|

市場調查報告書

商品編碼

2043834

北美智慧電錶:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)North America Smart Meters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

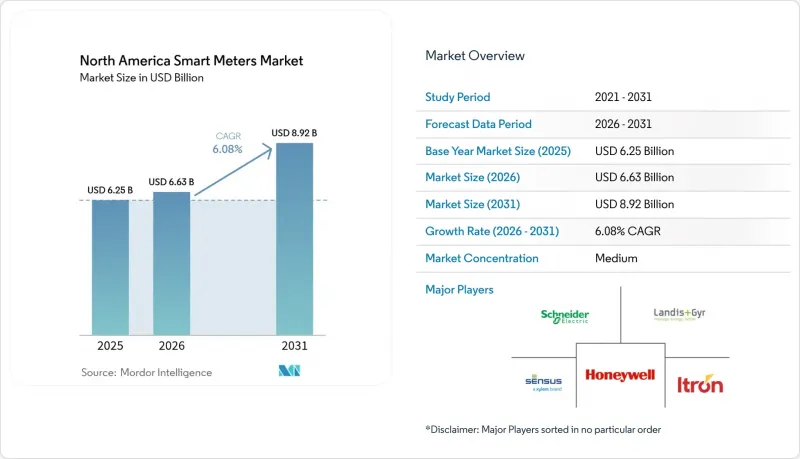

預計北美智慧電錶市場將從 2025 年的 62.5 億美元成長到 2026 年的 66.3 億美元,然後在 2031 年達到 89.2 億美元,2026 年至 2031 年的複合年成長率為 6.08%。

在輸配電基礎設施持續現代化、聯邦政府對高級計量基礎設施 (AMI) 的直接資助以及不斷擴大的能源效率要求的推動下,電力、水務和燃氣公用事業的升級浪潮持續高漲。智慧電錶普及率已超過 80%,下一個成長支柱將從第一階段部署轉向 AMI 2.0 的替換,後者融合了邊緣運算、電壓最佳化和分散式能源的雙向計量功能。即時、準確的計費、更短的現場回應時間和詳細的能耗數據(用於支援動態定價方案和客戶參與網站)的需求進一步推動了公共產業的需求。儘管自 2024 年底以來半導體供應鏈有所緩解,但組件採購風險仍然是阻礙因素,公共產業正透過簽訂多年期合約、增加供應商多元化和提高安全庫存來應對這些風險,從而保持北美智慧電錶市場的採購勢頭。

北美智慧電錶市場趨勢與洞察

全國推廣智慧電錶的監理義務

強制安裝法規已將高級計量技術從可選技術轉變為電網基礎設施的一部分。安大略省的一項早期指令將分時電價方案的採用率提升至90%,向北美各地的監管機構表明,價格改革和智慧電錶部署可以同步進行。加州國會第2572號法案對水務業施加了類似的壓力,強制要求所有家庭在2025年前安裝智慧水錶。紐約州參議院第S1550號法案增加了關於健康影響的報告要求,顯示在保持部署勢頭的同時,加強了監管。可預測的合規時間表增強了供應商擴大產能和簽訂多年合約的信心,以滿足北美智慧電錶市場的需求。

公共產業主導的輸配電網路現代化計劃

公共產業正在將進階計量基礎設施 (AMI) 整合到配電自動化、電壓調節器和停電管理方面的投資。美國能源局的智慧電網投資津貼已資助了 99 個項目,總額達 80 億美元,這些項目將高級電錶作為現代電網的感測器基礎設施。光是新墨西哥州公共產業公司就在其 3.44 億美元的現代化藍圖中撥款 1.88 億美元用於電錶升級。許多公司現在選擇具有更高處理能力和內存的 AMI 2.0 終端。這使得板載分析能夠即時檢測電壓異常和來自分散式能源 (DER) 的反向電力傳輸,從而提高電網可視性,同時為分析軟體供應商創造新的商機。

