|

市場調查報告書

商品編碼

1937307

美國乙烯基複合地板材料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)US Vinyl Floor Covering - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

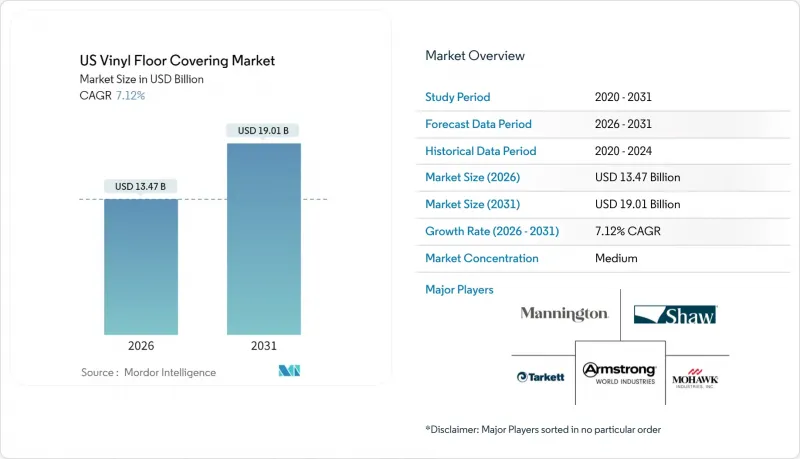

美國乙烯基地板材料市場預計將從 2025 年的 125.7 億美元成長到 2026 年的 134.7 億美元,到 2031 年達到 190.1 億美元,2026 年至 2031 年的複合年成長率為 7.12%。

美國PVC地板材料市場持續保持穩健成長勢頭,強勁的房屋翻新支出、多用戶住宅竣工量的增加以及硬芯技術的快速普及抵消了原料成本波動和監管審查的影響。住宅維修繼續支撐著銷量,而隨著辦公室、醫療機構和住宿設施優先考慮感染控制、隔音效果和低維護成本,商用級PVC地板的需求也在復甦。

在美國國內,製造商正利用對中國產品徵收關稅的機會,提升本地生產能力並縮短前置作業時間,從而在全球供應鏈中斷的情況下,進一步增強美國PVC地板材料市場的競爭力。與聯邦災害緩解計畫相關的緊急資金,加上消費者對防水地板材料的需求,正在推動石塑複合材料(SPC)和木塑複合材料(WPC)產品的銷售成長。數位印刷技術和卡扣系統的不斷改進,提升了地板的美觀度並縮短了安裝時間,促進了專業通路和DIY通路的普及。這確保了美國PVC地板材料市場能夠持續滿足不斷變化的終端用戶需求。

美國乙烯基複合地板材料市場趨勢與洞察

住宅翻新需求加速成長

預計到2025年,美國房屋翻新總支出將達到5,090億美元,較2024年成長1.22%,仍比疫情前水準高出50%。平均房齡44年的老舊住宅對兼具美觀和易於安裝的地板材料需求持續成長。乙烯基(PVC)地板材料滿足了注重預算的住宅的需求,它擁有與實木地板相似的外觀,安裝成本卻比實木地板低40%至60%,而且無需像瓷磚那樣進行勾縫維護。不斷上漲的房價推動了住宅淨值貸款的增加,刺激了自由裁量權的維修支出,從而促進了美國乙烯基(PVC)地板材料市場的發展。老年家庭是目前房屋翻新支出最大的群體,他們越來越傾向於選擇易於維護的地板材料,進一步推動了這個成長要素。不同種族家庭參與房屋翻新活動的增加,拓寬了人們的風格偏好,並促使大型零售商的產品種類(庫存單位)不斷增加。儘管出現了競爭性的覆膜產品,但印刷精度和壓紋精度的持續創新將有助於乙烯基材料保持其受歡迎程度,預計這種成長勢頭至少會持續到 2020 年代中期。

