|

市場調查報告書

商品編碼

1940696

亞太地區數位戶外(DOOH):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Asia Pacific Digital-Out-of-Home (DOOH) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

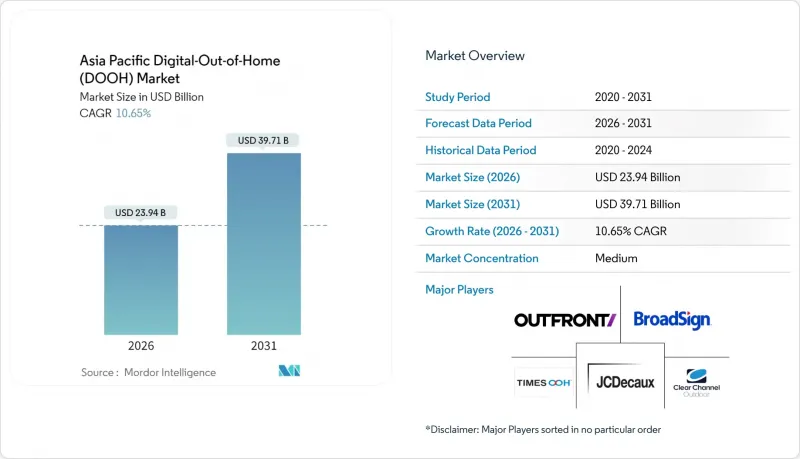

亞太地區數位戶外(DOOH) 市場預計將從 2025 年的 216.4 億美元成長到 2026 年的 239.4 億美元,預計到 2031 年將達到 397.1 億美元,2026 年至 2031 年的複合年成長率為 10.65%。

加速的都市化、5G 連接的擴展以及 LED 硬體價格的下降,正推動媒體營運商將路邊、交通和室內網路數位化,從而實現更豐富的創新表達和更可靠的效果衡量。到 2025 年,光是中國就將佔全球廣告支出的 51.2%,凸顯了全部區域依賴。同時,隨著地鐵、機場和高速公路計劃的建設釋放出優質廣告資源並推動程序化購買,印度的廣告支出正經歷兩位數的成長。廣告主正迅速將預算轉移到經過受眾檢驗的地點,因為位置資料為依賴 cookie 的數位管道提供了品牌安全的替代方案。德高集團 (JCDecaux) 的程序化廣告支出將在 2024 年成長 45.6%,這印證了全部區域自動化購買技術的成熟。

亞太地區數位戶外(DOOH)市場趨勢與洞察

城市軌道交通線路的快速擴張釋放了優質房源。

大規模地鐵、機場和快速公車(BRT)計劃正在打造封閉式環境,為乘客提供更長的停留時間和更豐富的上下文資料饋送。印度Times OOH獲得了孟買地鐵3號線的獨家廣告權,涵蓋2萬平方公尺和27個車站,充分展現了亞太地區數位戶外(DOOH)市場新增廣告資源的規模。香港地鐵正在擴展其數位肖像廣告單元,並在身臨其境型區域中試行氣味行銷。車站內的照明控制和保全系統支援高清LED、3D和互動式標牌,使品牌能夠在乘客旅途中持續訊息。隨著亞洲許多城市交通走廊的建設,預計未來十年廣告供應成長速度將超過路邊廣告轉換率。

程序化戶外數位廣告與零售媒體網路的整合

零售商正將銷售點 (POS) 數據與店內螢幕連接起來,以完善歸因分析,並顯示銷售成長帶來的益處。京東商城與漢秀的聯合解決方案將電子貨架標籤與天花板標誌連接起來,同步更新產品價格、QR碼和創新。 GroupM 和 Moving Walls 正在印尼、馬來西亞和菲律賓實現這一工作流程的自動化,使消費品品牌能夠購買與其目標受眾群體相關的廣告曝光率。在亞太地區的數位戶外(DOOH) 市場,零售媒體融合正在推動 CPM 的提升,支援客流量歸因分析,並將以往僅限於商品行銷的多格式預算擴展到店內網路。

