|

市場調查報告書

商品編碼

1940588

撒哈拉以南非洲汽車市場:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Sub-Saharan Africa Automotive - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

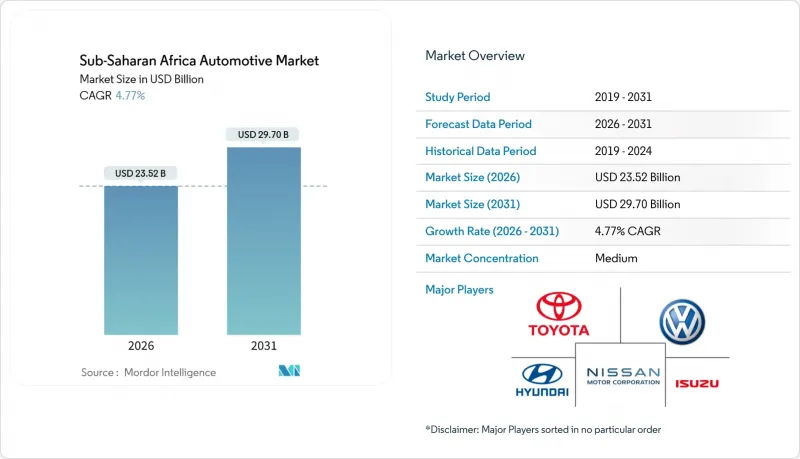

預計到 2026 年,撒哈拉以南非洲汽車市值將達到 235.2 億美元,高於 2025 年的 224.5 億美元。

預計到 2031 年將達到 297 億美元,2026 年至 2031 年的複合年成長率為 4.77%。

儘管貨幣波動和基礎設施不足,但加速的都市化、共乘汽車的激增以及政府對本地組裝的激勵措施共同維持了市場成長勢頭。衣索比亞和南非的電氣化舉措顯示市場需求結構趨於多元化,但由於柴油物流和服務網路的完善,柴油平台仍佔據主導地位。平行輸入活動持續抑制授權經銷商的銷售,但結構化的車隊融資計畫正在推動共享汽車營運商購買新車。在非洲大陸自由貿易協定(AfCFTA)關稅減讓的推動下,原始設備製造商(OEM)與本地組裝的策略合作正在加強區域供應鏈整合。

撒哈拉以南非洲汽車市場趨勢與洞察

中產階級收入成長與都市化

隨著都市區以每年4.1%的速度成長,購買力正向經銷商網路、融資管道和售後服務更為集中的大都會圈轉移。奈及利亞、肯亞和加納的中等收入家庭正在尋找價格適中的車型,加劇了中國和印度汽車製造商之間的競爭。緊湊型SUV和掀背車因其在堵塞道路上的靈活性而備受歡迎,而城郊消費者則依賴於二手車供應,這主要得益於都市區不斷成長的舊車置換需求。貸款機構也傾向於選擇就業集中的地區,在人口超過百萬的都市區,汽車貸款產品的供應量是農村地區的五倍之多。疲軟的該地貨幣降低了進口車的購買力,而與採礦業相關的工資上漲則在一定程度上抵消了價格壓力,並維持了市場需求。

共享出行平台的激增正在加速車輛更新換代。

來自 Moove 等供應商提供的結構化車隊融資方案,使叫車司機能夠繞過傳統的信用審核障礙,從而提振撒哈拉以南非洲汽車市場的多年基準需求。叫車每天運作8-12 小時,大約是私家車隊的運轉率,因此更新週期縮短至三到四年。這種可預測的周期使汽車製造商能夠將庫存計劃與平台採購計劃相匹配,即使在消費者信心減弱的情況下也能保障銷售量。預計到 2025 年,奈及利亞、肯亞和南非的活躍叫車司機總合將超過 45 萬,隨著平台向農村城市的擴張,潛在需求將進一步成長。政府機構日益認知到這些車隊是推動交通服務正規化的催化劑,衣索比亞和加納已為低排放叫車提供稅收優惠。由此帶來的車隊成長降低了許多市場零售融資管道有限的風險。

進口二手車的優勢

根據非洲汽車製造商協會(AAAM)預測,到2024年,撒哈拉以南非洲地區83%的輕型車輛註冊量將為二手。南非稅務局的海關數據顯示,二手和新車之間存在45%至60%的價格差距,影響了消費者的購買偏好。當該地貨幣貶值導致新車價格上漲時,這一差距會進一步擴大。預計2030年,富裕國家註銷內燃機(ICE)車輛的計畫每年將新增1,500萬輛符合出口條件的車輛。除非制定更嚴格的進口品質標準,否則這可能會延長該地區高排放氣體車輛的比例。聯合國歐洲經濟委員會(UNECE)的道路適航性通訊協定旨在遏制不合格車輛的流入,但邊境口岸執法不力的問題持續削弱了該議定書的有效性。

