|

市場調查報告書

商品編碼

1940894

西班牙醫藥物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Spain Pharmaceutical Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

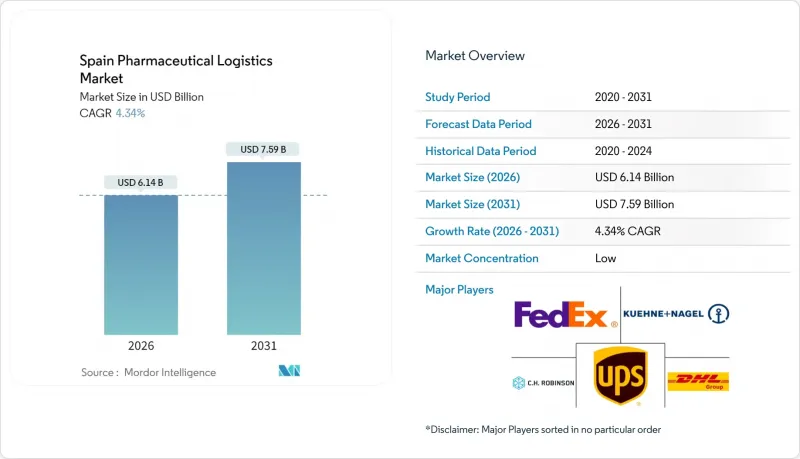

預計到 2026 年,西班牙醫藥物流市場規模將達到 61.4 億美元。

預計該產業規模將從 2025 年的 58.8 億美元成長到 2031 年的 75.9 億美元,2026 年至 2031 年的複合年成長率為 4.34%。

西班牙強大的公路、港口和機場基礎設施使其成為通往南歐的門戶,縮短了對溫度敏感的藥品的前置作業時間,並推動了對端到端可視性工具的需求。沿著地中海和大西洋走廊分佈的物流園區加速了跨境藥品流向法國和義大利的進程,鑑於80%的歐洲藥品需要溫控,這一點至關重要。有關GDP認證的監管改革強化了品質標準,並有利於擁有自動化監控系統的營運商。隨著全球領導企業向西班牙物流能力投資數十億歐元,競爭日益激烈,加速了技術應用並推動了產業整合。

西班牙醫藥物流市場趨勢與洞察

國內藥品銷售量增加

西班牙國內藥品銷售額超過230億歐元(250億美元),支撐著超過26萬個就業崗位,並為物流業成長奠定了堅實的基礎。 1,340億歐元(1,430億美元)的公共醫療支出為西班牙藥品物流市場創造了穩定的需求。人均藥品支出477歐元(510美元),高於歐洲平均水平,進一步鞏固了銷售量的穩定性。然而,2024年藥品短缺率激增41%,影響到4983種產品,暴露了補貨週期中的脆弱性。 2024年1月,947種產品缺貨,凸顯了預測性庫存管理工具的必要性,以減少對醫療服務造成的連鎖干擾。

人口老化和慢性病發病率上升將推動最後一公里配送需求。

長期人口預測顯示,到2074年,65歲及以上人口的比例將大幅增加。慢性病發生率的上升正促使處方藥的配送模式轉向定時送處方箋上門,這增加了西班牙藥品物流市場「最後一公里」配送的複雜性。數位健康平台整合了遠端醫療和藥房網路,對心血管和糖尿病藥物的定時配送提出了更高的要求。主導的學名藥的興起,在提高藥品可負擔性的同時也提高了配送頻率。 PharmaMar的個人化癌症治療方法需要針對特定病患、可追溯的低溫運輸運輸,從醫院藥局一直延伸到居家醫療機構。

司機短缺和勞動成本飆升

低溫運輸業者佔伊比利半島食品GDP的2.5%,但嚴重的司機短缺導致人事費用飆升。 DHL已推出一項20億歐元(約20.8億美元)的醫療保健物流計劃,優先推進自動化,以應對勞動力短缺問題。 UPS的目標是到2026年將其醫療保健收入加倍,達到200億美元,並致力於透過機器人技術和配送路線最佳化軟體來提高生產力。儘管有資金注入,即時短缺的現狀限制了運力,而此時流感疫苗的需求正處於高峰期,這阻礙了西班牙醫藥物流市場的擴張。