媒體所有權分散化增加了購買的複雜性。

光是在日本,就有大約1000家戶外數位廣告(DOOH)媒體所有者,這迫使行銷人員在開展大範圍宣傳活動前,需要協商多份合約並驗證衡量標準的一致性。印度也面臨類似的挑戰,61%的本地所有者傾向於透過聯合競標的方式贏得城市計劃的國內宣傳活動競標。這些摩擦阻礙了程序化廣告的普及,增加了廣告投放訂單出錯的風險,並延長了結算週期,從而削弱了亞太地區戶外數位廣告市場相對於線上展示廣告在「預算執行速度」方面的優勢。

細分市場分析

室內螢幕在亞太地區數位戶外(DOOH) 市場的佔有率正在不斷成長,年複合成長率 (CAGR) 為 10.92%,而到 2025 年,戶外廣告仍將佔總收入的 62.05%。室內場所避免了天氣造成的運作,並能延長顧客的停留時間。在新加坡萊佛士城,一項 11.1 萬平方英尺的整修整合了教學鏡、行動 POS 機和診斷亭,旨在為美妝和科技品牌帶來可衡量的互動。東南亞各地配備空調的購物中心正在延長消費者的停留時間,並幫助廣告商測試將會員 ID 與螢幕互動相結合的遊戲化策略。

儘管戶外廣告形式在亞太地區的數位戶外(DOOH) 市場佔據主導地位,但印度加特科帕爾廣告看板崩壞後,地方政府實施了更嚴格的安全法規,導致許可核准週期延長,維護成本增加。儘管如此,路邊 LED 塔式廣告看板仍然佔據一定的預算佔有率,為汽車、電信和金融科技產品的發布提供了無可比擬的覆蓋範圍。

到2025年,戶外廣告看板將佔總收入的45.39%,保持傳統廣告支出水平,並在主要高速公路沿線擁有廣泛的曝光度。同時,受鐵路網擴張和匿名乘客數據分析的推動,程序化交通廣告庫存正以11.9%的複合年成長率快速成長,直至2031年。 Hit Co.和Vistar Media已向全球DSP開放其澀谷「Synchro 7」網路(七塊同步螢幕),徵兆高容量競標機制正逐步應用於亞洲最繁忙的交通樞紐。

街道、場所和機場媒體正受益於融入物聯網感測器的智慧城市計劃;然而,採購週期延長和政府競標繁瑣阻礙了其成長。相較之下,交通廣告螢幕能夠提供精準的客流量模式,使品牌能夠透過行動端推廣活動重新接觸乘客,從而為原本單向的媒體增添了效果行銷的維度。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 產業價值鏈分析

- 宏觀經濟因素的影響

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 監管環境

- 技術展望

第5章 市場動態

- 市場促進因素

- 5G部署能夠實現高頻寬創新

- 城市軌道交通網路的快速擴張創造了優質房源。

- 程序化戶外數位廣告與零售媒體網路的整合

- LED成本下降加速數位轉型

- 將廣告從基於 cookie 的廣告轉向基於位置的數位戶外廣告,作為品牌安全措施

- 節能環保的螢幕吸引了注重環境、社會和治理(ESG)的廣告商。

- 市場限制

- 媒體所有權分散化使購買過程變得複雜。

- 電力價格波動會推高營運成本。

- 資料隱私法規限制行動重定向

- 新興市場數位戶外廣告創新人才短缺

第6章 市場規模與成長預測

- 按位置

- 室內的

- 戶外

- 按格式類型

- 廣告看板

- 交通

- 街道家具

- 基於地點的媒體

- 透過使用

- 動態廣告

- 即時資訊和路線

- 互動式/體驗式

- 其他用途

- 最終用戶

- 零售與電子商務

- 車

- 金融服務

- 醫療和藥品

- 政府/公共部門

- 娛樂與媒體

- 其他最終用戶

- 依所有權類型

- 媒體所有者網路

- 設施內專用網路

- 按國家/地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 新加坡

- 泰國

- 香港

- 亞太其他地區

第7章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- JCDecaux SE

- Focus Media Information Technology Co. Ltd.

