|

市場調查報告書

商品編碼

2043900

美國汽車引擎機油:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)United States Automotive Engine Oils - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

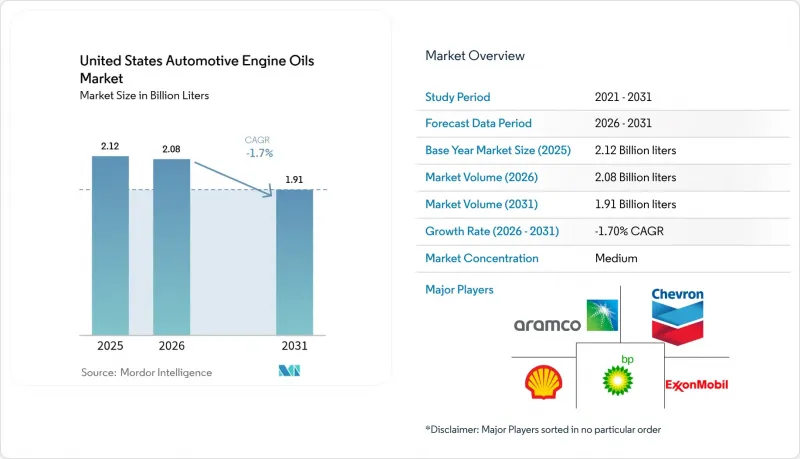

預計到 2025 年,美國汽車機油市場將萎縮至 21.2 億公升;到 2026 年將萎縮至 20.8 億公升;到 2031 年將萎縮至 19.1 億升。

預計從 2026 年到 2031 年,複合年成長率將下降 1.7%。

市場萎縮是由結構性變化所驅動的。儘管單車潤滑油消耗量有所下降,但得益於貫穿車輛整個使用壽命的原廠加註計劃、預測性維護演算法以及超低黏度規格的引入,潤滑油品質卻在不斷提高。根據2025年3月推出的API SP和ILSAC GF-7標準,已有超過1800種配方獲得許可,這些標準依賴更昂貴的添加劑化學技術和大量的測功機測試。同時,福特的「智慧機油壽命監測系統」將在2025年底前將平均換油週期延長一倍以上,達到10,000英里;同年,勝牌(Valvoline)也獲得了康明斯(Cummins)的核准,其重負荷機油的使用壽命可達100,000英里。雖然這些進步提高了產品利潤率,但卻縮小了市場需求量,從而鞏固了美國汽車機油市場的長期下滑趨勢。

美國汽車機油市場的趨勢與洞察

API SP/ILSAC GF-7 標準的引入

API SP 和 ILSAC GF-7 標準於 2025 年 3 月推出,目前已批准超過 1800 種混合油,但由於北美只有少數實驗室擁有必要的 Sequence IX 和 Sequence X 測試設備,認證工作仍積壓 6-9 個月。每次測試週期成本為 5 萬至 7 萬美元,需要佔用測功機長達六週,這使得擁有自有測試設施的製造商更具優勢。福特、通用汽車、豐田、本田和 Stellantis 等公司將於 2026 年強制要求工廠出貨的機油符合 GF-7 標準,這將使獲得認證的品牌能夠比傳統的 API SN Plus 機油獲得 10-15% 的溢價。儘管由於中型調配商退出市場以及 Lubrizol 和 Infinium 等公司對添加劑包的授權,銷售量有所下降,但每公升機油的利潤率卻在擴大,這為美國汽車引擎油市場的複合年成長率貢獻了約 0.3 個百分點。

快速過渡到全合成機油和0W-20及以下黏度等級的機油

到2024年,合成油將佔潤滑油市場價值的近68%,42%的新車車主手冊中都列出了0W-20機油。到2025年,超過70%的車型規格要求使用0W-20或更低黏度的機油,一些混合動力汽車型也開始使用0W-16機油,以滿足美國環保署(EPA)到2032年設定的更嚴格的車隊平均二氧化碳排放上限(85克/英里)。混合油生產商透過投資III類基礎油和聚偏二氧(PAO)原料來應對這一需求。埃克森美孚位於新加坡的升級廠於2025年初運作,每年將為全球供應鏈增加120萬噸高黏度指數基礎油。儘管每公升的需求量持續下降,但合成油的市場佔有率正在迅速成長,為美國汽車機油市場貢獻了0.4個百分點的淨成長。

