|

市場調查報告書

商品編碼

1940629

美國塑膠瓶蓋和封蓋:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)United States (US) Plastic Caps And Closures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

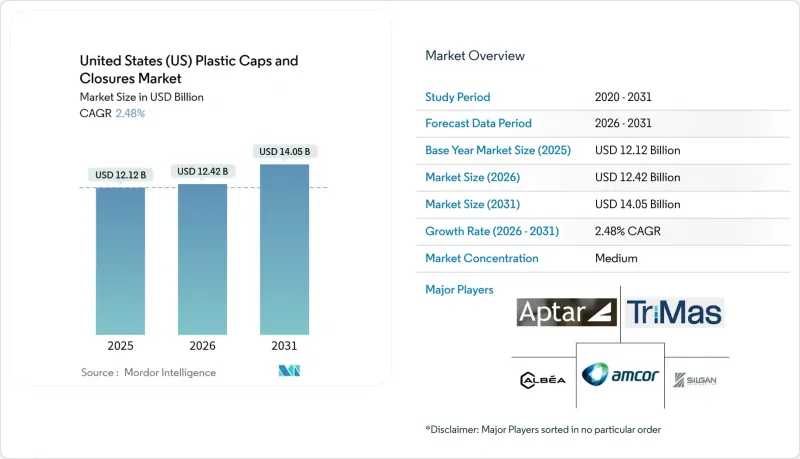

預計到 2025 年,美國塑膠瓶蓋和封蓋市場價值將達到 121.2 億美元,從 2026 年的 124.2 億美元成長到 2031 年的 140.5 億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 2.48%。

這種緩慢的成長速度是多種因素共同作用的結果,包括監管合規成本、樹脂價格波動以及飲料、醫藥和電商包裝行業需求的激增。有關紮帶蓋的法規、更嚴格的兒童安全標準以及品牌對NFC認證技術日益成長的興趣,都在推動對材料選擇和製造方法的重新評估。儘管聚丙烯(PP)憑藉其低成本和優異的阻隔性能保持著主導地位,但隨著品牌追求輕量化和循環利用的目標,聚對苯二甲酸乙二醇酯(PET)的市場佔有率正在不斷成長。能夠將經濟高效的射出成型與優質智慧封蓋技術相結合的製造商,最有可能在美國塑膠瓶蓋和封蓋市場抓住新的機會。

美國塑膠瓶蓋及封蓋市場趨勢及洞察

對便利包裝飲料的需求激增

受便利消費習慣和功能性補水產品推出的推動,市場對配備易開可重複密封瓶蓋的單份寶特瓶的需求持續成長。飲料填充商擴大指定使用與運動瓶蓋和翻蓋式瓶蓋相容的瓶蓋,以便單手操作,同時符合21 CFR S211.132防篡改法規。品牌擁有者正在瓶蓋上整合NFC標籤和QR碼,以促進售後互動和忠誠度計畫,並將瓶蓋作為數位媒體的載體。隨著高階水、能量飲料和即飲咖啡佔據貨架主導地位,瓶蓋製造商看到了銷售增值產品的商機,例如吸氧內襯、整合式吸嘴和顏色匹配的表面處理,這些都能強化品牌形象。美國塑膠瓶蓋市場正受益於這些需求,因為增值設計彌補了碳酸飲料銷售成長緩慢的影響。

不斷擴大的藥品包裝要求

隨著人口老化和處方藥治療的普及,對符合美國消費品安全委員會 (CPSC) 扭力和推拉測試標準的兒童安全型、老年人友善瓶蓋的需求日益成長。醫院和藥房在部署自動配藥櫃時,需要高度一致的扭矩範圍和內襯完整性,以防止劑量錯誤。合法的大麻產品(目前在24個州被列為管制藥品)必須符合防中毒包裝標準,這為經認證的可重複密封系統創造了一個高價值的細分市場。整合微型感測器和時間戳功能的智慧瓶蓋有助於追蹤治療依從性並提醒潛在的誤用情況,這為專業加工商在醫療保健技術領域的合作創造了機會。

