|

市場調查報告書

商品編碼

1939605

非洲汽車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)Africa Automotive - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

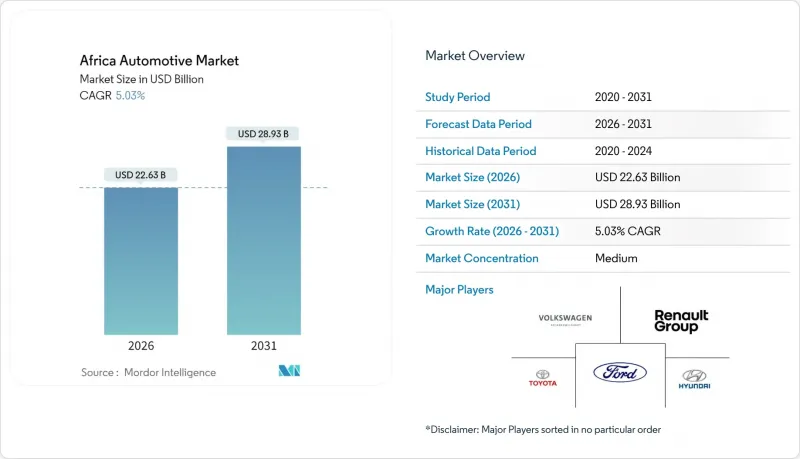

預計到 2026 年,非洲汽車市場價值將達到 226.3 億美元,高於 2025 年的 215.5 億美元,預計到 2031 年將達到 289.3 億美元。

預計2026年至2031年年複合成長率(CAGR)為5.03%。

非洲汽車市場需求蓬勃發展,這主要得益於都市區中產階級消費能力的提升、中國對CKD/SKD(散件組裝/半散件組裝)投資的加速以及非洲大陸自由貿易協定(AfCFTA)下的關稅自由化。數位匯款平台將海外韓國人的資金用於購車、叫車服務和最後一公里配送車隊的擴張,進一步擴大了潛在市場。區域原始設備製造商(OEM)正受益於優先考慮本地增值的政策獎勵。同時,礦業公司在銅帶地區開展的電動皮卡試驗計畫正在開闢一個獨特的商業市場。然而,物流瓶頸、貨幣波動以及大量灰色市場二手車的湧入仍然是可能減緩非洲汽車市場成長勢頭的重大阻力。

非洲汽車市場趨勢與洞察

非洲都市區中產階級汽車擁有量不斷上升

汽車擁有量與收入成長密切相關,預計到2060年,非洲中產階級人口將成長至11億,這將進一步提升人們對個人出行的需求。潛在購車者紛紛湧向入門級和緊湊型乘用車,這些車型兼具經濟性和都市區實用性。長期汽車貸款和訂閱模式等金融創新降低了購車門檻,進一步強化了非洲汽車市場需求的上升趨勢。

非洲大陸自由貿易區(AfCFTA)下的關稅削減將促進區域內貿易。

非洲大陸自由貿易區(AfCFTA)將逐步取消90%商品的關稅,大多數非最低度開發國家(NDC)需在五年內遵守該規定。汽車製造商將受益於區域內原料採購成本的降低,明確的原產地規則將鼓勵本地增值並允許享受優惠關稅。目前已有46個國家提交了讓步方案,貿易自由化正在為全散件組裝(CKD)業務帶來實際的成本節約。非關稅壁壘改革(包括海關程序數位化、標準統一和簡化邊境程序)預計將創造200億美元的額外貿易額,直接惠及非洲汽車市場。

港口長期擁擠及內陸物流瓶頸

德班港和拉各斯港的車輛吞吐量位居全球最低之列,導致貨物滯留時間和滯期費不斷攀升。鐵路利用率不足和老舊車輛正促使運輸轉向公路,而高昂的通行費和安全風險則推高了車輛的到岸成本。對於組裝,零件到貨不穩定阻礙了準時生產;對於出口商而言,貨物延誤損害了供應商的可靠性。除非正在進行的走廊建設和單一窗口海關系統能夠帶來可衡量的效率提升,否則物流摩擦將繼續阻礙非洲汽車市場的發展。

細分市場分析

到2025年,乘用車將佔非洲汽車市場的66.58%,反映出廣大城市地區對個人出行的需求。然而,由於非洲大陸自由貿易協定(AfCFTA)的實施以及蓬勃發展的電子商務,貨運量不斷成長,推動了人們對廂式貨車、皮卡和重型卡車的關注度提升,預計這些車型的複合年成長率將達到8.36%,超過乘用車。輕型商用車將受益於最後一公里配送業務的成長,而中型和重型卡車將沿著關稅協調走廊運輸區域間貿易貨物。礦業公司正在快速試用電池電動自動卸貨卡車,這表明它們有可能成為未來重型車輛的替代方案。

