|

市場調查報告書

商品編碼

2044080

塑膠廢棄物管理:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Plastic Waste Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

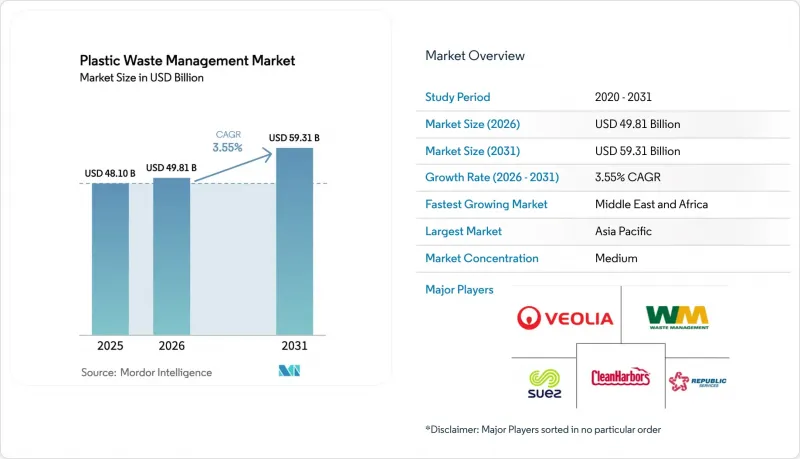

預計塑膠廢棄物管理市場將從 2025 年的 481 億美元成長到 2026 年的 498.1 億美元,然後在 2031 年達到 593.1 億美元,2026 年至 2031 年的複合年成長率為 3.55%。

更嚴格的法規,包括在超過25個司法管轄區實施的生產者延伸責任制(EPR)計劃,正迫使相關人員重新設計包裝,並投資於符合強制性再生材料含量要求的回收系統。亞太地區的需求量最高,且擁有規模最大的回收基礎設施;而中東和非洲地區由於各國政府設定了雄心勃勃的廢棄物掩埋減量目標,成長速度更快。在私人「循環經濟」基金和企業啟動協議的支持下,投資動能正從傳統的廢棄物處理轉向先進的化學回收,這些措施降低了新建設施的風險。現場部署的人工智慧光學分類機已將物料回收設施(MRF)的營運成本降低了高達25%,提高了原料質量,並在原生聚合物價格下跌的情況下提高了再生材料的獲利能力。

全球塑膠廢棄物管理市場趨勢與洞察

生產者延伸責任制 (EPR) 法規正在加速歐盟和加拿大的付費回收。

生產者責任延伸(EPR)計劃正在改變經濟結構,它將收集和處理成本轉移給生產商,從而直接獎勵他們減少材料重量並提高再生材料含量。歐盟法規將於2025年2月生效,要求2030年食品包裝中必須使用30%的再生PET材料。同時,包括不列顛哥倫比亞省在內的加拿大各省,在成熟的EPR計畫下,回收率已達79.6%。美國各州的EPR計劃,例如加州和明尼蘇達州正在實施的計劃,也採用了這種模式,這表明北美地區正朝著統一的方向發展。如今,生產商除了原料採購成本外,還要將遵循成本納入預算,而注重回收的設計和閉合迴路採購(循環採購)已成為成本管理和品牌聲譽的核心。

中國禁止進口低品質廢金屬,提高了亞洲國內回收的獲利能力。

中國2017年禁止進口大部分塑膠廢料,迫使出口商要麼提高廢料包的純度,要麼改變出貨地,同時也擴大了國內持證回收商的利潤空間。國務院的循環經濟計畫旨在2025年每年回收45億噸資源,而PET飲料容器的回收率已達96.48%。廣東和浙江等省份的區域中心正在向國內包裝市場和出口市場銷售塑膠碎片,這顯示本地原物料價格上漲與全球套利機會可以並存。鄰近的東協成員國正在透過引入品質標準來應對,以避免成為低品質廢棄物的傾倒場,這正在提升區域處理能力。

塑膠的過度生產和過度消費給廢棄物管理帶來了沉重負擔,並阻礙了回收和循環經濟的努力。

預計2022年全球聚合物產量將達4.03億噸,到2035年可能翻倍。這將使現有的回收網路不堪重負,導致供應超過終端市場需求,進而造成再生材料價格下跌。全球整體僅9%的塑膠廢棄物被回收利用,在海洋污染佔全球65%的非洲,其中22%的塑膠垃圾處理不當。此外,產能過剩將壓低原生聚合物的價格,除非政府強制推行回收計劃,否則再生材料的經濟效益將受到損害。