電錶和安裝的初始成本較高。

智慧電錶的成本是傳統類比電錶的五到七倍,其中包括現場人工、通訊模組和後勤部門整合成本。聖荷西水務公司斥資1億美元安裝了23萬台智慧電錶,平均每台成本約435美元。卑詩水電公司在全省範圍內推廣智慧電錶的項目需要20億加元(15億美元),但預計到2033年,其淨現值將達到5.2億加元(3.9億美元)。雖然電價調整程序通常允許透過提高電價來收回成本,但藉貸能力有限的小規模合作社可能會將部署週期延長至八到十年,導致北美智慧電錶市場短期安裝量有限,且需求波動不定。

細分市場分析

至2025年,電錶將佔北美智慧電錶銷售額的79.60%,凸顯其在北美智慧電錶市場的核心地位。美國強制實施的更換計畫和已部署的1.11億個終端確保了AMI 2.0系統的穩定更新週期。電力公司高度重視電壓分析、停電偵測和服務中斷功能,這些功能有助於挽回因竊電造成的損失並降低運維成本。

預計到2025年,水錶銷售額僅佔總銷售額的13.10%,但其複合年成長率高達7.20%,超過了其他所有設備類別。節水法規、減少漏損目標以及州政府資助的抗旱救災計畫是推動水錶市場成長的主要因素。例如,舊金山等公共產業在5,600萬美元的預算下部署了18萬台水錶。美國水務公司(American Water)已完成超過100萬台水錶的安裝,並報告漏損持續時間減少了38%,無收益水量也實現了兩位數的下降。

剩餘的市場佔有率由燃氣表佔據。燃氣表數量的逐步成長得益於安全法規的推動,這些法規強制要求遠端關閉和甲烷洩漏檢測。一些公共產業正在將電力、燃氣和水錶的安裝捆綁在一起,以最大限度地提高現場施工效率,這種做法進一步擴大了北美智慧電錶市場的整體潛在市場規模。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 全國推廣智慧電錶的監理義務

- 電力公司主導的輸電網現代化計劃

- 聯邦和州政府為基礎建設提供資金

- 即時消費數據和準確計費的需求

- 用於整合分散式能源資源的雙向測量

- 乾旱應對措施中的分時供水事業

- 市場限制因素

- 儀表和安裝的初始成本較高。

- 網路安全和資料隱私問題

- 半導體供應鏈的波動性

- 社區對射頻輻射危害健康的擔憂出現強烈反彈

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 按類型

- 電錶

- 水錶

- 燃氣表

- 透過通訊技術

- 射頻網狀網路

- 電力線路通訊(PLC)

- 細胞

- 其他短程通訊(Wi-Fi、Zigbee、BLE)

- 最終用戶

- 住宅

- 商業的

- 工業的

- 按地區

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略性舉措(併購、合作、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Landis+Gyr

- Itron

- Xylem(Sensus)

- Schneider Electric

- Honeywell International

- Siemens AG

- ABB Ltd

- Aclara(Hubbell)

- Kamstrup

- Badger Meter

- Neptune Technology Group

- EDMI

- Holley Technology

- Elster Group

- Silver Spring Networks(Itron)

- Trilliant

- Sagemcom

- Iskraemeco

- Hexing Electric

- EKM Metering

第7章 市場機會與未來展望

The North America Smart Meters Market size is expected to grow from USD 6.25 billion in 2025 to USD 6.63 billion in 2026 and is forecast to reach USD 8.92 billion by 2031 at 6.08% CAGR over 2026-2031.

Continued modernization of transmission and distribution assets, direct federal appropriations for advanced metering infrastructure, and widening conservation mandates keep the upgrade wave intact across electric, water, and gas utilities. Smart meter penetration has already surpassed 80%, so the next growth leg pivots from first-wave roll-outs to AMI 2.0 replacements that embed edge computing, voltage optimization, and bidirectional measurement of distributed energy resources. Utility demand is further buoyed by real-time billing accuracy, shrinking truck rolls, and the need for granular consumption data that underpins dynamic pricing programs and customer engagement portals. Semiconductor supply-chain pressures have moderated since late 2024, yet component risk remains a gating factor that utilities manage through multi-year procurement contracts, strengthened vendor diversification, and higher safety inventories, sustaining purchasing momentum in the North America Smart Meters market.

