|

市場調查報告書

商品編碼

1937375

英國金融科技:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)United Kingdom Fintech - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

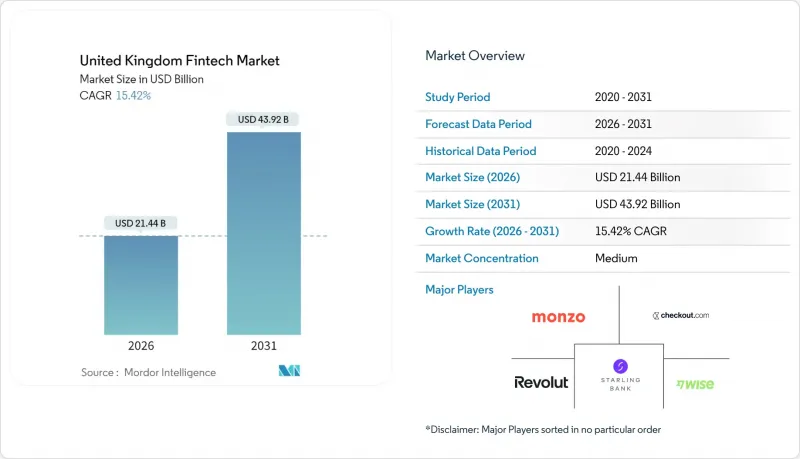

英國金融科技市場預計到 2026 年將達到 214.4 億美元,高於 2025 年的 185.7 億美元。

預計到 2031 年將達到 439.2 億美元,2026 年至 2031 年的複合年成長率為 15.42%。

開放銀行、即時支付和監管沙盒框架的普及,即便宏觀經濟的不確定性重塑了資金籌措格局,也正在擴大潛在需求。倫敦對創業投資依然具有吸引力,而曼徹斯特和愛丁堡等區域中心城市也不斷拓展其專業領域。新興銀行正從成長階段邁向獲利階段,嵌入式金融正在推動零售商與金融科技公司之間建立更深入的合作關係。科技的應用,尤其是人工智慧,正在支持經濟高效的規模化發展,並推動英國金融科技市場持續保持兩位數的成長。

英國金融科技市場趨勢與洞察

開放銀行監理加速了基於API的支付

到2024年,將有700萬英國消費者積極使用開放銀行服務,進而為第三方服務供應商提供標準化的API介面。強制性資料共用使帳戶間交易量增加了30%,並使一些小眾支付公司得以繞過傳統卡組織。在金融行為監理局(FCA)的主導,監理政策的製定已將英國金融科技市場打造成為競爭主導創新的標竿。支付服務提供者目前正在整合即時支付和身份驗證功能,從而降低商家費用,並促進各種嵌入式金融應用場景的實現。互通性的提升降低了客戶轉換方式的門檻,並加大了傳統支付處理商面臨的競爭壓力。

英國脫歐後的監管沙盒吸引了全球參與者

自2016年以來,已有55家公司參與了FCA的監管沙盒,數位證券沙盒在2025年3月迎來了12家國際參與者。託管測試環境降低了合規成本並縮短了產品上市時間,吸引了來自新加坡和美國的公司。 2025年1月宣布的一項新的人工智慧測試走廊將擴大覆蓋範圍,涵蓋演算法信貸承銷和自主交易。 FCA與加拿大、澳洲和日本監管機構簽署的跨境合作備忘錄簡化了通行證流程,使英國金融科技市場穩固地成為尋求國際擴張的成長型公司的理想跳板。

英國GDPR和彈性法規增加雲端合規成本

2025年3月全面落實業務彈性要求,需要對關鍵業務服務進行詳細梳理,並進行嚴謹而又貼近實際的情境測試。使用超大規模雲端服務供應商的金融科技公司需要證明其具備端到端的控制能力,這將導致審核頻率增加和供應商管理成本上升。將於2025年1月生效的《數位業務彈性法案》將在英國GDPR義務的基礎上,增加額外的ICT風險報告要求。中小企業面臨著能力發展與合規之間的權衡,將改變英國金融科技市場的成本曲線。

