|

市場調查報告書

商品編碼

1940893

非洲二手車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)Africa Used Car - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

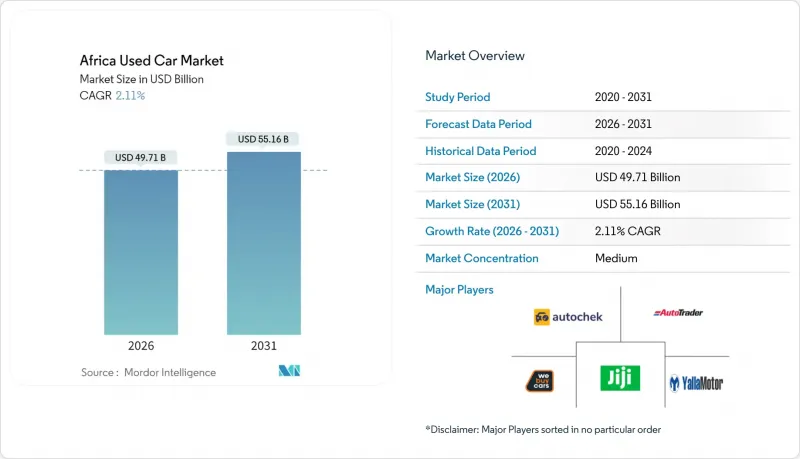

預計非洲二手車市場規模將從 2025 年的 486.8 億美元成長到 2026 年的 497.1 億美元,到 2031 年將達到 551.6 億美元,2026 年至 2031 年的複合年成長率為 2.11%。

日益成長的購買力限制、更嚴格的進口法規以及向數位化零售通路的穩步轉型,構成了這條成長路徑的特徵。儘管南非仍然是最大的單一區域市場,但烏干達已成為成長最快的市場,這得益於區域貿易協定促進了跨境汽車分銷。 SUV銷售佔主導地位,純線上經銷商的銷售速度超過了所有其他分銷模式,而正規的銷售商在機構資本和專業化管理的推動下,正逐步削弱非正規貿易商的主導地位。同時,歐規混合動力汽車和電動車進口量的增加,預示著東非主要交通走廊正在向更清潔的出行方式轉型。

非洲二手車市場趨勢與洞察

新車價格高昂,購買力差距懸殊

到2024年,奈及利亞1.8億人口中只有2%的人能夠買得起新車,凸顯了購車能力的巨大差距,也促使消費者轉向二手進口車。在衣索比亞,稅收制度對車輛監管採取了截然不同的做法,對老舊的內燃機汽車徵收高達500%的巨額關稅。相較之下,電動車(EV)基本上免徵這些高額稅款,這使得潛在買家要么選擇免稅的準新汽油或柴油車,要么選擇純電動車。這種顯著的價格差異正在非洲二手車市場創造強勁且持續的需求,預計這一趨勢將持續到2030年後。在這些經濟獎勵和環境因素的共同作用下,汽車所有權格局正經歷一場巨大的變化。

拓展汽車金融選擇

在奈及利亞、烏干達和加納,區域金融機構推出了以資產為抵押的二手車貸款,填補了長達數十年的信貸缺口。同時,南非的銀行也開始提供跨境貸款服務。歐洲投資銀行(EIB)估計,非洲每年需要1,940億美元才能實現永續發展目標,而到2025年,更寬鬆的金融環境將有助於信貸供應。在烏干達,強勢貨幣和較低的先令貸款利率使得中等價位的進口商品對企業和消費者來說更實惠。這種有利的經濟環境正在創造新的貿易和購買力機遇,並擴大市場上可供選擇的商品種類。

嚴格的進口車輛年齡限制和排放氣體法規

肯亞對進口車輛的車齡設定了八年上限,並收緊了2025年的排放氣體標準,導致進口價格上漲了10%至20%。奈及利亞提高了關稅,加納則對車齡超過10年的車輛實施了進口限制。這些監管變化造成了規則的混亂,嚴重擠壓了經銷商的利潤空間。政策制定者正在推行鼓勵本地車輛組裝的策略,但其直接結果是供應緊張,並導致整個非洲二手車市場短期成長放緩。

細分市場分析

預計到2025年,SUV和MUV將佔非洲二手車市場59.88%的佔有率,並在2031年之前以4.64%的複合年成長率成長。它們的高離地間隙、靈活的貨物空間和七座配置既能滿足都市區通勤需求,也能滿足農村貨運需求。雖然在停車位有限的人口密集都市區,轎車仍然佔據銷售主導地位,但越來越多的消費者開始轉向跨界車,因為跨界車兼具轎車的舒適性和SUV的實用性。