細分市場分析

到2025年,聚乙烯將佔塑膠廢棄物管理市場的32.28%,這反映了其在軟包裝和硬包裝領域的主導地位。完善的上門回收計畫和廣泛的機械回收基礎設施支撐著穩定的處理量。然而,PET是成長最快的聚合物閉合迴路系統中,96.48%的寶特瓶已被回收利用,為國內加工商生產高品質的PET薄片。隨著更多食品級PET解聚工廠投入運作,PET正逐漸成為高規格回收應用的理想材料。

需求趨勢已超越監理限制。 PET的化學結構使其能夠透過溶劑法進行解聚,從而將樹脂還原至單體純度,實現無限次重複使用且不劣化其物理性能。聚丙烯和聚苯乙烯由於污染和終端市場機會有限而發展滯後,而PVC的回收利用則隨著人工智慧預分揀系統和高效切碎機的引入而迅速發展。技術人員目前正致力於混合聚合物的熱解,以生產煉油廠所需的原料並分離氫氣產品。儘管這種多元化發展可能會削弱PE的主導地位,但其規模優勢和低成本的回收能力確保了其在塑膠廢棄物管理市場中繼續保持重要地位。

到2025年,工業部門將佔塑膠廢棄物總量的51.74%,這得益於其原料來源的同質化和較低的污染率。生產廢料、包裝薄膜和消費前廢料正被送往專業化工廠,這些工廠能夠實現更高的回收率並享受可預測的原料價格。預計到2031年,住宅垃圾量將以6.08%的複合年成長率快速成長,這主要得益於各市政當局實施標準化垃圾收集容器、開展污染防治教育以及安裝智慧攝影機。金縣的一個試點計畫將污染率降低到12%的臨界閾值以下,從而提高了垃圾打包的價值。

住宅垃圾處理量的增加得益於生產者延伸責任制(EPR)費用收入的支持,這些收入用於資助住宅垃圾收集系統的開發。羅德島州一項智慧感測器試點計畫減少了被拒收的廢棄物量,為納稅人節省了數百萬美元的運輸成本。由於廢棄物工業廢棄物規模龐大,物流相對簡化,預計其處理合約價格仍將居高不下。但隨著收集路線的數位化最佳化降低了每戶的收整合本,預計居民生活垃圾量增加最大的將是家庭生活垃圾。因此,塑膠廢棄物管理市場正在轉向兼顧小批量收集和材料純度標準的解決方案。

《塑膠廢棄物管理市場報告》按聚合物類型(例如聚乙烯 (PE)、聚丙烯 (PP))、來源(例如工業、住宅)、服務類型(例如處置和處理)、最終用途行業(例如包裝、汽車)以及地區(例如亞太地區、北美、歐洲)進行細分。本報告提供了上述所有細分市場的市場規模和預測(價值:美元)。

區域分析

到2025年,亞太地區將佔全球收入的40.21%,並繼續在塑膠廢棄物管理市場佔據核心地位。中國的循環經濟政策旨在2025年每年回收45億噸資源,而印度從2025年7月起強制實施的條碼制度正在加強生產者責任制。日本已將塑膠廢棄物減少了11%,但要實現2030年的目標,仍需加強執法力度。印尼依靠社區「廢棄物銀行」和私人回收商來解決高達58%的未回收率問題。同時,越南的循環城市試驗計畫展示了一個集收集和處理於一體的綜合流程。外國直接投資正湧入區域中心,高昂的打包價格抵消了基礎設施風險,使其在合規成本不斷上升的情況下仍保持著亞洲主導地位。

在塑膠廢棄物管理市場,中東和非洲地區預計將成為成長最快的地區,到2031年複合年成長率將達到6.09%。沙烏地阿拉伯的「2030願景」旨在實現94%的掩埋再利用率,為此計畫將廢棄物管理分類為25個區域叢集,並建立超過840個處理中心。埃及於2025年3月正式立法實施塑膠購物袋生產者延伸責任制(EPR),以促進私部門的分類和造粒計畫。阿拉伯聯合大公國將於2025年1月起禁止使用一次性塑膠製品,並對塑膠購物袋徵收關稅並要求進行數據報告。在整個非洲,塑膠回收率仍然只有9%,但捐助者資助的計畫和不斷上漲的市政廢棄物處置費正在為中期技術轉移的成長創造空間。

