|

市場調查報告書

商品編碼

2044044

中國LED外延MOCVD設備:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)China LED Epitaxy MOCVD Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

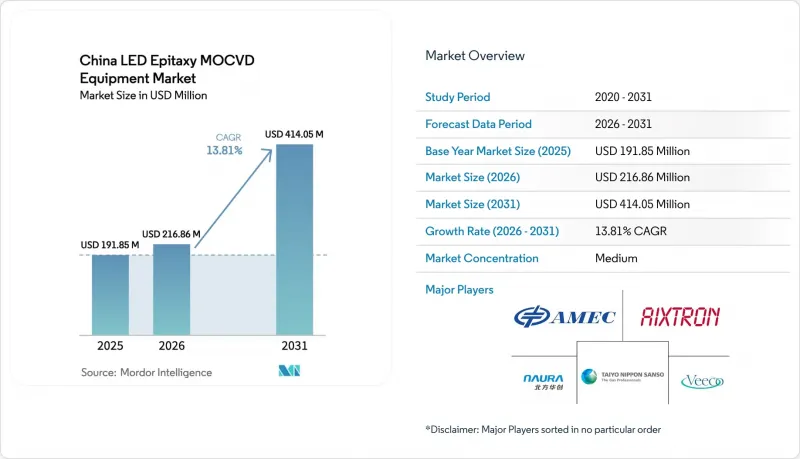

預計到 2025 年,中國用於 LED 外延的 MOCVD 設備市場規模將達到 1.9185 億美元,到 2026 年將達到 2.1686 億美元,到 2031 年將達到 4.1405 億美元,2026 年至 2031 年的複合年成長率為 13.1%。

強力的政策支持、垂直整合型裝置製造商的快速產能擴張以及向先進顯示器和汽車應用領域的穩步轉型,正推動國內反應器的投資。強而有力的在地採購政策將政府獎勵與本地設備採購掛鉤,使得中國供應商成為新建生產線的首選。同時,即將向200毫米晶圓的過渡有望帶來結構性的成本重置,即使通用照明需求趨於平穩,也能保持單位成本的吸引力。目前,主要的智慧型手機和麵板製造商正在投資建造中試規模的微型LED生產線,並透過提高均勻性標準來最佳化緊密耦合的淋浴設備結構。同時,鎵和鋁前驅體持續存在的供應風險,促使企業加速簽訂多年合約以確保國內化學品供應。儘管通用裝置市場出現週期性低迷,但這些因素共同推動了中國LED外延MOCVD設備市場的強勁前景。

中國LED外延MOCVD設備市場趨勢及洞察。

汽車照明領域對高亮度氮化鎵基LED的需求不斷成長。

汽車製造商正從鹵素燈和HID燈轉向自適應GaN陣列,後者可提供高達200流明/瓦的光效,從而降低能耗並延長電動車的續航里程。三安光電於2025年收購Lumileds,圖了龐大的專利組合和汽車級認證的GaN製造程序,使本地一級供應商能夠搶佔高價值模組市場。中國工業和資訊化部(工信部)發布的新車燈法規要求採用無眩光遠光燈模式,這實際上鞏固了像素尋址GaN作為合規技術的地位。 2025年以後原料成本的上漲將進一步凸顯這些高效率晶片的優勢,因為達到所需亮度所需的晶片數量將會減少。這些因素共同推動了對設備的日益成長的需求,因為車燈製造商正在將其所有生產線改造為高功率GaN生產線。

補貼改革將加速日本MOCVD的引進。

2025年12月的一項指令規定,獲得國家補貼的條件是國產設備的採用率必須達到50%。這意味著依賴公共資金的晶圓廠將面臨困境:除非採用國產反應堆,否則將損失810億元人民幣(約114億美元)的補貼。為此,中國先進微加工設備有限公司(AME)已批量交付其最新的6片和8片晶圓設備,在地採購超過80%,從而降低了美國出口限制帶來的授權風險。早期採用者報告稱,在50個晶圓加工週期內,波長均勻性誤差小於2%,這一水平此前只有高階進口設備才能達到,進一步加速了國產化進程。

