|

市場調查報告書

商品編碼

2043860

汽車物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Automotive Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

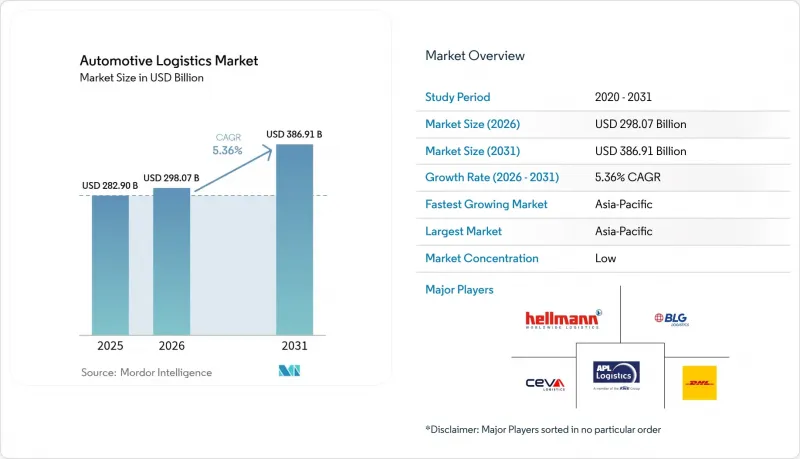

預計汽車物流市場將從 2025 年的 2,829 億美元成長到 2026 年的 2,980.7 億美元,然後從 2026 年到 2031 年以 5.36% 的複合年成長率成長,到 2031 年達到 3,869.1 億美元。

乘用車和商用車電氣化程度的不斷提高、售後市場履約的快速數位化以及交通行動服務的普及,正在擴大合約範圍,並增加物流供應商運輸的複雜性。隨著企業永續發展目標的日益嚴格,公路運輸向鐵路和海運的轉變正在加速,而全球第三方物流(3PL) 公司之間的併購正在創造規模經濟,重塑競爭格局。同時,隨著電子商務對當日達和隔日達的期望不斷提高,對微型倉配自動化的投資也在增加,整合的可視化平台對於確保長期汽車相關合約至關重要。

全球汽車物流市場趨勢及洞察

電池式電動車的加速普及將增加流通中的成品車數量。

預計到2025年,全球電動車(EV)滲透率將超過20%,這將推動對專業電池供應鏈和新型車輛運輸路線的需求。 DHL已在亞太地區和歐洲開設電動車卓越中心,提供溫控倉儲、危險品(DG)處理和多模態解決方案。馬士基的「電動車電池靈活物流」計畫透過使用可重複使用的貨櫃和先進的滅火系統,將倉庫面積減少一半,並將電池製造商的物流成本降低30%。由於中國持續佔全球70%的正極材料產量和85%的負極材料產量,歐美第三方物流公司正在投資中國運輸路線的運力,使得近岸緩衝庫存對歐美原始設備製造商(OEM)至關重要。鑑於電池處理設施的高資本密集度,運輸公司和能源公司正在組建合資企業,共同投資基礎設施建設。

售後零件電子商務的快速成長,使得消費者對當日達和隔日達服務抱有很高的期望。

如今,線上汽車零件銷售額已佔全球售後市場銷售額的兩位數佔有率,配送模式也正從區域配送中心轉向更靠近都市區車主的微型倉配中心。由一家大型汽車零件批發商實施的AutoStore系統,使其儲存密度提高了300%,運轉率達到99.6%,從而實現了3萬個SKU的訂單兩小時截止。起亞以色列的無硬體追蹤系統將車輛搜尋時間從數小時縮短至數分鐘,降低了50%的人事費用,並將處理時間縮短了高達40%。物流供應商正將預測性庫存管理工具與最後一公里配送網路結合,以確保長期合約的簽訂;郊區轉運中心則在夜間為農村路線補貨,以滿足週末的服務保障。