製造商們正在迅速做出反應。吉利在埃及的全散件組裝廠計劃每年生產3萬輛Coolray SUV,這反映出汽車製造商對SUV需求永續性的信心。叫車業者越來越青睞緊湊型SUV,因為它們比掀背車盈利更高。因此,SUV的殘值堅挺,增強了其對經銷商的吸引力,而經銷商則優先考慮周轉率和融資合格。

到2025年,汽油動力系統將佔非洲二手車市場的67.70%,而混合動力汽車和電動車的進口量預計到2031年將以10.82%的複合年成長率成長。柴油引擎憑藉其出色的扭矩和燃油經濟性,繼續在商業運營商中佔據主導地位。然而,這些業者也面臨日益嚴格的排放氣體法規,挑戰了他們對傳統柴油動力的依賴。

混合動力汽車的普及是政策主導的。衣索比亞禁止內燃機汽車的政策導致大量免稅電動車湧入亞的斯亞貝巴的展示室。盧安達對電動車實施零增值稅,摩洛哥則提供以美元計價的電池組裝補貼,這些都進一步推動了這一趨勢。儘管由於充電網路不足,里程焦慮依然存在,但加油站等非正式解決方案,例如太陽能微電網,正在迅速普及,降低了早期採用者的使用門檻。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 新車高成本且缺乏價格適中的車型。

- 擴大汽車融資選擇

- 網路普及率和網路廣告的不斷提高

- 快速的都市化推動了對出行的需求。

- 二手歐規混合動力汽車和電動車湧入

- 廠商認證二手車計劃

- 市場限制

- 進口汽車有嚴格的車型年份和排放氣體規定。

- 供應國的出口禁令

- 數位化價格透明化給利潤率帶來壓力。

- 售後服務網薄弱

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭強度

第5章 市場規模與成長預測

- 按車輛類型

- 掀背車

- 轎車

- SUV 和 MUV

- 按燃料類型

- 汽油

- 柴油引擎

- 混合動力汽車和電動車

- 其他(液化石油氣、壓縮天然氣等)

- 按價格範圍

- 低於 5,500 美元

- 5,500 美元至 10,999 美元

- 11,000 美元至 21,999 美元

- 超過22,000美元

- 按銷售管道

- 線上數位分類廣告入口網站

- 純線上零售商

- 經銷商/OEM線上平台

- 實體加盟店

- 獨立二手車經銷商

- 競標場所(線上線下混合模式)

- 私人銷售

- 依供應商類型

- 組織

- 雜亂無章

- 按車輛年份

- 0-2歲

- 3-5年

- 6-8歲

- 8年以上

- 按國家/地區

- 南非

- 摩洛哥

- 阿爾及利亞

- 埃及

- 奈及利亞

- 迦納

- 肯亞

- 衣索比亞

- 坦尚尼亞

- 烏干達

- 其他非洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Autochek Africa

- Erata Motors

- AutoTrader South Africa

- WeBuyCars(Pty)Ltd

- Westvaal Motors(PTY)Ltd

- CFAO Mobility South Africa

- KIFAL Auto

- Sylndr

- Peach Cars

- Carzami Inc.

- AutoTager

- Abdul Latif Jameel Motors

- Halfway Group(Hey Halfway)

- YallaMotor

- Cars 4 Africa

- Automark South Africa

- CMH Ford

- Southern Motor Holdings(PTY)Ltd(SMH Group)

- Global Cars Trading FZ LLC

- cars2africa

- Rola Motor Group

- AUTO24

- CarMax East Africa Ltd

- Jiji Cars

第7章 市場機會與未來展望

The Africa used car market is expected to grow from USD 48.68 billion in 2025 to USD 49.71 billion in 2026 and is forecast to reach USD 55.16 billion by 2031 at 2.11% CAGR over 2026-2031.

Heightened affordability constraints, tighter import regulations, and a steady pivot toward digital retail channels define the growth path. South Africa remains the largest single geography, yet Uganda emerges as the fastest-growing market as regional trade pacts unlock cross-border vehicle flows. SUVs dominate volumes, digital pure-plays outpace all other sales formats, and organized vendors gradually erode informal trader dominance as institutional capital and professional management gain traction. Meanwhile, rising imports of Euro-spec hybrid and electric vehicles (EVs) signal an early transition toward cleaner mobility options across key East African corridors.

Africa Used Car Market Trends and Insights

High Cost of New Cars and Affordability Gap

Only 2% of Nigeria's 180 million citizens could afford a new vehicle in 2024, underlining the affordability gulf that pushes consumers toward used imports. In Ethiopia, the tax framework takes a striking approach to vehicle regulation, imposing staggering duties that can soar up to 500% on older internal-combustion engine vehicles. In stark contrast, electric vehicles (EVs) enjoy a generous exemption from these hefty taxes, steering potential buyers toward either nearly new petrol and diesel models or fully electrified options that come without the burden of duty. This significant price gap creates a robust and sustained demand for the used car market across Africa, a trend expected to persist well into 2030 and beyond. The landscape of vehicle ownership is shifting dramatically, driven by these economic incentives and environmental considerations.