通用照明用LED的需求放緩與飽和

到2024年,LED在都市區家庭的普及率將超過75%,更換週期將從3年延長至約7年。加之新屋開工速度放緩,預計2025年,通用氮化鎵(GaN)晶圓的價格將下降8%,製造商的運轉率也將降至70%以上。儘管供應商正在將資金重新配置到汽車、園藝和UVC產業,但這項轉型期對傳統150毫米設備的短期訂單造成了嚴重影響。

細分市場分析

預計2025年,氮化鎵(GaN)平台將在中國LED外延MOCVD設備市場佔67.19%的佔有率。這主要得益於汽車頭燈、園藝燈具和中試級微顯示器生產線等領域的應用。 AlGaN紫外設備預計將以14.53%的複合年成長率成長。這主要歸功於市政供水事業和醫療機構對不含汞、波長265-275奈米且符合消毒標準、不產生化學副產物的發光元件的需求。氮化鋁晶片技術的進步也為此成長提供了支持。與藍寶石晶片相比,氮化鋁晶片可實現更高的電流密度,從而減少每盞燈所需的晶片數量,降低燈具成本。

為因應通用照明需求成長乏力,氮化鎵 (GaN) 製造商正將過剩產能轉向高亮度汽車陣列和早期微顯示器認證測試生產。雖然這些應用需要嚴格的篩選,但由此帶來的溢價確保了整體產運轉率的健康成長。紫外線 (UV) 領域的持續發展勢頭取決於基板技術的進步,其中氮化鋁晶片在提升性能和成本效益方面發揮著至關重要的作用。

截至2025年,傳統150mm反應器在中國LED外延MOCVD設備市場中佔45.24%的比重。預計到2031年,對200mm以上尺寸系統的需求將以每年14.14%的速度成長。這一成長主要歸功於晶圓廠能夠透過提高產能和改善基板利用率,將單晶片成本降低35%至40%。

ALLOS 和 Ennostar 合作進行的 200 毫米矽基基板(GaN) 專案等合作開發專案的激增,凸顯了這一轉變。反應器 OEM 廠商正在增大晶片直徑,同時精細調整氣體流速,以確保在大尺寸晶圓上波長變化小於 2%,這對於高品質微顯示器至關重要。一旦晶體生長設備製造商克服了目前的前置作業時間瓶頸,那些能夠及早掌握這些參數的設備製造商將有望抓住下一波訂單浪潮。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 汽車照明領域對高亮度氮化鎵基LED的需求不斷成長。

- 補貼制度改革將加速日本MOCVD的引進。

- 自2026年起,中國IDM LED製造商的產能將持續擴大。

- 半導體製造設備供應鏈的本地化努力

- 透過過渡到 200 毫米藍寶石晶圓降低裝置單位成本

- 智慧型手機廠商支援的新興Micro-LED顯示器項目

- 市場限制因素

- 一般照明用LED的需求放緩並趨於飽和。

- 新建反應器資本密集度高,投資回收期長

- 高純度原料供應鏈的波動性

- 外延設施遵守嚴格環境法規的成本

- 產業供應鏈分析

- 技術展望

- 監理情勢

- 宏觀經濟因素對市場的影響

- 波特五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 按類別分類的LED材料系統

- 基於氮化鎵的LED外延系統

- AlGaN紫外線LED外延系統

- AlInGaP LED外延系統

- 晶圓尺寸特定功能

- 最大可達 100 毫米

- 150 mm

- 200毫米或以上

- 反應器配置

- 行星反應爐

- 淋浴設備噴頭式反應器

- 最終用戶

- LED整合製造商(IDM)

- 外延代工廠及外延專業供應商

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Advanced Micro-Fabrication Equipment Inc. China

- Veeco Instruments Inc.