基礎油價格與供應波動

2024年至2025年間,由於煉油廠的計畫性維護以及輕質原油供應結構的變化,II類和III類原油現貨價格每季波動15%至20%,給獨立調和商的利潤空間帶來壓力。鉬和硼等添加劑價格上漲12%至18%,進一步擠壓了成本。在能源轉型壓力下,由於美國預計不會再有新的煉油廠擴建,價格進一步波動的可能性不大,這可能導致美國汽車機油市場年複合成長率約為0.4個百分點,直到亞洲新增產能填補國內缺口為止。

細分市場分析

到2025年,乘用車引擎油將占美國汽車引擎油市場的63.45%,這與美國2.9億輛汽車的規模相符。儘管內燃機汽車仍將佔據市場主導地位,但由於電氣化、遠端資訊處理技術以及原廠機油使用壽命延長等因素推動的保養模式變化,預計乘用車引擎油的銷售量將有所下降。重型車輛機油的銷售量下降速度將較為緩慢,因為長途柴油車的電氣化仍面臨挑戰,而且這些車輛的運作通常為15-20年。摩托車機油的銷量降幅最小(預測期(2026-2031年)的複合年成長率為-1.64%),因為巡航摩托車和旅行摩托車的騎士仍然保持傳統的換油週期,而且電氣化選擇有限。

產品組合也在改變。在乘用車引擎油(PCMO)領域,0W-20及更低黏度等級的產品成長最為迅速,這主要受原始設備製造商(OEM)針對多污染物排放法規的要求所驅動。傳統的10W-30和10W-40等級的產品則僅限於2015年以前生產的車輛,而這類車輛的市場佔有率正在不斷萎縮。重型柴油引擎油(HDMO)市場也呈現類似的趨勢,車隊正在採用0W-30或5W-30 CK-4機油來提高冷啟動效率。勝牌(Valvoline)經康明斯認證的10萬英里重型柴油引擎油表明,即使產品價值不斷提升,延長換油週期也進一步加劇了單次使用銷售量的下滑。

《美國汽車機油市場報告》按樹脂類型(乘用車引擎油、重型車輛機油、摩托車機油)和基料(礦物油、合成油、半合成油、生物基油)進行細分。市場預測以銷售量(公升)為單位。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- API SP/ILSAC GF-7 標準的引入

- 快速過渡到全合成機油和≤0W-20黏度等級

- 美國車輛保有量老化,其中許多車輛已服役超過 12 年,這支撐了市場需求。

- 人工智慧驅動的預測性維護程序延長了換油週期。

- 原始設備製造商的排碳權策略正在推動超低黏度原廠潤滑油的使用。

- 市場限制因素

- 基礎油價格與供應波動

- 由於GF-7測試設施產能不足,認證被推遲。

- 所有車輛使用的原廠配套全壽命機油抑制了售後市場的銷售量。

- 價值鏈分析

- 監理情勢

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 產業間競爭

第5章 市場規模與成長預測

- 按油型

- 乘用車引擎機油(PCMO)

- 0W-XX

- 5W-XX

- 10W-XX

- 15W-XX

- 單級油

- 其他年級

- 重型機油(HDMO)

- 0W-XX

- 5W-XX

- 10W-XX

- 15W-XX

- 單級油

- 其他年級

- 摩托車機油(MCO)

- 0W-XX

- 5W-XX

- 10W-XX

- 15W-XX

- 單級油

- 其他年級

- 乘用車引擎機油(PCMO)

- 基礎油

- 礦物油

- 合成

- 半複合材料

- 生物基

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- AMSOIL INC.

- Blauparts LLC

- BP plc

- Chevron Corporation

- CITGO Petroleum

- ExxonMobil Corporation

- FUCHS

- Gulf Oil International Ltd

- Idemitsu Kosan Co., Ltd.

- Liqui Moly GmbH

- Lucas Oil Products, Inc.

- Motul

- Petro-Canada Lubricants Inc.,

- Phillips 66 Lubricants

- Quaker Houghton.

- Shell plc

- TotalEnergies

- Saudi Arabian Oil Co.

第7章 市場機會與未來展望

第8章:執行長面臨的主要策略挑戰:

The United States Automotive Engine Oils Market size is projected to be 2.12 billion liters in 2025, 2.08 billion liters in 2026, and decline to 1.91 billion liters by 2031, declining at a CAGR of -1.7% from 2026 to 2031.

A structural shift is driving this contraction: life-of-vehicle factory-fill programs, predictive-maintenance algorithms, and ultra-low-viscosity specifications raise lubricant quality even as per-vehicle consumption falls. API SP and ILSAC GF-7 standards, introduced in March 2025, have already licensed more than 1,800 formulations that rely on costlier additive chemistries and extensive dynamometer testing. Meanwhile, Ford's Intelligent Oil-Life Monitor more than doubled the average drain interval to 10,000 miles by late 2025, and Valvoline secured Cummins approval for a 100,000-mile heavy-duty oil the same year. Although these advances elevate product margins, they also shrink the serviceable volume pool, anchoring the long-term downtrend for the United States automotive engine oils market.