Expansion of Vehicle-financing Options

Regional lenders are filling a decades-long credit void by rolling out asset-backed loans for used purchases in Nigeria, Uganda, and Ghana, while South African banks now offer cross-border financing. The European Investment Bank estimates Africa needs USD 194 billion annually to meet SDGs, with monetary conditions easing through 2025, supporting loan availability . Uganda's currency has strengthened, and the easing of shilling lending rates has made it easier for businesses and consumers to afford mid-range imports. This favorable shift in the economic landscape opens up new opportunities for trade and purchasing power, allowing for a wider selection of goods to become accessible to the market.

Stringent Import-age and Emissions Rules

Kenya enforces an eight-year age cap and tighter 2025 emissions standards that lifted import prices 10-20% . Nigeria has increased tariffs, while Ghana has imposed restrictions on importing vehicles older than ten years. These regulatory shifts are creating a patchwork of rules that are pinching dealer margins tightly. Though policymakers are pursuing strategies to stimulate local vehicle assembly, the immediate consequence has been a constricted supply that dampens short-term growth in the used car market across Africa.

Other drivers and restraints analyzed in the detailed report include:

- Growing Internet Penetration and Online Classifieds

- Rapid Urbanization Driving Mobility Demand

- Export Bans in Source Countries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

SUVs and MUVs held 59.88% of the Africa used car market share in 2025 and will post a 4.64% CAGR to 2031. Robust ground clearance, flexible cargo capacity, and seven-seat configurations meet both urban commute and rural haulage demands. Sedans still claim volume in densely populated city centers where parking is tight, yet buyers are migrating to crossovers that combine sedan comfort with SUV utility.

Manufacturers are responding swiftly: Geely's Completely Knocked-Down plant in Egypt targets 30,000 Coolray SUVs annually, reflecting OEM conviction in sustained SUV appetite. Ride-hailing operators increasingly favor compact SUVs, citing higher earning potential than hatchbacks. Consequently, SUV residual values remain resilient, reinforcing their appeal to organized dealers who prioritize turnover speed and financing eligibility.

Petrol powertrains commanded 67.70% of the Africa used car market size in 2025, while hybrid and EV imports will expand at 10.82% CAGR through 2031. Diesel engines continue to assert their dominance among commercial operators, who appreciate their formidable torque and impressive fuel efficiency. However, these operators are now navigating an increasingly stringent landscape of emissions regulations that challenge their reliance on traditional diesel power.

The hybrid surge is policy-led: Ethiopia's ICE ban funnels duty-free electrified stock into Addis Ababa showrooms. Rwanda's zero-rate VAT on EVs and Morocco's USD-backed battery-assembly incentives compound momentum. Range anxiety persists due to sparse charging networks, yet informal solutions solar micro-grids at fuel stations, are proliferating and lowering early-adopter barriers.

The Africa Used Car Market Report is Segmented by Vehicle Type (Hatchbacks, Sedans, and More), Fuel Type (Petrol, Diesel, and More), Price Segment (Below USD 5, 500, USD 5, 500-10, 999, and More), Sales Channel (Online Digital Classified Portals, Pure-Play E-Retailers, and More), Vendor Type (Organized and Unorganized), Vehicle Age, and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Autochek Africa

- Erata Motors

- AutoTrader South Africa

- WeBuyCars (Pty) Ltd

- Westvaal Motors (PTY) Ltd

- CFAO Mobility South Africa

- KIFAL Auto

- Sylndr

- Peach Cars

- Carzami Inc.

- AutoTager

- Abdul Latif Jameel Motors

- Halfway Group (Hey Halfway)

- YallaMotor

- Cars 4 Africa

- Automark South Africa

- CMH Ford

- Southern Motor Holdings (PTY) Ltd (SMH Group)

- Global Cars Trading FZ LLC

- cars2africa

- Rola Motor Group

- AUTO24

- CarMax East Africa Ltd

- Jiji Cars

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High Cost of New Cars and Affordability Gap

- 4.2.2 Expansion of Vehicle-financing Options

- 4.2.3 Growing Internet Penetration and Online Classifieds

- 4.2.4 Rapid Urbanization Driving Mobility Demand

- 4.2.5 Influx of Euro-spec Hybrid/EV Used Cars

- 4.2.6 OEM-certified Pre-owned Programs

- 4.3 Market Restraints

- 4.3.1 Stringent Import-age and Emissions Rules

- 4.3.2 Export Bans in Source Countries

- 4.3.3 Margin Squeeze from Digital Price Transparency

- 4.3.4 Weak After-sales Service Network

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Vehicle Type

- 5.1.1 Hatchbacks

- 5.1.2 Sedans

- 5.1.3 SUVs and MUVs

- 5.2 By Fuel Type

- 5.2.1 Petrol

- 5.2.2 Diesel

- 5.2.3 Hybrid and Electric

- 5.2.4 Others (LPG, CNG, etc.)