North America Smart Meters Market Trends and Insights

Regulatory Mandates for Nationwide Smart-Electric Meter Roll-outs

Obligatory installation rules have transformed advanced metering from a discretionary technology into grid infrastructure. Ontario's early directive, which has driven 90% time-of-use rate adoption, showed regulators across North America how tariff reform and smart-meter penetration can move in lockstep. California's Assembly Bill 2572 applies parallel pressure in the water sector by requiring smart water meters at every home by 2025. New York's Senate Bill S1550 adds a health-impact reporting layer, signaling expanded oversight while still keeping deployment engines running. Predictable compliance timelines give suppliers confidence to scale production capacity, locking in multi-year contracts that sustain volume for the North America Smart Meters market.

Utility-led Grid-Modernization Programs

Utilities are bundling AMI with distribution automation, voltage control, and outage management investments. The U.S. Department of Energy's Smart Grid Investment Grant funded 99 projects valued at USD 8 billion, embedding advanced meters as the sensor backbone of modern grids. Public Service Company of New Mexico alone earmarked USD 188 million for meter upgrades inside a broader USD 344 million modernization road map. Most firms now specify AMI 2.0 endpoints with extra processing power and memory, enabling on-board analytics that detect voltage anomalies and DER back-feed in real time, thus improving grid visibility while creating incremental revenue opportunities for analytics software providers.

High Upfront Meter & Installation Costs

Smart meters cost five to seven times more than legacy analog devices once field labor, communications modules, and back-office integration are included. San Jose Water's USD 100 million outlay for 230,000 units equates to roughly USD 435 per endpoint. BC Hydro's province-wide program required CAD 2 billion (USD 1.5 billion) but promises CAD 520 million (USD 390 million) in net present value by 2033. Rate cases often allow recovery through tariff adders, yet smaller cooperatives with limited borrowing power sometimes stretch deployments over eight to ten years, dampening near-term installation volumes and injecting episodic demand variance into the North America Smart Meters market.

Other drivers and restraints analyzed in the detailed report include:

- Federal and State Funding for Infrastructure Upgrades

- Demand for Real-time Consumption Data & Accurate Billing

- Cyber-security and Data-privacy Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electricity meters generated 79.60% of 2025 revenue, underscoring their anchor role in the North America Smart Meters market. Mandatory replacement schedules and 111 million deployed endpoints across the United States ensure a steady AMI 2.0 refresh cycle. Utilities value voltage analytics, outage detection, and service disconnection features that help recoup theft losses and reduce O&M spending.

Water meters, though only 13.10% of 2025 revenue, are outpacing every other device category at a 7.20% CAGR. Conservation mandates, leak-reduction targets, and state-funded drought resilience programs drive growth, with utilities like San Francisco rolling out 180,000 units under a USD 56 million budget. American Water has already surpassed 1 million installations, reporting 38% leak-duration reductions and a double-digit cut in non-revenue water.

Gas meters comprise the remaining share. Their modest unit growth is buoyed by safety regulations that mandate remote shut-off and methane-leak detection. Several utilities bundle electric, gas, and water installations to maximize truck-roll efficiency, a practice that further increases total addressable volume for the North America Smart Meters market.