樹脂價格波動

集中在墨西哥灣沿岸的聚烯原料易受颶風和裂解裝置意外停產的影響,這可能導致聚丙烯 (PP) 和聚乙烯 (PE) 現貨價格在幾週內上漲 30% 至 50%。瓶蓋製造商不願將附加費轉嫁給消費者,這在價格飆升期間擠壓了利潤空間,並抑制了對新模具的投資。雖然一些加工商使用期貨合約對沖樹脂採購風險,但價格波動仍然使依賴固定價格指數的長期飲料供應協議變得複雜。儘管計劃於 2026 年至 2027 年運作的新頁岩氣裂解裝置有望提高產能,但短期風險狀況促使企業採取更薄型化和多元化的籌資策略。

細分市場分析

聚丙烯(PP)因其化學穩定性好且與高速射出成型線相容,在美國塑膠瓶蓋和封蓋市場佔據41.12%的佔有率。隨著飲料灌裝商普遍採用輕質螺旋蓋,預計該細分市場將維持個位數低成長;而家用化學品產業則因其耐溶劑性而繼續青睞PP翻蓋。聚對苯二甲酸乙二醇酯(PET)雖然仍處於個位數中成長水平,但由於其低密度且與瓶蓋回收工藝兼容,預計到2031年將以3.45%的複合年成長率快速成長。 Origin Materials公司推出的新型熱成型製程進一步強化了這一優勢,該工藝可縮短生產週期並減少廢棄物。

除了前兩大材料之外,高密度聚苯乙烯(HDPE) 是需要抗穿刺性和兒童安全扭矩範圍的藥品管瓶的首選材料,永續性。這些趨勢共同推動了加工商和壓力樹脂供應商可選擇的材料範圍,使他們不僅能夠在價格上脫穎而出,還能在對循環經濟的承諾上展現差異化優勢。

到2025年,飲料業將占美國塑膠瓶蓋和封蓋市場的30.05%,這主要得益於瓶裝水和碳酸飲料補充裝的強勁需求。然而,隨著碳酸飲料市場日趨成熟,預計成長速度將放緩,而機能飲料飲料和運動飲料正在向利潤更高的運動型瓶蓋轉型。同時,受處方藥銷售成長以及各州大麻市場新增需要符合兒童安全/老年人安全認證標準的SKU的推動,藥品瓶蓋將以4.79%的複合年成長率成長。儘管醫院擴大採用單劑量泡殼包裝,但靜脈輸液瓶和口服懸浮液的瓶蓋仍然佔據主導地位,即使一些治療方法正在轉向使用藥袋和注射筆,其潛在需求依然存在。

食品業在電子商務市場的推動下,持續保持穩定成長,而電子商務市場對防篡改和防漏性能的要求也日益提高。化妝品和盥洗用品產業則憑藉其高階瓶蓋、金屬飾面和品牌配色等特性,開闢了一個雖小但盈利的細分市場。家用化學品產業對安全密封和劑量精準度的重視,再次凸顯了堅固的內襯系統和扭力控制的重要性。這些因素共同表明,成功的供應商並非過度依賴飲料市場的需求,而是會根據多個成長領域的需求,客製化其瓶蓋產品組合。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 包裝便利飲料的需求激增

- 不斷擴大的藥品包裝要求

- 從金屬帽換成輕質塑膠帽

- 電子商務的發展需要防篡改設計。

- 採用與約束條件掛鉤的上限規定

- 利用高速壓縮成型能力實現回流

- 市場限制

- 樹脂價格波動

- 來自永續替代品的競爭

- 預計聯邦政府將對一次性塑膠製品進行監管

- 人們對微塑膠問題的關注正在推動無內襯瓶蓋的普及。

- 產業價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 宏觀經濟因素如何影響市場

第5章 市場規模與成長預測

- 材料

- 聚對苯二甲酸乙二醇酯(PET)

- 聚丙烯(PP)

- 低密度聚乙烯(LDPE)

- 高密度聚苯乙烯(HDPE)

- 其他材料

- 按最終用戶行業分類

- 飲料

- 食物

- 製藥和醫療保健

- 化妝品和盥洗用品

- 家用化學品

- 其他終端用戶產業

- 按帽型

- 螺帽

- 繫繩帽

- 翻蓋式和按扣式瓶蓋

- 兒童安全帽

- 豪華/高級裝飾帽

- 分配蓋

- 透過製造技術

- 射出成型

- 壓縮成型

- 三件式在線連續組裝

- 數位印刷智慧帽

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Silgan Holdings Inc.

