|

市場調查報告書

商品編碼

1937296

中國豪華車市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)China Luxury Car - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

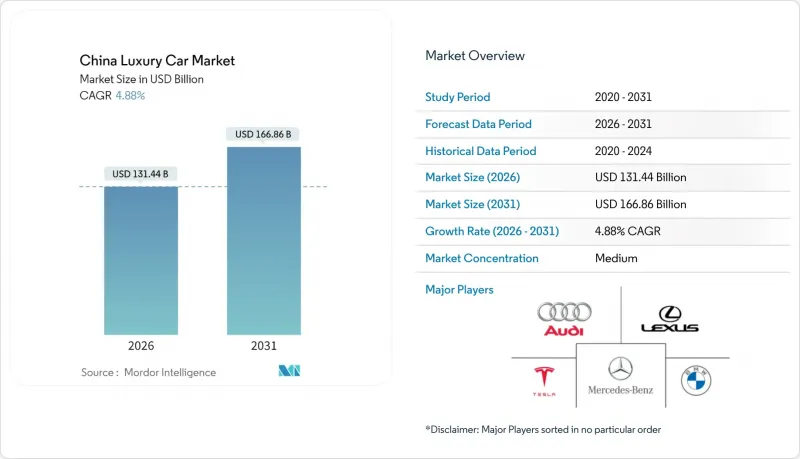

中國豪華車市場預計將從 2025 年的 1,253.2 億美元成長到 2026 年的 1,314.4 億美元,到 2031 年達到 1,668.6 億美元,2026 年至 2031 年的複合年成長率為 4.88%。

這一擴張得益於電氣化進程的加速、區域城市居民可支配收入的成長以及對新能源汽車(NEV)的有利政策支持。消費者對高階汽車作為行動技術平台的態度轉變也推動了需求成長,迫使製造商提升自動駕駛能力和連網服務生態系統。隨著國內高階電動車品牌縮小技術差距,而外國品牌則尋求透過平台在地化鞏固其在中國高階市場的地位,競爭日益激烈。半導體國產化程度的提高和稅制改革的趨勢預計將繼續影響整個價值鏈的利潤率、供應鏈策略和產品組合決策。

中國豪華車市場趨勢與洞察

區域城市富裕消費者的擴張

區域城市居民家庭收入逐年成長,成長超過大都會圈,由此催生了一批新的豪華車買家,他們將汽車視為身份的象徵和科技的展示。理想汽車等國產品牌預計到2024年將交付500,508輛汽車,顯示追求品質生活的家庭正在擁抱配備ADAS(高級駕駛輔助系統)的大型豪華SUV。高達2萬元人民幣(約2,800美元)的舊車置換補助提升了消費者的購買力,使中產階級家庭也能進入中國豪華車市場。

國內豪華電動車品牌擴張

國內領先的汽車製造商正利用換電網路、L2+級自動駕駛技術和OTA空中升級等多種手段來滿足市場需求:蔚來汽車預計2024年交付221,970輛汽車,而理想汽車在成立五年內就實現了年交付50萬輛的目標。這種成長正在重塑中國高階汽車市場,將競爭格局從傳統的內燃機模式轉向軟體生態系統和服務模式。

聯網汽車資料安全法規

中國的資料安全法要求汽車製造商將車輛產生的資料儲存在國內,這增加了外國製造商的成本,迫使他們複製全球雲端架構。跨境數據流動的限制使空中下載(OTA)升級流程複雜化,擴大了與全球平台的功能差距,並阻礙了中國高階汽車市場的差異化。

細分市場分析

到2025年,SUV將佔據中國高階汽車市場63.12%的佔有率,凸顯了消費者對更高駕駛視野和更適合家庭使用的內部空間的偏好。隨著蔚來ES6和理想汽車L9等旗艦純電動車的推出,SUV細分展示室預計到2031年將以6.25%的複合年成長率成長。雖然轎車仍然是商務人士出行的首選,但銷售成長正轉向專為多代家庭設計的多功能車型。廣汽集團推出的L3級自動駕駛技術以及理想MEGA靈活的座椅佈局,都展現了自動化和內裝多功能性如何樹立新的豪華車標竿。