細分市場分析

截至2025年,數位支付佔英國金融科技市場的32.15%,而新銀行預計將以19.18%的複合年成長率成長至2031年,成為成長最快的領域。 Revolut和Starling創紀錄的盈利證明了規模化後業務單位經濟效益的可行性。 Revolut於2024年7月獲得英國銀行牌照,旨在擴大存款融資利潤率並加強產品交叉銷售。隨著區域信貸差距的擴大,中小企業的數位貸款正在加速發展。保險科技公司正在利用數據分析來改善核保流程,而數位投資則受益於人工智慧主導的投資組合視覺化。英格蘭銀行於2024年9月啟動的人工智慧聯盟正在推動各種提案領域的演算法創新,從而深化英國金融科技市場。

隨著嵌入式金融合作夥伴的興起,新銀行的客戶獲取成本將會下降,這些合作夥伴會將帳戶嵌入零售商的支付流程中。盈利的轉捩點將與手續費和交換費收入的增加有關,例如來自加密貨幣交易的收入。另類貸款機構將利用開放銀行數據,透過現金流審查來縮短中小企業的批准時間。財富科技公司將使零售投資更加普及,而保險科技公司將透過理賠自動化來提高客戶滿意度。總而言之,這些變化凸顯了英國金融科技產業正在進行的結構性調整。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 開放銀行監理加速英國基於API的支付創新

- 英國脫歐後的監理沙盒吸引全球金融科技擴張

- 全國範圍內的快速支付和即時支付(RTP)基礎設施將推動數位錢包的普及。

- 倫敦金融服務人才儲備和創業投資資金籌措將有助於金融科技公司擴大規模。

- 英國地區銀行規避風險,中小企業對替代融資的需求增加

- 透過與零售商建立嵌入式金融合作關係,擴大消費者「先買後付」的普及率

- 市場限制

- 英國金融行為監理局(FCA)加強對金融推廣活動的審查,抑制了金融科技公司的行銷支出。

- 英國GDPR和業務永續營運法規導致雲端合規成本不斷上升

- 詐騙的損失詐騙了消費者對新興銀行的信任。

- 自2022年起,資金籌措和估值重置將導致後期金融科技資金籌措停滯不前。

- 價值/供應鏈分析

- 監管或技術環境

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 投資和資金籌措趨勢分析

第5章 市場規模與成長預測

- 透過服務提案

- 數位支付

- 數字借貸和資金籌措

- 數位投資

- 保險科技

- 新銀行

- 最終用戶

- 零售

- 公司

- 透過使用者介面

- 行動應用

- 網頁/瀏覽器

- POS/物聯網設備

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Revolut Ltd

- Monzo Bank Ltd

- Wise plc

- Starling Bank Ltd

- Checkout.com

- Zopa Bank Ltd

- OakNorth Bank plc

- Klarna Bank AB(UK Ops)

- Stripe Payments UK Ltd

- GoCardless Ltd

- Atom Bank plc

- Zepz

- PaySafe Group Ltd

- Tide Platform Ltd

- Onfido Ltd

- Soldo Ltd

- Nutmeg Saving & Investment Ltd

- Rapyd Financial Network(UK)

- Funding Circle UK

- PensionBee plc

第7章 市場機會與未來展望

United Kingdom fintech market size in 2026 is estimated at USD 21.44 billion, growing from 2025 value of USD 18.57 billion with 2031 projections showing USD 43.92 billion, growing at 15.42% CAGR over 2026-2031.

Open banking adoption, real-time payments, and a supportive regulatory sandbox framework are expanding addressable demand even as macro-uncertainty reshapes funding patterns. London retains its magnetic pull for venture capital, yet regional hubs in Manchester and Edinburgh are capturing specialized niches. Neobanks move from growth to profitability, while embedded finance deepens retailer-fintech partnerships. Technology adoption, especially artificial intelligence, underpins cost-efficient scale-ups and positions the United Kingdom fintech market for sustained double-digit growth.