- Aixtron SE

- NAURA Technology Group Co., Ltd.

- Jiangsu Advanced Power Semiconductor Co., Ltd.

- Taiyo Nippon Sanso Corporation

- Jusung Engineering Co., Ltd.

- Wuhan HC Semitek Corporation

- Silan Azure Co., Ltd.

- San'an Optoelectronics Co., Ltd.

- HC SemiTek Corp.

- Optigon Technologies(Shanghai)Co., Ltd.

- EpiWorld International Co., Ltd.

- Tsinghua Tongfang Co., Ltd.

- Tianjin Zhonghuan Semiconductor Co., Ltd.

- Chongqing Silan Azure Tech Co., Ltd.

- ProLight Opto Technology Inc.

- Epileds Technologies Inc.

- Changelight Co., Ltd.

- MOCVD Semiconductor Equipment Co., Ltd.

第7章 市場機會與未來展望

The China LED epitaxy MOCVD equipment market size is projected to be USD 191.85 million in 2025, USD 216.86 million in 2026, and reach USD 414.05 million by 2031, growing at a CAGR of 13.81% from 2026 to 2031.

Solid policy support, rapid capacity expansion by vertically integrated device makers, and a steady pivot toward advanced display and automotive applications are steering capital toward domestic reactors. Strong localization rules that tie government incentives to local tool purchases have made Chinese suppliers the default choice for new lines, while a looming switch to 200 millimeter wafers promises a structural cost reset that keeps unit economics attractive even as general lighting demand plateaus. Large smart phone and panel makers are now underwriting pilot micro LED lines, tightening uniformity specifications that favor close coupled showerhead architectures. Meanwhile, persistent supply risk around gallium and aluminum precursors accelerates multi-year procurement contracts that lock in domestic chemical streams. Together, these factors sustain a robust outlook for the China LED epitaxy MOCVD equipment market despite cyclical softness in commodity devices.

China LED Epitaxy MOCVD Equipment Market Trends and Insights

Rising Demand for High Brightness GaN Based LEDs in Automotive Lighting

Automakers are shifting from halogen or HID lamps to adaptive GaN arrays that deliver up to 200 lumens per watt, cutting power draw and boosting electric-vehicle range. Sanan Optoelectronics' 2025 purchase of Lumileds secured a sizeable patent library and automotive-qualified GaN recipes, positioning local tier-one suppliers to capture higher value modules. New headlamp rules issued by MIIT mandate glare-free high beam patterns, effectively locking in pixel-addressable GaN as the compliant technology. Higher raw material costs since 2025 further favor these efficient dies, because fewer chips now achieve the required brightness. Collectively, these forces lift equipment demand as headlamp makers convert entire production lines to high-power GaN.

Subsidy Reforms Accelerating Domestic MOCVD Adoption

A December 2025 directive links state subsidies to a 50% domestic tool quota, forcing fabs that rely on public funding to qualify Chinese reactors or lose access to RMB 81 billion (USD 11.4 billion) in aid. Advanced Micro-Fabrication Equipment Inc. China responded by shipping production batches of its newest six and eight-wafer tools with over 80% local content, easing licensing risk under United States export controls. Early adopters report wavelength uniformity under 2% across 50 wafer runs, a level once attainable only on premium imports, supporting accelerated switch overs.

Slowdown In General Lighting LED Demand Saturation

Urban households surpassed 75% LED penetration by 2024, elongating replacement cycles from three to roughly seven years. Combined with slower real estate starts, this dynamic reduced commodity GaN wafer pricing by 8 % in 2025 and cut merchant utilization into the high seventies. Suppliers are reallocating capital toward automotive, horticultural, and UVC segments, but the transition period weighs on near term orders for legacy 150 millimeter tools.

