|

市場調查報告書

商品編碼

1940691

乙烯基複合地板材料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Vinyl Floor Covering - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

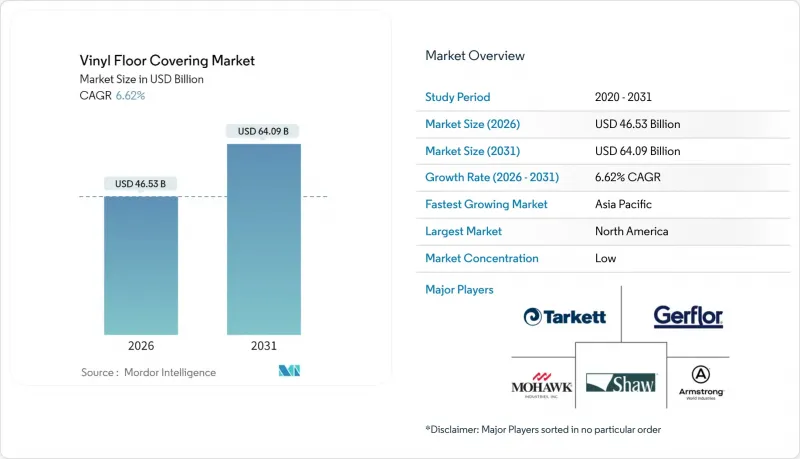

預計乙烯基地板材料市場將從 2025 年的 436.4 億美元成長到 2026 年的 465.3 億美元,並預計到 2031 年將達到 640.9 億美元,2026 年至 2031 年的複合年成長率為 6.62%。

目前市場擴張主要得益於剛性芯材技術,該技術正在取代工程木地板和複合地板,使乙烯基複合地板材料市場免受建設產業波動的影響。循環經濟的必要性、低維護成本和成本效益,以及住宅和商業維修需求,都在加速乙烯基複合地板的普及。雖然豪華乙烯基瓷磚(LVT)仍保持主導地位,但豪華乙烯基板材(LVP)在石材複合材料(SPC)和木塑複合材料(WPC)技術進步的推動下,正超越其競爭對手。亞太地區的規模優勢、南美洲的成長動能以及北美地區的近岸外包舉措,凸顯了全球產能和需求格局的重新調整。

全球PVC地板材料市場趨勢與洞察

新興經濟體建築需求復甦

隨著新興市場建築業的擴張,各國政府優先考慮經濟耐用的解決方案以應對快速的都市化,這推動了PVC地板材料市場的發展。印度的智慧城市計畫和巴西的住宅獎勵策略正集中資源升級地板材料,優先選擇專為承受高人流而設計的SPC和WPC地板。製造商正利用越南的生產能力,憑藉具有競爭力的勞動成本,高效滿足東協和拉丁美洲的需求。當地經銷商將PVC地板的快速施工特性與緊湊的施工進度結合,以加快計劃速度。這些因素共同作用,在原物料價格波動的情況下,提振了基準需求並支撐了價格穩定。

轉向耐用性和低維護成本

醫療保健、教育和酒店業的設施管理人員正在拓展乙烯基(PVC)地板材料市場,將其作為瓷磚和木地板的替代品,以提高清潔效率和感染控制。乙烯基地板的無縫表面可抑制微生物滋生,而免膠鋪設系統則便於在維護週期內快速更換。製造商正在採用超低揮發性有機化合物(VOC)配方和不含鄰苯二甲酸酯的塑化劑,以滿足日益嚴格的室內空氣品質標準,同時又不影響其性能。設計師看重這些先進技術帶來的高階定位,縮小了乙烯基地板與高級地面材料之間的認知差距。耐用性優勢意味著更低的生命週期成本,這更符合注重預算的機構的需求。

PVC樹脂和塑化劑價格波動

PVC樹脂價格與能源和石腦油價格波動密切相關,對整個PVC地板材料市場帶來成本衝擊。儘管製造商透過長期合約對沖部分成本,但仍易受亞洲乙烯價格飆升的影響。小型製造商被迫壓縮利潤率以維持銷售量,限制了研發預算和資本投資。全球買家協商的價格有效期限縮短,使大型計劃的競標過程更加複雜。雖然製造商正尋求透過將前端流程整合到回收製程來減少對原生PVC的依賴,但多層LVT的回收仍面臨許多技術挑戰。