歐洲憑藉其《包裝和包裝廢棄物法規》保持著監管領域的主導。該法規要求所有包裝在2030年前必須可回收,並設定了30%的rPET(再生PET)標準。成員國統一的生產者延伸責任制(EPR)費用減輕了行政負擔,並為跨境廢棄物追蹤系統提供資金。在加拿大,繼不列顛哥倫比亞省在生產者全額資助下實現了79.6%的回收率之後,亞伯達的框架將於2025年4月生效。在美國,環保署的《國家防止塑膠污染戰略》在鼓勵各省自願採取措施的同時,也促進各省採用生產者延伸責任制。隨著中國禁止進口高品質壓縮包裝,出口商正在尋求新的市場,跨境材料流動正在發生變化,凸顯了塑膠廢棄物管理市場正向以本地為中心、循環利用的模式轉變。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場趨勢與市場動態

- 市場概覽

- 市場促進因素

- 歐盟和加拿大強制實施生產者延伸責任制(EPR),正在加速付費回收的進程。

- 中國禁止進口低品質廢料,提高了亞洲國內回收的獲利能力。

- 美國墨西哥灣沿岸地區先進(熱解和溶劑解)回收設施的快速擴張

- 透過企業主導的循環經濟基金(例如,閉迴路合作夥伴)降低基礎設施項目的風險

- 人工智慧驅動的光學分類線可將物料回收設施的營運成本降低 18-25%。

- 將快速消費品重新設計為單一材料的軟性包裝將提高其可回收性。

- 市場限制因素

- 塑膠的過度生產和過度消費加重了廢棄物管理負擔,阻礙了回收和循環經濟的發展。

- 如果布蘭特原油價格跌破每桶 55 美元,再生 PE 和 PP 的淨收益將為負值。

- 家庭垃圾(路邊垃圾)中污染程度較高(超過 12%),限制了機械回收材料的品質。

- 北歐國家對焚燒垃圾免徵碳排放稅,這正在削弱回收的經濟可行性。

- 價值/供應鏈分析

- 監理展望

- 技術展望

- 產業吸引力—五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭強度

- 投資和產能擴張分析

第5章 市場規模及成長預測(價值,十億美元)

- 聚合物類型

- 聚乙烯(PE)

- 聚丙烯(PP)

- 聚對苯二甲酸乙二醇酯(PET)

- 聚苯乙烯(PS)

- 聚氯乙烯(PVC)

- 其他聚合物(ABS、PA 等)

- 來源

- 產業

- 商業(零售和辦公)

- 住宅

- 建設與拆除

- 其他(組織、醫療服務、街頭廢棄物等)

- 按服務類型

- 收集、運送、分類

- 處置和處理

- 機械回收

- 化學/先進回收

- 焚燒與能源回收

- 受控掩埋處置

- 其他服務(諮詢、審計、訓練等)

- 按最終用途行業分類

- 包裝

- 建造

- 汽車和電動旅行

- 電氣和電子

- 紡織與時尚

- 衛生保健

- 其他(農業、消費品等)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 秘魯

- 南美洲其他地區

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 比荷盧經濟聯盟(比利時、荷蘭、盧森堡)

- 北歐國家(丹麥、芬蘭、冰島、挪威、瑞典)

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東協(印尼、泰國、菲律賓、馬來西亞、越南)

- 亞太其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 科威特

- 土耳其

- 埃及

- 南非

- 奈及利亞

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Veolia Environnement SA

- SUEZ SA

- Waste Management Inc.

- Republic Services Inc.

- Clean Harbors Inc.

- Remondis SE & Co. KG

- Biffa PLC

- Stericycle Inc.

- Covanta Holding Corp.

- TOMRA Systems ASA

- Plastic Energy Ltd.

- Brightmark LLC

- Agilyx Corporation

- TerraCycle Inc.

- Waste Connections Inc.

- DS Smith PLC

- Borealis AG

- LyondellBasell Industries NV

- Marius Pedersen A/S

第7章 市場機會與未來展望

The Plastic Waste Management Market size is expected to grow from USD 48.10 billion in 2025 to USD 49.81 billion in 2026 and is forecast to reach USD 59.31 billion by 2031 at 3.55% CAGR over 2026-2031.