宏觀經濟的不確定性抑制了汽車的自願購買和交付。

受信貸緊縮和消費者信心疲軟的影響,預計2024年全球汽車產量將成長0.8%,而歐洲成品車港口吞吐量將下降9.4%。福特汽車正在墨西哥瓜伊馬斯港試點採用替代鐵路和短途海運路線,以在需求波動的情況下降低成本並維持前置作業時間。儘管滾裝碼頭的運轉率下降擠壓了利潤空間,但營運商必須確保剩餘運輸能力以應對經濟復甦,這將考驗其定價紀律。中國的電動車出口也使預測變得更加複雜,因為新品牌正在獨立於歐美宏觀經濟週期之外擴大生產。

細分市場分析

到2025年,運輸業將在全球汽車物流市場中保持58.34%的佔有率。陸路運輸仍將發揮核心作用,但隨著托運人尋求低碳運輸方式,鐵路和海運的運輸量正在成長。 BMW在德國國內線路營運的氫燃料卡車,透過減少從儲槽到車輪的排放,展現了運輸方式的創新。受客製化、軟體編程和交付前檢查等需求的驅動,附加價值服務預計將以6.94%的複合年成長率推動市場成長。供應商正在將現有倉庫改造為多客戶組裝中心,並引入機器人技術,從而在不增加傳統固定成本負擔的情況下,縮短專案推出週期。

自動化正在重塑倉儲經濟格局。 AutoStore 的「貨到人」系統將貨量利用率提高了三倍,將揀貨錯誤率降低到 0.1% 以下,並使售後訂單能夠在兩小時內完成。隨著原始設備製造商 (OEM) 向模組化電動車平台轉型,子組件的組裝和電池組的排序正在為服務專家創造新的利潤來源。因此,合約收入的重心正從長途運輸轉向高附加價值服務,這不僅使供應商的收入來源多元化,還有助於提高長期合約的續約率。

2025年,在複雜的零件接收流程和整車出口的推動下,OEM物流將佔全球汽車物流市場的72.55%。隨著電氣化的發展,對符合ADR標準的電池儲能設施、溫控拖車和緊急應變方案的資本投資正在增加。特斯拉與現代環球運輸公司簽訂的從上海到鹿特丹的Model 3長期包車協議,體現了新型跨洲電動車運輸路線的形成。

在汽車物流市場中,售後物流是成長最快的細分市場,複合年成長率達6.28%,這主要得益於車輛老化和零件直接面對消費者銷售的成長。 DHL收購Inmar Supply Chain後新增14個退貨中心,使其能更能滿足北美日益成長的逆向物流需求。拉丁美洲的平均車齡為18-20年,該地區對進口零件的需求不斷成長,吸引了第三方物流企業投資保稅自由貿易中心,以避開港口擁塞。

區域分析

預計到2025年,亞太地區將佔全球汽車物流市場的47.35%,並在2031年之前以6.55%的複合年成長率成長。中國在電動車生產和電池材料提煉領域的領先地位,使得該地區物流路線密度極高;而印度與生產連結獎勵計畫,則吸引了零件製造企業遷至該地區。 DHL於2025年在澳洲開設了電動車卓越中心,進一步拓展了其溫控電池運輸的區域網路。日本物流業者率先在高速公路上引入自動編隊行駛技術,以應對司機短缺問題並提高資產利用率。各大港口業者正在擴建滾裝泊位,其中高雄港37萬標準箱的擴建工程是縮短整車週轉時間的典型案例。

北美仍然是汽車物流市場的戰略樞紐,但進口汽車及零件關稅的不斷上漲正給運輸路線的選擇帶來壓力。分析師估計,如果關稅持續到2026年,汽車日運輸量可能減少2萬輛,迫使汽車製造商進一步尋求在墨西哥和加拿大進行近岸外包。喬治亞亞州港務局正投資2.62億美元維修科羅內爾斯島港,目標是到2026年將其打造成為美國領先的滾裝船港口。目前正在進行試點項目,在太平洋沿岸引入替代港口,例如瓜伊穆斯港,以緩解西海岸的擁塞狀況並平衡陸路運輸成本。

在汽車物流市場,歐洲面臨地緣政治動盪和嚴格的碳排放法規。預計到2024年,成品車碼頭吞吐量將下降9.4%,而亞洲電動車出口卻激增,該地區已成為淨進口地區。然而,歐盟在綠色物流方面主導。奧迪已引進可再生能源運作列車運輸電池模組,每年減少2600噸二氧化碳排放。皮爾港在希爾內斯建造的價值3000萬英鎊的滾裝船泊位(計劃於2025年運作)表明,儘管貨運量下降,但歐盟仍在持續投資。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 調查範圍