細分市場分析

預計到2025年,豪華乙烯基瓷磚(LVT)將佔據乙烯基地板材料市場74.12%的佔有率,這主要得益於其豐富的款式選擇和卓越的耐用性,吸引了眾多設施負責人和住宅。 LVT在醫療保健、教育和住宿設施的廣泛應用,為其提供了穩定的需求基礎,從而支撐了乙烯基地板材料市場的整體規模。同時,豪華乙烯基木地板預計到2031年將以6.79%的複合年成長率成長,這主要得益於其剛性芯材技術提升了尺寸穩定性並增強了木紋的逼真度。壓紋精度、霧面飾面和壓制倒角技術的進步進一步提升了其美觀度,擴大了乙烯基地板在高階裝修市場與工業實木地板競爭的潛力。抗菌和耐刮擦塗層的不斷改進,也進一步拉大了LVT與陶瓷和強化複合地板產品之間的性能差距。

在預測期內,LVP的卡扣式組裝縮短了安裝週期,這對於面臨勞動力短缺的專業安裝人員來說極具吸引力。製造商將利用數位印刷技術減少圖案庫存,並在PVC價格波動的情況下改善現金流。為此,LVT製造商將推出更厚的耐磨層和整合式底層,用於企業辦公室和多用戶住宅走廊,旨在保持高人流量場所的市場佔有率。生物基PVC配方將率先應用於歐洲LVT產品線,以滿足生態標章採購法規的要求。整個產品格局正在從低成本與高階的二元對立轉變為由核心技術、表面處理和永續性認證定義的頻譜。

到2025年,互鎖式乙烯基地磚的銷售額將佔總銷售額的56.20%,這反映出市場對可縮短計劃施工時間並減少多用戶住宅中黏合劑氣味的浮動地板的需求日益成長。卡扣式結構提高了對不平整地面的適應性,因此在公寓翻新和辦公空間裝修中得到廣泛應用,因為在這些場所,速度比持久性更為重要。自黏式地磚預計到2031年將以7.02%的複合年成長率成長,目前主要面向對尺寸穩定性要求極高的應用領域,例如機場、超市和工業組裝。改良的聚氨酯接著劑和高摩擦背襯降低了翹曲風險,並使維護週期超過10年。

免膠鋪裝創新技術與互鎖式地板相輔相成,其可重新定位的地板條設計,使得迎賓套房能夠快速實現租戶更換。整合式隔音墊無需額外鋪設襯墊即可降低樓層間的噪音傳播,這在高層建築中尤其重要。製造商正投資於機器人加工技術,以實現完美的榫槽公差,從而減少施工現場的廢棄物和保固索賠。黏合劑系統還能減少揮發性有機化合物(VOC)的排放,有助於取得LEED認證,並推動綠建築專案中乙烯基地板材料市場的擴張。總而言之,應用技術正與視覺設計和原料的化學特性一起,成為關鍵的差異化因素。

區域分析

北美地區將佔2025年總收入的36.20%,這主要得益於近岸外包業務,該業務降低了與UFLPA相關的供應風險,並縮短了改造項目的前置作業時間。喬治亞和田納西州國內製造業產能的擴張,降低了對亞洲進口的依賴,並穩定了大型零售商和商業承包商的庫存。同時,預計到2031年,亞太地區的複合年成長率將達到7.90%。隨著中國、印度和東南亞的都市化和基礎設施項目推動需求成長,越南新興的製造業基地正利用其成本優勢,既滿足本地消費需求,也向美國出口產品。

韓國和澳洲可支配收入的成長正推動偏好轉向高階硬芯地板,從而推高平均售價。印度的智慧城市計畫和住宅政策正在打破傳統陶瓷地板材料的壟斷地位,直接將市場轉向現代化的抗衝擊地板材料。區域全面經濟夥伴關係協定(RCEP)下的貿易協定正在簡化亞洲內部運輸,加速產品周轉率和市場滲透。同時,加拿大日益嚴格的揮發性有機化合物(VOC)排放法規正促使消費者轉向低排放的乙烯基產品。這些地理趨勢凸顯了供應鏈重組和多元化成長要素如何重塑全球乙烯基地板材料市場佔有率的分佈模式。