Tightening regulations, notably Extended Producer Responsibility (EPR) schemes across more than 25 jurisdictions, are pushing stakeholders to redesign packaging and invest in recovery systems that meet recycled-content mandates. Asia-Pacific retains the highest regional demand as well as the largest installed recycling base, while the Middle East and Africa outpace other regions as governments adopt ambitious landfill-diversion targets. Investment momentum is shifting from traditional disposal toward advanced chemical recycling, supported by private "circularity" funds and corporate off-take agreements that de-risk new capacity. On-site AI-powered optical sorters are cutting Material Recovery Facility operating costs by up to 25%, improving feedstock quality and bolstering recyclate margins even when virgin polymer prices soften.

Global Plastic Waste Management Market Trends and Insights

Extended Producer-Responsibility (EPR) Mandates Accelerating Fee-based Collection in EU & Canada

EPR systems are reshaping economics by shifting collection and processing costs onto producers, creating direct incentives to reduce material weight and increase recycled content. The EU regulation, effective February 2025, sets a 30% recycled-PET requirement for food packaging by 2030, while Canadian provinces such as British Columbia already record 79.6% recovery rates under mature schemes. Emerging US state programs in California, Minnesota, and others mirror this approach, signalling continent-wide convergence. Producers now budget for compliance fees alongside raw-material purchasing, making design-for-recycling and closed-loop sourcing central to cost control and brand reputation.

China's Ban on Low-grade Scrap Imports Boosting Domestic Recycling Margins in Asia

China's 2017 prohibition on most plastic scrap imports forced exporters to improve bale purity or divert shipments elsewhere, simultaneously widening domestic profit margins for licensed recyclers. The State Council's circular-economy plan targets 4.5 billion tons of annual resource recycling by 2025, and PET beverage containers already achieve 96.48% recovery. Regional hubs in Guangdong and Zhejiang sell flakes into both domestic packaging and export markets, demonstrating that higher local feedstock prices can coexist with global arbitrage opportunities. Neighboring ASEAN members have responded with quality standards to avoid becoming low-grade dumps, reinforcing regional capacity build-out.

Plastic Overproduction and Overconsumption Strain Waste Management, Hindering Recycling and Circular-economy Efforts

Global polymer output hit 400.3 million tons in 2022 and could double by 2035, overwhelming existing collection networks and depressing recyclate prices when supply outpaces end-market demand. Only 9% of plastic waste is recycled worldwide, with 22% mismanaged in Africa, where 65% of marine leakage originates. Overcapacity also lowers virgin-polymer prices, undermining recycled-content economics absent policy-mandated offtake.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Scale-up of Advanced (Pyrolysis & Solvolysis) Recycling Facilities in U.S. Gulf Coast

- Corporate-backed Circularity Funds De-risking Infrastructure Projects

- Negative Netbacks for Recycled PE & PP When Brent Less Than USD 55/barrel

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyethylene held 32.28% of plastic waste management market share in 2025, reflecting its dominance in flexible and rigid packaging streams. Robust curbside programs and widespread mechanical-recycling infrastructure support steady volumes. Yet PET is the fastest-growing polymer segment, expanding at a 5.82% CAGR on the back of bottle-to-bottle mandates such as the EU's 30% recycled-content rule by 2030. China's closed-loop system already recovers 96.48% of PET beverage bottles, creating high-quality flake for domestic converters. As more food-grade depolymerization plants come on stream, PET positions itself as the preferred material for high-specification recycling applications.

Demand dynamics go beyond regulation. PET's chemical structure allows solvent-based depolymerization that returns resin to monomer purity, facilitating infinite reuse without property loss. Polypropylene and polystyrene lag because of contamination and limited end-markets, while PVC recycling gains traction through AI-assisted pre-sorting systems and high-efficiency shredders. Technology developers now target mixed-polymer pyrolysis that yields hydrocarbons for refinery feedstocks or hydrogen co-products. Such diversification may temper PE's lead, but its scale and low-cost collection ensure continued relevance in the plastic waste management market.

Industrial generators contributed 51.74% of total plastic waste volumes in 2025, benefiting from homogenous material flows and lower contamination. Manufacturing off-cuts, distribution film, and pre-consumer scrap feed specialized plants that achieve higher recovery yields and enjoy predictable input pricing. Residential waste streams are projected to grow fastest at 6.08% CAGR through 2031, as municipalities roll out standardized bins, anti-contamination education, and smart cameras. King County's pilot reduced contamination below the critical 12% threshold, unlocking higher bale values.

Residential expansion is underpinned by EPR fee revenue that finances household collection upgrades. Smart-sensor trials in Rhode Island cut rejected tonnage, saving taxpayers millions in hauling charges. Industrial streams will still command premium contracts because scale simplifies logistics, yet the broadest tonnage uplift will come from homes as digital route optimization reduces the per-household cost of collection. The plastic waste management market, therefore, pivots toward solutions that reconcile small-lot pick-ups with material purity standards.