- 調查結果

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 當前市場狀況及汽車物流的價值提案

- 全球物流產業基準(LPI、貨運KPI)

- 汽車生產與銷售趨勢分析

- 電子商務對汽車物流的影響

- 逆向物流:挑戰與最佳實踐

- 市場促進因素

- 電池式電動車的加速普及正在增加全球流通成品車的數量。

- 售後零件電子商務的快速成長,提高了人們對當日達和隔日達的期望。

- 車輛訂閱和交通行動服務(MaaS) 的發展正在加速物流中車輛的更替。

- 消費者對端到端運輸可視性的需求正在推動平台驅動的第三方物流合約。

- 全球汽車平均車齡不斷上升,導致售後零件更換頻率越來越高。

- 企業永續發展目標正在推動運輸方式模式轉換鐵路和海運。

- 市場限制因素

- 宏觀經濟的不確定性抑制了自願購車和汽車出貨量。

- 貨運價格波動影響了卡車運輸商預算的可預測性。

- 嚴格的碳排放法規增加了長途車輛運輸的成本。

- 全球物流勞動力在需求高峰短缺,限制了運輸能力。

- 波特五力模型

- 買方的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

- 價值/供應鏈分析

- 行業法規和政策

- 技術展望(相容物聯網、RFID、ADAS)

- 地緣政治事件對市場的影響

第5章 市場規模與成長預測

- 按服務

- 運輸

- 路

- 鐵路

- 海上/滾裝船/海濱

- 航空

- 倉儲、物流和庫存管理

- 附加價值服務

- 運輸

- 按類型

- OEM

- 售後市場

- 貨物類型

- 已完成的汽車

- 汽車零件

- 電動汽車電池和電力電子

- 其他貨物

- 準時送達

- 標準

- 特快/緊急

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 秘魯

- 智利

- 阿根廷

- 南美洲其他地區

- 亞太地區

- 印度

- 中國

- 日本

- 澳洲

- 韓國

- 東南亞(新加坡、馬來西亞、泰國、印尼、越南、菲律賓)

- 亞太其他地區

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 比荷盧經濟聯盟(比利時、荷蘭、盧森堡)

- 北歐國家(丹麥、芬蘭、冰島、挪威、瑞典)

- 其他歐洲地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 策略性措施(併購、合資、擴大運輸能力)

- 市佔率分析

- 公司簡介

- DHL Group

- Kuehne+Nagel International AG

- CEVA Logistics

- DSV A/S

- Hellmann Worldwide Logistics SE & Co. KG

- BLG Logistics Group AG & Co. KG

- Kerry Logistics Network Ltd

- APL Logistics Ltd

- Ryder System Inc.

- Penske Logistics Inc.

- XPO Logistics Inc.

- Expeditors International

- TIBA Group

- CFR Rinkens

- NYK Line(Auto Logistics Division)

- SNCF Geodis

- Wallenius Wilhelmsen Logistics

- UPS Supply Chain Solutions

- Maersk Logistics & Services

- Nippon Express Holdings

- CJ Logistics*

第7章 市場機會與未來展望

The Automotive Logistics Market size is expected to grow from USD 282.90 billion in 2025 to USD 298.07 billion in 2026 and is forecast to reach USD 386.91 billion by 2031 at 5.36% CAGR over 2026-2031.

Continued electrification of passenger and commercial fleets, the rapid digitalization of aftermarket fulfillment, and the spread of mobility-as-a-service programs are expanding contract scope and shipment complexity for logistics providers. Modal shifts from road to rail and sea are accelerating as corporate sustainability targets tighten, while mergers among global 3PLs are creating scale advantages that reshape competitive dynamics. At the same time, same-day and next-day delivery expectations in e-commerce are pushing automation investments in micro-fulfillment, and integrated visibility platforms are becoming a prerequisite for winning long-term automotive contracts.