剛性芯材(SPC/WPC)技術的應用日益廣泛

Rigid Core產品線已在豪華乙烯基瓷磚市場佔據63%的市場佔有率,而SPC產品憑藉其低調的設計和低成本優勢,正在不斷擴大市場佔有率。尺寸穩定性使得建築商能夠在傳統上以捲材為主的區域,例如地下室、浴室和人流量大的大廳等潮濕環境,指定使用乙烯基產品。卡扣式鎖扣技術縮短了安裝時間,即使在技術純熟勞工持續短缺的情況下,也能幫助計劃按時完成。 Mohawk公司正在增設一條自動化SPC生產線,並計劃在未來幾年內投入9億美元,以維持其19%的市佔率領先地位。 Shaw公司正在升級位於卡爾霍恩的工廠,以生產WPC產品,擴大國內產能並降低關稅風險。建築規範中關於防水性能的要求從表面水測試改為“安裝後防水性能”,這增強了SPC產品的價值提案,並促進了高密度石灰石芯材的研發。這些因素共同作用,將鞏固Rigid Core產品在2030年後美國乙烯基地板材料市場的主導地位。

加強對鄰苯二甲酸酯和全氟烷基物質的監管。

美國環保署 (EPA) 的 DINP 評估草案得出結論,兒童接觸乙烯基塑膠地板材料粉塵構成不合理的風險,並已啟動公眾意見徵詢期,建議未來收緊監管。同時,《綜合環境反應、賠償和責任法》(CERCLA) 將全氟烷基和多氟烷基物質 (PFAS) 列入有害物質清單,增加了使用含氟加工助劑的製造商的法律責任風險。合規措施促使人們開發出不含聚氯乙烯 (PVC) 的彈性體,例如 Schau 公司的 EcoWorx Resilient,該產品符合「從搖籃到搖籃」鉑金標準,並榮獲 2025 年愛迪生獎。配方調整成本和產品停產的可能性正在擠壓毛利率,尤其是對於那些規模小規模、無法承擔測試成本的製造商。加州和華盛頓州的產品資訊揭露要求使標籤標註更加複雜,並延長了新產品商店的時間。零售買家提出的額外供應鏈問卷調查也導致採購決策延遲,並暫時減緩了計劃進度。儘管對替代化學技術的投資未來可能會帶來溢價,但美國乙烯基地板材料市場在短期內仍將持續放緩。

細分市場分析

預計到2025年,豪華乙烯基瓷磚(LVT)將佔據美國乙烯基地板材料市場67.62%的佔有率,並在2031年之前以8.64%的複合年成長率成長,成為規模最大且成長最快的產品線。由於其主導地位,在整個預測期內,美國乙烯基地板材料市場的規模將繼續高度依賴LVT的性能指標。 SPC(超聚苯乙烯複合材料)結構減少了基材微小不規則性造成的透光現象,使其在租賃物業的維修中得到更廣泛的應用,因為長時間的停工是不可接受的。 WPC(木塑複合材料)因其吸音性能和柔軟的觸感,在住宅生活空間中仍然很受歡迎,通常採用軟木或IXPE背襯,從而提高了聲學性能。捲材乙烯基在醫療保健和教育場所的室內裝飾中保持著需求,焊接接縫有助於無菌清潔程序。然而,黏合劑技術的進步正在推動市場佔有率轉移到焊接LVT板材。儘管乙烯基複合地磚(VCT)因其低成本而在工業設施中仍佔有一席之地,但日益繁重的維護工作正促使人們轉向免打蠟的LVT地磚,後者可最大限度地減少地面維護工作。數位裝飾層在不顯著增加重量的情況下增加了地磚的複雜性,即使在燃油價格上漲時期,也能保持運輸效率並控制到岸成本。

儘管產品組合發生了顯著變化,但整體產能擴張仍採取謹慎策略,以避免供應過剩。國內工廠正逐步調整運作計劃,根據提前六個月確定的自有品牌產品陳列圖進行生產。這項策略維持了美國乙烯基複合地板材料市場良好的工廠使用率和價格紀律。供應商提供的硬質和軟質同步裝飾托盤,使零售商能夠銷售配套產品組合,從而促進多房間計劃的實施。從歐洲引進的連續壓制技術,實現了媲美實木的深度壓紋效果,開闢了高階市場,在不影響產品價值認知的前提下,提高了平均售價。