The Plastic Waste Management Market Report is Segmented by Polymer Type (Polyethylene (PE), Polypropylene (PP), and More), by Source (Industrial, Residential, and More), by Service Type (Disposal/Treatment, and More), by End-Use Industry (Packaging, Automotive, and More), and by Geography (Asia-Pacific, North America, Europe, and More). The Report Offers Market Size and Forecasts in Value (USD) for all the Above Segments.

Geography Analysis

Asia-Pacific generated 40.21% of global revenue in 2025 and remains the anchor of the plastic waste management market. China's circular-economy policies aim for 4.5 billion tons of annual resource recycling by 2025, and India's July 2025 barcode mandate improves producer accountability. Japan posts an 11% reduction in plastic waste but still needs stricter enforcement to hit 2030 benchmarks. Indonesia relies on community "waste banks" and private haulers to tackle its 58% uncollected rate, while Vietnam's pilot circular-city programs showcase integrated collection and treatment paths. Foreign direct investment flows into regional hubs where high bale prices offset infrastructure risk, maintaining Asia's leadership despite rising compliance costs.

The Middle East and Africa segment in the plastic waste management market holds the fastest growth trajectory at 6.09% CAGR to 2031. Saudi Arabia's Vision 2030 targets 94% landfill diversion, supported by more than 840 treatment centers and a plan to divide waste management into 25 regional clusters. Egypt formally enacted EPR on shopping bags in March 2025, spurring private-sector sorting and pelletizing projects. The UAE's single-use plastic ban, effective January 2025, adds tariffs on carrier bags and imposes data-reporting duties. Africa overall recycles only 9% of its plastic, but donor-funded projects and rising urban-waste tipping fees create a medium-term runway for technology transfer.

Europe sustains regulatory leadership through the Packaging and Packaging Waste Regulation that demands all packaging be recyclable by 2030 and sets a 30% rPET threshold. Harmonized EPR fees across member states cut administrative burdens and fund trans-frontier waste-tracking systems. Canada mirrors success with British Columbia's 79.6% recovery under full producer funding, and Alberta's framework goes live in April 2025. In the United States, the EPA's National Strategy to Prevent Plastic Pollution presses voluntary action but also encourages state-level EPR adoption. Cross-border material flows adjust as exporters seek high-quality bale outlets after China's import ban, underscoring the plastic waste management market's shift toward localized circular loops.

- Veolia Environnement SA

- SUEZ SA

- Waste Management Inc.

- Republic Services Inc.

- Clean Harbors Inc.

- Remondis SE & Co. KG

- Biffa PLC

- Stericycle Inc.

- Covanta Holding Corp.

- TOMRA Systems ASA

- Plastic Energy Ltd.

- Brightmark LLC

- Agilyx Corporation

- TerraCycle Inc.

- Waste Connections Inc.

- DS Smith PLC

- Borealis AG

- LyondellBasell Industries NV

- Marius Pedersen A/S

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Insights and Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Extended Producer-Responsibility (EPR) Mandates Accelerating Fee-Based Collection in EU & Canada

- 4.2.2 China's Ban on Low-Grade Scrap Imports Boosting Domestic Recycling Margins in Asia

- 4.2.3 Rapid Scale-up of Advanced (Pyrolysis & Solvolysis) Recycling Facilities in U.S. Gulf Coast

- 4.2.4 Corporate-Backed Circularity Funds (e.g., Closed Loop Partners) De-Risking Infrastructure Projects

- 4.2.5 AI-Driven Optical Sorting Lines Cutting OPEX by 18-25 % in MRFs

- 4.2.6 FMCG Re-design toward Mono-Material Flexible Packaging Lifting Recoverable Volumes

- 4.3 Market Restraints

- 4.3.1 Plastic overproduction and overconsumption strain waste management, hindering recycling and circular economy efforts

- 4.3.2 Negative Netbacks for Recycled PE & PP When Brent < US$55/bbl

- 4.3.3 High Contamination (>12 %) in Curb-Side Streams Limiting Mechanical Recyclate Quality

- 4.3.4 Carbon-Tax Exemptions for Incineration Undercutting Recycling Economics in Nordics

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

- 4.8 Investment & Capacity Expansion Analysis

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Polymer Type

- 5.1.1 Polyethylene (PE)

- 5.1.2 Polypropylene (PP)

- 5.1.3 Polyethylene Terephthalate (PET)

- 5.1.4 Polystyrene (PS)

- 5.1.5 Polyvinyl Chloride (PVC)

- 5.1.6 Other Polymers (ABS, PA, etc.)