United Kingdom Fintech Market Trends and Insights

Open Banking Regulations Accelerate API-Based Payments

Seven million UK consumers actively used open-banking services in 2024, unlocking standardized API access for third-party providers. Mandatory data-sharing spurred a 30% rise in account-to-account transactions and enabled niche payment firms to bypass incumbent card networks. The regulatory design, championed by the Financial Conduct Authority (FCA), positions the United Kingdom fintech market as a benchmark for competition-led innovation. Payment providers now integrate real-time settlement and identity verification, lowering merchant fees and fuelling broader embedded-finance use cases. Elevated interoperability also reduces customer switching friction, intensifying competitive pressure on legacy processors.

Post-Brexit Regulatory Sandboxes Attract Global Entrants

Since 2016, the FCA sandbox has admitted 55 firms, and the Digital Securities Sandbox opened to 12 additional international participants in March 2025. Controlled testing cuts compliance costs and time-to-market, drawing firms from Singapore and the United States. A new AI-testing corridor, announced in January 2025, broadens the scope to algorithmic underwriting and autonomous trading. Cross-border memoranda between the FCA and Canadian, Australian, and Japanese regulators streamline passporting, thereby anchoring the United Kingdom fintech market as a launchpad for multi-jurisdictional scale-ups.

Rising Cloud-Compliance Costs Under UK GDPR and Resilience Rules

Full implementation of operational-resilience mandates by March 2025 requires granular mapping of important business services and severe-but-plausible scenario tests. Fintechs leveraging hyperscale cloud providers must evidence end-to-end controls, increasing audit frequency, and vendor-management expense. The Digital Operational Resilience Act, effective January 2025, layers additional ICT-risk reporting on top of UK GDPR obligations. Smaller firms face trade-offs between feature development and compliance, changing cost curves across the United Kingdom fintech market.

Other drivers and restraints analyzed in the detailed report include:

- Nationwide Faster Payments & RTP Infrastructure Boost Digital Wallet Uptake

- London Talent Pool and Venture Capital Density Catalyze Scale-Ups

- Digital Fraud and APP-Scam Losses Dent Consumer Trust

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Digital Payments retained 32.15% of the United Kingdom fintech market size in 2025, yet Neobanking posted the fastest outlook with a 19.18% CAGR to 2031. Record profitability at Revolut and Starling demonstrates viable unit-economics once scale is reached. Revolut secured a UK banking licence in July 2024, expanding deposit-funded margins and improving product cross-sell. Digital Lending to SMEs accelerates as regional credit gaps broaden. Insurtech deploys data analytics to refine underwriting, while Digital Investments benefit from AI-led portfolio visualization. The Bank of England's AI Consortium, launched in September 2024, catalyzes algorithmic innovation across propositions, adding depth to the United Kingdom fintech market.

Customer acquisition costs for neobanks fall as embedded-finance partners bundle accounts inside retail checkout journeys. Profitability inflection points align with higher interchange income and fee-based revenues, such as crypto trading. Alternative lenders leverage open-banking data for cash-flow underwriting, cutting decision times for SMEs. Wealth-tech providers democratize fractional investing, while Insurtech firms automate claims, raising user satisfaction. Collectively, these shifts underline the structural re-rating occurring in the United Kingdom fintech industry.

The United Kingdom Fintech Market is Segmented by Service Proposition (Digital Payments, Digital Lending and Financing, Digital Investments, Insurtech, and Neobanking), by End-User (Retail and Businesses), and by User Interface (Mobile Applications, Web / Browser, and POS / IoT Devices). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Revolut Ltd

- Monzo Bank Ltd

- Wise plc

- Starling Bank Ltd

- Checkout.com

- Zopa Bank Ltd

- OakNorth Bank plc

- Klarna Bank AB (UK Ops)

- Stripe Payments UK Ltd

- GoCardless Ltd

- Atom Bank plc

- Zepz

- PaySafe Group Ltd

- Tide Platform Ltd

- Onfido Ltd

- Soldo Ltd

- Nutmeg Saving & Investment Ltd

- Rapyd Financial Network (UK)