細分市場分析

截至2025年,運輸業佔西班牙醫藥物流市場的59.30%。這主要得益於連接巴塞隆納、瓦倫西亞和阿爾赫西拉斯港口的15,825公里高速公路網。這項核心基礎設施透過Logista和DHL營運的網路,將藥品分銷至歐洲20萬個銷售點。儘管道路運輸憑藉其次日達能力仍是主要運輸方式,但空運(經由赫羅納和薩拉戈薩機場)也在不斷擴張,以滿足生物製藥的迫切需求。為實現排放目標,托運人正擴大轉向海鐵聯運走廊;據西班牙生物製品協會(SEBA)稱,冷藏海運航線可減少70%的排放。預計到2031年,附加價值服務和其他細分市場將以4.66%的複合年成長率成長,因為GDP文件、配套包裝和後期客製化將成為標準合約條款。 FedEx 於 2025 年獲得 CEIV 製藥企業認證,並贏得價值 4 億美元的醫療保健契約,這完美地詮釋了合規卓越如何帶來商業性成果。

隨著西班牙醫院擴大外包業務,西班牙醫藥物流市場的附加價值服務和其他細分領域預計將會成長。運輸方式正轉向配備物聯網感測器的溫控貨櫃,這些貨櫃產生的資料流可透過預測路線檢驗服務來實現貨幣化。 UPS整合Frigo-Trans和BPL後,擴大了其在歐洲2-8°C的運輸覆蓋範圍,為西班牙醫藥出口商提供涵蓋陸運、海運和空運的單一發票解決方案。永續性也是推動因素之一,CEVA旗下FORPLANET品牌的電動卡車服務於馬德里的診所,預計到2024年將減少2.6萬噸的排放。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 國內藥品銷售量增加

- 人口老化和慢性病發病率上升將推動最後一公里配送需求。

- 生物製藥和溫度敏感療法的擴張

- 歐盟假藥指令序列化截止日期生效

- RRF支援的低溫運輸基礎設施投資

- 醫院網路向外包供應模式轉型

- 市場限制

- 促進要素短缺和勞動成本上升

- 在極端氣候變化期間確保端到端的溫度控制

- 冷庫房地產所有權結構分散

- 能源成本上漲正在影響冷藏倉庫的利潤率。

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 地緣政治和疫情對市場的影響

第5章 市場規模與成長預測

- 按服務類型

- 運輸

- 公路貨運

- 空運

- 海上運輸

- 鐵路貨運

- 倉儲

- 附加價值服務及更多

- 運輸

- 按操作模式

- 低溫運輸物流

- 非低溫運輸物流

- 依產品類型

- 處方藥

- 非處方藥

- 生物製藥和生物相似藥

- 疫苗和血液製品

- 臨床試驗材料

- 細胞和基因治療

- 醫療設備與診斷

- 動物用藥品

- 其他

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- DHL Supply Chain Spain

- FedEx Express

- Kuehne+Nagel SA

- United Parcel Service(UPS)

- CH Robinson

- CEVA Logistics

- DSV

- Movianto

- Eurotranspharma

- Primafrio

- Cencora

- Yusen Logistics(Part of NYK Line)

- Scan Global Logistics

- Rhenus Logistics

- Geodis

- TIBA

- Logista Pharma

- Noatum Logistics

- Ibercondor

- Logisber

第7章 市場機會與未來展望

The Spain Pharmaceutical Logistics Market size in 2026 is estimated at USD 6.14 billion, growing from 2025 value of USD 5.88 billion with 2031 projections showing USD 7.59 billion, growing at 4.34% CAGR over 2026-2031.

Robust motorway, port, and airport capacity positions Spain as a Southern European gateway that reduces lead times for temperature-sensitive medicines and heightens demand for end-to-end visibility tools. Logistic parks clustered along the Mediterranean and Atlantic corridors speed cross-border flows into France and Italy, which is critical as 80% of European medicines now require temperature control. Regulatory reforms around GDP certification tighten quality thresholds and reward operators with automated monitoring systems. Competitive intensity is rising because global leaders are injecting billions into Spanish capacity, accelerating technology adoption, and sparking consolidation.