商用車組裝正利用政府的激勵政策,免除底盤和傳動系統零件的進口關稅,從而縮小與二手二手平行輸入的價格差距。全球產能重新分配也至關重要,預計摩洛哥將在2024年以61.4萬輛的產量超越南非,從而打造一個強大的供應商基礎,這些供應商可以轉型為貨運平台。隨著物流業者營運的標準化,車隊更新周期正在縮短,維持了非洲汽車市場這一細分領域的成長動能。

到2025年,內燃機汽車仍將維持90.68%的市場佔有率,這主要得益於價格合理的燃油和完善的維護系統。然而,在新的汽車製造商(OEM)推出新車型以及盧安達、肯亞和埃及等國的財政激勵措施的推動下,純電動車(BEV)預計將以10.12%的複合年成長率成長。從日本進口二手二手將有助於消費者儘早熟悉電動驅動系統,而電動車零件的關稅減免將降低商用車隊的整體擁有成本。

在主要都會區以外,由於電網穩定性的限制,電動皮卡的普及速度較為緩慢。但在銅礦區,離網太陽能和電池儲能中心已經投入使用,為電動皮卡提供動力。展望未來,隨著電池成本的下降和充電基礎設施的擴展,電動皮卡的普及速度將加快,內燃機汽車在非洲汽車市場的主導地位預計將逐漸減弱。

非洲汽車市場報告按車輛類型(乘用車和商用車)、動力類型(內燃機等)、最終用途(個人、車隊租賃等)、銷售管道(整車進口、散裝/散件組裝等)以及國家(南非、摩洛哥、阿爾及利亞、埃及、奈及利亞、加納、肯亞和其他非洲國家)進行細分。市場預測以價值(美元)和銷售(輛)為單位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 非洲都市區中產階級汽車擁有量不斷上升

- 中國整車製造商(例如比亞迪、奇瑞)加大對CKD/SKD的投資

- 非洲大陸自由貿易區(AFCFTA)關稅削減促進區域內貿易

- 擴大共乘與最後一公里配送車隊

- 透過金融科技匯款平台進行的海外僑民購車交易激增

- 銅帶國家礦業部門的電動車試驗計畫推動了對電動皮卡的需求。

- 市場限制

- 港口長期擁擠及內陸物流瓶頸

- 匯率波動推高了CKD套件的進口成本。

- 平行輸入二手車湧入抑制了對新車的需求。

- 西非ISO認證汽車用鋼材軋延產能短缺

- 價值/供應鏈分析

- 監管環境

- 科技展望(內燃機汽車、混合動力汽車、純電動車、燃料電池電動車)

- 波特五力模型

- 供應商的議價能力

- 買方和消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模及成長預測(金額:美元/數量:單位,2019-2030 年)

- 按車輛類型

- 搭乘用車

- 掀背車

- 轎車

- SUV 與跨界車

- MPV 及其他車型

- 商用車輛

- 輕型商用車(LCV)

- 中型和大型卡車

- 公車和長途客車

- 搭乘用車

- 依推進類型

- 內燃機(ICE)

- 混合動力電動車(HEV)

- 電池式電動車(BEV)

- 替代燃料(CNG/LPG、彈性燃料、燃料電池電動車)

- 按最終用途

- 個人所有

- 車隊租賃

- 叫車/出行服務供應商

- 對於政府和機構

- 按銷售管道

- 整車組裝(CBU)

- 半散件/全散件組裝(SKD/CKD)

- 二手車進口

- 按國家/地區

- 南非

- 摩洛哥

- 阿爾及利亞

- 埃及

- 奈及利亞

- 迦納

- 肯亞

- 其他非洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Toyota Motor Corporation

- Volkswagen AG

- Groupe Renault

- Hyundai Motor Company

- Ford Motor Company

- Daimler Truck AG

- Volvo Group

- Isuzu Motors Ltd

- Tata Motors Ltd

- Ashok Leyland

- Innoson Vehicle Manufacturing Co.

- Stellantis(Peugeot, Opel)

- Nissan Motor Co.

- Kia Corporation

- BAIC Group

- Chery Automobile Co.

- BYD Auto

- Geely Automobile Holdings

- Great Wall Motor(Haval)

- Guangzhou Automobile Group(GAC)

第7章 市場機會與未來展望

Africa automotive market size in 2026 is estimated at USD 22.63 billion, growing from 2025 value of USD 21.55 billion with 2031 projections showing USD 28.93 billion, growing at 5.03% CAGR over 2026-2031.