細分市場分析

到2025年,乘用車將佔撒哈拉以南非洲汽車市場總量的73.80%,預計到2031年,隨著中等收入階層的壯大,乘用車市場將以5.56%的複合年成長率成長。輕型商用車(LCV)受益於電子商務的快速發展,尤其是在奈及利亞和肯亞,兩國的末端配送業者正在租賃專為密集城市路線最佳化的小型貨車。在南非、尚比亞和安哥拉,中型和重型卡車的成長落後於整體市場成長,這與大宗商品出口週期密切相關。共乘車隊透過降低前期成本的結構化融資方案,幫助穩定乘用車需求並消化轎車和掀背車的庫存。

政策主導的電氣化正在改變埃塞俄比亞乘用車的組成。一項規定,新註冊車輛中必須有60%是電動車,這推動了專門的電動車組裝的建設和公共部門的採購。同時,由於負載容量和續航里程的限制,商用車電氣化較為滯後,儘管約翰尼斯堡目前正在城市物流循環中測試純電動貨車。乘用車市場的持續成長取決於貨幣穩定以及撒哈拉以南非洲汽車市場信貸改革的進展。

柴油平台憑藉著卓越的燃油經濟性和完善的服務基礎設施,在2025年佔據了撒哈拉以南非洲汽車市場54.60%的佔有率,預計到2031年將維持6.02%的複合年成長率。汽油車在都市區的普及率正在上升,因為成本差異正在縮小,排放氣體法規也不斷加強。正如奈及利亞的壓縮天然氣(CNG)計畫所表明的那樣,由於獎勵鼓勵計程車和公車改裝,CNG和液化石油氣(LPG)等替代燃料正在小眾車隊中獲得應用。利用當地原料的生質燃料計畫在加納和肯亞正在興起,但政策協調和對混合設施的投資是其發展壯大的關鍵。

由於建築和礦業車輛需求不斷成長,撒哈拉以南非洲柴油動力系統汽車的市場規模正在擴大。然而,隨著電動車推廣政策的實施,新的需求轉向電動平台,柴油動力汽車的市場佔有率正在逐漸下降。政府在燃油價格自由化方面的進展也將影響電動車的普及速度。那些較早取消柴油補貼的國家可能會加速汽油和混合動力汽車的普及。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 中產階級收入成長與都市化

- 共享出行平台的激增正在加速車輛更新換代。

- 政府對CKD/SKD組裝的獎勵措施

- 透過基礎設施建設改善道路連通性

- 透過非洲大陸自由貿易區(AfCFTA)降低關稅,擴大區域內貿易

- 中國製造的微型電動車進口量不斷成長,填補了超低成本市場的空白。

- 市場限制

- 在二手車進口領域佔據主導地位

- 消費貸款的限制和高利率

- 由於該地貨幣波動,進口成本增加。

- 社會安全署認證標準分散

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 買方和消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模及成長預測(價值及數量)

- 按車輛類型

- 搭乘用車

- 輕型商用車

- 中型和重型商用車輛

- 按燃料類型

- 汽油

- 柴油引擎

- 替代燃料(壓縮天然氣、液化石油氣、生質燃料)

- 透過推進技術

- 內燃機(ICE)

- 混合動力電動車(HEV)

- 電池電動車(BEV)

- 插電式混合動力車(PHEV)

- 按銷售管道

- 汽車製造商(OEM)授權經銷商

- 灰色進口/平行輸入

- 按國家/地區

- 南非

- 奈及利亞

- 肯亞

- 衣索比亞

- 迦納

- 坦尚尼亞

- 安哥拉

- 尚比亞

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Toyota Motor Corporation

- Volkswagen AG

- Hyundai Motor Company

- Nissan Motor Corporation

- Isuzu Motors Ltd.

- Ford Motor Company

- Groupe Renault

- Honda Motor Corporation

- Suzuki Motor Corporation

- Subaru Corporation

- Stellantis NV

- Daimler AG(Mercedes-Benz)

- BYD Co.

- Geely Auto Group

- Changan Auto

- JAC Motors

- BAIC Group

- Tata Motors

- Mahindra & Mahindra

- Innoson Vehicle Manufacturing(Nigeria)

第7章 市場機會與未來展望

The Sub-Saharan Africa automotive market size in 2026 is estimated at USD 23.52 billion, growing from the 2025 value of USD 22.45 billion, with projections for 2031 showing USD 29.7 billion, representing a 4.77% CAGR over the 2026-2031 period.