United States Automotive Engine Oils Market Trends and Insights

API SP/ILSAC GF-7 Specification Roll-Out

Launched in March 2025, API SP and ILSAC GF-7 have already licensed more than 1,800 blends, yet certification backlogs of 6-9 months persist because only a handful of North American labs own the requisite Sequence IX and Sequence X stands. Each test cycle costs USD 50,000-75,000 and ties up a dynamometer for up to six weeks, favoring producers with captive facilities. Ford, General Motors, Toyota, Honda, and Stellantis mandated GF-7 for 2026 factory fills, letting certified brands capture 10-15% price premiums over legacy API SN Plus oils. As mid-tier blenders exit or co-license additive packages from Lubrizol or Infineum, volume erosion continues, but margin per litre widens, adding roughly 0.3 percentage points to the United States automotive engine oils market CAGR.

Rapid Shift to Full-Synthetic and less than or equal to 0W-20 Grades

Synthetic formulas represented close to 68% of lubricant value in 2024, with 0W-20 appearing in 42% of new-vehicle owner manuals. By 2025, more than 70% of model-year specifications called for 0W-20 or thinner, and select hybrid lines moved to 0W-16 to meet tightening EPA fleet-average CO2 ceilings of 85 g/mile by 2032. Blenders responded by investing in Group III and PAO feedstock: ExxonMobil's Singapore Resid Upgrade, commissioned early 2025, added 1.2 million ton/year of high-viscosity-index base stocks for global allocation. Although litre demand keeps falling, the synthetic share grows fast enough to contribute a net 0.4 percentage-point lift to the United States automotive engine oils market trajectory.

Base-Oil Price and Supply Volatility

Group II and Group III spot prices swayed 15-20% quarter-to-quarter during 2024-2025 because of refinery turnarounds and lighter crude slates, leaving independent blenders exposed to margin compression. Additive elements such as molybdenum and boron climbed 12-18%, further squeezing costs. US refinery additions remain unlikely under energy-transition pressure, so volatility will persist and shave around 0.4 percentage points off the United States automotive engine oils market CAGR until new Asian capacity backfills domestic shortfalls.

Other drivers and restraints analyzed in the detailed report include:

- Aging Vehicle Parc more than 12 Years Sustaining Demand

- AI-Driven Predictive-Maintenance Programs Extending Drain Intervals

- Limited GF-7 Test-Stand Capacity Delaying Certifications

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passenger car motor oil accounted for 63.45% of the United States Automotive Engine Oils market size in 2025, reflecting the nation's 290 million-unit vehicle parc. Although internal-combustion cars continue to dominate the fleet, PCMO volume is forecast to fall as electrification, telematics, and factory-fill longevity reshape service patterns. Heavy-duty motor oil volumes erode more slowly because long-haul diesels remain hard to electrify and typically stay in service 15-20 years. Motorcycle engine oil shows the smallest contraction (-1.64% CAGR during the forecast period (2026-2031)) because cruiser and touring riders maintain legacy drain intervals and have limited electric alternatives.

The internal mix is also changing. Within PCMO, 0W-20 and thinner grades expand fastest, driven by OEM mandates tied to multi-pollutant standards. Conventional 10W-30 and 10W-40 grades retreat to a shrinking pool of vehicles built before 2015. HDMO mirrors this trend as fleets adopt 0W-30 or 5W-30 CK-4 oils for cold-start efficiency. Valvoline's 100,000-mile Cummins-approved HDMO illustrates how extended drains deepen litre-volume shrinkage even when product value rises.

The United States Automotive Engine Oils Market Report is Segmented by Resin Type (Passenger Car Motor Oil, Heavy Duty Motor Oil, and Motorcycle Engine Oil) and Base Stock (Mineral, Synthetic, Semi-Synthetic, and Bio-Based). The Market Forecasts are Provided in Terms of Volume (Liters).

List of Companies Covered in this Report:

- AMSOIL INC.

- Blauparts LLC

- BP p.l.c.

- Chevron Corporation

- CITGO Petroleum

- ExxonMobil Corporation

- FUCHS

- Gulf Oil International Ltd

- Idemitsu Kosan Co., Ltd.

- Liqui Moly GmbH

- Lucas Oil Products, Inc.