Rising urban middle-class spending, accelerated Chinese CKD/SKD investments, and AfCFTA tariff liberalization collectively set a positive demand trajectory for the Africa automotive market . Digital remittance platforms channeling diaspora funds into vehicle purchases and ride-hailing and last-mile delivery fleet expansion further widen addressable volumes. Regional OEMs benefit from policy incentives prioritizing local value addition, while miners' pilot programs for electric pickups in the copper-belt introduce a specialist commercial niche. Logistics bottlenecks, currency volatility, and grey-market used-car inflows remain the critical headwinds that can temper growth momentum in the Africa automotive market.

Africa Automotive Market Trends and Insights

Rising Passenger-Car Ownership Among Africa's Urban Middle Class

Vehicle ownership closely tracks income gains, and Africa's middle class is projected to swell toward 1.1 billion people by 2060. Driving incremental demand for personal mobility. Aspirational buyers gravitate toward entry-level and compact passenger models that balance affordability with urban practicality. Financing innovations such as longer-tenor auto loans and subscription models improve affordability, reinforcing the upward demand cycle across the Africa automotive market.

AfCFTA Tariff Reductions Stimulating Intra-Regional Trade

The African Continental Free Trade Area (AfCFTA) will phase out tariffs on 90% of goods, with most non-LDC nations obliged to comply within five years. Automotive OEMs stand to gain lower input costs on regional parts procurement, while clear rules of origin encourage local value addition that unlocks preferential tariffs. Forty-six countries have already submitted concession schedules, translating trade liberalization into tangible cost relief for CKD operations. Non-tariff barrier reforms-customs digitization, harmonized standards, and streamlined border procedures-are expected to release an extra USD 20 billion in trade value, a direct boon for the Africa automotive market.

Chronic Port Congestion and Inland Logistics Bottlenecks

Durban and Lagos ports rank among the world's slowest for automotive throughput, inflating dwell times and demurrage fees. Rail under-utilization and aging rolling stock shift traffic onto roads where high tolls and security risks push up landed vehicle costs. For CKD assemblers, inconsistent component arrivals disrupt just-in-time production, while exporters face missed sailing windows that erode supplier credibility. Unless ongoing corridor upgrades and single-window customs systems deliver measurable efficiencies, logistics friction will remain a drag on the Africa automotive market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Ride-Hailing and Last-Mile Delivery Fleets

- Mining-Sector EV Pilot Programs in Copper-Belt Nations

- Currency Volatility Elevating Import Costs for CKD Kits

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passenger cars dominated the Africa automotive market with a 66.58% share in 2025, reflecting personal mobility's appeal across sprawling urban centers. However, freight growth under AfCFTA and booming e-commerce pivot attention toward vans, pickups, and heavy trucks that are forecast to outpace passenger models at an 8.36% CAGR. Light commercial vehicles benefit from last-mile parcel volumes, whereas medium and heavy trucks haul regionally traded goods under harmonized customs corridors. Mining firms quickly test battery-electric dumpers, signaling future substitution opportunities in heavy-duty fleets.

Commercial vehicle assemblers leverage government incentives that waive import duties on chassis and drivetrains, narrowing price gaps versus grey-market used imports. Global production reallocations also matter: Morocco surpassed South Africa in 2024 with 614,000 units, creating a deep supplier base that can pivot toward freight platforms. As logistics players formalize operations, fleet replenishment cycles shorten, sustaining momentum in this segment of the Africa automotive market.

Internal combustion engines retained a 90.68% share in 2025, underscoring affordable fuel and servicing ecosystems. Nevertheless, battery electrics are projected to post a 10.12% CAGR on the back of Chinese OEM launches and fiscal incentives in Rwanda, Kenya, and Egypt. Pre-owned hybrid imports from Japan seed early consumer familiarity with electrified drivetrains, while duty exemptions on EV components lower the total cost of ownership for commercial fleets.

Grid stability constraints slow rollout outside major metros, yet copper-belt mining sites deploy off-grid solar-battery hubs to power electric pickups. Over time, diminishing battery costs and wider charging corridors could unlock a steeper adoption curve, gradually trimming ICE dominance in the African automotive market.

The Africa Automotive Market Report is Segmented by Vehicle Type (Passenger Cars and Commercial Vehicles), Propulsion Type (ICE, and More), End-Use (Personal, Fleet and Leasing, and More), Sales Channel (CBU, SKD/CKD, and More), and by Country (South Africa, Morocco, Algeria, Egypt, Nigeria, Ghana, Kenya, Rest of Africa). Market Forecasts are Provided in Terms of Value (USD) and Volume in (Units).

List of Companies Covered in this Report:

- Toyota Motor Corporation

- Volkswagen AG

- Groupe Renault

- Hyundai Motor Company

- Ford Motor Company

- Daimler Truck AG

- Volvo Group

- Isuzu Motors Ltd

- Tata Motors Ltd

- Ashok Leyland

- Innoson Vehicle Manufacturing Co.

- Stellantis (Peugeot, Opel)

- Nissan Motor Co.

