|

市場調查報告書

商品編碼

1934762

東南亞二手車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)South-East Asia Used Car - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

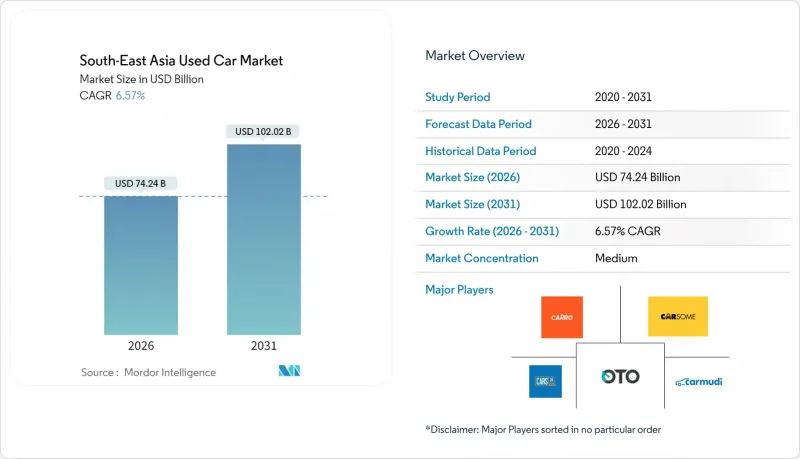

2025年東南亞二手車市場價值696.6億美元,預計到2031年將達到1,020.2億美元,高於2026年的742.4億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 6.57%。

推動這項擴張的因素包括車輛周轉率率高、準新SUV供應穩定以及零售流程的快速數位化。同時,透過標準化的品質和金融合作,有組織的經銷商網路正在蓬勃發展。東南亞二手車市場受益於可支配收入的成長、都市區擁塞促使駕駛員轉換小型車輛,以及政府獎勵推動電動車普及和結構化報廢計畫。線上平台利用人工智慧驅動的定價增強了買家的議價能力,縮小了數位鴻溝,而綜合融資則刺激了那些難以獲得銀行服務的買家的需求。馬來西亞取消部分車型的新車稅以及泰國對舊車的優惠進口政策進一步影響了該地區的跨境貿易流動。

東南亞二手車市場趨勢與洞察

透過線上通路和數位市場實現銷售額成長

隨著平台透過卓越的客戶獲取和留存機制不斷擴大市場佔有率,數位市場的興起正從根本上改變交易模式。 Carsome在2024年第一季實現了EBITDA獲利,單位毛利年增48%。同時,該公司透過與Google雲端的雲端基礎設施整合,提升了其人工智慧驅動的客戶經驗。智慧型手機普及率超過80%的都市區市場正在加速數位化管道轉型,實現遠端車輛偵測、數位化文件和整合金融解決方案,減少交易摩擦。線上平台正在利用數據分析最佳化定價演算法,從而獲得相對於依賴人工估價流程的傳統經銷商的競爭優勢。

經銷商網路和認證二手車專案的發展

隨著車輛(尤其是混合動力汽車和電動動力系統)日益複雜,消費者對標準化品質保證和保固服務的需求不斷成長,正規經銷商的擴張也反映了這一趨勢。豐田、本田和梅賽德斯-奔馳等汽車製造商紛紛設立專門的二手車部門,提供全面的檢測通訊協定和延長的保固服務,其認證動力傳動系統二手項目也因此日益普及。監管合規要求越來越傾向於那些擁有完善的文件、符合稅務規定並遵守消費者保護標準的正規經銷商,這使得它們相對於非正規市場參與企業而言具有結構性優勢。在法規結構中更完善的市場,例如印尼和越南,政府透過稅收優惠和簡化許可程序等措施鼓勵企業參與正規市場,從而加速向正規網路的轉型。

非正規經銷商和路邊攤販佔據主導地位

非正規經銷商的激增阻礙了市場專業化,限制了消費者獲得正規融資管道,造成結構性效率低下,並抑制了整體貿易量。這些非正規管道缺乏標準化的檢驗程序、保固條款和融資夥伴關係,迫使消費者依賴現金交易,將相當一部分潛在買家排除在外。農村市場滲透仍然主要由路邊經銷商主導,他們利用當地關係和靈活的議價技巧。然而,他們難以提供建立長期客戶忠誠度所需的品質保證和售後服務。