- 5.2 By Source

- 5.2.1 Industrial

- 5.2.2 Commercial (Retail & Office)

- 5.2.3 Residential

- 5.2.4 Construction & Demolition

- 5.2.5 Others(Institutional, Healthcare, Curb-side waste, etc.)

- 5.3 By Service Type

- 5.3.1 Collection, Transportation & Sorting

- 5.3.2 Disposal/ Treatment

- 5.3.2.1 Mechanical Recycling

- 5.3.2.2 Chemical / Advanced Recycling

- 5.3.2.3 Incineration with Energy Recovery

- 5.3.2.4 Controlled Landfilling

- 5.3.3 Others (Consulting, Audit & Training, etc.)

- 5.4 By End-Use Industry

- 5.4.1 Packaging

- 5.4.2 Construction

- 5.4.3 Automotive & E-Mobility

- 5.4.4 Electrical & Electronics

- 5.4.5 Textiles & Fashion

- 5.4.6 Healthcare

- 5.4.7 Others (Agriculture, Consumer Goods, etc.)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Peru

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.5.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 Kuwait

- 5.5.5.5 Turkey

- 5.5.5.6 Egypt

- 5.5.5.7 South Africa

- 5.5.5.8 Nigeria

- 5.5.5.9 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)}

- 6.4.1 Veolia Environnement SA

- 6.4.2 SUEZ SA

- 6.4.3 Waste Management Inc.

- 6.4.4 Republic Services Inc.

- 6.4.5 Clean Harbors Inc.

- 6.4.6 Remondis SE & Co. KG

- 6.4.7 Biffa PLC

- 6.4.8 Stericycle Inc.

- 6.4.9 Covanta Holding Corp.

- 6.4.10 TOMRA Systems ASA

- 6.4.11 Plastic Energy Ltd.

- 6.4.12 Brightmark LLC

- 6.4.13 Agilyx Corporation

- 6.4.14 TerraCycle Inc.

- 6.4.15 Waste Connections Inc.

- 6.4.16 DS Smith PLC

- 6.4.17 Borealis AG

- 6.4.18 LyondellBasell Industries NV

- 6.4.19 Marius Pedersen A/S

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

日本塑膠廢棄物管理服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)德國塑膠廢棄物管理服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

日本塑膠廢棄物管理服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)德國塑膠廢棄物管理服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 塑膠廢棄物管理服務市場:按服務類型、塑膠類型、來源和最終用途產業分類-2026-2032年全球市場預測塑膠廢棄物管理與回收:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

塑膠廢棄物管理服務市場:按服務類型、塑膠類型、來源和最終用途產業分類-2026-2032年全球市場預測塑膠廢棄物管理與回收:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球塑膠廢棄物管理市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球塑膠廢棄物管理市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 塑膠廢棄物管理市場:依塑膠類型、應用、回收方法、技術、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測

塑膠廢棄物管理市場:依塑膠類型、應用、回收方法、技術、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測 寵物水族箱及池塘維護系統市場預測至2034年-全球水族箱設備及系統、池塘設備及系統、水族箱及池塘耗材、水族箱及池塘配件、服務及解決方案以及區域分析自動化寵物護理系統市場預測至2034年—按系統類型、寵物類型、連接方式、技術、最終用戶、分銷管道和地區分類的全球分析

寵物水族箱及池塘維護系統市場預測至2034年-全球水族箱設備及系統、池塘設備及系統、水族箱及池塘耗材、水族箱及池塘配件、服務及解決方案以及區域分析自動化寵物護理系統市場預測至2034年—按系統類型、寵物類型、連接方式、技術、最終用戶、分銷管道和地區分類的全球分析 塑膠監管市場:按監管類型、應用、監管機構、塑膠類型和地區分類塑膠廢棄物升級再造市場預測-全球分析(按塑膠類型、來源、升級再造類型、製程技術、產量、應用、最終用戶和地區分類)——2034年

塑膠監管市場:按監管類型、應用、監管機構、塑膠類型和地區分類塑膠廢棄物升級再造市場預測-全球分析(按塑膠類型、來源、升級再造類型、製程技術、產量、應用、最終用戶和地區分類)——2034年