|

市場調查報告書

商品編碼

2035123

日本汽車機油:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Japan Automotive Engine Oils - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

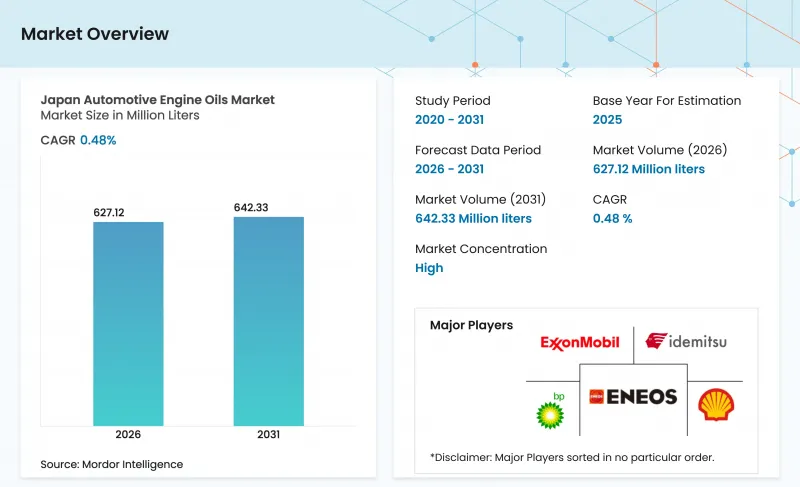

2025年日本汽車機油市場價值為6.2412億升,預計到2031年將達到6.4233億升,而2026年為6.2712億升,預測期(2026-2031年)複合年成長率為0.48%。

這種漸進式成長軌跡反映了車輛保有量的成熟、電氣化的快速發展以及產業加速向長效合成機油(更換頻率低)的轉變。隨著汽車製造商努力達到嚴格的企業平均燃油經濟性目標,超低黏度機油(0W-20及以下)約佔原廠加註機油的89%至95%。全國強制車輛年檢使得保養週期更加可預測,在一定程度上緩解了銷售量下滑。同時,由於全球混合動力汽車滲透率最高,與怠速熄火相容的合成機油也越來越受歡迎。由於原廠加註夥伴關係在經銷商網路中建立了長期的品牌忠誠度,因此OEM品牌潤滑油在換油需求中佔據主導地位。

日本汽車機油市場的趨勢與洞察

日益嚴格的 CAFE 等效燃油效率標準正在促進超低黏度潤滑油的採用。

日本的目標是到2030年實現平均車輛燃油經濟性達到25.4公里/公升,比2016年增加32%。實現這一目標的關鍵在於使用0W-16和0W-8配方,這些配方能夠在不影響抗磨損保護的前提下降低泵送損失。國土交通省和經濟產業省已製定企業平均合規框架,要求汽車製造商在其所有車型系列中指定使用減摩合成潤滑油。豐田和ENEOS共同推動了新的JASO GLV-2標準的實施,該標準能夠促進適用於電動動力系統的超高黏度指數潤滑油的開發。由於日本混合動力汽車的引擎在低溫下運作,因此保持觸媒轉換器的耐久性需要在潤滑油的化學成分中兼顧低溫流動性和足夠的高溫剪切穩定性。

混合動力汽車的日益普及,對能夠支援啟動停止功能的合成機油提出了更高的要求。

2019年,混合動力汽車佔日本新微型車銷量的18%,在主要經濟體中市佔率最高。車輛在其整個生命週期內,啟停循環次數可能超過50萬次,因此潤滑油膜的保持性和添加劑的耐久性至關重要。 ENEOS和出光興產公司已檢驗了一種新型III+基油混合物,即使在再生煞車導致的引擎停機過程中發生多次輕微氧化後,也能保持粘度。經銷商服務中心報告稱,標有「混合動力汽車認證」的SP級合成油需求不斷成長,這表明消費者願意支付更高的價格,以換取保固服務和燃油效率的提升。

電動車的普及將削弱對內燃機油的長期需求。

政府補貼、通行費減免以及公共充電網路的擴展,使得2024年電池式電動車(BEV)的註冊量比前一年增加了72%。純電動車(EV)無需使用引擎機油,而有效距離式混合動力汽車則可將油耗降低一半。日本石油協會預測,潤滑油產量將從2023年的260萬千公升下降到2030年的230萬千升,反映了汽油加工量的減少。因此,產業領導企業正在將多元化經營至電子流體、溫度控管冷卻劑以及氫燃料相關夥伴關係,以對沖收入風險。

