

Rising rack densities above 40 kilowatts are pressuring operators to swap legacy air systems for liquid architectures that draw heat directly from processors, a shift reinforced by federal mandates that link lease renewals to power-usage-effectiveness benchmarks. Inflation Reduction Act tax credits covering up to 30% of eligible equipment costs accelerate the retirement of high-GWP chillers, while state water-use caps in desert markets push demand for closed-loop dry coolers. Competitive intensity remains elevated as HVAC majors retrofit chiller portfolios and liquid-cooling specialists secure design wins by guaranteeing sub-25 °C chip temperatures. Developers are also navigating power-grid constraints in Northern Virginia and drought-related insurance surcharges that influence site selection and total cost of ownership.

North America Data Center Cooling Market Trends and Insights

Stringent PUE Targets Under U.S. Executive Order on Federal Sustainability

Federal agencies must now prove PUE ratios below 1.4 for new builds and below 1.5 for existing sites by fiscal 2027, effectively disqualifying legacy raised-floor designs that rely on perimeter air handlers. Updated leasing rules require landlords to share sub-metered cooling energy data, giving tenants the right to terminate contracts if efficiency covenants are missed. Contractors are pivoting to modular chiller plants with variable-speed compressors that trim PUE by up to 0.20 points. Defense workloads that once favored air-gapped security are adopting rear-door heat exchangers to cut the load seen by central plants. Commercial tenants are mirroring federal expectations, forcing multi-tenant providers to guarantee similar efficiency thresholds.

Escalating Rack Densities in Hyperscale Facilities

Training clusters for frontier AI models routinely exceed 40 kW per rack, with some GPU configurations nearing 80 kW as high-bandwidth memory and multi-die packages condense heat output. Air systems struggle to keep inlet temperatures under 27 °C at these loads without energy-intensive fan over-provisioning. Hyperscalers are moving to direct-to-chip cold plates that intercept 70%-90% of processor heat before it enters room air, easing demand on air handlers. This density also reshapes site selection, pushing operators toward regions with affordable electricity and climates that permit more free-cooling hours. Legacy air infrastructure is being repurposed for lower-density storage rows, maximizing sunk investments while liquid systems protect the compute core.

Power-Grid Constraints Delaying New Builds in Northern Virginia

Dominion Energy's transmission queue listed more than 7 GW of interconnection requests in January 2026, with average waits of 36 months for projects needing new substations. Underinvestment in 500 kV lines and local opposition to new corridors stall capacity expansions and force developers to explore backup generation or relocate to Ohio and North Carolina. Interim solutions such as hydrogen fuel cells add significant capital expense and trigger additional air-permit reviews. Some operators downsize footprints to fit within existing feeder headroom, fragmenting once-megasite-oriented investment plans. The congestion risk also elevates financing costs, as lenders price delays into required returns.

Other drivers and restraints analyzed in the detailed report include:

- Growing Adoption of Liquid Cooling for AI and ML Workloads

- Inflation Reduction Act Tax Credits for Low-GWP Chillers

- Volatility in Refrigerant Prices Amid HFC Phase-Down

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Liquid-based approaches will grow at a 12.54% CAGR through 2031, far ahead of air methods that still dominated with 59.64% share in 2025. The North America data center cooling market size for liquid solutions is expanding as hyperscalers retrofit compute rows that now host GPUs drawing 40-80 kW per rack. Immersion baths in edge nodes solve space and acoustic limits, while direct-to-chip plates dominate large training clusters. Rear-door heat exchangers act as a bridge, extending the life of air-cooled halls and reducing capex burdens. HVAC vendors disclose multi-hundred-percent order growth for liquid skids, signaling a secular pivot rather than a niche experiment. Regulatory pushes for low-GWP refrigerants further encourage operators to bypass chillers altogether, relying on warm-water loops that reject heat through dry coolers.

The hybridization trend means both technologies will coexist. Operators segment halls by workload, dedicating liquid zones to AI while leaving storage and network gear on air cooling. This flexible approach protects prior investments and allows gradual skill-set development among facilities staff. Suppliers now bundle control software that orchestrates both regimes, shifting workloads to racks with the most favorable thermal headroom. As liquid penetration rises, aftermarket demand emerges for sensors, fittings, and quick-disconnect couplings, opening ancillary revenue pools. The North America data center cooling market continues to witness pilots that evaluate two-phase refrigerant loops, though commercial readiness may postdate the current forecast period.