- Clear Channel Outdoor Holdings Inc.

- oOh!media Limited

- Outfront Media Inc.

- Times Innovative Media Limited

- Plan B Media Public Company Limited

- Asiaray Media Group Limited

- Shanghai Airports Advertisement Co. Ltd.

- Balintimes Media Group Co. Ltd.

- Hivestack Inc.

- Vistar Media Inc.

- Daktronics Inc.

- Broadsign International LLC

- Ayuda Media Systems Inc.

- QMS Media Limited

- AdOnMo Private Limited

- Laqshya Media Group

- MediaCorp Pte Ltd.

第8章:市場機會與未來展望

- 閒置頻段與未滿足需求評估

The Asia Pacific Digital-Out-of-Home (DOOH) market is expected to grow from USD 21.64 billion in 2025 to USD 23.94 billion in 2026 and is forecast to reach USD 39.71 billion by 2031 at 10.65% CAGR over 2026-2031.

Accelerated urbanization, expanding 5G connectivity, and falling LED hardware prices are simultaneously pushing media owners to digitize roadside, transit, and indoor networks, creating richer creative canvases and more accountable measurement. China alone captures 51.2% of worldwide spend in 2025, demonstrating how regional performance hinges on a single, high-scale advertising economy. At the same time, India is posting double-digit growth as metro, airport, and highway projects unlock premium inventory and programmatic-ready. Advertisers are rapidly shifting budgets toward audience-verified locations because location data delivers brand-safe alternatives to cookie-dependent digital channels. Programmatic spend rose 45.6% at JCDecaux in 2024, underscoring how automated buying is maturing across the region.

Asia Pacific Digital-Out-of-Home (DOOH) Market Trends and Insights

Rapid Urban Rail Expansion Opening Premium Inventory

Large-scale metro, airport, and bus-rapid-transit projects are unlocking enclosed environments with superior dwell times and contextual data feeds. India's Times OOH secured exclusive rights for Mumbai Metro Line 3, covering 20,000 m2 and 27 stations, evidencing the size of fresh inventory entering the Asia Pacific Digital-Out-of-Home (DOOH) market. Hong Kong's MTR expanded digital portrait units and is piloting scent marketing in immersive zones. Controlled lighting and security inside stations allow fine-pitch LED, 3D, and interactive wayfinding screens, enabling brands to run sequential messaging throughout a rider's trip. With many Asian cities still mid-build on transit corridors, supply growth is likely to outpace roadside conversions over the next decade.

Programmatic DOOH Integration with Retail Media Networks

Retailers are pairing point-of-sale data with on-premise screens to close attribution loops and prove incremental sales lift. JD Mall's joint solution with Hanshow links electronic shelf labels and overhead boards so product prices, QR codes, and creative refresh simultaneously. GroupM and Moving Walls automate this workflow in Indonesia, Malaysia, and the Philippines, letting CPG brands buy impressions tied to first-party audience segments. For the Asia Pacific Digital-Out-of-Home (DOOH) market, the retail-media collision creates incremental CPMs, aids footfall attribution, and drives multi-format budgets into in-store networks once confined to merchandising budgets.

Fragmented Media Ownership Inflating Buying Complexity

Japan alone hosts roughly 1,000 DOOH media owners, forcing marketers to negotiate multiple contracts and reconcile measurement gaps before pan-regional flights ever go live. India faces similar hurdles, prompting 61% of local owners to support consortium bids for metro projects to win national campaigns. The friction depresses programmatic adoption, raises insertion-order error risk, and prolongs settlement cycles, dampening the Asia Pacific Digital-Out-of-Home (DOOH) market's speed-to-budget advantage over online display.

