|

市場調查報告書

商品編碼

1937330

美國第三方物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)United States 3PL - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

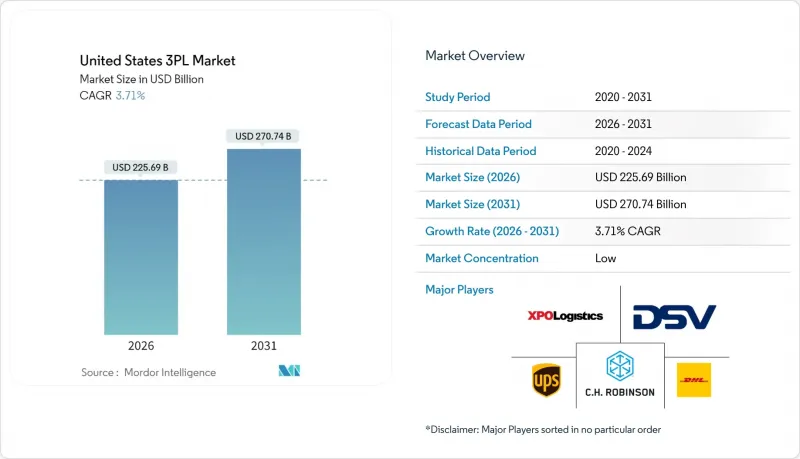

美國第三方物流(3PL) 市場預計將從 2025 年的 2,176.2 億美元成長到 2026 年的 2,256.9 億美元,預計到 2031 年將達到 2,707.4 億美元,2026 年至 2031 年的複合年成長率為 3.71%。

市場的穩定擴張反映了行業的成熟、供應鏈的持續複雜性以及近岸外包趨勢的不斷推進——近岸外包將生產和分銷環節更靠近國內消費者。儘管製造業客戶仍然是關鍵客戶群,但醫療保健、電子商務和科技業的托運人目前已成為成長最快的收入驅動力。為了應對勞動力短缺和燃油價格波動,供應商持續將資金重新分配到自動化、倉儲機器人和視覺化軟體領域。隨著數十億美元的收購案不斷湧現,產業整合正在加速進行,而混合資產策略則在貨運需求週期不確定的情況下分散風險。托運人與第三方物流(3PL) 供應商夥伴關係的成功率下降至 83%,也凸顯了美國 3PL 市場日益激烈的競爭和更高的績效預期。

美國第三方物流市場趨勢與洞察

電子商務和全通路的快速成長

持續成長的線上消費(預計到2024年將成長9.3%)支撐了對更密集的全國配送網路的需求,並推動了DHL供應鏈收購IDS 履約,新增130萬平方英尺的倉儲空間。各大品牌正將其配送網路從沿海大型物流中心分散到區域市場的微型倉配中心,以縮短配送時間。逆向物流日益複雜,促使DHL收購Inmar供應鏈解決方案公司,打造北美最大的退貨平台,並為供應商提供了利用循環經濟模式的機會。自動化和自主配送試點計畫不斷改變最後一公里配送的成本結構,為靈活型專業服務商創造了更多機會。這些趨勢共同推動美國第三方物流市場在未來幾年實現穩健成長。

外包以降低成本並專注於核心競爭力

托運人正逐漸減少對物流管理的關注,而將更多精力投入產品開發,並將執行風險轉移給規模化的第三方物流 (3PL) 服務商。 C.H. Robinson 的管理解決方案平台整合了運輸管理系統 (TMS)、第三方物流 (3PL) 和第四方物流 (4PL) 服務,利用每年 3500 萬件的貨運量來降低成本並提高可視性。營運資金壓力迫使 80% 的製造商重新調整庫存,這進一步增加了對先進附加價值服務(VAS) 倉庫的需求。這些結構性變化正在擴大美國第三方物流市場的覆蓋範圍和收入來源。

卡車運輸和倉儲業勞動力短缺

產業協會警告稱,未來十年美國將出現120萬名駕駛者的缺口,這將導致人事費用上升和服務可靠性下降。倉儲業也面臨類似的人才短缺問題,78%的托運人表示,由於持續的招募難題,其運力有所下降。 XPO的LTL 2.0員工敬業度策略使員工滿意度提高了40%,顯示文化因素有助於提高員工留任率。為了因應日益成長的自動化和安全法規,各服務商也正在擴大技能提升計畫。在自動化全面普及之前,勞動力短缺仍將是美國第三方物流市場面臨的最大限制。