Computer room air handlers held 40.72% share in 2025, reflecting the historical base of raised-floor halls across the region. Yet pumps and valves are projected to rise at a 12.66% CAGR, mirroring the liquid-technology surge. Modern loops require precision flow control; even slight imbalances can spike chip temperatures and throttle performance. Manufacturers respond with variable-speed pumps featuring embedded flow sensors and smart valves that auto-balance circuits in real time. Chillers remain the single largest line-item in capital projects, but their role shifts toward modularity, arriving on site in 500 kW blocks that match staged IT deployments.

Control software differentiates offerings as AI-driven platforms learn load patterns and pre-cool loops before inference bursts. Operators integrate these systems with workload schedulers so compute and cooling act as a unified efficiency engine. Hybrid dry-coolers cut water draw by 60-70%, aiding compliance in jurisdictions with withdrawal caps. Upstream component vendors enjoy pull-through sales as hyperscalers lock in multi-year contracts to guarantee supply continuity. The North America data center cooling market share for traditional air components will erode, but retrofit demand ensures an extended tail for replacement filters, belts, and economizer kits.

The North America Data Center Cooling Market Report is Segmented by Cooling Technology (Air-Based, and Liquid-Based), Cooling Component (CRAH/CRAC, Chillers and Heat Exchangers, Cooling Towers and Dry Coolers, and More), Tier Type (Tier 1 and 2, and Tier 4), Data Center Size (Small, Medium, Large, and Hyperscale), Data Center Type (Colocation, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Vertiv Group Corp.

- Stulz GmbH

- Schneider Electric SE

- Rittal GmbH and Co. KG

- Asetek A/S

- Alfa Laval AB

- Iceotope Technologies Ltd.

- Green Revolution Cooling Inc.

- Chilldyne Inc.

- Airedale International Air-Conditioning Ltd.

- Nortek Air Solutions LLC

- Mitsubishi Electric Corporation

- Johnson Controls International plc

- Munters Group AB

- Delta Electronics Inc.

- Hewlett Packard Enterprise Company

- IBM Corporation

- Cisco Systems Inc.

- LiquidStack Inc.

- Submer Technologies, S.L.

- CoolIT Systems Inc.

- Trane Technologies plc

- Super Micro Computer Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent PUE Targets Under U.S. Executive Order on Federal Sustainability

- 4.2.2 Escalating Rack Densities in Hyperscale Facilities

- 4.2.3 Growing Adoption of Liquid Cooling for AI/ML Workloads

- 4.2.4 Heat-To-District Energy Purchase Agreements in Canadian Provinces

- 4.2.5 Inflation Reduction Act Tax Credits for Low-GWP Refrigerant Chillers

- 4.2.6 State-Level Water Withdrawal Caps Accelerating Closed-Loop Retrofits

- 4.3 Market Restraints

- 4.3.1 Volatility in Refrigerant Prices Amid HFC Phase-Down

- 4.3.2 Power-Grid Constraints Delaying New Builds in Northern Virginia

- 4.3.3 Limited Skills for Immersion-Cooling Maintenance

- 4.3.4 Insurance-Premium Surcharges for Water-Based Systems in Drought Zones

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Impact of Macroeconomic Factors on the Market

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 ANALYSIS OF THE CURRENT DATA CENTER FOOTPRINT IN NORTH AMERICA

- 5.1 Analysis of IT Load Capacity (MW) and Area footprint (Sq. Ft.) of Data Centers (for the Period of 2019-2031)

- 5.2 Analysis of Major Data Center Hotspots in North America

- 5.3 Analysis of Major Upcoming Hyperscale Facilities in North America

6 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 6.1 By Cooling Technology

- 6.1.1 Air-Based Cooling

- 6.1.1.1 CRAH

- 6.1.1.2 Chiller and Economizer

- 6.1.1.3 Cooling Tower (Direct, Indirect, Two-Stage)