Accelerating urbanization, surging ride-hailing fleets, and government incentives for local assembly collectively sustain momentum despite persistent currency volatility and infrastructure gaps. Electrification initiatives in Ethiopia and South Africa signal a structurally diversifying demand mix, while diesel platforms remain dominant because of established fuel logistics and service networks. Grey-import activity continues to temper authorized-dealer volumes, yet structured fleet financing programs unlock new-vehicle penetration among ride-hailing operators. Strategic OEM partnerships with local assemblers, supported by AfCFTA tariff reductions, reinforce regional supply-chain integration.

Sub-Saharan Africa Automotive Market Trends and Insights

Rising Middle-Class Income and Urbanization

An annual 4.1% urban-population uptick shifts purchasing power toward metropolitan nodes where dealer networks, financing options, and aftermarket services coalesce. Middle-income households in Nigeria, Kenya, and Ghana gravitate towards affordable models, intensifying competition between Chinese and Indian OEMs. Compact SUVs and hatchbacks hold favor for maneuverability in congested corridors, whereas peri-urban consumers rely on incoming used stock propelled by rising urban trade-in flows. Lenders follow employment clusters, resulting in cities above 1 million inhabitants offering up to five times more car-loan products than rural districts. Although local-currency depreciation erodes import affordability, wage growth linked to extractive sectors partially offsets price pressure, sustaining demand.

Surge of Ride-Hailing Platforms Accelerating Fleet Renewal

Structured fleet-financing programs from providers such as Moove enable ride-hailing drivers to bypass conventional credit hurdles, lifting multi-year baseline demand for the Sub-Saharan Africa automotive market. Ride-hailing vehicles operate 8-12 hours daily, roughly quadrupling private-use utilization, which shortens replacement cycles to 3-4 years. This predictable cadence enables OEMs to align inventory planning with platform procurement schedules, thereby protecting volumes when consumer sentiment declines. Nigeria, Kenya, and South Africa collectively host over 450,000 active ride-hailing drivers as of 2025, and platform expansion into secondary cities deepens the addressable demand. Government agencies increasingly recognize such fleets as catalysts for formalizing transport services, offering duty rebates on low-emission vehicles deployed for ride-hailing in Ethiopia and Ghana. Resultant fleet growth moderates the risk of limited retail financing reach in many markets.

Dominance of Used-Car Imports

Used vehicles represented 83% of all light-duty vehicle registrations across Sub-Saharan Africa in 2024, according to the African Association of Automotive Manufacturers . South African Revenue Service customs data show that price gaps of 45-60% between used and new models tilt buyer preference. This disparity is magnified whenever local-currency depreciation inflates showroom prices. Projected deregistrations of ICE cars in wealthier economies could add 15 million exportable units annually by 2030, prolonging the region's high-emission fleet unless stricter import-quality rules take hold. UNECE roadworthiness protocols aim to stem sub-standard flows, but uneven enforcement across border posts still dilutes effectiveness.

Other drivers and restraints analyzed in the detailed report include:

- Government CKD/SKD Assembly Incentives

- Infrastructure Upgrades Improving Road Connectivity

- Limited Consumer Credit Access and High Interest Rates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passenger cars preserved a 73.80% share of the Sub-Saharan Africa automotive market volume in 2025 and are forecast to grow at a 5.56% CAGR through 2031, as middle-income cohorts expand. Light commercial vehicles (LCVs) benefit from e-commerce acceleration, especially in Nigeria and Kenya, where last-mile delivery providers lease small vans optimized for dense urban routes. Medium- and heavy-duty trucks trail the overall market growth, tied to commodity-export cycles in South Africa, Zambia, and Angola. Ride-hailing fleets underpin steady passenger-car demand, absorbing sedan and hatchback stock through structured financing programs that lower upfront cost burdens.

Policy-driven electrification in Ethiopia reshapes the passenger-car mix: 60% of newly registered cars must be EVs, catalyzing dedicated assembly ventures and public-sector procurement. Conversely, commercial-vehicle electrification lags due to payload-range constraints, although pilot programs in Johannesburg are testing battery-electric vans under urban logistics duty cycles. Sustained momentum within the passenger-car segment remains contingent on currency stability and progressive credit-access reforms across the Sub-Saharan Africa automotive market.

Diesel platforms held a 54.60% share of the Sub-Saharan Africa automotive market volume in 2025, buoyed by superior fuel economy and extensive service infrastructure, and they are projected to post a 6.02% CAGR through 2031. Gasoline penetration increases in urban centers where cost gaps narrow, and emissions policies become stricter. Alternative fuels, such as CNG and LPG, capture niche fleet deployments, as highlighted by Nigeria's compressed natural gas scheme, which incentivizes taxi and bus conversions. Biofuel initiatives are germinating in Ghana and Kenya, utilizing local feedstocks, but scaling up hinges on policy consistency and investment in blending facilities.