細分市場分析

預計到2025年,乘用車引擎油(PCMO)銷量將佔日本汽車機油銷售量的63.12%,支撐著日本6,100萬輛乘用車的市場。幾乎所有新車型都指定使用0W-20或更低黏度的機油,同時,市場對能夠提高燃油效率且不影響保固的III類合成機油的需求也在不斷成長。此外,消費者對原廠配套品牌的高度忠誠度也支撐著這個細分市場,使其維持了穩定的高階定價結構。

2023年,機車機油市場複合年成長率(CAGR)達0.74%,成為成長最快的市場之一。這主要得益於摩托車註冊量增加至376,720輛,以及微型出行趨勢推動了擁擠都市區踏板車使用量的增加。 JASO MA2濕式離合器性能標準是高級產品的差異化優勢,而日本騎士對本土品牌的忠誠度也很高。重型車輛機油市場因電動物流的試營運以及政府對氫燃料電池卡車的支持而成長停滯,但建築和船舶等細分市場仍保持強勁勢頭。

《日本汽車機油市場報告》按產品類型(乘用車引擎油 (PCMO)、重負荷引擎油 (HDMO)、摩托車引擎油 (MCO))和基料(礦物油、合成油、半合成油、生物基油)進行細分。市場預測以體積(公升)為單位。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 更嚴格的燃油效率標準,相當於 CAFE 標準(促進向 0W-16/0W-8 過渡)

- 隨著混合動力汽車數量的增加,對能夠應對啟動停止功能的合成潤滑油的需求也日益成長。

- 強制性的“啟動”檢查確保定期更換機油。

- 我們透過與OEM製造商建立工廠灌裝合作關係來確保我們品牌潤滑油的銷售。

- 透過快速換油中心和電子商務通路擴大優質機油的供應。

- 市場限制因素

- 電動車的廣泛普及導致內燃機用油的長期需求下降。

- 優質合成油和礦物油之間的價格差距正在擴大。

- 延長換油週期的技術減少了每輛車的機油消耗量。

- 價值鍊和通路分析

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 產業間競爭

- 法律規範

- 汽車產業的發展趨勢

第5章 市場規模與成長預測

- 依樹脂類型

- 乘用車引擎機油(PCMO)

- 0W-XX

- 5W-XX

- 10W-XX

- 15W-XX

- 單黏度

- 其他年級

- 重型機油(HDMO)

- 0W-XX

- 5W-XX

- 10W-XX

- 15W-XX

- 單黏度

- 其他年級

- 摩托車機油(MCO)

- 0W-XX

- 5W-XX

- 10W-XX

- 15W-XX

- 單黏度

- 其他年級

- 乘用車引擎機油(PCMO)

- 基礎油

- 礦物油

- 合成

- 半複合材料

- 生物基

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- AKT Japan Co. Ltd(TAKUMI Motor Oil)

- BP plc

- Chevron Japan(Caltex Havoline)

- Cosmo Energy Holdings Co. td

- ENEOS Corporation

- Exxon Mobil Corporation

- FUCHS

- Honda Motor Co. Ltd(Honda Genuine Oil)

- Idemitsu Kosan Co. Ltd

- Japan Sun Oil Company Ltd(SUNOCO Inc.)

- Motul

- NAKAJIMA.BC Co.,Ltd.

- Saudi Arabian Oil Co.

- Shell plc

- Suzuki Motor Corporation

- Wako Chemical Co. Ltd

第7章 市場機會與未來展望

第8章:執行長面臨的關鍵策略挑戰

The Japan Automotive Engine Oils Market size was valued at 624.12 Million liters in 2025 and estimated to grow from 627.12 Million liters in 2026 to reach 642.33 Million liters by 2031, at a CAGR of 0.48% during the forecast period (2026-2031).

This modest trajectory reflects a mature vehicle parc, rapid electrification, and the industry's accelerating pivot toward extended-drain synthetic formulations. Ultra-low-viscosity oils (0W-20 and below) account for an estimated 89-95% of factory fills as OEMs chase stringent corporate average fuel-economy targets. Mandatory nationwide "Shaken" inspections create predictable service intervals that partly cushion volume erosion, while start-stop-ready synthetics gain traction alongside Japan's world-leading hybrid penetration. OEM-branded lubricants dominate replacement demand because factory-fill partnerships embed long-term brand loyalty inside dealer networks.