細分市場分析

截至2025年,國內運輸管理將占美國第三方物流市場佔有率的47.55%,這顯示貨運協調仍是一項基礎服務。預測定價工具、路線密度分析和多模態最佳化正在創造競爭優勢,使承運商能夠在波動的現貨市場中保持利潤率。同時,加值倉儲和配送服務正以7.55%的複合年成長率快速成長,並隨著電經銷商對預售庫存、套件組裝、貼標和當日截止等服務需求的增加而日益重要。 C.H. Robinson的管理解決方案套件將這些功能整合到一個統一的控制面板中,體現了美國第三方物流市場服務架構的融合趨勢。

倉儲投資也與低溫運輸擴張相契合。 DHL、UPS 和 Americold 加快了符合 FDA 標準、溫控範圍為 2-8°C 並具備 GDP 認證能力的設施建設。受服裝和電子產品退貨需求的推動,逆向物流領域正在為其服務組合增添新的維度。同時,儘管國際運輸管理面臨貿易政策和海運附加費帶來的運力波動,但在全球供應鏈中仍保持著重要地位,為近岸工廠提供原料。總體而言,捆綁式服務模式正在推動客戶留存,並支持美國第三方物流行業持續實現利潤多元化。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 電子商務和全通路的快速成長

- 外包以降低成本並專注於核心競爭力

- 數位運輸管理系統/倉庫管理系統及自動化採用情況

- 低溫運輸和醫療物流的快速成長

- 由於近岸外包,區域DCC需求增加

- 自動駕駛卡車貨運走廊

- 市場限制

- 卡車運輸和倉儲業勞動力短缺

- 燃油價格波動

- 網路風險與不斷上漲的保險費

- 港口壅塞導致附加費的不確定性

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 來自相鄰環節(CEP、最後一公里、低溫運輸)的需求

- 倉儲業的整體趨勢

- 新冠疫情的影響及後疫情時代的常態化

第5章 市場規模與成長預測

- 透過服務

- 國內運輸管理(DTM)

- 道路運輸

- 鐵路

- 空運

- 水道

- 國際運輸管理(ITM)

- 路

- 鐵路

- 空運

- 水道

- 加值倉儲及配送服務 (VAWD)

- 國內運輸管理(DTM)

- 最終用戶

- 車

- 能源與公共產業

- 製造業

- 生命科學與醫療保健

- 科技與電子

- 電子商務

- 消費品和日用必需品(快速消費品)

- 食品/飲料

- 其他

- 透過物流模型

- 輕資產(管理基礎)

- 資產密集型(擁有車輛和倉庫)

- 混合

- 按美國地區

- 東北

- 中西部

- 南部

- 西

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- CH Robinson Worldwide Inc.

- XPO Logistics

- United Parcel Service, Inc.

- DHL Group

- DSV

- Kuehne+Nagel Inc

- Hub Group, Inc.

- Ryder System, Inc.

- Expeditors International

- Lineage Logistics

- Americold Logistics

- Penske Logistics

- Schneider Logistics

- NFI Industries

- GXO Logistics

- Geodis

- CEVA Logistics

- CJ Logistics

- Saddle Creek Logistics Services

- JB Hunt Transport Services

第7章 市場機會與未來展望

第8章附錄

The United States 3PL Market is expected to grow from USD 217.62 billion in 2025 to USD 225.69 billion in 2026 and is forecast to reach USD 270.74 billion by 2031 at 3.71% CAGR over 2026-2031.

The steady expansion of the market reflects the sector's maturation, persistent supply-chain complexity, and ongoing nearshoring that pulls production and distribution closer to domestic consumers. Manufacturing customers remain the anchor segment, yet healthcare, e-commerce, and tech shippers now supply the fastest incremental revenue streams. Providers continue reallocating capital toward automation, warehouse robotics, and visibility software to counter labor scarcity and fuel price volatility. Consolidation accelerates through billion-dollar acquisitions while hybrid asset strategies spread risk in an uncertain freight-demand cycle. Competitive intensity, measured by a declining 83% shipper-3PL partnership success rate, underscores rising performance expectations in the United States third-party logistics market.