The Sub-Saharan African automotive market size for diesel powertrains expands alongside demand for construction and mining vehicles. Yet, its share gradually erodes as EV incentives redirect incremental demand toward electrified platforms. Government fuel-price deregulation trajectories also influence adoption curves; countries that phase out diesel subsidies sooner may prompt faster adoption of gasoline or hybrids.

The Sub-Saharan Africa Automotive Market Report is Segmented by Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Fuel Type (Gasoline, Diesel, and More), Propulsion Technology (Internal Combustion Engine (ICE), Hybrid Electric Vehicle (HEV), and More), Sales Channel, and Country. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

List of Companies Covered in this Report:

- Toyota Motor Corporation

- Volkswagen AG

- Hyundai Motor Company

- Nissan Motor Corporation

- Isuzu Motors Ltd.

- Ford Motor Company

- Groupe Renault

- Honda Motor Corporation

- Suzuki Motor Corporation

- Subaru Corporation

- Stellantis N.V.

- Daimler AG (Mercedes-Benz)

- BYD Co.

- Geely Auto Group

- Changan Auto

- JAC Motors

- BAIC Group

- Tata Motors

- Mahindra & Mahindra

- Innoson Vehicle Manufacturing (Nigeria)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Middle-Class Income and Urbanization

- 4.2.2 Surge of Ride-Hailing Platforms Accelerating Fleet Renewal

- 4.2.3 Government CKD/SKD Assembly Incentives

- 4.2.4 Infrastructure Upgrades Improving Road Connectivity

- 4.2.5 AfCFTA Tariff Reductions Expanding Intra-Regional Trade

- 4.2.6 Growth of Chinese Micro-EV Imports Filling Ultra-Low-Cost Niche

- 4.3 Market Restraints

- 4.3.1 Dominance of Used-Car Imports

- 4.3.2 Limited Consumer Credit Access and High Interest Rates

- 4.3.3 Local-Currency Volatility Inflating Import Costs

- 4.3.4 Fragmented Homologation Standards Across SSA

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Light Commercial Vehicles

- 5.1.3 Medium and Heavy Commercial Vehicles

- 5.2 By Fuel Type

- 5.2.1 Gasoline

- 5.2.2 Diesel

- 5.2.3 Alternative Fuels (CNG, LPG, Bio-fuel)

- 5.3 By Propulsion Technology

- 5.3.1 Internal Combustion Engine (ICE)

- 5.3.2 Hybrid Electric Vehicle (HEV)

- 5.3.3 Battery Electric Vehicle (BEV)

- 5.3.4 Plug-in Hybrid Electric Vehicle (PHEV)

- 5.4 By Sales Channel

- 5.4.1 Original Equipment Manufacturer (OEM)-Authorized Dealer

- 5.4.2 Grey Import / Parallel

- 5.5 By Country

- 5.5.1 South Africa

- 5.5.2 Nigeria

- 5.5.3 Kenya

- 5.5.4 Ethiopia

- 5.5.5 Ghana

- 5.5.6 Tanzania

- 5.5.7 Angola

- 5.5.8 Zambia

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Toyota Motor Corporation

- 6.4.2 Volkswagen AG

- 6.4.3 Hyundai Motor Company

- 6.4.4 Nissan Motor Corporation

- 6.4.5 Isuzu Motors Ltd.

- 6.4.6 Ford Motor Company

- 6.4.7 Groupe Renault

- 6.4.8 Honda Motor Corporation

- 6.4.9 Suzuki Motor Corporation

- 6.4.10 Subaru Corporation

- 6.4.11 Stellantis N.V.

- 6.4.12 Daimler AG (Mercedes-Benz)

- 6.4.13 BYD Co.

- 6.4.14 Geely Auto Group

- 6.4.15 Changan Auto

- 6.4.16 JAC Motors

- 6.4.17 BAIC Group

- 6.4.18 Tata Motors

- 6.4.19 Mahindra & Mahindra

- 6.4.20 Innoson Vehicle Manufacturing (Nigeria)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

2034年汽車銷售市場預測-按車輛類型、驅動方式、所有權類型、價格範圍、自動化程度、銷售管道和地區分類的全球分析

2034年汽車銷售市場預測-按車輛類型、驅動方式、所有權類型、價格範圍、自動化程度、銷售管道和地區分類的全球分析 2026年全球汽車市場報告

2026年全球汽車市場報告 中國汽車市場展望(2026年)2026年東協汽車產業的成長機遇

中國汽車市場展望(2026年)2026年東協汽車產業的成長機遇 南美汽車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)非洲汽車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)北美汽車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

南美汽車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)非洲汽車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)北美汽車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 越南汽車塗料市場(2025)中國的汽車用塗料市場(2025年)印尼的汽車用塗料市場(2025年)

越南汽車塗料市場(2025)中國的汽車用塗料市場(2025年)印尼的汽車用塗料市場(2025年)