- Motul

- Petro-Canada Lubricants Inc.,

- Phillips 66 Lubricants

- Quaker Houghton.

- Shell plc

- TotalEnergies

- Saudi Arabian Oil Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 API SP/ILSAC GF-7 specification roll-out

- 4.2.2 Rapid shift to full-synthetic and <=0W-20 grades

- 4.2.3 Aging US vehicle parc >12 yrs sustaining demand

- 4.2.4 AI-driven predictive-maintenance programs extending drain intervals

- 4.2.5 OEMs' carbon-credit strategies favouring ultra-low-viscosity factory-fill

- 4.3 Market Restraints

- 4.3.1 Base-oil price and supply volatility

- 4.3.2 Limited GF-7 test-stand capacity delaying certifications

- 4.3.3 OEM factory-fill life-of-vehicle oils curbing after-market volumes

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Industry Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Passenger Car Motor Oil (PCMO)

- 5.1.1.1 0W-XX

- 5.1.1.2 5W-XX

- 5.1.1.3 10W-XX

- 5.1.1.4 15W-XX

- 5.1.1.5 Monogrades

- 5.1.1.6 Other Grades

- 5.1.2 Heavy Duty Motor Oil (HDMO)

- 5.1.2.1 0W-XX

- 5.1.2.2 5W-XX

- 5.1.2.3 10W-XX

- 5.1.2.4 15W-XX

- 5.1.2.5 Monogrades

- 5.1.2.6 Other Grades

- 5.1.3 Motorcycle Engine Oil (MCO)

- 5.1.3.1 0W-XX

- 5.1.3.2 5W-XX

- 5.1.3.3 10W-XX

- 5.1.3.4 15W-XX

- 5.1.3.5 Monogrades

- 5.1.3.6 Other Grades

- 5.1.1 Passenger Car Motor Oil (PCMO)

- 5.2 By Base Stock

- 5.2.1 Mineral

- 5.2.2 Synthetic

- 5.2.3 Semi-Synthetic

- 5.2.4 Bio-Based

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 AMSOIL INC.

- 6.4.2 Blauparts LLC

- 6.4.3 BP p.l.c.

- 6.4.4 Chevron Corporation

- 6.4.5 CITGO Petroleum

- 6.4.6 ExxonMobil Corporation

- 6.4.7 FUCHS

- 6.4.8 Gulf Oil International Ltd

- 6.4.9 Idemitsu Kosan Co., Ltd.

- 6.4.10 Liqui Moly GmbH

- 6.4.11 Lucas Oil Products, Inc.

- 6.4.12 Motul

- 6.4.13 Petro-Canada Lubricants Inc.,

- 6.4.14 Phillips 66 Lubricants

- 6.4.15 Quaker Houghton.

- 6.4.16 Shell plc

- 6.4.17 TotalEnergies

- 6.4.18 Saudi Arabian Oil Co.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

8 Key Strategic Questions for CEOs

汽車機油市場:按產品類型、車輛類型、應用、最終用戶和分銷管道分類-2026-2032年全球市場預測

汽車機油市場:按產品類型、車輛類型、應用、最終用戶和分銷管道分類-2026-2032年全球市場預測 2026年全球汽車機油市場報告

2026年全球汽車機油市場報告 汽車機油市場:依產品類型、黏度等級、應用、銷售管道和地區分類

汽車機油市場:依產品類型、黏度等級、應用、銷售管道和地區分類 2026-2030年全球汽車機油市場

2026-2030年全球汽車機油市場 日本汽車機油:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

日本汽車機油:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 全球汽車機油市場:2025年至2030年預測全球汽車機油市場規模(按等級、燃料類型、車輛類型、區域範圍和預測)

全球汽車機油市場:2025年至2030年預測全球汽車機油市場規模(按等級、燃料類型、車輛類型、區域範圍和預測) 全球汽車機油市場:產業分析、規模、佔有率、成長、趨勢和預測(2025-2032 年)

全球汽車機油市場:產業分析、規模、佔有率、成長、趨勢和預測(2025-2032 年) 汽車機油市場規模、佔有率、成長分析、按等級、引擎類型、應用、地區 - 產業預測,2024-2031

汽車機油市場規模、佔有率、成長分析、按等級、引擎類型、應用、地區 - 產業預測,2024-2031 汽車用機油的全球市場的評估:各車輛類型,各產品類型,各引擎類型,各等級類型,各地區,機會,預測(2017年~2031年)

汽車用機油的全球市場的評估:各車輛類型,各產品類型,各引擎類型,各等級類型,各地區,機會,預測(2017年~2031年)