Spain Pharmaceutical Logistics Market Trends and Insights

Rising Domestic Pharmaceutical Sales Volume

Annual domestic drug revenue exceeds EUR 23 billion (USD 25 billion) and supports more than 260,000 jobs, which strengthens the baseline for logistics growth. Public health spending at EUR 134 billion (USD 143 billion) creates dependable demand across the Spanish pharmaceutical logistics market. Per-capita medicine outlays at EUR 477 (USD 510) surpass European averages, reinforcing volume stability. Yet drug shortages jumped 41% in 2024, with 4,983 items affected, exposing vulnerabilities in replenishment cycles. January 2024 recorded 947 unavailable products, underscoring the need for predictive inventory tools that reduce cascading care disruptions.

Ageing Population & Chronic Disease Burden Intensifying Last-Mile Demand

Long-term demographic projections show a sharply rising proportion of citizens older than 65 by 2074. Chronic illnesses shift dispensing patterns toward repeat prescriptions delivered to patients' homes, which magnifies last-mile complexity within Spain pharmaceutical logistics market. Digital health platforms integrate telemedicine with pharmacy networks and require timed deliveries of cardiovascular and diabetes drugs. Generic penetration led by Kern Pharma and Teva supports affordability but raises shipment frequency. Personalized oncology regimens from PharmaMar demand traceable, patient-specific cold-chain movements that extend beyond hospital pharmacies into home-care settings.

Driver Shortage & Escalating Labour Costs

Cold-chain operators represent 2.5% of Iberian food GDP and face acute driver shortages that inflate wage bills. DHL answered with a EUR 2 billion (USD 2.08 billion) health-logistics program that prioritizes automation to counter labor gaps. UPS seeks to double healthcare revenue to USD 20 billion by 2026, banking on robotics and routing software to lift productivity. Despite capital injections, immediate driver scarcity restricts capacity during influenza vaccine peaks, restraining Spain pharmaceutical logistics market expansion.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Biologics & Temperature-Sensitive Therapies

- EU Falsified Medicines Directive Serialization Deadline Enforcement

- Rising Energy Costs Impacting Refrigerated-Warehouse Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation captured 59.30% of Spain pharmaceutical logistics market share in 2025, propelled by 15,825 km of motorways connecting ports at Barcelona, Valencia, and Algeciras. This backbone delivers medicines to 200,000 European points of sale through networks managed by Logista and DHL. Road haulage remains the preferred mode for its overnight reach, but airfreight is scaling via Girona and Zaragoza airports to meet urgent biologic demand. Sea and rail corridors increasingly attract shippers pursuing carbon-reduction targets, with CEVA citing 70% lower emissions for refrigerated sea lanes. Value-added services & others are expected to post a 4.66% CAGR to 2031 as GDP documentation, kitting, and late-stage customization become standard contract inclusions. FedEx secured a CEIV Pharma Corporate Certificate in 2025 and won USD 400 million in healthcare contracts, illustrating the commercial payoff from compliance excellence.

Spain pharmaceutical logistics market size for value-added services & others is forecast to rise, aligned with expanding outsourcing by Spanish hospitals. The modal mix will tilt toward temperature-controlled containers that embed IoT sensors, creating data streams monetized through predictive lane validation services. UPS's integration of Frigo-Trans and BPL widens its European 2-8 °C footprint and offers Spanish pharma exporters a single invoice solution spanning road, sea and air. Sustainability is another driver, with electric trucks now servicing inner-city clinics in Madrid under CEVA's FORPLANET label, reducing emissions by 26,000 tons in 2024.

The Spain Pharmaceutical Logistics Market Report is Segmented by Service Type (Transportation, Warehousing & Storage, and Value-Added Services & Others), Mode of Operation (Cold-Chain Logistics and Non-Cold-Chain Logistics), Product Type (Prescription Drugs, OTC Drugs, Biologics & Biosimilars, Vaccines & Blood Products, Cell & Gene Therapies, Veterinary Medicine, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- DHL Supply Chain Spain

- FedEx Express

- Kuehne + Nagel S.A.