Other drivers and restraints analyzed in the detailed report include:

- Capacity Expansion of Chinese IDM LED Manufacturers Post-2026

- Localization Initiatives for Semiconductor Equipment Supply Chains

- High Capital Intensity and Long Payback Periods for New Reactors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

GaN platforms accounted for 67.19% of the China LED epitaxy MOCVD equipment market share in 2025, driven by their use in automotive headlamps, horticultural lamps, and pilot micro display lines. AlGaN ultraviolet tools are expected to grow at a 14.53% CAGR as municipal water and healthcare operators prefer mercury-free 265-275 nanometer emitters that meet disinfection standards without chemical byproducts. This growth is supported by advancements in aluminum nitride wafers, which enable higher current density compared to sapphire, reducing die counts per lamp and lowering fixture costs.

GaN producers are addressing flat general lighting demand by redirecting surplus capacity into high-brightness automotive arrays and early micro display qualification runs. These applications require tight binning but offer price premiums, ensuring healthy overall utilization. Sustained UV momentum relies on substrate breakthroughs, with aluminum nitride wafers playing a critical role in enhancing performance and cost efficiency.

Legacy 150 millimeter reactors accounted for 45.24% of the China LED epitaxy MOCVD equipment market size in 2025. The demand for 200 millimeter and larger systems is expected to grow at a rate of 14.14% through 2031. This growth is driven by fabs achieving 35-40% per die cost savings through higher throughput and improved substrate utilization.

A surge of joint development projects, such as the 200 millimeter GaN on silicon program between ALLOS and Ennostar, underlines the migration. Reactor OEMs are enlarging platen diameters while refining gas flow to hold sub-2% wavelength variation across larger wafers, prerequisites for premium micro displays. Tool makers that master these parameters early will capture next wave orders once crystal growers clear current lead time bottlenecks.

The China LED Epitaxy MOCVD Equipment Market Report is Segmented by LED Material System (GaN-Based LED Epitaxy Systems, and More), Wafer Size Capability (Up To 100mm, 150mm, and 200mm and Above), Reactor Configuration (Planetary Reactors, and Showerhead Reactors), End User (Integrated LED Manufacturers, and Epitaxy Foundries and Merchant Epi Suppliers). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Advanced Micro-Fabrication Equipment Inc. China

- Veeco Instruments Inc.

- Aixtron SE

- NAURA Technology Group Co., Ltd.

- Jiangsu Advanced Power Semiconductor Co., Ltd.

- Taiyo Nippon Sanso Corporation

- Jusung Engineering Co., Ltd.

- Wuhan HC Semitek Corporation

- Silan Azure Co., Ltd.

- San'an Optoelectronics Co., Ltd.

- HC SemiTek Corp.

- Optigon Technologies (Shanghai) Co., Ltd.

- EpiWorld International Co., Ltd.

- Tsinghua Tongfang Co., Ltd.

- Tianjin Zhonghuan Semiconductor Co., Ltd.

- Chongqing Silan Azure Tech Co., Ltd.

- ProLight Opto Technology Inc.

- Epileds Technologies Inc.

- Changelight Co., Ltd.

- MOCVD Semiconductor Equipment Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for High Brightness GaN-Based LEDs in Automotive Lighting

- 4.2.2 Subsidy Reforms Accelerating Domestic MOCVD Adoption

- 4.2.3 Capacity Expansion of Chinese IDM LED Manufacturers Post-2026

- 4.2.4 Localization Initiatives for Semiconductor Equipment Supply Chains

- 4.2.5 Shift to 200 mm Sapphire Wafers Reducing Per-Device Cost

- 4.2.6 Emerging Micro-LED Display Projects Backed by Smartphone OEMs

- 4.3 Market Restraints

- 4.3.1 Slowdown in General Lighting LED Demand Saturation

- 4.3.2 High Capital Intensity and Long Payback Periods for New Reactors

- 4.3.3 Supply Chain Volatility in High Purity Source Materials

- 4.3.4 Stringent Environmental Compliance Costs for Epitaxy Facilities

- 4.4 Industry Supply Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By LED Material System