Global Automotive Logistics Market Trends and Insights

Acceleration of Battery-Electric Vehicle Adoption Raising Finished-Vehicle Flows

Global electric vehicle penetration is forecast to top 20% in 2025, driving demand for specialized battery supply chains and new finished-vehicle corridors. DHL has opened EV Centers of Excellence in Asia-Pacific and Europe, providing temperature-controlled storage, DG-compliant handling, and multimodal outbound solutions. Maersk's EV Battery Flex Flow program halves warehouse footprints by using reusable containers and advanced fire-suppression, cutting logistics costs by 30% for cell manufacturers. Western 3PLs are also investing in Chinese corridor capacity as the country maintains 70% cathode and 85% anode output, making near-shoring of buffer stocks crucial for European and North American OEMs. The capital intensity of battery handling depots is prompting joint ventures between carriers and energy firms to pool infrastructure spending.

E-commerce Boom in Aftermarket Parts Creating Same-Day/Next-Day Delivery Expectations

Online parts revenue now accounts for double-digit share of global aftermarket sales, prompting a shift from regional distribution centers to micro-fulfillment nodes closer to urban drivers. AutoStore deployments at leading spare-parts distributors raise storage density by 300% and deliver 99.6% uptime, enabling two-hour cut-off times for 30,000 SKU assortments. Kia Israel's hardware-less tracking reduced vehicle search time from hours to minutes, freeing 50% of labor and trimming processing time by up to 40%. Logistics providers now bundle predictive inventory tools with last-mile networks to secure long-term contracts, while suburban cross-docks replenish rural routes overnight to meet weekend service guarantees.

Macroeconomic Uncertainty Suppressing Discretionary Vehicle Purchases and Shipments

Global automotive output slowed to 0.8% growth in 2024 on tighter credit and weak consumer sentiment, reducing finished-vehicle port throughput by 9.4% in Europe. Ford is testing rail-short-sea alternatives from Mexico's Guaymas port to cut costs while maintaining lead-times under demand volatility. Lower utilization presses margins at ro-ro terminals, yet operators must retain surge capacity for recovery, straining pricing discipline. Chinese EV exports add forecasting complexity, as new brands scale output regardless of Western macrocycles.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Vehicle Subscription & Mobility-as-a-Service Increasing Fleet Turnover Logistics

- Consumer Demand for End-to-End Shipment Visibility Fostering Platform-Enabled 3PL Contracts

- Freight-Rate Volatility Eroding Budget Predictability for Automotive Shippers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation retained 58.34% share of the global automotive logistics market in 2025. Road haulage remains pivotal, yet rail and sea volumes are rising as shippers seek lower-carbon options. BMW's hydrogen trucks on German lanes lower tank-to-wheel emissions and illustrate modal innovation. Value-added services are forecast to outpace with a 6.94% CAGR, buoyed by customization, software flashing, and pre-delivery inspection demands. Providers are converting brown-field warehouses into multi-client assembly hubs that embed robotics, enabling shorter program launches without legacy overhead.

Automation reshapes storage economics: AutoStore's goods-to-person systems triple cubic utilization and cut pick errors below 0.1%, supporting two-hour aftermarket order windows. As OEMs migrate to modular EV platforms, sub-assembly kitting and battery-pack sequencing generate new margin pools for service specialists. The balance of contract revenue is therefore tilting from line-haul to high-touch add-ons, diversifying provider income and reinforcing sticky multiyear agreements.

OEM logistics accounted for 72.55% of the global automotive logistics market size in 2025, driven by complex inbound component flows and finished-vehicle exports. Electrification increases capital expenditure on ADR-compliant battery depots, temperature-controlled trailers, and emergency response protocols. Tesla's long-term charter with Hyundai Glovis to ship Model 3 from Shanghai to Rotterdam reflects new transcontinental EV corridors.

In the automotive logistics market, Aftermarket logistics is growing faster at 6.28% CAGR, underpinned by rising vehicle age and direct-to-consumer parts sales. DHL's purchase of Inmar Supply Chain adds 14 return centers, positioning the company to capture escalating reverse-logistics volumes in North America. Latin American fleets averaging 18-20 years heighten regional demand for import parts, attracting 3PL investment in bonded free-trade hubs that bypass port congestion.