- 6.1.1.4 Others

- 6.1.2 Liquid-Based Cooling

- 6.1.2.1 Immersion Cooling

- 6.1.2.2 Direct-to-Chip Cooling

- 6.1.2.3 Rear-Door Heat Exchanger

- 6.1.1 Air-Based Cooling

- 6.2 By Cooling Component

- 6.2.1 Computer-Room Air Handlers (CRAH/CRAC)

- 6.2.2 Chillers and Heat-Exchanger Units

- 6.2.3 Cooling Towers and Dry Coolers

- 6.2.4 Pumps and Valves

- 6.2.5 Control and Monitoring Software

- 6.3 By Tier Type

- 6.3.1 Tier 1 and 2

- 6.3.2 Tier 3

- 6.3.3 Tier 4

- 6.4 By Data Center Size

- 6.4.1 Small Data Center

- 6.4.2 Medium Data Center

- 6.4.3 Large Data Center

- 6.4.4 Hyperscale Data Center

- 6.5 By Data Center Type

- 6.5.1 Colocation Data Center

- 6.5.2 Hyperscalers Data Center/CSPs

- 6.5.3 Enterprise and Edge Data Center

- 6.6 By Country

- 6.6.1 United States

- 6.6.2 Canada

- 6.6.3 Mexico

7 COMPETITIVE LANDSCAPE

- 7.1 Market Share Analysis

- 7.2 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 7.2.1 Vertiv Group Corp.

- 7.2.2 Stulz GmbH

- 7.2.3 Schneider Electric SE

- 7.2.4 Rittal GmbH and Co. KG

- 7.2.5 Asetek A/S

- 7.2.6 Alfa Laval AB

- 7.2.7 Iceotope Technologies Ltd.

- 7.2.8 Green Revolution Cooling Inc.

- 7.2.9 Chilldyne Inc.

- 7.2.10 Airedale International Air-Conditioning Ltd.

- 7.2.11 Nortek Air Solutions LLC

- 7.2.12 Mitsubishi Electric Corporation

- 7.2.13 Johnson Controls International plc

- 7.2.14 Munters Group AB

- 7.2.15 Delta Electronics Inc.

- 7.2.16 Hewlett Packard Enterprise Company

- 7.2.17 IBM Corporation

- 7.2.18 Cisco Systems Inc.

- 7.2.19 LiquidStack Inc.

- 7.2.20 Submer Technologies, S.L.

- 7.2.21 CoolIT Systems Inc.

- 7.2.22 Trane Technologies plc

- 7.2.23 Super Micro Computer Inc.

8 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 8.1 White-Space and Unmet-Need Assessment

全球資料中心晶片直接冷卻市場(至2032年):按類型、冷卻劑類型、最終用戶和地區分類

全球資料中心晶片直接冷卻市場(至2032年):按類型、冷卻劑類型、最終用戶和地區分類 資料中心冷媒的市場機會、成長要素、產業趨勢與預測(2026-2035 年)。資料中心冷卻器市場商機、成長要素、產業趨勢分析及2026-2035年預測。

資料中心冷媒的市場機會、成長要素、產業趨勢與預測(2026-2035 年)。資料中心冷卻器市場商機、成長要素、產業趨勢分析及2026-2035年預測。 資料中心冷卻市場:2026-2032年全球市場預測(以交付方式、系統整合、冷卻方式、額定功率、資料中心類型、最終用戶和部署模式分類)

資料中心冷卻市場:2026-2032年全球市場預測(以交付方式、系統整合、冷卻方式、額定功率、資料中心類型、最終用戶和部署模式分類) 全球資料中心冷卻系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球資料中心冷卻系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年航太港資料中心冷卻全球市場報告

2026年航太港資料中心冷卻全球市場報告 全球資料中心管道市場:按管道類型、管道材質、應用、資料中心類型和地區分類-預測至2032年英洛冷凍市場:依產品類型、冷凍方式、安裝方式、冷氣量和最終用戶分類-2026-2032年全球預測

全球資料中心管道市場:按管道類型、管道材質、應用、資料中心類型和地區分類-預測至2032年英洛冷凍市場:依產品類型、冷凍方式、安裝方式、冷氣量和最終用戶分類-2026-2032年全球預測 亞太地區資料中心冷卻:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

亞太地區資料中心冷卻:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 資料中心冷卻市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、部署、最終用戶、設備及解決方案分類

資料中心冷卻市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、部署、最終用戶、設備及解決方案分類