細分市場分析

到2025年,SUV將佔東南亞二手車市場30.98%的佔有率,這反映出東南亞消費者偏好正在發生變化,尤其是在城市環境中。在政府獎勵和主要大都市地區充電基礎設施改善的推動下,SUV類別中的電動車細分市場預計將在2031年之前以26.15%的複合年成長率快速成長。掀背車在注重性價比的細分市場中保持著強勁的勢頭,尤其是在印尼和越南,小型車的價格與中產階級的購買力相符。同時,隨著消費者轉向更實用的車型,轎車的需求正在下降。多用途汽車(MPV)在以家庭為導向的消費者中佔據了相當大的市場佔有率,例如三菱Xpander等車型在2025年第一季推動了越南的銷量。

都市化的加快推動了對能夠應對各種路況(從城市交通到偶爾的郊區駕駛)的車輛的需求,加速了SUV的普及。越南市場數據顯示,2025年上半年轎車銷售量將呈下降趨勢,消費者越來越傾向選擇車身較高的車輛,因為這些車輛在視野和安全性方面具有優勢。這一趨勢對二手車市場產生了連鎖反應,SUV庫存價格上漲。同時,轎車價格面臨下行壓力,從根本上改變了全部區域的經銷商庫存策略和貸款風險評估。

截至2025年,汽油動力汽車在東南亞二手車市場佔比高達72.13%,這主要得益於完善的加油基礎設施以及相比其他燃料技術更低的初始成本。電動車是成長最快的細分市場,年複合成長率達26.05%,但由於充電基礎設施不足以及電池劣化導致的二手車殘值問題,其普及受到阻礙。柴油汽車主要集中在商用和重型車輛領域,而液化石油氣(LPG)、壓縮天然氣(CNG)和混合動力系統等替代燃料在政府扶持政策和燃料成本優勢顯著的市場中正日益普及。

印尼已將電動車100%的奢侈品稅免稅政策延長至2025年,以鼓勵電動車的普及。然而,由於消費者購買力下降以及對新車型上市的預期,2024年電動車銷量下降了15%。二手電動車市場仍處於發展階段,技術的快速進步導致折舊率加快,電池性能也限制了消費者對二手電動車的信心。新加坡在東南亞電動車市場的領先地位正在產生示範效應,這將影響該地區的電動車普及模式。然而,區域城市的基礎設施限制阻礙了電動車在東協市場的廣泛普及。

到2025年,車齡4-6年的車輛將佔東南亞二手車市場佔有率的37.98%,代表了折舊免稅額、功能性和中等收入消費者融資管道的最佳平衡。車齡0-3年的車輛細分市場將以18.62%的複合年成長率快速成長,直至2031年,這主要得益於新車周轉率的上升以及消費者對仍在原廠保固期內的二手車的偏好。車齡7-10年的車輛在價格敏感型細分市場將保持穩定的需求,而車齡10年以上的車輛則面臨著排放氣體法規和車輛現代化改造報廢激勵政策帶來的監管壓力。

中檔車市場的集中度反映了融資的便利性,因為銀行和非銀行金融公司(NBFC)更傾向於以折舊免稅額曲線可預測且剩餘使用壽命充足的資產作為抵押,以確保貸款條款的有效性。越南2024年的經濟成長將擴大4-6年車齡車輛的潛在市場,因為收入的成長將使消費者更換舊車或首次購車。政府的報廢政策主要針對車齡超過15年的車輛,這人為地加速了對4-8年車齡車輛(配備最新安全和排放氣體標準的替代車型)的需求。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 透過線上通路和數位市場實現銷售額成長

- 經銷商網路和認證二手車專案的發展

- 新車(尤其是SUV)銷售的周轉率正在促進二手車供應。

- 提供綜合金融和保險解決方案

- 政府的循環經濟政策和報廢激勵措施促進了以舊換新。

- 透過人工智慧驅動的檢測和定價平台,買家信心增強

- 市場限制

- 非正規經銷商和路邊銷售點的主導地位

- 缺乏標準化的車輛狀況報告通訊協定

- 加強對二手車進口的監管

- 都市區出行即服務(MaaS)的普及導致私家車擁有量下降

- 價值/價值鏈分析

- 技術展望

- 監管環境

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按車輛類型

- 掀背車

- 轎車

- 運動型多用途車(SUV)

- 多用途汽車(MPV)

- 按燃料類型

- 汽油

- 柴油引擎

- 電動車

- 替代燃料(液化石油氣/壓縮天然氣/混合動力)