The Automotive Logistics Market is Segmented by Service (Transportation, Warehousing, Distribution & Inventory Management and More), by Type (OEM and Aftermarket), by Cargo Type (Finished Vehicles, Auto Components, and More), by Delivery Time (Standard and Express / Critical), and by Geography (North America, South America, Asia-Pacific, Europe, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 47.35% share of the global automotive logistics market in 2025 and is forecast to grow at 6.55% CAGR to 2031. China's dominance in EV output and battery material refining sustains high intra-regional lane density, while India's production-linked incentives attract component manufacturing migrations. DHL added an EV Centre of Excellence in Australia in 2025, expanding its regional network for temperature-controlled battery flows. Japanese providers pioneer autonomous platooning on expressways, addressing driver shortages and lifting asset utilization. Major port operators are enlarging ro-ro berths, evidenced by Kaohsiung's 370,000-TEU expansion that boosts vessel turnaround for finished vehicles.

North America remains a strategic hub in the automotive logistics market, but tariff hikes on imported vehicles and components are pressuring routing decisions. Analysts estimate potential reductions of 20,000 units per day if tariffs hold through 2026, compelling OEMs to deepen Mexico and Canada near-shoring. Georgia Ports will invest USD 262 million to upgrade Colonel's Island, targeting top position in United States ro-ro throughput by 2026. Alternative Pacific gate entries such as Guaymas are under trial to limit west-coast congestion and balance drayage costs.

In the automotive logistics market, Europe grapples with geopolitical disruptions and stringent carbon regulation. Throughput at finished-vehicle terminals fell 9.4% in 2024, shifting the region to net-importer status as Asian EV exports surge. Yet the bloc leads in green logistics mandates: Audi deploys renewable-powered trains for battery modules, shaving 2,600 tonnes of annual CO2. Peel Ports' GBP 30 million ro-ro berth at Sheerness, operational in 2025, underscores continued investment despite softer volumes.

- DHL Group

- Kuehne + Nagel International AG

- CEVA Logistics

- DSV A/S

- Hellmann Worldwide Logistics SE & Co. KG

- BLG Logistics Group AG & Co. KG

- Kerry Logistics Network Ltd

- APL Logistics Ltd

- Ryder System Inc.

- Penske Logistics Inc.

- XPO Logistics Inc.

- Expeditors International

- TIBA Group

- CFR Rinkens

- NYK Line (Auto Logistics Division)

- SNCF Geodis

- Wallenius Wilhelmsen Logistics

- UPS Supply Chain Solutions

- Maersk Logistics & Services

- Nippon Express Holdings

- CJ Logistics*

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Scope of the Study

- 1.2 Study Deliverables

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Current Market Scenario & Automotive Logistics Value Proposition

- 4.2 Global Logistics Sector Benchmarking (LPI, Freight KPIs)

- 4.3 Automotive Production & Sales Trend Analysis

- 4.4 Impact of E-commerce on Automotive Logistics

- 4.5 Reverse Logistics: Challenges & Best Practices

- 4.6 Market Drivers

- 4.6.1 Acceleration of Battery-Electric Vehicle Adoption Raising Global Finished-Vehicle Flows

- 4.6.2 E-commerce Boom in Aftermarket Parts Creating Same-Day/Next-Day Delivery Expectations

- 4.6.3 Growth of Vehicle Subscription & Mobility-as-a-Service Increasing Fleet Turnover Logistics

- 4.6.4 Consumer Demand for End-to-End Shipment Visibility Fostering Platform-Enabled 3PL Contracts

- 4.6.5 Rising Global Average Vehicle Age Elevating Aftermarket Parts Replacement Frequency

- 4.6.6 Corporate Sustainability Targets Steering Modal Shift Toward Rail & Sea Transport

- 4.7 Market Restraints

- 4.7.1 Macroeconomic Uncertainty Suppressing Discretionary Vehicle Purchases and Shipments

- 4.7.2 Freight-Rate Volatility Eroding Budget Predictability for Automotive Shippers

- 4.7.3 Stringent Carbon-Emission Caps Increasing Cost of Long-Distance Vehicle Transport

- 4.7.4 Global Logistics Talent Shortage Constraining Capacity During Peak Demand Cycles

- 4.8 Porter's Five Forces

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

- 4.9 Value / Supply-Chain Analysis

- 4.10 Industry Regulations and Policies

- 4.11 Technological Outlook (IoT, RFID, ADAS Handling)