Japan Automotive Engine Oils Market Trends and Insights

Stricter CAFE-Equivalent Fuel-Economy Norms Drive Ultra-Low-Viscosity Adoption

Japan targets a fleet average of 25.4 km per liter by 2030, a 32% jump over 2016 levels. Achieving this goal hinges on 0W-16 and 0W-8 formulations that reduce pumping losses without sacrificing wear protection. The Ministry of Land, Infrastructure, and Transport and METI use a corporate-average compliance framework that pressures every OEM to spec friction-modified synthetics across model ranges. Toyota and ENEOS jointly advanced the new JASO GLV-2 standard, enabling ultra-high-viscosity-index oils suited to electrified drivetrains. As Japanese hybrids operate engines at lower temperatures, lubricant chemistries must balance very-low-temperature fluidity with adequate high-temperature shear stability to preserve catalytic-converter durability.

Hybrid-Fleet Expansion Demanding Start-Stop-Capable Synthetics

Hybrids captured 18% of Japan's new light-duty sales in 2019, the highest share among major economies. Start-stop events can exceed 500,000 cycles over a vehicle life, making film retention and additive robustness critical. ENEOS and Idemitsu validated new Group III+ basestock blends that retain viscosity after repeated micro-oxidation episodes during regenerative-braking shutdowns. Dealer workshops report rising demand for SP-rated synthetics labeled "Hybrid-Approved," indicating consumer acceptance of premium price points in exchange for warranty adherence and fuel-economy retention.

EV Penetration Eroding Long-Term ICE-Oil Demand

Government subsidies, toll exemptions, and a growing public-charging network lifted battery-electric registrations 72% year on year in 2024. Full EVs eliminate engine oil use, while range-extender hybrids halve consumption. The Petroleum Association of Japan projects lubricant production sliding to 2.3 million kiloliters by 2030, versus 2.6 million kiloliters in 2023, mirroring falling gasoline throughput. Industry leaders therefore diversify into e-fluids, thermal-management coolants and hydrogen fuel partnerships to hedge revenue risk.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory "Shaken" Inspections Sustaining Regular Oil-Change Volumes

- OEM Factory-Fill Partnerships Locking in Branded Oil Sales

- Wide Price Gap Between Premium Synthetics and Mineral Oils

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PCMO generated 63.12% of 2025 volume, underpinning the Japan automotive engine oil market through the country's 61 million-unit passenger-car fleet. Nearly all new car models specify 0W-20 or thinner, cementing demand for Group III synthetics that deliver fuel-economy gains without warranty risk. The segment also benefits from high loyalty to OEM-genuine labels, reinforcing stable premium pricing.

Motorcycle Engine Oil records the fastest 0.74% CAGR as two-wheel registrations rose to 376,720 units in 2023 and micro-mobility trends expand scooter use in crowded urban corridors. JASO MA2 specifications for wet-clutch performance differentiate premium offerings, and Japanese riders show strong brand affinity toward domestic suppliers. Heavy-duty motor oil faces stagnation because electrified logistics pilots and hydrogen fuel-cell trucks gain government support, though construction and marine niches provide resilience.

The Japan Automotive Engine Oil Report is Segmented by Product Type (Passenger Car Motor Oil (PCMO), Heavy Duty Motor Oil (HDMO), and Motorcycle Engine Oil (MCO)), Base Stock (Mineral, Synthetic, Semi-Synthetic, and Bio-Based). The Market Forecasts are Provided in Terms of Volume (Litres).

List of Companies Covered in this Report:

- AKT Japan Co. Ltd (TAKUMI Motor Oil)

- BP p.l.c.

- Chevron Japan (Caltex Havoline)

- Cosmo Energy Holdings Co. td

- ENEOS Corporation

- Exxon Mobil Corporation

- FUCHS

- Honda Motor Co. Ltd (Honda Genuine Oil)

- Idemitsu Kosan Co. Ltd

- Japan Sun Oil Company Ltd (SUNOCO Inc.)

- Motul

- NAKAJIMA.B.C Co.,Ltd.

- Saudi Arabian Oil Co.