- 車齡

- 0-3歲

- 4-6年

- 7-10歲

- 超過10年

- 按里程

- 不到3萬公里

- 30,001~60,000 km

- 60,001~100,000 km

- 超過10萬公里

- 按銷售管道

- 線上

- 離線

- 依供應商類型

- 組織

- 雜亂無章

- 透過購買方式

- 大量購買

- 購買融資

- 獨家金融

- 銀行貸款

- 非銀行金融公司(NBFC)

- 按國家/地區(東南亞)

- 印尼

- 泰國

- 越南

- 馬來西亞

- 菲律賓

- 新加坡

- 其他國家(柬埔寨、寮國、緬甸、汶萊)

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Carro

- Carsome

- Cars24 Services Pvt Ltd

- Carousell

- OLX

- iCar Asia(Carlist.my)

- myTukar

- BeliMobilGue.co.id

- Carmudi

- Oto.com

- Automart PH

- Mercedes-Benz Certified

- Toyota U Trust

- Honda Certified Pre-Owned

- BMW Premium Selection

- Nissan Intelligent Choice

- Hyundai Promise

- Mitsubishi Diamond Certified

- Isuzu Used Car Program

- LausAutoGroup(Carmix)

第7章 市場機會與未來展望

The Southeast Asia used car market was valued at USD 69.66 billion in 2025 and estimated to grow from USD 74.24 billion in 2026 to reach USD 102.02 billion by 2031, at a CAGR of 6.57% during the forecast period (2026-2031).

Strong vehicle turnover, a steady pipeline of nearly-new SUVs, and rapid digitization of the retail journey underpin this expansion, while organized dealer networks gain traction through standardized quality and financing partnerships. The Southeast Asia used car market benefits from rising disposable incomes, urban congestion that favors smaller vehicle upgrades, and government incentives that stimulate both electric vehicle adoption and structured scrappage programs. Online platforms strengthen bargaining power through AI-driven pricing that narrows informational asymmetries, and integrated financing unlocks demand from underbanked buyers. Malaysia's elimination of new-car taxes on selected segments and Thailand's favorable import rules for older vehicles further shape regional cross-border trade flows.

South-East Asia Used Car Market Trends and Insights

Rising Sales Through Online Channels and Digital Marketplaces

Digital marketplace adoption fundamentally reshapes transaction patterns as platforms capture increasing market share through superior customer acquisition and retention mechanisms. Carsome achieved EBITDA positivity in Q1 2024 with 48% year-on-year gross profit per unit improvement, while consolidating cloud infrastructure with Google Cloud to enhance AI-driven customer experiences. The shift toward digital channels accelerates in urban markets where smartphone penetration exceeds 80%, enabling remote vehicle inspection, digital documentation, and integrated financing solutions that reduce transaction friction. Online platforms leverage data analytics to optimize pricing algorithms, creating competitive advantages over traditional dealerships that rely on manual valuation processes.

Growth in Organized Dealership Networks and Certified Pre-Owned Programs

Organized dealership expansion reflects consumer demand for standardized quality assurance and warranty protection, particularly as vehicle complexity increases with hybrid and electric powertrains. OEM-backed certified pre-owned programs gain traction as manufacturers like Toyota, Honda, and Mercedes-Benz establish dedicated used vehicle divisions with comprehensive inspection protocols and extended warranty coverage. Regulatory compliance requirements increasingly favor organized dealers who maintain proper documentation, tax compliance, and consumer protection standards, creating structural advantages over informal market participants. The shift toward organized networks accelerates in markets with strengthening regulatory frameworks, particularly Indonesia and Vietnam, where government initiatives promote formal sector participation through tax incentives and simplified licensing procedures.

Dominance of Unorganized Dealers and Roadside Lots

Unorganized dealer prevalence constrains market professionalization and limits access to formal financing channels, creating structural inefficiencies that suppress overall transaction volumes. These informal channels lack standardized inspection protocols, warranty provisions, and financing partnerships, forcing consumers to rely on cash transactions that exclude significant portions of the potential buyer base. Rural market penetration remains dominated by roadside dealers who leverage local relationships and flexible negotiation practices, yet struggle to provide quality assurance or post-purchase support that builds long-term customer loyalty.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Turnover of New-Car Sales Feeding Used Supply