到2025年,互鎖地板材料將佔出貨量的53.65%,這印證了消費者對無需黏合劑、方便週末自行安裝的地板計劃的偏好。黏合式地磚雖然市場佔有率較小,但正以7.62%的複合年成長率成長,因為醫療機構、超市和辦公室等終端用戶對在集中荷載下耐用性的需求日益成長。預計到2026年,美國黏合式乙烯基地板材料市場規模將達到44.1億美元,反映出商業建築的穩定需求。自黏式地板捲材受到注重價格的房東的青睞,他們希望在租戶更迭時無需聘請專業安裝人員即可更換地板。混合型解決方案結合了緊密的互鎖結構和周邊剝離式黏合劑,以減少高人流量走廊的橫向剪切力。

互鎖技術的進步取決於精確的加工公差。 SPC芯材最大限度地減少了膨脹,即使在美國常見的濕度波動下也能保持鎖扣的完整性。零售商建議使用與相同凹槽相符的裝飾條,從而簡化配件SKU的複雜性。商業安裝人員使用塗膠滾筒在過渡區域塗抹互鎖地板的黏合劑,既保證了現場安裝速度,也確保了地板的耐用性。領先製造商提供的培訓模組使安裝人員能夠在不到兩小時內獲得認證。在人手不足的情況下,這是一個關鍵的賣點,也是推動美國乙烯基複合地板材料市場普及的催化劑。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 住宅裝修需求快速成長

- 剛性芯材(SPC/WPC)技術的應用日益廣泛

- 與實木地板和瓷磚相比,價格更具競爭力

- 多用戶住宅數迅速增加

- 聯邦緊急事務管理局(FEMA)資助的災害易發州對抗災地板材料的需求

- 零售商自有品牌擴張推動 SKU周轉率

- 市場限制

- 加強對鄰苯二甲酸酯和全氟烷基物質的監管審查

- PVC樹脂價格的波動與石油和天然氣價格的波動有關。

- 掩埋成本不斷上漲,給最終廢棄物處理帶來了壓力。

- 墨西哥灣沿岸停產後,國內氯氣供應網緊張。

- 產業價值鏈分析

- 波特五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 洞察市場最新趨勢與創新

- 深入了解市場近期發展動態(新產品發表、策略性舉措、投資、合作、合資、擴張、併購等)

第5章 市場規模及成長預測(金額:美元)

- 依產品類型

- 豪華乙烯基瓷磚(LVT)

- 石塑複合材料(SPC)

- 木塑複合材料(WPC)

- 豪華乙烯基木地板(LVP)

- 乙烯基片材

- 其他(乙烯基複合地磚(VCT)、彈性乙烯基背襯橡膠混合材料)

- 豪華乙烯基瓷磚(LVT)

- 透過施工方法

- 自黏乙烯基瓷磚

- 黏合劑類型

- 互鎖式乙烯基瓷磚

- 其他

- 最終用戶

- 住宅

- 商業的

- 飯店及休閒

- 零售和購物中心

- 醫療設施

- 教育

- 總公司

- 公共和政府設施

- 其他商業用戶

- 依建築類型

- 新建工程

- 重建和維修

- 透過分銷管道

- B2C/零售

- 家居建材商店

- 專業地板商店

- 線上

- 其他分銷管道

- B2B/承包商/建築商

- B2C/零售

- 按地區

- 東北

- 中西部

- 東南

- 西南

- 西方

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Mohawk Industries

- Shaw Industries

- Armstrong Flooring

- Tarkett North America

- Mannington Mills

- Gerflor USA

- Karndean Designflooring

- The Dixie Group

- CFL Flooring

- Novalis Innovative Flooring

- Interface Inc.

- LG Hausys America

- Congoleum

- Roppe Corporation

- Forbo Flooring Systems

- Stonhard

- Parterre Flooring Systems

- Polyflor Ltd.

- Metroflor

- Halstead New England(LifeProof)

第7章 市場機會與未來展望

The US vinyl floor covering market is expected to grow from USD 12.57 billion in 2025 to USD 13.47 billion in 2026 and is forecast to reach USD 19.01 billion by 2031 at 7.12% CAGR over 2026-2031.

Strong Remodeling spending sustained multi-family completions, and rapid adoption of rigid-core technologies counterbalance input-cost volatility and regulatory scrutiny, keeping the US vinyl floor covering market on a firmly expansionary trajectory. Residential renovations continue to underpin volume, while commercial specification rebounds as offices, healthcare facilities, and hospitality venues prioritize infection control, acoustic comfort, and lower maintenance costs.