- AptarGroup, Inc.

- Amcor plc

- Albea SA

- TriMas Corporation

- Tetra Pak International SA

- Guala Closures SpA

- MJS Packaging, Inc.

- O. Berk Company, LLC

- Closure Systems International, Inc.

- BERICAP GmbH & Co. KG

- Crown Holdings, Inc.

- Evergreen Packaging LLC

- Phoenix Closures, Inc.

- Portola Packaging, Inc.

- Plastipak Packaging, Inc.

- Mold-Rite Plastics, LLC

- Smurfit WestRock

- SIG Combibloc Group AG

第7章 市場機會與未來展望

The United States plastic caps and closures market was valued at USD 12.12 billion in 2025 and estimated to grow from USD 12.42 billion in 2026 to reach USD 14.05 billion by 2031, at a CAGR of 2.48% during the forecast period (2026-2031).

This measured pace reflects a mix of regulatory compliance costs, resin price swings, and surging demand from beverages, pharmaceuticals, and e-commerce packaging. Legislation on tethered caps, stricter child-resistant rules, and brand interest in NFC-enabled authentication are reshaping material choices and production methods. Polypropylene (PP) retains a dominant footprint due to its low cost and strong barrier performance, while polyethylene terephthalate (PET) is gaining share as brands pursue lightweighting and circularity objectives. Manufacturers that combine cost-efficient injection molding with premium smart-closure features are best positioned to capture emerging opportunities in the United States plastic caps and closures market.

United States (US) Plastic Caps And Closures Market Trends and Insights

Surge in Demand for Convenient Packaged Beverages

On-the-go consumption habits and functional hydration launches continue to pull volume through single-serve PET bottles fitted with easy-open, resealable tops. Beverage fillers increasingly specify closures compatible with sports caps and flip-top formats that support one-handed operation while complying with 21 CFR S211.132 tamper-evident rules. Brand owners are pairing NFC tags and QR codes on caps to drive post-purchase engagement and loyalty programs, turning closures into a digital media surface. As premium water, energy drinks, and ready-to-drink coffee command shelf space, closure makers gain opportunities to upsell oxygen-scavenging liners, integrated spouts, and color-matched finishes that reinforce brand identity. The United States plastic caps and closures market benefits from these requirements because value-added designs offset modest volume growth in carbonated soft drinks.

Expanding Pharmaceutical Packaging Requirements

An aging population and wider access to prescription therapies elevate demand for child-resistant, senior-friendly caps that pass Consumer Product Safety Commission torque and push-turn protocols. Hospitals and pharmacies rolling out automated dispensing cabinets also require highly consistent torque ranges and liner integrity to prevent dosage errors. Legal cannabis products-now regulated as controlled substances in 24 states-must meet poison-prevention packaging standards, spawning a premium niche for certified reclosable systems. Smart closures embedding micro-sensors or time-stamp features help track therapy adherence and flag potential misuse, giving specialty converters an entry point into health-tech partnerships.

Volatility in Resin Prices

Polyolefin feedstocks clustered along the Gulf Coast remain vulnerable to hurricanes and unplanned cracker outages that can lift spot PP and PE prices by 30-50% within weeks. Closure makers pass through surcharges with a lag, compressing margins and curbing investment in new tooling during spikes. Some converters hedge resin purchases via futures contracts, yet volatility still complicates long-term beverage supply agreements that favor fixed-price indexation. While new shale-gas crackers slated for 2026-2027 promise incremental capacity, the near-term risk profile encourages leaner inventories and multiple-sourcing strategies.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Lightweight Plastic Over Metal Closures

- Growth of E-commerce Requiring Tamper-Evident Designs

- Competition from Sustainable Alternative Materials

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polypropylene commands 41.12% share of the United States plastic caps and closures market, anchored by its chemical stability and suitability for high-speed injection molding lines. The segment is expected to post low-single-digit growth as beverage fillers standardize lightweight screw tops and household chemicals continue to favor PP flip caps for solvent resistance. PET, while only a mid-single-digit share contributor, is forecast as the fastest-growing at a 3.45% CAGR through 2031 thanks to its low density and compatibility with bottle-to-cap recycling streams, an advantage amplified by Origin Materials' novel thermoforming route that lowers cycle time and waste.