- 5.3 By Price Segment

- 5.3.1 Below USD 5,500

- 5.3.2 USD 5,500 - 10,999

- 5.3.3 USD 11,000 - 21,999

- 5.3.4 >= USD 22,000

- 5.4 By Sales Channel

- 5.4.1 Online Digital Classified Portals

- 5.4.2 Pure-play e-Retailers

- 5.4.3 Dealer/OEM Online Platforms

- 5.4.4 Physical Franchise Dealerships

- 5.4.5 Independent Used-Car Lots

- 5.4.6 Auction Houses (Physical and Online Hybrid)

- 5.4.7 Peer-to-Peer (Private) Sales

- 5.5 By Vendor Type

- 5.5.1 Organized

- 5.5.2 Unorganized

- 5.6 By Vehicle Age

- 5.6.1 0 -2 Years

- 5.6.2 3-5 Years

- 5.6.3 6-8 Years

- 5.6.4 Above 8 Years

- 5.7 By Country

- 5.7.1 South Africa

- 5.7.2 Morocco

- 5.7.3 Algeria

- 5.7.4 Egypt

- 5.7.5 Nigeria

- 5.7.6 Ghana

- 5.7.7 Kenya

- 5.7.8 Ethiopia

- 5.7.9 Tanzania

- 5.7.10 Uganda

- 5.7.11 Rest of Africa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Autochek Africa

- 6.4.2 Erata Motors

- 6.4.3 AutoTrader South Africa

- 6.4.4 WeBuyCars (Pty) Ltd

- 6.4.5 Westvaal Motors (PTY) Ltd

- 6.4.6 CFAO Mobility South Africa

- 6.4.7 KIFAL Auto

- 6.4.8 Sylndr

- 6.4.9 Peach Cars

- 6.4.10 Carzami Inc.

- 6.4.11 AutoTager

- 6.4.12 Abdul Latif Jameel Motors

- 6.4.13 Halfway Group (Hey Halfway)

- 6.4.14 YallaMotor

- 6.4.15 Cars 4 Africa

- 6.4.16 Automark South Africa

- 6.4.17 CMH Ford

- 6.4.18 Southern Motor Holdings (PTY) Ltd (SMH Group)

- 6.4.19 Global Cars Trading FZ LLC

- 6.4.20 cars2africa

- 6.4.21 Rola Motor Group

- 6.4.22 AUTO24

- 6.4.23 CarMax East Africa Ltd

- 6.4.24 Jiji Cars

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

二手電動車市場規模、佔有率和成長分析:按車輛類型、驅動方式、年份、續航里程、電池狀況、電池容量和地區分類-2026-2033年產業預測

二手電動車市場規模、佔有率和成長分析:按車輛類型、驅動方式、年份、續航里程、電池狀況、電池容量和地區分類-2026-2033年產業預測 2026-2030年全球二手車市場

2026-2030年全球二手車市場 二手車市場:2026-2032年全球市場預測(按車輛類型、燃料類型、年份、變速箱類型、所有權、用途和銷售管道)

二手車市場:2026-2032年全球市場預測(按車輛類型、燃料類型、年份、變速箱類型、所有權、用途和銷售管道) 全球二手車市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球二手車市場規模、佔有率、趨勢和成長分析報告(2026-2034) 二手半拖車市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、流程及最終用戶二手

二手半拖車市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、流程及最終用戶二手 東南亞二手車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南二手車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)二手車市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,以及2026-2034年的預測

東南亞二手車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南二手車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)二手車市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,以及2026-2034年的預測 二手拖車市場-全球產業規模、佔有率、趨勢、機會和預測:按車輛類型、動力類型、銷售管道、地區和競爭格局分類,2021-2031年二手車市場 - 全球產業規模、佔有率、趨勢、競爭格局、機會、預測(按車輛類型、動力類型、銷售管道、最終用途、地區和競爭情況分類),2021-2031年

二手拖車市場-全球產業規模、佔有率、趨勢、機會和預測:按車輛類型、動力類型、銷售管道、地區和競爭格局分類,2021-2031年二手車市場 - 全球產業規模、佔有率、趨勢、競爭格局、機會、預測(按車輛類型、動力類型、銷售管道、最終用途、地區和競爭情況分類),2021-2031年