United States 3PL Market Trends and Insights

E-commerce & Omnichannel Boom

Persistent online spending-up 9.3% in 2024-anchors demand for dense national fulfillment networks, prompting DHL Supply Chain's acquisition of IDS Fulfillment that added 1.3 million sq ft of capacity. Brands diversify distribution away from coastal mega-centers toward micro-fulfillment nodes in secondary markets to compress delivery windows. Reverse-logistics complexity rises; DHL's Inmar Supply Chain Solutions deal created the largest North American returns platform, positioning providers for margin capture in circular commerce. Automation and autonomous delivery pilots continue reshaping last-mile cost structures, expanding opportunity for nimble specialists. Collectively, these dynamics keep the United States third-party logistics market on a firm multiyear growth footing.

Outsourcing for Cost & Focus on Core Competencies

Shippers concentrate on product development rather than logistics administration, transferring execution risk to scaled 3PLs. C.H. Robinson's Managed Solutions platform unifies TMS, 3PL, and 4PL services, leveraging 35 million annual shipments to deliver cost and visibility gains. Working-capital pressures push 80% of manufacturers to rebalance inventory, which in turn amplifies demand for sophisticated VAS warehousing. These structural shifts widen the service scope-and revenue pool-inside the United States third-party logistics market.

Labor Shortages in Trucking & Warehousing

Industry groups warn of a 1.2 million-driver deficit over the next decade, inflating wage bills and straining service reliability. Warehouses face similar scarcity, with 78% of shippers reporting persistent recruitment hurdles that cut into throughput. XPO's LTL 2.0 employee-engagement playbook lifted satisfaction scores 40%, hinting at cultural levers for retention. Providers also expand upskilling programs to meet growing automation and safety mandates. Until automation reaches full scale, labor scarcity remains the single largest drag on the United States third-party logistics market.

Other drivers and restraints analyzed in the detailed report include:

- Digital TMS/WMS & Automation Uptake

- Nearshoring-Driven Regional DCC Demand

- Cyber-Risk & Rising Insurance Premiums

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Domestic Transportation Management held 47.55% of the United States third-party logistics market share in 2025, showing that freight orchestration remains the bedrock service offering. Predictive pricing tools, lane-density analytics, and multimodal optimization now shape competitive positioning, enabling carriers to navigate volatile spot markets without surrendering margin. Conversely, Value-Added Warehousing & Distribution, advancing at 7.55% CAGR, is gaining strategic heft as e-commerce sellers demand inventory postponement, kitting, labeling, and same-day cutoffs. C.H. Robinson's Managed Solutions suite fuses these functions on a single dashboard, showcasing the converging service architecture that characterizes the United States third-party logistics market.

Warehouse investments also track cold-chain expansion: DHL, UPS, and Americold accelerated builds of FDA-compliant facilities with 2-8 °C zones and GDP-certified handling. Reverse-logistics units, fueled by apparel and electronics returns, added another dimension to service portfolios. Meanwhile, International Transportation Management battled capacity swings tied to trade policy and ocean-freight surcharges, yet retained relevance for global supply chains funneling inputs into nearshore plants. Altogether, bundled service models strengthen stickiness across the United States third-party logistics industry and support ongoing margin diversification.

The United States 3PL Market Report is Segmented by Service (Domestic Transportation Management, International Transportation Management, and More), by End User (Automotive, Energy and Utilities, Manufacturing, and More), by Logistics Model (Asset-Light, Asset-Heavy, Hybrid), and by Region (Northeast, Midwest, South, West). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- C.H. Robinson Worldwide Inc.

- XPO Logistics

- United Parcel Service, Inc.

- DHL Group

- DSV

- Kuehne + Nagel Inc

- Hub Group, Inc.

- Ryder System, Inc.

- Expeditors International

- Lineage Logistics

- Americold Logistics

- Penske Logistics

- Schneider Logistics

- NFI Industries

- GXO Logistics

- Geodis

- CEVA Logistics

- CJ Logistics

- Saddle Creek Logistics Services

- J.B. Hunt Transport Services

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce & omnichannel boom

- 4.2.2 Outsourcing for cost & focus on core competencies

- 4.2.3 Digital TMS/WMS & automation uptake

- 4.2.4 Cold-chain & healthcare logistics surge

- 4.2.5 Nearshoring-driven regional DCC demand

- 4.2.6 Autonomous-truck freight corridors

- 4.3 Market Restraints

- 4.3.1 Labor shortages in trucking & warehousing

- 4.3.2 Fuel-price volatility

- 4.3.3 Cyber-risk & rising insurance premiums

- 4.3.4 Port-congestion surcharge uncertainty

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Demand from Adjacent Segments (CEP, Last-Mile, Cold-Chain)