次要影響包括長軸距底盤和自適應氣壓懸吊套件的需求增加,以提升省道行駛的乘坐舒適性。掀背車雖然屬於小眾車型,但卻受益於都市區停車位緊張的現狀,尤其是在擁擠的沿海大都會圈。 SUV 的主導也推動了電池更換技術的普及,因為更大的底盤可以容納標準化的電池模組,從而增強了中國高階市場固有的基礎設施網路效應。

到2025年,內燃機汽車仍將佔中國汽車銷量的61.95%,目前仍佔中國高階汽車市場的最大佔有率。然而,在購置稅減免、電池成本下降以及全國充電樁密度不斷提高的推動下,預計到2031年,純電動車的年複合成長率將達到9.72%。插電式混合動力汽車可以有效緩解里程焦慮,並填補沿海地區基礎設施的不足。由於氫氣物流的挑戰,燃料電池汽車的試驗仍處於實驗階段,短期內其影響力有限。

純電動車(BEV)的優勢在於強化了以軟體為中心的價值提案,例如高級駕駛輔助系統、身臨其境型資訊娛樂系統和持續的空中升級,從而開闢了內燃機汽車無法企及的領域。國內汽車製造商正利用垂直整合的電力電子供應鏈來降低零件成本,並滿足半導體國產化的要求。因此,預計到2031年,售價在30萬至60萬元人民幣之間的電動車品牌將佔據中國高階市場55%以上的佔有率,取代傳統上受注重身份的高管青睞的渦輪增壓六缸轎車。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 二、三線城市消費者財富不斷成長

- 政府對高階新能源汽車的獎勵措施

- 對優質化和品牌地位的需求日益成長

- 國內豪華電動車品牌(蔚來、理想汽車)的擴張

- L3級自動駕駛功能提昇平均售價

- 基於NFT的數位所有權獎勵

- 市場限制

- 高昂的前期成本和奢侈稅

- 聯網汽車資料安全法規

- 高階半導體供應受限

- 高階叫車服務的普及抑制了人們的購買意願

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模及成長預測(價值(美元)及銷售量(單位))

- 按車身樣式

- 掀背車

- 轎車

- 運動型多用途車(SUV)

- 多用途汽車(MPV)

- 依動力傳動系統類型

- 內燃機車輛

- 電動車(純電動車、插電式混合動力車、油電混合車、燃料電池電動車)

- 按品牌和原產國

- 中國本土品牌

- 外國品牌

- 按銷售管道

- 授權經銷商

- 直營店

- 線上直銷

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Mercedes-Benz Group AG

- BMW Group

- Volkswagen Group(Audi AG)

- Lexus(Toyota Motor Corp.)

- Tesla Inc.

- Zhejiang Geely Holding(Zeekr)

- Dongfeng Motor Company

- China FAW Group(Hongqi)

- NIO Inc.

- Li Auto Inc.

- XPeng Motors

- SAIC-GM(Cadillac)

- GAC Aion

- Infiniti(Nissan Motor Co.)

- Acura(Honda Motor Co.)

- Porsche AG

- Jaguar Land Rover Ltd.

- Lincoln Motor Co.(Ford)

- Rolls-Royce Motor Cars

- Maserati SpA

第7章 市場機會與未來展望

The China luxury car market is expected to grow from USD 125.32 billion in 2025 to USD 131.44 billion in 2026 and is forecast to reach USD 166.86 billion by 2031 at 4.88% CAGR over 2026-2031.

This expansion is underpinned by accelerating electrification, rising disposable income in lower-tier cities, and policy support that favors new-energy vehicles. Demand momentum also stems from consumers who now view premium vehicles as mobile technology platforms, prompting manufacturers to elevate autonomous-driving capabilities and connected-services ecosystems. Competitive intensity has sharpened as domestic electric-luxury brands close traditional technology gaps, while foreign marques localize platforms to safeguard their positions within the China premium car market. Ongoing semiconductor localization and evolving tax regulations will continue to reshape margins, supply-chain strategies, and product-mix decisions across the value chain.