Domestic producers leverage tariffs on Chinese imports, boosting local capacity and shortening lead times, which further fortifies the competitive stance of the US vinyl floor covering market amid global supply disruptions. Resilience funding tied to federal hazard-mitigation programs, together with consumer demand for waterproof flooring, amplifies sales of Stone Plastic Composite (SPC) and Wood Plastic Composite (WPC) formats. Ongoing technological improvements in digital printing and click-lock systems enhance aesthetics, reduce installation time, and spur broader acceptance across both professional and do-it-yourself channels, ensuring that the US vinyl floor covering market remains responsive to evolving end-user expectations.

US Vinyl Floor Covering Market Trends and Insights

Accelerated Residential Remodeling Boom

The remodeling expenditure pool touched USD 509.0 billion in 2025, 1.22% higher than 2024, and outlays remain 50% above pre-pandemic benchmarks. Aging homes with a median age of 44 years sustain demand for floor upgrades that combine aesthetics and ease of installation. Vinyl formats satisfy budget-conscious homeowners by offering hardwood visuals at 40-60% lower installed cost while avoiding grout maintenance common to ceramic tiles. Rising property values enhance home-equity borrowing capacity, encouraging discretionary renovation spending that lifts the US vinyl floor covering market. Older householders, now the largest spenders on remodeling, gravitate toward low-maintenance surfaces, reinforcing this driver. Elevated participation of racially diverse households in renovation activity widens style preference ranges, adding tailwinds for SKU proliferation across big-box assortments. Continuous innovation in print fidelity and embossed-in-register textures helps vinyl maintain mindshare despite competing laminate launches, ensuring momentum through at least mid-decade.

Growing Adoption of Rigid-Core (SPC/WPC) Technologies

Rigid-core lines reached 63% penetration within Luxury Vinyl Tile, with SPC commanding incremental share because of a thinner profile and lower material cost. Dimensional stability lets builders specify vinyl in moisture-exposed basements, bathrooms, and high-traffic lobbies where sheet goods once dominated. Click-lock formats cut labor hours, meeting project schedules amid ongoing skilled-labor shortages. Mohawk's USD 900.0 million multi-year capex adds automated SPC lines that help the company defend its 19% leadership share. Shaw upgrades Calhoun facilities for WPC production, widening domestic capacity and lowering tariff exposure. Building-code wording on in-place water resistance, rather than topical spill testing, strengthens SPC's value proposition and funnels R&D toward higher-density limestone cores. Together, these forces guarantee rigid-core dominance in the US vinyl floor covering market well beyond 2030.

Increasing Regulatory Scrutiny on Phthalates & PFAS

EPA's draft DINP evaluation concludes unreasonable risk to children from vinyl flooring dust exposure, prompting public-comment rounds that signal future restrictions. Parallel PFAS designations under CERCLA widen liability exposure for manufacturers using fluorinated processing aids. Compliance drives R&D into PVC-free elastomers such as Shaw's EcoWorx Resilient, which met Cradle-to-Cradle Platinum criteria and captured the 2025 Edison Award. Re-formulation costs and potential product delistings compress gross margins, especially for small producers lacking scale to spread testing expense. Product-disclosure mandates in California and Washington increase labeling complexity, lengthening time-to-shelf for new lines. Retail buyers add supply-chain questionnaires that can delay award decisions, temporarily slowing project pipelines. Over time, investment in alternative chemistries may unlock premium pricing, but near-term drag persists on the US vinyl floor covering market.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Multi-Family Housing Completions

- FEMA-Funded Resilient-Flooring Demand in Disaster-Prone States

- Volatile PVC Resin Prices Linked to Oil & Gas Swings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Luxury Vinyl Tile held 67.62% of US vinyl floor covering market share in 2025, and the segment is tracking an 8.64% CAGR to 2031, underscoring its status as both the largest and fastest-expanding product line. This dominance ensures that the US vinyl floor covering market size remains anchored in LVT performance metrics over the forecast horizon. SPC compositions reduce telegraphing over minor subfloor irregularities, widening retrofit use cases in rental units that cannot tolerate extended downtime. WPC remains popular in single-family living areas for its softer underfoot feel, absorbing footfall noise with cork or IXPE backers that enhance acoustic ratings. Sheet vinyl still claims pockets of medical and education interiors where welded seams support sterile cleaning regimes, though incremental shares migrate toward welded LVT planks as adhesive chemistries improve. Vinyl Composition Tile (VCT) defends industrial installations through low material cost yet rising maintenance favors migration to no-wax LVT that minimizes floor-care labor. Digital decor layers add complexity without meaningfully raising unit weight, enabling freight efficiency that protects landed cost even during fuel-price spikes.