- United Parcel Service (UPS)

- C.H. Robinson

- CEVA Logistics

- DSV

- Movianto

- Eurotranspharma

- Primafrio

- Cencora

- Yusen Logistics (Part of NYK Line)

- Scan Global Logistics

- Rhenus Logistics

- Geodis

- TIBA

- Logista Pharma

- Noatum Logistics

- Ibercondor

- Logisber

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising domestic pharmaceutical sales volume

- 4.2.2 Ageing population & chronic disease burden intensifying last-mile demand

- 4.2.3 Expansion of biologics & temperature-sensitive therapies

- 4.2.4 EU Falsified Medicines Directive serialization deadline enforcement

- 4.2.5 RRF-backed cold-chain infrastructure investments

- 4.2.6 Hospital network shift toward outsourced supply models

- 4.3 Market Restraints

- 4.3.1 Driver shortage & escalating labour costs

- 4.3.2 Ensuring end-to-end temperature integrity amid climate extremes

- 4.3.3 Fragmented cold-storage real-estate ownership

- 4.3.4 Rising energy costs impacting refrigerated-warehouse margins

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Geopolitics & Pandemic on the Market

5 Market Size & Growth Forecasts (Value)

- 5.1 By Service Type

- 5.1.1 Transportation

- 5.1.1.1 Road Freight

- 5.1.1.2 Air Freight

- 5.1.1.3 Sea Freight

- 5.1.1.4 Rail Freight

- 5.1.2 Warehousing & Storage

- 5.1.3 Value-added Services and Others

- 5.1.1 Transportation

- 5.2 By Mode of Operation

- 5.2.1 Cold-Chain Logistics

- 5.2.2 Non-Cold-Chain Logistics

- 5.3 By Product Type

- 5.3.1 Prescription Drugs

- 5.3.2 OTC Drugs

- 5.3.3 Biologics & Biosimilars

- 5.3.4 Vaccines & Blood Products

- 5.3.5 Clinical Trail Materials

- 5.3.6 Cell & Gene Therapies

- 5.3.7 Medical Devices & Diagnostics

- 5.3.8 Veterinary Medicine

- 5.3.9 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 DHL Supply Chain Spain

- 6.4.2 FedEx Express

- 6.4.3 Kuehne + Nagel S.A.

- 6.4.4 United Parcel Service (UPS)

- 6.4.5 C.H. Robinson

- 6.4.6 CEVA Logistics

- 6.4.7 DSV

- 6.4.8 Movianto

- 6.4.9 Eurotranspharma

- 6.4.10 Primafrio

- 6.4.11 Cencora

- 6.4.12 Yusen Logistics (Part of NYK Line)

- 6.4.13 Scan Global Logistics

- 6.4.14 Rhenus Logistics

- 6.4.15 Geodis

- 6.4.16 TIBA

- 6.4.17 Logista Pharma

- 6.4.18 Noatum Logistics

- 6.4.19 Ibercondor

- 6.4.20 Logisber

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

生物製藥物流市場-全球產業規模、佔有率、趨勢、機會、預測:按服務、營運類型、地區和競爭格局分類,2021-2031年

生物製藥物流市場-全球產業規模、佔有率、趨勢、機會、預測:按服務、營運類型、地區和競爭格局分類,2021-2031年 醫藥物流市場規模、佔有率及成長分析:依運輸方式、服務類型、物流類型、產品類型、最終用戶、應用及地區分類-2026-2033年產業預測

醫藥物流市場規模、佔有率及成長分析:依運輸方式、服務類型、物流類型、產品類型、最終用戶、應用及地區分類-2026-2033年產業預測 醫藥物流市場:按類型、產品類型、組件、運輸方式和最終用戶分類-2026-2032年全球市場預測生物製藥物流市場:依產品類型、服務類型、運輸方式、溫度需求及最終用戶分類-2026-2032年全球市場預測

醫藥物流市場:按類型、產品類型、組件、運輸方式和最終用戶分類-2026-2032年全球市場預測生物製藥物流市場:依產品類型、服務類型、運輸方式、溫度需求及最終用戶分類-2026-2032年全球市場預測 生物製藥物流市場:按類型、服務類型、應用和地區分類

生物製藥物流市場:按類型、服務類型、應用和地區分類 2026年全球生物製藥物流市場報告

2026年全球生物製藥物流市場報告 全球醫藥物流市場規模、佔有率、趨勢及成長分析報告(2026-2034)全球生物製藥物流市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球醫藥物流市場規模、佔有率、趨勢及成長分析報告(2026-2034)全球生物製藥物流市場規模、佔有率、趨勢和成長分析報告(2026-2034) 美國醫學流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)醫藥物流市場規模、佔有率、成長及全球產業分析:按類型、應用和地區洞察,2026-2034年預測

美國醫學流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)醫藥物流市場規模、佔有率、成長及全球產業分析:按類型、應用和地區洞察,2026-2034年預測