- 5.1.1 GaN-based LED Epitaxy Systems

- 5.1.2 AlGaN UV LED Epitaxy Systems

- 5.1.3 AlInGaP LED Epitaxy Systems

- 5.2 By Wafer Size Capability

- 5.2.1 Upto 100 mm

- 5.2.2 150 mm

- 5.2.3 200 mm and Above

- 5.3 By Reactor Configuration

- 5.3.1 Planetary Reactors

- 5.3.2 Showerhead Reactors

- 5.4 By End User

- 5.4.1 Integrated LED Manufacturers (IDMs)

- 5.4.2 Epitaxy Foundries and Merchant Epi Suppliers

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Advanced Micro-Fabrication Equipment Inc. China

- 6.4.2 Veeco Instruments Inc.

- 6.4.3 Aixtron SE

- 6.4.4 NAURA Technology Group Co., Ltd.

- 6.4.5 Jiangsu Advanced Power Semiconductor Co., Ltd.

- 6.4.6 Taiyo Nippon Sanso Corporation

- 6.4.7 Jusung Engineering Co., Ltd.

- 6.4.8 Wuhan HC Semitek Corporation

- 6.4.9 Silan Azure Co., Ltd.

- 6.4.10 San'an Optoelectronics Co., Ltd.

- 6.4.11 HC SemiTek Corp.

- 6.4.12 Optigon Technologies (Shanghai) Co., Ltd.

- 6.4.13 EpiWorld International Co., Ltd.

- 6.4.14 Tsinghua Tongfang Co., Ltd.

- 6.4.15 Tianjin Zhonghuan Semiconductor Co., Ltd.

- 6.4.16 Chongqing Silan Azure Tech Co., Ltd.

- 6.4.17 ProLight Opto Technology Inc.

- 6.4.18 Epileds Technologies Inc.

- 6.4.19 Changelight Co., Ltd.

- 6.4.20 MOCVD Semiconductor Equipment Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

化學氣相沉積 (CVD) 市場規模、佔有率和趨勢分析報告:按類別、應用、地區和細分市場分類 - 預測 (2026–2033)

化學氣相沉積 (CVD) 市場規模、佔有率和趨勢分析報告:按類別、應用、地區和細分市場分類 - 預測 (2026–2033) 化學氣相沉積設備市場報告:按技術、應用、最終用戶和地區分類(2026-2034 年)

化學氣相沉積設備市場報告:按技術、應用、最終用戶和地區分類(2026-2034 年) LED外延MOCVD設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區LED外延MOCVD設備:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本LED外延MOCVD設備:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

LED外延MOCVD設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區LED外延MOCVD設備:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本LED外延MOCVD設備:市佔率分析、產業趨勢與統計及成長預測(2026-2031年) 化學氣相沉積(CVD)市場:按技術類型、材料、前驅體類型、應用和最終用途產業分類-2026-2032年全球市場預測

化學氣相沉積(CVD)市場:按技術類型、材料、前驅體類型、應用和最終用途產業分類-2026-2032年全球市場預測 2026年全球異質接面(HJT)等離子體增強化學氣相沉積(PECVD)設備市場報告2026年全球等離子體增強化學蒸氣沉積(PECVD)設備市場報告

2026年全球異質接面(HJT)等離子體增強化學氣相沉積(PECVD)設備市場報告2026年全球等離子體增強化學蒸氣沉積(PECVD)設備市場報告 半導體化學氣相沉積設備市場:依產品類型、應用、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測半導體薄膜沉積設備市場:按材料、設備、技術、產業、終端用戶應用、國家和地區分類-全球產業分析、市場規模、市場佔有率和預測(2026-2033 年)

半導體化學氣相沉積設備市場:依產品類型、應用、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測半導體薄膜沉積設備市場:按材料、設備、技術、產業、終端用戶應用、國家和地區分類-全球產業分析、市場規模、市場佔有率和預測(2026-2033 年)