南美洲的增產主要得益於巴西的「居家生活」住宅計畫和智利對教育設施的維修,這兩項計畫都強調了耐用性和衛生性。貨幣穩定和資源出口支撐了家庭維修預算,並促進了乙烯基材料的消費。阿根廷的進口限制提振了當地SPC工廠的前景,而秘魯則依賴北美進口來補充抗震重組材料。南方共同市場(Mercosur)的貿易協定正在簡化區域內運輸,並促進經銷商的整合。隨著市場信心的恢復,商業開發商正從花崗岩轉向木紋SPC,以縮短工期並減輕結構荷載。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 新興國家建築需求的復甦

- 轉向耐用、易於維護的地板材料

- 剛性芯材技術(SPC/WPC)的快速普及

- 住宅裝修活動激增

- 基於循環經濟的乙烯基地板材料回收義務

- 將LVT生產外包至北美和歐盟

- 市場限制

- 聚氯乙烯(PVC)和塑化劑的價格波動

- 人們對室內空氣品質和揮發性有機化合物(VOC)排放的擔憂

- 中美貿易摩擦和《美國工人自由選擇法案》(UFLPA)導致供應鏈中斷

- 多層LVT的報廢回收所面臨的挑戰。

- 產業價值鏈分析

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 洞察市場最新趨勢與創新

- 深入了解市場近期發展動態(新產品發表、策略性舉措、投資、合作、合資、擴張、併購等)

第5章 市場規模與成長預測

- 依產品類型

- 豪華乙烯基瓷磚(LVT)

- 石塑複合材料(SPC)

- 木塑複合材料(WPC)

- 豪華乙烯基木地板(LVP)

- 乙烯基片材

- 其他(VCT,抗衝擊乙烯基背襯橡膠混合材料)

- 豪華乙烯基瓷磚(LVT)

- 透過安裝方法

- 自黏乙烯基瓷磚

- 黏合劑連接

- 互鎖式乙烯基瓷磚

- 其他

- 最終用戶

- 住宅

- 商業的

- 飯店及休閒

- 零售商店和購物中心

- 醫療設施

- 教育

- 總公司

- 公共和政府設施

- 其他商業用戶

- 依建築類型

- 新房產

- 改造/維修

- 透過分銷管道

- B2C/零售

- 家居建材商店

- 專業地板商店

- 線上

- 其他分銷管道

- B2B/承包商/建築商

- B2C/零售

- 按地區

- 北美洲

- 加拿大

- 美國

- 墨西哥

- 南美洲

- 巴西

- 秘魯

- 智利

- 阿根廷

- 其他南美洲

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 比荷盧經濟聯盟(比利時、荷蘭、盧森堡)

- 北歐國家(丹麥、芬蘭、冰島、挪威、瑞典)

- 其他歐洲地區

- 亞太地區

- 印度

- 中國

- 日本

- 澳洲

- 韓國

- 東南亞

- 亞太其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Mohawk Industries

- Tarkett SA

- Shaw Industries Group

- Armstrong World Industries

- Gerflor Group

- Mannington Mills

- Interface Inc.

- Beaulieu International Group

- Forbo Holding AG

- LG Hausys

- Novalis Innovative Flooring

- Milliken & Company

- Raskin Industries

- Congoleum Corporation

- IVCT(IndoFloor Vinyl Composite Tile)

- Karndean Designflooring

- CFL Flooring

- Responsive Industries

- Polyflor Ltd

- ShawContract

第7章 市場機會與未來展望

The vinyl floor covering market is expected to grow from USD 43.64 billion in 2025 to USD 46.53 billion in 2026 and is forecast to reach USD 64.09 billion by 2031 at 6.62% CAGR over 2026-2031.

Current expansion is propelled by rigid-core technologies that displace engineered wood and laminate, a move that shields the vinyl floor covering market from construction volatility. Adoption accelerates as circular-economy mandates, low-maintenance attributes, and cost efficiencies converge in residential remodeling and commercial retrofits. Luxury Vinyl Tile (LVT) retains leadership, yet Luxury Vinyl Plank (LVP) outpaces peers on the back of stone plastic composite (SPC) and wood plastic composite (WPC) advances. Asia-Pacific's scale advantage, South America's growth momentum, and near-shoring efforts in North America together highlight the global re-allocation of capacity and demand vectors.