China Luxury Car Market Trends and Insights

Growing Consumer Wealth in Tier-2 and Tier-3 Cities

Household incomes in secondary urban centers are growing annually, outpacing tier-1 growth and spawning a new cohort of premium buyers who view vehicles as status symbols and technology showcases. Domestic brands such as Li Auto delivered 500,508 units in 2024, illustrating how aspirational families embrace large premium SUVs equipped with ADAS. Trade-in subsidies worth up to RMB 20,000 (~USD 2,800 ) have amplified purchasing power, allowing middle-class households to enter the China premium car market.

Expansion of Domestic EV-Luxury Brands

Domestic champions have combined battery-swapping networks, Level 2+ autonomy, and over-the-air upgrades to capture demand. NIO delivered 221,970 vehicles in 2024, and Li Auto reached half a million annual deliveries within five years of launch. Such growth reshapes the China premium car market by shifting the basis of competition from combustion-engine heritage to software ecosystems and service models .

Data-Security Regulation on Connected Vehicles

China's Data Security Law compels automakers to store vehicle-generated data domestically, inflating costs for foreign OEMs that must duplicate global cloud architectures. Limitations on cross-border data flows complicate over-the-air update pipelines, diminishing feature parity with global platforms and restraining differentiation in the China premium car market.

Other drivers and restraints analyzed in the detailed report include:

- L3 Autonomy Features Driving Higher ASP

- NFT-Based Digital Ownership Perks

- Premium Ride-Hailing Curbing Ownership Intent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

SUVs captured 63.12% of the Chinese premium car market 2025, underscoring consumer preference for commanding driving positions and family-oriented interiors. The SUV sub-segment will expand at a 6.25% CAGR through 2031 as battery-electric flagships like the NIO ES6 and Li Auto L9 dominate showroom traffic. Sedans maintain gravitas in executive transport, but incremental volume shifts to versatile multi-purpose vehicles designed for multi-generational households. GAC's forthcoming Level 3 rollout and Li MEGA's flexible seating highlight how automation and interior versatility set new luxury benchmarks.

The second-order effects include a stronger demand for long-wheelbase chassis and adaptive air-suspension packages that enhance ride comfort on variable road quality in lower-tier cities. Hatchbacks remain niche yet benefit from tight urban parking constraints, particularly in coastal megacities where congestion is severe. SUV leadership also advances battery-swapping adoption because larger underbodies accommodate standardized modules, reinforcing infrastructure network effects unique to the Chinese premium car market.

Internal-combustion vehicles still represented 61.95% of the 2025 volume, translating to the most significant current slice of the China premium car market size. Yet battery-electric models will climb at a 9.72% CAGR through 2031, propelled by purchase-tax exemptions, falling battery costs, and growing charger density nationwide. Plug-in hybrids serve as range-anxiety hedges, bridging coastal infrastructure gaps. Fuel-cell pilots remain experimental owing to hydrogen logistics, limiting near-term influence.

Battery-electric leadership amplifies software-centric value propositions-advanced driver-assistance, immersive infotainment, and continuous over-the-air updates-that combustion rivals cannot match. Domestic OEMs leverage vertically integrated power-electronics supply chains to reduce bill-of-materials and comply with chip-localization directives. Consequently, the China premium car market share for electric nameplates in the RMB 300,000-600,000 bracket is projected to exceed 55% by 2031, displacing turbocharged six-cylinder sedans historically favored by status-conscious executives.

The China Luxury Car Market Report is Segmented by Vehicle Body Style (Hatchbacks, Sedans, and More), Powertrain Type (Internal Combustion Engine Vehicles and Electric Vehicles), Brand Origin (Domestic Chinese Brands and Foreign Brands), and Sales Channel (Authorized Dealerships, Company-Owned Stores, and Online Direct-To-Consumer). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

List of Companies Covered in this Report:

- Mercedes-Benz Group AG

- BMW Group

- Volkswagen Group (Audi AG)

- Lexus (Toyota Motor Corp.)

- Tesla Inc.

- Zhejiang Geely Holding (Zeekr)

- Dongfeng Motor Company

- China FAW Group (Hongqi)

- NIO Inc.

- Li Auto Inc.

- XPeng Motors

- SAIC-GM (Cadillac)

- GAC Aion

- Infiniti (Nissan Motor Co.)

- Acura (Honda Motor Co.)

- Porsche AG

- Jaguar Land Rover Ltd.