- Availability of Integrated Financing and Insurance Solutions

- Lack of Standardized Vehicle-Condition Reporting Protocols

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

SUVs command 30.98% of the Southeast Asia used car market share in 2025, reflecting consumer preference shifts toward higher ground clearance and perceived safety advantages in Southeast Asian urban environments. The electric vehicle segment within the SUV category allows the overall segment to surge at a 26.15% CAGR through 2031, driven by government incentives and improving charging infrastructure across major metropolitan areas. Hatchbacks maintain a strong presence in price-sensitive segments, particularly in Indonesia and Vietnam, where compact vehicle affordability aligns with middle-class purchasing power. At the same time, sedans face declining demand as consumers migrate toward utility-focused vehicle formats. Multi-Purpose Vehicles (MPVs) capture significant market share in family-oriented demographics, with models like Mitsubishi Xpander leading Vietnamese sales in Q1 2025.

The shift toward SUVs accelerates as urbanization increases demand for vehicles capable of handling diverse road conditions, from city traffic to occasional rural excursions. Vietnamese market data reveals sedan sales declining in the first half of 2025, with consumers increasingly favoring higher-riding vehicles that offer superior visibility and perceived safety advantages. This trend creates cascading effects in the used car market, where SUV inventory commands premium pricing. At the same time, sedan values face downward pressure, fundamentally altering dealer inventory strategies and financing risk assessments across the region.

Gasoline-powered vehicles account for 72.13% of the Southeast Asia used car market share in 2025, supported by established refueling infrastructure and lower upfront costs than alternative fuel technologies. Electric vehicles represent the fastest-growing segment at 26.05% CAGR, though adoption faces challenges from limited charging infrastructure and battery degradation concerns that impact resale values. Diesel vehicles concentrate in commercial and heavy-duty applications, while alternative fuels, including LPG, CNG, and hybrid systems, gain traction in markets with supportive government policies and fuel cost advantages.

Indonesia's extension of 100% luxury tax exemption for electric vehicles through 2025 stimulates EV adoption, though sales declined 15% in 2024 due to reduced consumer purchasing power and anticipation of new model launches. The used EV market remains nascent due to rapid technological advancement that accelerates depreciation rates, with battery performance limiting consumer confidence in pre-owned electric vehicles. Singapore's EV market leadership in Southeast Asia creates demonstration effects that influence regional adoption patterns. However, infrastructure limitations in secondary cities constrain widespread electric vehicle penetration across the broader ASEAN market.

Vehicles aged 4-6 years captured 37.98% of the Southeast Asia used car market share in 2025, representing the optimal balance between depreciation, functionality, and financing accessibility for middle-income consumers. The 0-3 year segment grows fastest at 18.62% CAGR through 2031, driven by increasing new car turnover rates and consumer preference for near-new vehicles with remaining manufacturer warranties. Vehicles aged 7-10 years maintain steady demand in price-sensitive segments, while the 10+ year category faces regulatory pressure from emissions standards and scrappage incentives designed to modernize vehicle fleets.

The concentration in mid-life vehicles reflects financing accessibility, as banks and NBFCs prefer lending against assets with predictable depreciation curves and sufficient remaining useful life to secure loan terms. Vietnam's economic growth in 2024 expands the addressable market for 4-6 year vehicles, as rising incomes enable consumers to upgrade from older vehicles or enter car ownership for the first time. Government scrappage policies increasingly target vehicles over 15 years old, creating artificial demand acceleration for replacement vehicles in the 4-8 year age range that offer modern safety and emissions compliance features.

The Southeast Asia Used Car Market Report is Segmented by Vehicle Type (Hatchback, Sedan, SUV, MPV), Fuel Type (Gasoline, and More), Vehicle Age (0-3 Years, and More), Mileage (Under 30K Km, and More), Sales Channel (Online, Offline), Vendor Type (Organized, Unorganized), Purchase Method (Outright, and Financed), and Geography (Indonesia, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

List of Companies Covered in this Report:

- Carro

- Carsome

- Cars24 Services Pvt Ltd

- Carousell

- OLX

- iCar Asia (Carlist.my)

- myTukar

- BeliMobilGue.co.id

- Carmudi

- Oto.com

- Automart PH

- Mercedes-Benz Certified

- Toyota U Trust

- Honda Certified Pre-Owned

- BMW Premium Selection

- Nissan Intelligent Choice

- Hyundai Promise

- Mitsubishi Diamond Certified

- Isuzu Used Car Program

- LausAutoGroup (Carmix)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising sales through online channels and digital marketplaces

- 4.2.2 Growth in organized dealership networks and certified-pre-owned programs

- 4.2.3 Increasing turnover of new-car sales (especially SUVs) feeding used supply