Although product-mix evolution is pronounced, overall capacity additions proceed cautiously to avoid oversupply. Domestic mills stagger commissioning schedules, aligning runs with private-label planograms secured six months ahead. The strategy maintains healthy mill utilization, preserving price discipline in the US vinyl floor covering market. As suppliers synchronize decor palettes across rigid and flexible formats, retailers can bundle coordinated offerings, stimulating multi-room projects. Continuous-press technology imports from Europe promise deeper embossing registers that rival real wood, opening premium niches that lift average selling prices without detracting from value perceptions.

Interlocking planks represented 53.65% of shipments in 2025, validating consumer preference for adhesive-free methodologies that facilitate weekend projects. Glue-down tiles, while a smaller slice, are growing at 7.62% CAGR because healthcare, grocery, and office end-users demand permanence under heavy point loads. The US vinyl floor covering market size for glue-down formats equaled USD 4.41 billion in 2026, reflecting steady commercial pull. Self-adhesive sheets serve price-sensitive landlords who replace floors between tenants without hiring certified installers. Hybrid solutions combine tight-fit tongue-and-groove engagement with peel-film tackifiers at perimeter courses, mitigating lateral shear in rolling-load corridors.

Interlocking advances hinge on precision milling tolerances; SPC cores show minimal expansion, holding lock integrity across humidity swings common in U.S. climates. Retailers promote coordinating moldings that click into the same groove, reducing accessory SKU complexity. Commercial installers leverage adhesive rollers to back-butter interlocking planks in transition zones, ensuring long service life without losing speed advantages in field areas. Training modules from leading manufacturers certify installers in under two hours, a key selling point during labor-short conditions and a catalyst for wider adoption throughout the US vinyl floor covering market.

The US Vinyl Floor Covering Market Report is Segmented by Product Type (LVT, Luxury Vinyl Plank, and More), Installation Method (Self-Adhesive Vinyl Tiles, Glue-Down, and More), End User (Residential, Commercial), Construction Type (New Construction, Remodeling / Retrofit), Distribution Channel (B2C/Retail, B2B/Contractors), and Geography (Northeast, Midwest, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Mohawk Industries

- Shaw Industries

- Armstrong Flooring

- Tarkett North America

- Mannington Mills

- Gerflor USA

- Karndean Designflooring

- The Dixie Group

- CFL Flooring

- Novalis Innovative Flooring

- Interface Inc.

- LG Hausys America

- Congoleum

- Roppe Corporation

- Forbo Flooring Systems

- Stonhard

- Parterre Flooring Systems

- Polyflor Ltd.

- Metroflor

- Halstead New England (LifeProof)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated residential remodeling boom

- 4.2.2 Growing adoption of rigid-core (SPC/WPC) technologies

- 4.2.3 Cost-competitiveness versus hardwood and ceramic tiles

- 4.2.4 Surge in multi-family housing completions

- 4.2.5 FEMA-funded resilient-flooring demand in disaster-prone states

- 4.2.6 Retailers' private-label expansion boosting SKU velocity

- 4.3 Market Restraints

- 4.3.1 Increasing regulatory scrutiny on phthalates and PFAS

- 4.3.2 Volatile PVC resin prices linked to oil and gas swings

- 4.3.3 Growing landfill fees pressuring end-of-life disposal

- 4.3.4 Tight domestic chlorine supply chain after Gulf-Coast outages

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product Type

- 5.1.1 Luxury Vinyl Tile (LVT)

- 5.1.1.1 Stone Plastic Composite (SPC)

- 5.1.1.2 Wood Plastic Composite (WPC)

- 5.1.2 Luxury Vinyl Plank (LVP)