Moving beyond the top two, high-density polyethylene remains the material of choice for pharmaceutical vials that demand puncture resistance and child-safe torque ranges, whereas low-density polyethylene is preferred in dispensing nozzles for condiments and personal-care creams. Specialty bio-polymers, though under 2% share, gain traction where brand sustainability mandates override cost. Collectively, these dynamics widen the material toolbox available to converters and force resin suppliers to differentiate on circularity credentials, not just price.

Beverages accounted for 30.05% of the United States plastic caps and closures market size in 2025 due to vast bottled-water volumes and carbonated soft drink refills. Growth, however, moderates as carbonated segments mature, while functional beverages and sports drinks shift toward higher-margin sports caps. Pharmaceutical closures, in contrast, will grow 4.79% annually as prescription drug volumes climb and state cannabis markets add SKUs that mandate certified child-resistant or senior-friendly designs. Hospitals converting to unit-dose blister packs still rely on closure-sealed infusion bottles and oral suspensions, sustaining baseline demand even as some therapies migrate to pouches or pens.

Food products maintain a stable trajectory, helped by e-commerce adoption, which places a premium on tamper-evident and leak-proof attributes. Cosmetics and toiletries reach for premium overcaps, metallized finishes, and color harmony with brand palettes, making them a lucrative niche despite modest volumes. Household chemicals emphasize safety seals and dosing accuracy, reinforcing the importance of robust liner systems and torque control. Together, the mix underscores why successful suppliers tailor closure portfolios to multiple growth vectors instead of over-relying on beverage volumes.

The United States Plastic Caps and Closures Market Report is Segmented by Material (PET, PP, LDPE, and More), End-User Industry (Beverage, Food, Pharmaceutical and Healthcare, and More), Cap Type (Screw Closures, Tethered Caps, and More), and Manufacturing Technology (Injection Molding, Compression Molding, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Silgan Holdings Inc.

- AptarGroup, Inc.

- Amcor plc

- Albea S.A.

- TriMas Corporation

- Tetra Pak International S.A.

- Guala Closures S.p.A.

- MJS Packaging, Inc.

- O. Berk Company, LLC

- Closure Systems International, Inc.

- BERICAP GmbH & Co. KG

- Crown Holdings, Inc.

- Evergreen Packaging LLC

- Phoenix Closures, Inc.

- Portola Packaging, Inc.

- Plastipak Packaging, Inc.

- Mold-Rite Plastics, LLC

- Smurfit WestRock

- SIG Combibloc Group AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in demand for convenient packaged beverages

- 4.2.2 Expanding pharmaceutical packaging requirements

- 4.2.3 Shift toward lightweight plastic over metal closures

- 4.2.4 Growth of e-commerce requiring tamper-evident designs

- 4.2.5 Adoption of tethered cap legislation

- 4.2.6 Reshoring via high-speed compression-molding capacity

- 4.3 Market Restraints

- 4.3.1 Volatility in resin prices

- 4.3.2 Competition from sustainable alternative materials

- 4.3.3 Prospective federal single-use-plastic restrictions

- 4.3.4 Micro-plastic scrutiny driving liner-less closures

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Degree of Competition

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Polyethylene Terephthalate (PET)

- 5.1.2 Polypropylene (PP)

- 5.1.3 Low Density Polyethylene (LDPE)

- 5.1.4 High-Density Polyethylene (HDPE)