- 4.2.4 Availability of integrated financing and insurance solutions

- 4.2.5 Government circular-economy and scrappage incentives accelerating trade-ins

- 4.2.6 AI-driven inspection/pricing platforms boosting buyer trust

- 4.3 Market Restraints

- 4.3.1 Dominance of unorganized dealers and roadside lots

- 4.3.2 Lack of standardized vehicle-condition reporting protocols

- 4.3.3 Emerging import restrictions on older used vehicles

- 4.3.4 Reduced private-car ownership in urban areas due to mobility-as-a-service

- 4.4 Value/Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Vehicle Type

- 5.1.1 Hatchback

- 5.1.2 Sedan

- 5.1.3 Sport-Utility Vehicle (SUV)

- 5.1.4 Multi-Purpose Vehicle (MPV)

- 5.2 By Fuel Type

- 5.2.1 Gasoline

- 5.2.2 Diesel

- 5.2.3 Electric

- 5.2.4 Alternative Fuels (LPG/CNG/Hybrid)

- 5.3 By Vehicle Age

- 5.3.1 0 to 3 Years

- 5.3.2 4 to 6 Years

- 5.3.3 7 to 10 Years

- 5.3.4 More than 10 Years

- 5.4 By Mileage

- 5.4.1 Less than 30 000 km

- 5.4.2 30 001 to 60 000 km

- 5.4.3 60 001 to 100 000 km

- 5.4.4 More than 100 000 km

- 5.5 By Sales Channel

- 5.5.1 Online

- 5.5.2 Offline

- 5.6 By Vendor Type

- 5.6.1 Organized

- 5.6.2 Unorganized

- 5.7 By Purchase Method

- 5.7.1 Outright Purchase

- 5.7.2 Financed Purchase

- 5.7.2.1 Captive Financing

- 5.7.2.2 Bank Financing

- 5.7.2.3 Non-Banking Financial Companies (NBFC)

- 5.8 By Country (Southeast Asia)

- 5.8.1 Indonesia

- 5.8.2 Thailand

- 5.8.3 Vietnam

- 5.8.4 Malaysia

- 5.8.5 Philippines

- 5.8.6 Singapore

- 5.8.7 Other Countries (Cambodia, Laos, Myanmar, Brunei)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Carro

- 6.4.2 Carsome

- 6.4.3 Cars24 Services Pvt Ltd

- 6.4.4 Carousell

- 6.4.5 OLX

- 6.4.6 iCar Asia (Carlist.my)

- 6.4.7 myTukar

- 6.4.8 BeliMobilGue.co.id

- 6.4.9 Carmudi

- 6.4.10 Oto.com

- 6.4.11 Automart PH

- 6.4.12 Mercedes-Benz Certified

- 6.4.13 Toyota U Trust

- 6.4.14 Honda Certified Pre-Owned

- 6.4.15 BMW Premium Selection

- 6.4.16 Nissan Intelligent Choice

- 6.4.17 Hyundai Promise

- 6.4.18 Mitsubishi Diamond Certified

- 6.4.19 Isuzu Used Car Program

- 6.4.20 LausAutoGroup (Carmix)

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Improved focus on bundled value-added services (Financing, insurance, extended warranty, subscription plans)

二手車市場-2026-2032年全球市場預測

二手車市場-2026-2032年全球市場預測 日本二手車市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031)美國二手車市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)泰國二手車市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

日本二手車市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031)美國二手車市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)泰國二手車市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 二手車交易服務市場:依車輛類型、燃料類型、銷售管道、銷售形式及地區分類。

二手車交易服務市場:依車輛類型、燃料類型、銷售管道、銷售形式及地區分類。 二手電動車市場規模、佔有率和成長分析:按車輛類型、驅動方式、年份、續航里程、電池狀況、電池容量和地區分類-2026-2033年產業預測

二手電動車市場規模、佔有率和成長分析:按車輛類型、驅動方式、年份、續航里程、電池狀況、電池容量和地區分類-2026-2033年產業預測 2026-2030年全球二手車市場二手車市場:依供應商、車款、銷售管道、地區分類

2026-2030年全球二手車市場二手車市場:依供應商、車款、銷售管道、地區分類 全球二手車市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球二手車市場規模、佔有率、趨勢和成長分析報告(2026-2034) 二手半拖車市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、流程及最終用戶二手

二手半拖車市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、流程及最終用戶二手