Global Vinyl Floor Covering Market Trends and Insights

Construction Rebound in Emerging Economies

Emerging market build-outs expand the vinyl floor covering market as governments prioritize cost-effective, durable solutions for rapid urbanization. India's Smart Cities Mission and Brazil's residential stimulus funnel resources into flooring upgrades that favor SPC and WPC formats for heavy traffic endurance. Manufacturers leverage Vietnam-based capacity to serve ASEAN and Latin American demand efficiently, capitalizing on competitive labor rates. Local distributors pair vinyl's quick installation with constrained construction schedules, accelerating project turnovers. Collectively, these factors raise baseline demand and underpin positive price discipline amid raw-material swings.

Shift Toward Resilient, Low-Maintenance Flooring

Facility managers in healthcare, education, and hospitality sectors elevate cleaning efficiency and infection control, expanding the vinyl floor covering market as an alternative to ceramic tile and wood . Vinyl's seamless surfaces reduce microbial harborage, while loose-lay systems facilitate rapid replacement during maintenance cycles. Producers integrate ultra-low VOC recipes and phthalate-free plasticizers, addressing stricter indoor-air-quality codes without sacrificing performance . Specifiers reward these advances with premium positioning, narrowing the perception gap between vinyl and high-end surfaces. The durability narrative translates into lower lifecycle costs that resonate with budget-sensitive institutions.

Volatility in PVC and Plasticizer Prices

PVC resin tracks energy and naphtha inputs, producing cost shocks that ripple through the vinyl floor covering market. Producers hedge partially with long-term contracts but remain exposed when Asian ethylene values spike . Smaller firms thin margins to preserve volume, limiting R&D budgets and capital investment. Global buyers negotiate shorter price-validity windows, complicating tender processes for large-scale projects. Forward integration into recycling streams aims to lower virgin PVC dependence but faces technical hurdles in multilayer LVT reclamation.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of Rigid-Core Technologies (SPC/WPC)

- Surge in Residential Remodeling Activity

- Indoor-Air-Quality & VOC Emission Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Luxury Vinyl Tile commanded 74.12% of the 2025 vinyl floor covering market share as facility planners and homeowners gravitated toward its broad design palette and proven durability. The segment's entrenched position across healthcare, education, and hospitality installations provides stable baseline volume that anchors the overall vinyl floor covering market size. Luxury Vinyl Plank, meanwhile, is projected to grow at a 6.79% CAGR through 2031 as rigid-core technology elevates dimensional stability and wood-look authenticity. Advancements in embossed-in-register textures, matte finishes, and pressed bevels heighten aesthetic realism, enabling vinyl to contest engineered hardwood in premium remodels. Continuous upgrades in antimicrobial and scratch-resistant coatings further widen the performance gap with ceramic and laminate alternatives.

Over the forecast horizon, LVP's click-lock assemblies shorten installation cycles, a feature that appeals to professional contractors juggling labor constraints. Makers capitalize on digital printing to reduce pattern inventory, improving cash flow amid PVC price swings. LVT producers respond with thicker wear layers and integrated underlayment aimed at corporate offices and multifamily corridors, preserving share in heavy-traffic venues. Bio-attributed PVC formulas debut first in European LVT lines to satisfy eco-label procurement rules. Collectively, the product landscape is shifting from a budget-versus-premium dichotomy toward a spectrum defined by core technology, surface finish, and sustainability credentials.

Interlocking vinyl tiles held 56.20% of 2025 revenue, underscoring buyer preference for floating floors that accelerate project timelines and minimize adhesive odors in occupied spaces. Click-lock geometries have grown increasingly tolerant of subfloor irregularities, encouraging adoption in multifamily renovations and office fit-outs where speed outweighs permanence. Glue-down formats, although forecast to climb at a 7.02% CAGR to 2031, now target applications demanding maximum dimensional stability such as airports, grocery aisles, and industrial assembly lines. Enhanced polyurethane adhesives and high-friction backings reduce curl risk, extending lifecycle beyond ten-year maintenance windows.