Other drivers and restraints analyzed in the detailed report include:

- 5G Roll-out Enabling High-Bandwidth Creative

- LED Cost Decline Accelerating Digital Conversion

- Data-Privacy Regulations Limiting Mobile Retargeting

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Indoor screens contribute a growing slice of the Asia Pacific Digital-Out-of-Home (DOOH) market, expanding at an 10.92% CAGR, while outdoor assets still accounted for 62.05% revenue in 2025. Indoor venues avoid weather-related downtime and deliver richer dwell times; Raffles City Singapore integrated tutorial mirrors, mobile POS, and diagnostic kiosks into a 111,000 sq ft facelift that boosted measurable interactions for beauty and tech brands. Shoppers linger longer in air-conditioned malls across Southeast Asia, helping advertisers test gamified activations that connect loyalty IDs to screen engagements.

Outdoor formats dominate inventory numbers for the Asia Pacific Digital-Out-of-Home (DOOH) market, yet municipal safety crackdowns after India's Ghatkopar hoarding collapse are lengthening permit cycles and elevating maintenance expenses. Even so, roadside LED towers provide unmatched reach for automobile, telecom, and fintech launches, preserving their budget share.

Billboards held 45.39% of 2025 revenue, consolidating legacy spend and broad sightlines across arterial roads. Meanwhile, programmatic transit inventory is surging at 11.9% CAGR to 2031 on the back of rail expansion and anonymous passenger analytics. Hit Co. and Vistar Media opened the Shibuya "Synchro 7" network seven synchronised screens to global DSPs, a signpost for high-volume auction mechanics migrating to Asia's most crowded intersections.

Street furniture, place-based, and airport media benefit from smart-city projects that embed IoT sensors; however, elongated procurement cycles and government tendering keep their growth moderate. Transit screens, by contrast, provide precise foot-traffic patterns, enabling brands to retarget riders with mobile promotions, adding a performance layer to what was once a broadcast medium.

The Asia Pacific Digital-Out-Of-Home (DOOH) Market Report is Segmented by Location (Indoor, Outdoor), Format Type (Billboard, Transit, Street Furniture and More), Application (Dynamic Advertising, Real-Time Information and More), End User (Retail and E-Commerce, Automotive and More), Ownership Model (Media Owner Networks, Venue-Based Private Networks) and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- JCDecaux SE

- Focus Media Information Technology Co. Ltd.

- Clear Channel Outdoor Holdings Inc.

- oOh!media Limited

- Outfront Media Inc.

- Times Innovative Media Limited

- Plan B Media Public Company Limited

- Asiaray Media Group Limited

- Shanghai Airports Advertisement Co. Ltd.

- Balintimes Media Group Co. Ltd.

- Hivestack Inc.

- Vistar Media Inc.

- Daktronics Inc.

- Broadsign International LLC

- Ayuda Media Systems Inc.

- QMS Media Limited

- AdOnMo Private Limited

- Laqshya Media Group

- MediaCorp Pte Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Impact of Macroeconomic Factors

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 5G roll-out enabling high-bandwidth creative