- 5.1.5 Other Materials

- 5.2 By End-user Industry

- 5.2.1 Beverage

- 5.2.2 Food

- 5.2.3 Pharmaceutical and Healthcare

- 5.2.4 Cosmetics and Toiletries

- 5.2.5 Household Chemicals

- 5.2.6 Other End-user industries

- 5.3 By Cap Type

- 5.3.1 Screw Closures

- 5.3.2 Tethered Caps

- 5.3.3 Flip-top and Snap-on Caps

- 5.3.4 Child-resistant Closures

- 5.3.5 Luxury/Premium Decorative Closures

- 5.3.6 Dispensing Caps

- 5.4 By Manufacturing Technology

- 5.4.1 Injection Molding

- 5.4.2 Compression Molding

- 5.4.3 3-Piece and In-line Assembly

- 5.4.4 Digitally Printed Smart Closures

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Silgan Holdings Inc.

- 6.4.2 AptarGroup, Inc.

- 6.4.3 Amcor plc

- 6.4.4 Albea S.A.

- 6.4.5 TriMas Corporation

- 6.4.6 Tetra Pak International S.A.

- 6.4.7 Guala Closures S.p.A.

- 6.4.8 MJS Packaging, Inc.

- 6.4.9 O. Berk Company, LLC

- 6.4.10 Closure Systems International, Inc.

- 6.4.11 BERICAP GmbH & Co. KG

- 6.4.12 Crown Holdings, Inc.

- 6.4.13 Evergreen Packaging LLC

- 6.4.14 Phoenix Closures, Inc.

- 6.4.15 Portola Packaging, Inc.

- 6.4.16 Plastipak Packaging, Inc.

- 6.4.17 Mold-Rite Plastics, LLC

- 6.4.18 Smurfit WestRock

- 6.4.19 SIG Combibloc Group AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

塑膠瓶蓋及瓶蓋市場報告:按產品類型、原料、容器類型、技術、最終用途和地區分類(2026-2034 年)

塑膠瓶蓋及瓶蓋市場報告:按產品類型、原料、容器類型、技術、最終用途和地區分類(2026-2034 年) 全球塑膠蓋子與封口裝置市場:市場規模、佔有率、成長和行業分析:按材料、產品類型、最終用途和地區分類的預測(至2034年)

全球塑膠蓋子與封口裝置市場:市場規模、佔有率、成長和行業分析:按材料、產品類型、最終用途和地區分類的預測(至2034年) 塑膠蓋子與封口裝置市場:2026-2032年全球市場預測(按產品類型、材料、最終用途和分銷管道分類)

塑膠蓋子與封口裝置市場:2026-2032年全球市場預測(按產品類型、材料、最終用途和分銷管道分類) 南美洲塑膠瓶蓋和封蓋:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

南美洲塑膠瓶蓋和封蓋:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 全球塑膠瓶蓋和封蓋市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球塑膠瓶蓋和封蓋市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球塑膠瓶蓋和封蓋市場報告

2026年全球塑膠瓶蓋和封蓋市場報告 塑膠瓶蓋和封蓋市場 - 全球產業規模、佔有率、趨勢、機會和預測(按產品類型、容器類型、原料、技術、最終用途行業、地區和競爭格局分類,2021-2031年)

塑膠瓶蓋和封蓋市場 - 全球產業規模、佔有率、趨勢、機會和預測(按產品類型、容器類型、原料、技術、最終用途行業、地區和競爭格局分類,2021-2031年) 70mm塑膠瓶蓋市場規模、佔有率和趨勢分析報告:按材料、應用、地區和細分市場預測,2026-2033年北美塑膠瓶蓋及封蓋市場:市佔率分析、產業趨勢、統計及成長預測(2026-2031)歐洲塑膠瓶蓋和封蓋:市場佔有率分析、行業趨勢、統計數據和成長預測(2026-2031 年)

70mm塑膠瓶蓋市場規模、佔有率和趨勢分析報告:按材料、應用、地區和細分市場預測,2026-2033年北美塑膠瓶蓋及封蓋市場:市佔率分析、產業趨勢、統計及成長預測(2026-2031)歐洲塑膠瓶蓋和封蓋:市場佔有率分析、行業趨勢、統計數據和成長預測(2026-2031 年)