Loose-lay innovations complement the interlocking segment by offering repositionable planks that facilitate rapid tenant turnovers in hospitality suites. Integrated acoustic pads mitigate floor-to-floor sound transfer without adding separate underlayment, an advantage in high-rise construction. Manufacturers invest in robotic milling to perfect tongue-and-groove tolerances, shrinking on-site waste and warranty claims. Adhesive-free systems also lower VOC emissions, helping projects qualify for LEED credits and propelling the vinyl floor covering market size within green-building programs. Overall, installation technology has emerged as a primary differentiator alongside visual design and raw-material chemistry.

The Vinyl Floor Covering Market is Segmented by Product Type ( Product Type, Luxury Vinyl Plank (LVP), and Other), Installation Method (Self-Adhesive Vinyl Tiles, Glue-Down, and Other), End-User (Residential and Commercial), Construction Type (New Construction and Remodeling / Retrofit), and Distribution Channel(B2C / Retail and B2B / Contractors / Builders ). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 36.20% of 2025 revenue, supported by near-shoring that mitigates UFLPA-related supply risk and shortens lead times for remodel projects. Domestic capacity expansions in Georgia and Tennessee reduce dependency on Asian imports, stabilizing inventory for big-box retailers and commercial contractors. Asia-Pacific, in contrast, is poised for an 7.90% CAGR through 2031 as urbanization and infrastructure programs fuel demand in China, India, and Southeast Asia. Vietnam's burgeoning production hub leverages cost advantages while serving both regional consumption and U.S. re-export flows.

Rising disposable incomes in South Korea and Australia shift consumer preference toward premium rigid-core planks, elevating average selling prices. India's Smart Cities and housing initiatives pivot directly to modern resilient flooring, bypassing legacy ceramic dominance. Trade agreements under RCEP streamline intra-Asia shipments, accelerating product turnover and market penetration. Meanwhile, Canada tightens VOC regulations, nudging buyers toward low-emission vinyl lines. Collectively, the geographic dynamics illustrate how supply-chain realignment and disparate growth drivers reshape the global vinyl floor covering market share distribution.

South America records underpinned by Brazil's Minha Casa Minha Vida housing push and Chilean education upgrades that target durable, hygienic surfaces. Currency stability and commodity exports shore up household renovation budgets, uplifting vinyl consumption. Argentine import restrictions lift prospects for local SPC factories, while Peru leans on North American imports to replenish quake-resilient reconstruction stock. Trade pacts under Mercosur simplify intra-regional shipments, fostering cross-border distributor consolidation. As confidence rebounds, commercial developers shift from granite to wood-look SPC to shorten build schedules and cut structural loads.

- Mohawk Industries

- Tarkett SA

- Shaw Industries Group

- Armstrong World Industries

- Gerflor Group

- Mannington Mills

- Interface Inc.

- Beaulieu International Group

- Forbo Holding AG

- LG Hausys

- Novalis Innovative Flooring

- Milliken & Company

- Raskin Industries

- Congoleum Corporation

- IVCT (IndoFloor Vinyl Composite Tile)

- Karndean Designflooring

- CFL Flooring

- Responsive Industries

- Polyflor Ltd

- ShawContract

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Construction rebound in emerging economies

- 4.2.2 Shift toward resilient, low-maintenance flooring

- 4.2.3 Rapid adoption of rigid-core technologies (SPC/WPC)

- 4.2.4 Surge in residential remodeling activity

- 4.2.5 Circular-economy take-back mandates for vinyl floors

- 4.2.6 Near-shoring of LVT production in North America & EU

- 4.3 Market Restraints

- 4.3.1 Volatility in PVC and plasticizer prices

- 4.3.2 Indoor-air-quality & VOC emission concerns

- 4.3.3 U.S.-China trade & UFLPA supply-chain disruptions

- 4.3.4 End-of-life recycling challenges for multilayer LVT

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Luxury Vinyl Tile (LVT)

- 5.1.1.1 Stone Plastic Composite (SPC)

- 5.1.1.2 Wood Plastic Composite (WPC)

- 5.1.2 Luxury Vinyl Plank (LVP)

- 5.1.3 Sheet Vinyl

- 5.1.4 Others (VCT, Resilient Vinyl-Backed Rubber Hybrid)

- 5.1.1 Luxury Vinyl Tile (LVT)

- 5.2 By Installation Method

- 5.2.1 Self-Adhesive Vinyl Tiles

- 5.2.2 Glue-Down

- 5.2.3 Interlocking Vinyl Tiles

- 5.2.4 Others

- 5.3 By End-User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.2.1 Hospitality & Leisure