- Kia Corporation

- BAIC Group

- Chery Automobile Co.

- BYD Auto

- Geely Automobile Holdings

- Great Wall Motor (Haval)

- Guangzhou Automobile Group (GAC)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Passenger-Car Ownership Among Africa's Urban Middle Class

- 4.2.2 Growing Chinese OEM CKD/SKD Investments (E.G., BYD, Chery)

- 4.2.3 AFCFTA Tariff Reductions Stimulating Intra-Regional Trade

- 4.2.4 Expansion of Ride-Hailing and Last-Mile Delivery Fleets

- 4.2.5 Surge in Diaspora-Financed Vehicle Purchases Via Fintech Remittance Platforms

- 4.2.6 Mining-Sector EV Pilot Programs in Copper-Belt Nations Driving Demand for Electric Pickups

- 4.3 Market Restraints

- 4.3.1 Chronic Port Congestion and Inland Logistics Bottlenecks

- 4.3.2 Currency Volatility Elevating Import Costs for CKD Kits

- 4.3.3 Grey-Market Used-Vehicle Influx Curbing New-Car Demand

- 4.3.4 Shortage Of ISO-Certified Auto-Grade Steel Rolling Capacity in West Africa

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook (ICE, Hybrid, BEV, FCEV)

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value in (USD) and Volume in (Units), 2019-2030)

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.1.1 Hatchback

- 5.1.1.2 Sedan

- 5.1.1.3 SUV & Crossover

- 5.1.1.4 MPV & Others

- 5.1.2 Commercial Vehicles

- 5.1.2.1 Light Commercial Vehicles (LCV)

- 5.1.2.2 Medium & Heavy Trucks

- 5.1.2.3 Buses & Coaches

- 5.1.1 Passenger Cars

- 5.2 By Propulsion Type

- 5.2.1 Internal Combustion Engine (ICE)

- 5.2.2 Hybrid Electric Vehicle (HEV)

- 5.2.3 Battery Electric Vehicle (BEV)

- 5.2.4 Alternative Fuels (CNG/LPG, Flex-fuel, FCEV)

- 5.3 By End-Use

- 5.3.1 Personal Ownership

- 5.3.2 Fleet & Leasing

- 5.3.3 Ride-hailing / Mobility Service Providers

- 5.3.4 Government & Institutional

- 5.4 By Sales Channel

- 5.4.1 Completely Built-up Imports (CBU)

- 5.4.2 Semi/Completely Knocked-down Assembly (SKD/CKD)

- 5.4.3 Used-Vehicle Imports

- 5.5 By Country

- 5.5.1 South Africa

- 5.5.2 Morocco

- 5.5.3 Algeria

- 5.5.4 Egypt

- 5.5.5 Nigeria

- 5.5.6 Ghana

- 5.5.7 Kenya

- 5.5.8 Rest of Africa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Toyota Motor Corporation

- 6.4.2 Volkswagen AG

- 6.4.3 Groupe Renault

- 6.4.4 Hyundai Motor Company

- 6.4.5 Ford Motor Company

- 6.4.6 Daimler Truck AG

- 6.4.7 Volvo Group

- 6.4.8 Isuzu Motors Ltd

- 6.4.9 Tata Motors Ltd

- 6.4.10 Ashok Leyland

- 6.4.11 Innoson Vehicle Manufacturing Co.

- 6.4.12 Stellantis (Peugeot, Opel)

- 6.4.13 Nissan Motor Co.

- 6.4.14 Kia Corporation

- 6.4.15 BAIC Group

- 6.4.16 Chery Automobile Co.

- 6.4.17 BYD Auto

- 6.4.18 Geely Automobile Holdings

- 6.4.19 Great Wall Motor (Haval)

- 6.4.20 Guangzhou Automobile Group (GAC)

7 Market Opportunities & Future Outlook

2034年汽車銷售市場預測-按車輛類型、驅動方式、所有權類型、價格範圍、自動化程度、銷售管道和地區分類的全球分析

2034年汽車銷售市場預測-按車輛類型、驅動方式、所有權類型、價格範圍、自動化程度、銷售管道和地區分類的全球分析 2026年全球汽車市場報告

2026年全球汽車市場報告 中國汽車市場展望(2026年)2026年東協汽車產業的成長機遇

中國汽車市場展望(2026年)2026年東協汽車產業的成長機遇 南美汽車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)撒哈拉以南非洲汽車市場:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)北美汽車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

南美汽車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)撒哈拉以南非洲汽車市場:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)北美汽車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 越南汽車塗料市場(2025)中國的汽車用塗料市場(2025年)印尼的汽車用塗料市場(2025年)

越南汽車塗料市場(2025)中國的汽車用塗料市場(2025年)印尼的汽車用塗料市場(2025年)