The North America Smart Meters Market Report is Segmented by Type (Electricity Meters, Water Meters, and Gas Meters), Communication Technology (RF Mesh, Power-Line Communication, Cellular, and Other Short-Range), End-User (Residential, Commercial, and Industrial), and Geography (United States, Canada, and Mexico). The Market Size and Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Landis+Gyr

- Itron

- Xylem (Sensus)

- Schneider Electric

- Honeywell International

- Siemens AG

- ABB Ltd

- Aclara (Hubbell)

- Kamstrup

- Badger Meter

- Neptune Technology Group

- EDMI

- Holley Technology

- Elster Group

- Silver Spring Networks (Itron)

- Trilliant

- Sagemcom

- Iskraemeco

- Hexing Electric

- EKM Metering

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory mandates for nationwide smart-electric meter roll-outs

- 4.2.2 Utility-led grid-modernization programs

- 4.2.3 Federal and state funding for infrastructure upgrades

- 4.2.4 Demand for real-time consumption data & accurate billing

- 4.2.5 Bi-directional metering to integrate distributed energy resources

- 4.2.6 Water-utility time-of-use tariffs amid drought management

- 4.3 Market Restraints

- 4.3.1 High upfront meter & installation costs

- 4.3.2 Cyber-security and data-privacy concerns

- 4.3.3 Semiconductor supply-chain volatility

- 4.3.4 Local pushback over RF-emission health fears

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products & Services

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Electricity Meters

- 5.1.2 Water Meters

- 5.1.3 Gas Meters

- 5.2 By Communication Technology

- 5.2.1 RF Mesh

- 5.2.2 Power-Line Communication (PLC)

- 5.2.3 Cellular

- 5.2.4 Other Short-Range (Wi-Fi, Zigbee, BLE)

- 5.3 By End-User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.4 By Geography

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Landis+Gyr

- 6.4.2 Itron

- 6.4.3 Xylem (Sensus)

- 6.4.4 Schneider Electric

- 6.4.5 Honeywell International

- 6.4.6 Siemens AG

- 6.4.7 ABB Ltd

- 6.4.8 Aclara (Hubbell)

- 6.4.9 Kamstrup

- 6.4.10 Badger Meter

- 6.4.11 Neptune Technology Group

- 6.4.12 EDMI

- 6.4.13 Holley Technology

- 6.4.14 Elster Group

- 6.4.15 Silver Spring Networks (Itron)

- 6.4.16 Trilliant

- 6.4.17 Sagemcom

- 6.4.18 Iskraemeco

- 6.4.19 Hexing Electric

- 6.4.20 EKM Metering

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

智慧電錶:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

智慧電錶:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 智慧電錶市場規模、佔有率和趨勢分析報告:按組件、類型、技術、最終用途、地區和細分市場分類(2026-2033 年)

智慧電錶市場規模、佔有率和趨勢分析報告:按組件、類型、技術、最終用途、地區和細分市場分類(2026-2033 年) 智慧電錶市場預測——全球產品、組件、通訊技術、技術、應用、最終用戶和地區分析——2034年

智慧電錶市場預測——全球產品、組件、通訊技術、技術、應用、最終用戶和地區分析——2034年 智慧電錶市場:按類型、通訊技術、技術、組件、階段、應用、最終用途、部署模式和客戶類型分類-2026-2032年全球市場預測

智慧電錶市場:按類型、通訊技術、技術、組件、階段、應用、最終用途、部署模式和客戶類型分類-2026-2032年全球市場預測 物聯網市場追蹤調查:計量

物聯網市場追蹤調查:計量 2026年全球智慧電錶市場報告多功能智慧電錶市場(按最終用戶、應用、通訊技術、相型、部署模式和安裝類型分類),全球預測,2026-2032年歐洲智慧電錶:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)美國智慧電錶:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)全球電網現代化投資市場:預測(至2034年)-按輸電基礎設施、組件、資金來源、電網類型、技術、應用、最終用戶和地區進行分析

2026年全球智慧電錶市場報告多功能智慧電錶市場(按最終用戶、應用、通訊技術、相型、部署模式和安裝類型分類),全球預測,2026-2032年歐洲智慧電錶:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)美國智慧電錶:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)全球電網現代化投資市場:預測(至2034年)-按輸電基礎設施、組件、資金來源、電網類型、技術、應用、最終用戶和地區進行分析