- Shell plc

- Suzuki Motor Corporation

- Wako Chemical Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter CAFE-equivalent fuel-economy norms (0W-16/0W-8 push)

- 4.2.2 Hybrid-fleet expansion demanding start-stop-capable synthetics

- 4.2.3 Mandatory "Shaken" inspections sustaining regular oil-change volumes

- 4.2.4 OEM factory-fill partnerships locking in branded oil sales

- 4.2.5 Quick-lube and e-commerce channels widening premium-oil access

- 4.3 Market Restraints

- 4.3.1 EV penetration eroding long-term ICE-oil demand

- 4.3.2 Wide price gap between premium synthetics and mineral oils

- 4.3.3 Longer drain-interval technology lowering litres/vehicle

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Industry Rivalry

- 4.6 Regulatory Framework

- 4.7 Automotive Industry Trends

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Resin Type

- 5.1.1 Passenger Car Motor Oil (PCMO)

- 5.1.1.1 0W-XX

- 5.1.1.2 5W-XX

- 5.1.1.3 10W-XX

- 5.1.1.4 15W-XX

- 5.1.1.5 Monogrades

- 5.1.1.6 Other Grades

- 5.1.2 Heavy Duty Motor Oil (HDMO)

- 5.1.2.1 0W-XX

- 5.1.2.2 5W-XX

- 5.1.2.3 10W-XX

- 5.1.2.4 15W-XX

- 5.1.2.5 Monogrades

- 5.1.2.6 Other Grades

- 5.1.3 Motorcycle Engine Oil (MCO)

- 5.1.3.1 0W-XX

- 5.1.3.2 5W-XX

- 5.1.3.3 10W-XX

- 5.1.3.4 15W-XX

- 5.1.3.5 Monogrades

- 5.1.3.6 Other Grades

- 5.1.1 Passenger Car Motor Oil (PCMO)

- 5.2 By Base Stock

- 5.2.1 Mineral

- 5.2.2 Synthetic

- 5.2.3 Semi-Synthetic

- 5.2.4 Bio-Based

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Production Capacity, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AKT Japan Co. Ltd (TAKUMI Motor Oil)

- 6.4.2 BP p.l.c.

- 6.4.3 Chevron Japan (Caltex Havoline)

- 6.4.4 Cosmo Energy Holdings Co. td

- 6.4.5 ENEOS Corporation

- 6.4.6 Exxon Mobil Corporation

- 6.4.7 FUCHS

- 6.4.8 Honda Motor Co. Ltd (Honda Genuine Oil)

- 6.4.9 Idemitsu Kosan Co. Ltd

- 6.4.10 Japan Sun Oil Company Ltd (SUNOCO Inc.)

- 6.4.11 Motul

- 6.4.12 NAKAJIMA.B.C Co.,Ltd.

- 6.4.13 Saudi Arabian Oil Co.

- 6.4.14 Shell plc

- 6.4.15 Suzuki Motor Corporation

- 6.4.16 Wako Chemical Co. Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

8 Key Strategic Questions for CEOs

汽車機油市場:按產品類型、車輛類型、應用、最終用戶和分銷管道分類-2026-2032年全球市場預測

汽車機油市場:按產品類型、車輛類型、應用、最終用戶和分銷管道分類-2026-2032年全球市場預測 2026年全球汽車機油市場報告

2026年全球汽車機油市場報告 美國汽車引擎機油:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

美國汽車引擎機油:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 汽車機油市場:依產品類型、黏度等級、應用、銷售管道和地區分類

汽車機油市場:依產品類型、黏度等級、應用、銷售管道和地區分類 2026-2030年全球汽車機油市場

2026-2030年全球汽車機油市場 全球汽車機油市場:2025年至2030年預測全球汽車機油市場規模(按等級、燃料類型、車輛類型、區域範圍和預測)

全球汽車機油市場:2025年至2030年預測全球汽車機油市場規模(按等級、燃料類型、車輛類型、區域範圍和預測) 全球汽車機油市場:產業分析、規模、佔有率、成長、趨勢和預測(2025-2032 年)

全球汽車機油市場:產業分析、規模、佔有率、成長、趨勢和預測(2025-2032 年) 汽車機油市場規模、佔有率、成長分析、按等級、引擎類型、應用、地區 - 產業預測,2024-2031

汽車機油市場規模、佔有率、成長分析、按等級、引擎類型、應用、地區 - 產業預測,2024-2031 汽車用機油的全球市場的評估:各車輛類型,各產品類型,各引擎類型,各等級類型,各地區,機會,預測(2017年~2031年)

汽車用機油的全球市場的評估:各車輛類型,各產品類型,各引擎類型,各等級類型,各地區,機會,預測(2017年~2031年)