- 5.1.2 Rapid urban rail expansion opening premium inventory

- 5.1.3 Programmatic DOOH integration with retail media networks

- 5.1.4 LED cost decline accelerating digital conversion

- 5.1.5 Brand-safety shift from cookies to location-verified DOOH

- 5.1.6 Carbon-efficient screens appealing to ESG-driven advertisers

- 5.2 Market Restraints

- 5.2.1 Fragmented media ownership inflating buying complexity

- 5.2.2 Power-price volatility raising operating costs

- 5.2.3 Data-privacy regulations limiting mobile retargeting

- 5.2.4 Shortage of DOOH-skilled creatives in emerging markets

6 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 6.1 By Location

- 6.1.1 Indoor

- 6.1.2 Outdoor

- 6.2 By Format Type

- 6.2.1 Billboard

- 6.2.2 Transit

- 6.2.3 Street Furniture

- 6.2.4 Place-Based Media

- 6.3 By Application

- 6.3.1 Dynamic Advertising

- 6.3.2 Real-Time Information and Way-finding

- 6.3.3 Interactive / Experiential

- 6.3.4 Other Applications

- 6.4 By End User

- 6.4.1 Retail and E-commerce

- 6.4.2 Automotive

- 6.4.3 Financial Services

- 6.4.4 Healthcare and Pharmaceuticals

- 6.4.5 Government and Public Sector

- 6.4.6 Entertainment and Media

- 6.4.7 Other End Users

- 6.5 By Ownership Model

- 6.5.1 Media Owner Networks

- 6.5.2 Venue-Based Private Networks

- 6.6 By Country

- 6.6.1 China

- 6.6.2 Japan

- 6.6.3 India

- 6.6.4 South Korea

- 6.6.5 Australia

- 6.6.6 Singapore

- 6.6.7 Thailand

- 6.6.8 Hong Kong

- 6.6.9 Rest of Asia Pacific

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles (includes Global level overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 7.4.1 JCDecaux SE

- 7.4.2 Focus Media Information Technology Co. Ltd.

- 7.4.3 Clear Channel Outdoor Holdings Inc.

- 7.4.4 oOh!media Limited

- 7.4.5 Outfront Media Inc.

- 7.4.6 Times Innovative Media Limited

- 7.4.7 Plan B Media Public Company Limited

- 7.4.8 Asiaray Media Group Limited

- 7.4.9 Shanghai Airports Advertisement Co. Ltd.

- 7.4.10 Balintimes Media Group Co. Ltd.

- 7.4.11 Hivestack Inc.

- 7.4.12 Vistar Media Inc.

- 7.4.13 Daktronics Inc.

- 7.4.14 Broadsign International LLC

- 7.4.15 Ayuda Media Systems Inc.

- 7.4.16 QMS Media Limited

- 7.4.17 AdOnMo Private Limited

- 7.4.18 Laqshya Media Group

- 7.4.19 MediaCorp Pte Ltd.

8 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 8.1 White-Space and Unmet-Need Assessment

2026年全球程序化戶外廣告平台市場報告

2026年全球程序化戶外廣告平台市場報告 數位戶外廣告市場:按形式、終端用戶產業、技術、互動性和應用程式分類-全球預測,2026-2032年2026年全球戶外數位廣告市場報告

數位戶外廣告市場:按形式、終端用戶產業、技術、互動性和應用程式分類-全球預測,2026-2032年2026年全球戶外數位廣告市場報告 數位戶外廣告市場報告:按形式、應用程式、最終用戶和地區分類(2026-2034 年)

數位戶外廣告市場報告:按形式、應用程式、最終用戶和地區分類(2026-2034 年) 東南亞數位戶外(DOOH):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

東南亞數位戶外(DOOH):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球數位戶外廣告市場規模、佔有率、趨勢和成長分析報告(2026-2034年)日本戶外廣告和數位戶外廣告:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)全球數位戶外廣告市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析及預測(2026-2034 年)戶外媒體廣告市場按媒體類型、形式、所有權、應用程式和最終用戶產業分類,全球預測(2026-2032年)中東和非洲數位戶外廣告 (DOOH) - 市場佔有率分析、行業趨勢、統計數據和成長預測 (2026-2031)

全球數位戶外廣告市場規模、佔有率、趨勢和成長分析報告(2026-2034年)日本戶外廣告和數位戶外廣告:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)全球數位戶外廣告市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析及預測(2026-2034 年)戶外媒體廣告市場按媒體類型、形式、所有權、應用程式和最終用戶產業分類,全球預測(2026-2032年)中東和非洲數位戶外廣告 (DOOH) - 市場佔有率分析、行業趨勢、統計數據和成長預測 (2026-2031)