- 5.3.2.2 Retail & Shopping Centers

- 5.3.2.3 Healthcare Facilities

- 5.3.2.4 Education

- 5.3.2.5 Corporate Offices

- 5.3.2.6 Public & Government Buildings

- 5.3.2.7 Other Commercial Users

- 5.4 By Construction Type

- 5.4.1 New Construction

- 5.4.2 Remodeling / Retrofit

- 5.5 By Distribution Channel

- 5.5.1 B2C / Retail

- 5.5.1.1 Home Centers

- 5.5.1.2 Specialty Flooring Stores

- 5.5.1.3 Online

- 5.5.1.4 Other Distribution Channels

- 5.5.2 B2B / Contractors / Builders

- 5.5.1 B2C / Retail

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 Canada

- 5.6.1.2 United States

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Peru

- 5.6.2.3 Chile

- 5.6.2.4 Argentina

- 5.6.2.5 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.6.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 India

- 5.6.4.2 China

- 5.6.4.3 Japan

- 5.6.4.4 Australia

- 5.6.4.5 South Korea

- 5.6.4.6 South-East Asia

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East & Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Nigeria

- 5.6.5.5 Rest of Middle East & Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Mohawk Industries

- 6.4.2 Tarkett SA

- 6.4.3 Shaw Industries Group

- 6.4.4 Armstrong World Industries

- 6.4.5 Gerflor Group

- 6.4.6 Mannington Mills

- 6.4.7 Interface Inc.

- 6.4.8 Beaulieu International Group

- 6.4.9 Forbo Holding AG

- 6.4.10 LG Hausys

- 6.4.11 Novalis Innovative Flooring

- 6.4.12 Milliken & Company

- 6.4.13 Raskin Industries

- 6.4.14 Congoleum Corporation

- 6.4.15 IVCT (IndoFloor Vinyl Composite Tile)

- 6.4.16 Karndean Designflooring

- 6.4.17 CFL Flooring

- 6.4.18 Responsive Industries

- 6.4.19 Polyflor Ltd

- 6.4.20 ShawContract

7 Market Opportunities & Future Outlook

- 7.1 Eco-Friendly Vinyl: Recyclable, Low-VOC, and Sustainable Materials

- 7.2 Luxury Vinyl Tiles (LVT) Surging with Hyper-Realistic Textures

- 7.3 DIY-Friendly Click-Lock and Peel-and-Stick Innovations

乙烯基複合地板材料市場:按產品類型、安裝方式、耐磨層厚度、應用和分銷管道分類-全球預測,2026-2032年

乙烯基複合地板材料市場:按產品類型、安裝方式、耐磨層厚度、應用和分銷管道分類-全球預測,2026-2032年 乙烯基複合地板材料市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場分類(2026-2033 年)

乙烯基複合地板材料市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場分類(2026-2033 年) 乙烯基地板材料市場-全球產業規模、佔有率、趨勢、機會、預測:按產品、應用、區域和競爭對手分類,2021-2031年

乙烯基地板材料市場-全球產業規模、佔有率、趨勢、機會、預測:按產品、應用、區域和競爭對手分類,2021-2031年 乙烯基複合地板材料市場規模、佔有率、趨勢和預測:按產品類型、產業和地區分類,2026-2034年

乙烯基複合地板材料市場規模、佔有率、趨勢和預測:按產品類型、產業和地區分類,2026-2034年 2026年全球PVC地板材料市場報告

2026年全球PVC地板材料市場報告 全球乙烯基地板材料市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球乙烯基地板材料市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2035年PVC地板材料市場分析及預測:類型、產品類型、應用、技術、安裝方式、材質類型、最終用戶、功能、解決方案

2035年PVC地板材料市場分析及預測:類型、產品類型、應用、技術、安裝方式、材質類型、最終用戶、功能、解決方案 美國乙烯基複合地板材料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本PVC地板材料市場規模、佔有率、趨勢和預測:按產品類型、行業和地區分類,2026-2034年

美國乙烯基複合地板材料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本PVC地板材料市場規模、佔有率、趨勢和預測:按產品類型、行業和地區分類,2026-2034年 2025-2029年全球抗衝擊PVC地板材料市場

2025-2029年全球抗衝擊PVC地板材料市場