- Lincoln Motor Co. (Ford)

- Rolls-Royce Motor Cars

- Maserati S.p.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Consumer Wealth in Tier-2 and Tier-3 Cities

- 4.2.2 Government NEV Incentives for the Premium Segment

- 4.2.3 Rising Demand for Premiumization and Brand Status

- 4.2.4 Expansion of Domestic EV-Luxury Brands (NIO, Li Auto)

- 4.2.5 L3 Autonomy Features Driving Higher ASP

- 4.2.6 NFT-Based Digital Ownership Perks

- 4.3 Market Restraints

- 4.3.1 High Upfront Cost and Luxury Tax

- 4.3.2 Data-Security Regulation on Connected Vehicles

- 4.3.3 High-End Semiconductor Supply Constraints

- 4.3.4 Premium Ride-Hailing Curbing Ownership Intent

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Vehicle Body Style

- 5.1.1 Hatchbacks

- 5.1.2 Sedans

- 5.1.3 Sport-Utility Vehicles (SUVs)

- 5.1.4 Multi-purpose Vehicles (MPVs)

- 5.2 By Powertrain Type

- 5.2.1 Internal-Combustion (ICE) Vehicles

- 5.2.2 Electric Vehicles (BEV, PHEV, HEV, FCEV)

- 5.3 By Brand Origin

- 5.3.1 Domestic Chinese Brands

- 5.3.2 Foreign Brands

- 5.4 By Sales Channel

- 5.4.1 Authorized Dealerships

- 5.4.2 Company-Owned Stores

- 5.4.3 Online Direct-to-Consumer

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.4.1 Mercedes-Benz Group AG

- 6.4.2 BMW Group

- 6.4.3 Volkswagen Group (Audi AG)

- 6.4.4 Lexus (Toyota Motor Corp.)

- 6.4.5 Tesla Inc.

- 6.4.6 Zhejiang Geely Holding (Zeekr)

- 6.4.7 Dongfeng Motor Company

- 6.4.8 China FAW Group (Hongqi)

- 6.4.9 NIO Inc.

- 6.4.10 Li Auto Inc.

- 6.4.11 XPeng Motors

- 6.4.12 SAIC-GM (Cadillac)

- 6.4.13 GAC Aion

- 6.4.14 Infiniti (Nissan Motor Co.)

- 6.4.15 Acura (Honda Motor Co.)

- 6.4.16 Porsche AG

- 6.4.17 Jaguar Land Rover Ltd.

- 6.4.18 Lincoln Motor Co. (Ford)

- 6.4.19 Rolls-Royce Motor Cars

- 6.4.20 Maserati S.p.A.

7 Market Opportunities & Future Outlook

2026年全球豪華車軟管市場報告

2026年全球豪華車軟管市場報告 2026-2030年全球豪華車市場2026年全球豪華穹頂車旅遊市場報告2026年全球豪華車市場報告

2026-2030年全球豪華車市場2026年全球豪華穹頂車旅遊市場報告2026年全球豪華車市場報告 豪華車市場規模、佔有率和趨勢分析報告:按車輛類型、驅動方式、地區和細分市場分類的預測(2026-2033 年)

豪華車市場規模、佔有率和趨勢分析報告:按車輛類型、驅動方式、地區和細分市場分類的預測(2026-2033 年) 豪華車市場規模、佔有率、趨勢及報告:按車型、燃料類型、價格範圍和地區分類(2026-2034 年)

豪華車市場規模、佔有率、趨勢及報告:按車型、燃料類型、價格範圍和地區分類(2026-2034 年) 豪華車市場分析及預測(至2035年):依類型、產品類型、服務、技術、零件、應用、材質、最終用戶、安裝類型、解決方案分類

豪華車市場分析及預測(至2035年):依類型、產品類型、服務、技術、零件、應用、材質、最終用戶、安裝類型、解決方案分類 歐洲豪華車市場-佔有率分析、產業趨勢、統計和成長預測(2026-2031)

歐洲豪華車市場-佔有率分析、產業趨勢、統計和成長預測(2026-2031) 2026-2034年全球豪華車市場規模、佔有率、趨勢及成長分析報告豪華車:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

2026-2034年全球豪華車市場規模、佔有率、趨勢及成長分析報告豪華車:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)