- 4.12 Impact of Geopolitical Events on the Market

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Service

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Rail

- 5.1.1.3 Sea / Ro-Ro / Short-Sea

- 5.1.1.4 Air

- 5.1.2 Warehousing, Distribution & Inventory Management

- 5.1.3 Value-Added Services

- 5.1.1 Transportation

- 5.2 By Type

- 5.2.1 OEM

- 5.2.2 Aftermarket

- 5.3 By Cargo Type

- 5.3.1 Finished Vehicles

- 5.3.2 Auto Components

- 5.3.3 EV Batteries & Power-Electronics

- 5.3.4 Other Cargo

- 5.4 By Delivery Time

- 5.4.1 Standard

- 5.4.2 Express / Critical

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Peru

- 5.5.2.3 Chile

- 5.5.2.4 Argentina

- 5.5.2.5 Rest of South America

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 Europe

- 5.5.4.1 United Kingdom

- 5.5.4.2 Germany

- 5.5.4.3 France

- 5.5.4.4 Spain

- 5.5.4.5 Italy

- 5.5.4.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.5.4.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.5.4.8 Rest of Europe

- 5.5.5 Middle East And Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East And Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Strategic Moves (M&A, JVs, Capacity Adds)

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 DHL Group

- 6.3.2 Kuehne + Nagel International AG

- 6.3.3 CEVA Logistics

- 6.3.4 DSV A/S

- 6.3.5 Hellmann Worldwide Logistics SE & Co. KG

- 6.3.6 BLG Logistics Group AG & Co. KG

- 6.3.7 Kerry Logistics Network Ltd

- 6.3.8 APL Logistics Ltd

- 6.3.9 Ryder System Inc.

- 6.3.10 Penske Logistics Inc.

- 6.3.11 XPO Logistics Inc.

- 6.3.12 Expeditors International

- 6.3.13 TIBA Group

- 6.3.14 CFR Rinkens

- 6.3.15 NYK Line (Auto Logistics Division)

- 6.3.16 SNCF Geodis

- 6.3.17 Wallenius Wilhelmsen Logistics

- 6.3.18 UPS Supply Chain Solutions

- 6.3.19 Maersk Logistics & Services

- 6.3.20 Nippon Express Holdings

- 6.3.21 CJ Logistics*

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

汽車物流市場:依運輸方式、服務類型、車輛類型和最終用戶分類-2026-2032年全球市場預測

汽車物流市場:依運輸方式、服務類型、車輛類型和最終用戶分類-2026-2032年全球市場預測 2026年全球汽車物流市場報告成品車物流市場:依運輸方式、服務類型、所有權類型、設備類型及最終用戶分類-2026-2032年全球市場預測

2026年全球汽車物流市場報告成品車物流市場:依運輸方式、服務類型、所有權類型、設備類型及最終用戶分類-2026-2032年全球市場預測 汽車物流市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測汽車OEM廠內物流市場:依零件、服務模式、自動化程度、物流方式、汽車零件類型及最終用戶分類-2026-2032年全球市場預測電動物流車輛馬達市場(按馬達類型、額定功率、車輛類型、應用和最終用戶產業分類)-全球預測,2026-2032年全球汽車物流市場規模、佔有率、趨勢和成長分析報告(2026-2034)

汽車物流市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測汽車OEM廠內物流市場:依零件、服務模式、自動化程度、物流方式、汽車零件類型及最終用戶分類-2026-2032年全球市場預測電動物流車輛馬達市場(按馬達類型、額定功率、車輛類型、應用和最終用戶產業分類)-全球預測,2026-2032年全球汽車物流市場規模、佔有率、趨勢和成長分析報告(2026-2034) 汽車物流市場規模、佔有率、趨勢及預測(按類型、活動、運輸方式、物流解決方案、分銷和地區分類),2026-2034年

汽車物流市場規模、佔有率、趨勢及預測(按類型、活動、運輸方式、物流解決方案、分銷和地區分類),2026-2034年 2026-2030年全球汽車OEM廠商廠內物流市場

2026-2030年全球汽車OEM廠商廠內物流市場 歐洲汽車物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

歐洲汽車物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)