- Funding Circle UK

- PensionBee plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Open Banking Regulations Accelerating API-Based Payment Innovation in UK

- 4.2.2 Post-Brexit UK Regulatory Sandboxes Attracting Global Fintech Expansion

- 4.2.3 Nationwide Faster Payments & RTP Infrastructure Boosting Digital Wallet Adoption

- 4.2.4 London's FinServ Talent Pool & VC Funding Density Catalyzing Fintech Scale-ups

- 4.2.5 SME Demand for Alternative Lending Amid Bank De-Risking in UK Regions

- 4.2.6 Embedded Finance Partnerships with Retailers Scaling Consumer BNPL Penetration

- 4.3 Market Restraints

- 4.3.1 Heightened FCA Scrutiny on Financial Promotions Limiting Fintech Marketing Spend

- 4.3.2 Rising Cloud Compliance Costs under UK GDPR & Operational Resilience Rules

- 4.3.3 Digital Fraud & APP-Scam Losses Eroding Consumer Trust in Neobanks

- 4.3.4 Funding Contraction Post-2022 Valuation Reset Stalling Late-Stage Fintech Rounds

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory or Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Investment & Funding Trend Analysis

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Service Proposition

- 5.1.1 Digital Payments

- 5.1.2 Digital Lending and Financing

- 5.1.3 Digital Investments

- 5.1.4 Insurtech

- 5.1.5 Neobanking

- 5.2 By End-User

- 5.2.1 Retail

- 5.2.2 Businesses

- 5.3 By User Interface

- 5.3.1 Mobile Applications

- 5.3.2 Web / Browser

- 5.3.3 POS / IoT Devices

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.4.1 Revolut Ltd

- 6.4.2 Monzo Bank Ltd

- 6.4.3 Wise plc

- 6.4.4 Starling Bank Ltd

- 6.4.5 Checkout.com

- 6.4.6 Zopa Bank Ltd

- 6.4.7 OakNorth Bank plc

- 6.4.8 Klarna Bank AB (UK Ops)

- 6.4.9 Stripe Payments UK Ltd

- 6.4.10 GoCardless Ltd

- 6.4.11 Atom Bank plc

- 6.4.12 Zepz

- 6.4.13 PaySafe Group Ltd

- 6.4.14 Tide Platform Ltd

- 6.4.15 Onfido Ltd

- 6.4.16 Soldo Ltd

- 6.4.17 Nutmeg Saving & Investment Ltd

- 6.4.18 Rapyd Financial Network (UK)

- 6.4.19 Funding Circle UK

- 6.4.20 PensionBee plc

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

金融科技市場商業分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、解決方案

金融科技市場商業分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、解決方案 2026年金融科技多重雲端全球市場報告

2026年金融科技多重雲端全球市場報告 金融科技市場規模、佔有率、趨勢和預測:按部署類型、技術、應用、最終用戶和地區分類,2026-2034 年

金融科技市場規模、佔有率、趨勢和預測:按部署類型、技術、應用、最終用戶和地區分類,2026-2034 年 2026-2030年全球金融科技市場金融科技市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶及功能分類

2026-2030年全球金融科技市場金融科技市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶及功能分類 美國金融科技市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

美國金融科技市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年) 全球金融科技即服務 (FaaS) 市場規模、佔有率、趨勢和成長分析報告,2026-2034 年金融科技市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年預測日本金融科技市場報告:依採用類型、技術、應用、最終用戶和地區分類(2026-2034年)

全球金融科技即服務 (FaaS) 市場規模、佔有率、趨勢和成長分析報告,2026-2034 年金融科技市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年預測日本金融科技市場報告:依採用類型、技術、應用、最終用戶和地區分類(2026-2034年) 金融科技領域生成式人工智慧市場-全球產業規模、佔有率、趨勢、機會及預測(按組件、部署、應用、地區和競爭格局分類,2021-2031年)

金融科技領域生成式人工智慧市場-全球產業規模、佔有率、趨勢、機會及預測(按組件、部署、應用、地區和競爭格局分類,2021-2031年)