- 5.1.3 Sheet Vinyl

- 5.1.4 Others (Vinyl Composition Tile (VCT), Resilient Vinyl-Backed Rubber Hybrid)

- 5.1.1 Luxury Vinyl Tile (LVT)

- 5.2 By Installation Method

- 5.2.1 Self-Adhesive Vinyl Tiles

- 5.2.2 Glue-Down

- 5.2.3 Interlocking Vinyl Tiles

- 5.2.4 Others

- 5.3 By End User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.2.1 Hospitality and Leisure

- 5.3.2.2 Retail and Shopping Centers

- 5.3.2.3 Healthcare Facilities

- 5.3.2.4 Education

- 5.3.2.5 Corporate Offices

- 5.3.2.6 Public and Government Buildings

- 5.3.2.7 Other Commercial Users

- 5.4 By Construction Type

- 5.4.1 New Construction

- 5.4.2 Remodeling/Retrofit

- 5.5 By Distribution Channel

- 5.5.1 B2C/Retail

- 5.5.1.1 Home Centers

- 5.5.1.2 Specialty Flooring Stores

- 5.5.1.3 Online

- 5.5.1.4 Other Distribution Channels

- 5.5.2 B2B/Contractors/Builders

- 5.5.1 B2C/Retail

- 5.6 By Geography

- 5.6.1 Northeast

- 5.6.2 Midwest

- 5.6.3 Southeast

- 5.6.4 Southwest

- 5.6.5 West

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Mohawk Industries

- 6.4.2 Shaw Industries

- 6.4.3 Armstrong Flooring

- 6.4.4 Tarkett North America

- 6.4.5 Mannington Mills

- 6.4.6 Gerflor USA

- 6.4.7 Karndean Designflooring

- 6.4.8 The Dixie Group

- 6.4.9 CFL Flooring

- 6.4.10 Novalis Innovative Flooring

- 6.4.11 Interface Inc.

- 6.4.12 LG Hausys America

- 6.4.13 Congoleum

- 6.4.14 Roppe Corporation

- 6.4.15 Forbo Flooring Systems

- 6.4.16 Stonhard

- 6.4.17 Parterre Flooring Systems

- 6.4.18 Polyflor Ltd.

- 6.4.19 Metroflor

- 6.4.20 Halstead New England (LifeProof)

7 Market Opportunities and Future Outlook

- 7.1 Increasing focus on sustainability, circularity and take-back/recycling programs

- 7.2 Surging demand for realistic visuals, textures, and customization

乙烯基複合地板材料市場:按產品類型、安裝方式、耐磨層厚度、應用和分銷管道分類-全球預測,2026-2032年

乙烯基複合地板材料市場:按產品類型、安裝方式、耐磨層厚度、應用和分銷管道分類-全球預測,2026-2032年 乙烯基複合地板材料市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場分類(2026-2033 年)

乙烯基複合地板材料市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場分類(2026-2033 年) 乙烯基地板材料市場-全球產業規模、佔有率、趨勢、機會、預測:按產品、應用、區域和競爭對手分類,2021-2031年

乙烯基地板材料市場-全球產業規模、佔有率、趨勢、機會、預測:按產品、應用、區域和競爭對手分類,2021-2031年 乙烯基複合地板材料市場規模、佔有率、趨勢和預測:按產品類型、產業和地區分類,2026-2034年

乙烯基複合地板材料市場規模、佔有率、趨勢和預測:按產品類型、產業和地區分類,2026-2034年 2026年全球PVC地板材料市場報告

2026年全球PVC地板材料市場報告 全球乙烯基地板材料市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球乙烯基地板材料市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2035年PVC地板材料市場分析及預測:類型、產品類型、應用、技術、安裝方式、材質類型、最終用戶、功能、解決方案

2035年PVC地板材料市場分析及預測:類型、產品類型、應用、技術、安裝方式、材質類型、最終用戶、功能、解決方案 乙烯基複合地板材料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本PVC地板材料市場規模、佔有率、趨勢和預測:按產品類型、行業和地區分類,2026-2034年

乙烯基複合地板材料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本PVC地板材料市場規模、佔有率、趨勢和預測:按產品類型、行業和地區分類,2026-2034年 2025-2029年全球抗衝擊PVC地板材料市場

2025-2029年全球抗衝擊PVC地板材料市場