- 4.9 General Trends in Warehousing

- 4.10 Impact of COVID-19 & Post-Pandemic Normalization

5 Market Size & Growth Forecasts (Value)

- 5.1 By Service

- 5.1.1 Domestic Transportation Management (DTM)

- 5.1.1.1 Roadways

- 5.1.1.2 Railways

- 5.1.1.3 Airways

- 5.1.1.4 Waterways

- 5.1.2 International Transportation Management (ITM)

- 5.1.2.1 Roadways

- 5.1.2.2 Railways

- 5.1.2.3 Airways

- 5.1.2.4 Waterways

- 5.1.3 Value-Added Warehousing & Distribution (VAWD)

- 5.1.1 Domestic Transportation Management (DTM)

- 5.2 By End User

- 5.2.1 Automotive

- 5.2.2 Energy & Utilities

- 5.2.3 Manufacturing

- 5.2.4 Life Sciences & Healthcare

- 5.2.5 Technology & Electronics

- 5.2.6 E-commerce

- 5.2.7 Consumer Goods & FMCG

- 5.2.8 Food & Beverages

- 5.2.9 Others

- 5.3 By Logistics Model

- 5.3.1 Asset-Light (Management-Based)

- 5.3.2 Asset-Heavy (Own Fleet & Warehouses)

- 5.3.3 Hybrid

- 5.4 By U.S. Region

- 5.4.1 Northeast

- 5.4.2 Midwest

- 5.4.3 South

- 5.4.4 West

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 C.H. Robinson Worldwide Inc.

- 6.4.2 XPO Logistics

- 6.4.3 United Parcel Service, Inc.

- 6.4.4 DHL Group

- 6.4.5 DSV

- 6.4.6 Kuehne + Nagel Inc

- 6.4.7 Hub Group, Inc.

- 6.4.8 Ryder System, Inc.

- 6.4.9 Expeditors International

- 6.4.10 Lineage Logistics

- 6.4.11 Americold Logistics

- 6.4.12 Penske Logistics

- 6.4.13 Schneider Logistics

- 6.4.14 NFI Industries

- 6.4.15 GXO Logistics

- 6.4.16 Geodis

- 6.4.17 CEVA Logistics

- 6.4.18 CJ Logistics

- 6.4.19 Saddle Creek Logistics Services

- 6.4.20 J.B. Hunt Transport Services

7 Market Opportunities & Future Outlook

8 Appendix

2026年全球第三方物流(3PL)市場報告

2026年全球第三方物流(3PL)市場報告 2026-2030年全球汽車第三者物流市場

2026-2030年全球汽車第三者物流市場 第三方物流軟體市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、功能及解決方案分類

第三方物流軟體市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、功能及解決方案分類 英國第三方物流(3PL):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)西班牙第三方物流(3PL) 市場:佔有率分析、產業趨勢與統計、成長預測 (2026-2031)

英國第三方物流(3PL):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)西班牙第三方物流(3PL) 市場:佔有率分析、產業趨勢與統計、成長預測 (2026-2031) 第三方物流全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)

第三方物流全球市場規模、佔有率、趨勢和成長分析報告(2026-2034) 生物製藥低溫運輸物流服務市場按服務類型、溫度類型、運輸方式、產品類型、包裝類型和最終用途分類,全球預測(2026-2032年)新加坡第三方物流(3PL) 市場:佔有率分析、產業趨勢、統計數據和成長預測 (2026-2031)日本第三方物流(3PL)市場:佔有率分析、產業趨勢、統計數據和成長預測(2026-2031)

生物製藥低溫運輸物流服務市場按服務類型、溫度類型、運輸方式、產品類型、包裝類型和最終用途分類,全球預測(2026-2032年)新加坡第三方物流(3PL) 市場:佔有率分析、產業趨勢、統計數據和成長預測 (2026-2031)日本第三方物流(3PL)市場:佔有率分析、產業趨勢、統計數據和成長預測(2026-2031) 第三方物流市場-全球產業規模、佔有率、趨勢、機會及預測(依運輸方式、服務類型、產業、地區及競爭格局分類,2021-2031年預測)

第三方物流市場-全球產業規模、佔有率、趨勢、機會及預測(依運輸方式、服務類型、產業、地區及競爭格局分類,2021-2031年預測)