|

市場調查報告書

商品編碼

1910708

歐洲電動自行車市場-佔有率分析、產業趨勢、統計數據和成長預測(2026-2031)Europe E-Bike - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

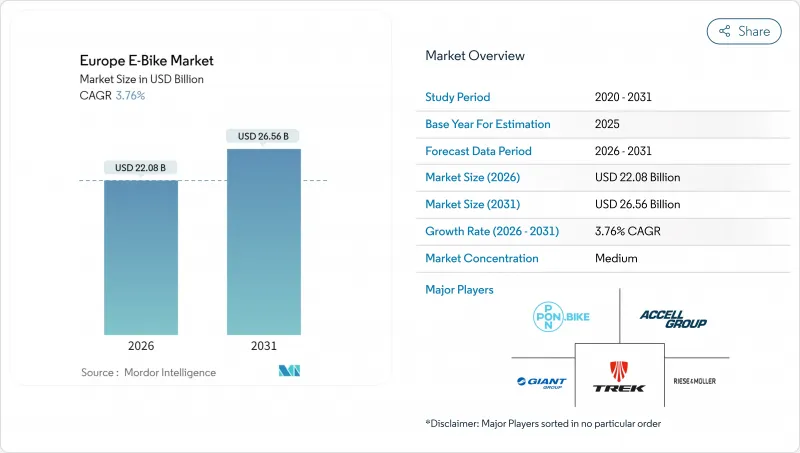

歐洲電動自行車市場預計將從 2025 年的 212.8 億美元成長到 2026 年的 220.8 億美元,預計到 2031 年將達到 265.6 億美元,2026 年至 2031 年的複合年成長率為 3.76%。

強勁的潛在需求,包括企業車隊、最後一公里物流和通勤替代出行等需求,抵消了疫情後庫存調整的影響。受保護自行車網路的擴張、對中國產電動自行車反傾銷稅延長五年以及電池技術的進步,共同維持了定價權並保障了利潤率。租賃模式將大規模採購轉化為可預測的營運支出,正在加速企業用戶的使用;而歐盟內部的在地化生產則降低了關稅風險並縮短了前置作業時間。高速電動電動式自行車監管法規的逐步統一,以及固體微型電池的技術突破,預計將擴大高性能車型的潛在市場。

歐洲電動自行車市場趨勢與洞察

企業自行車租賃熱潮

稅收優惠的租賃模式將電動自行車從可選項轉變為員工福利。薪資扣款可降低30%至50%的實際成本,進而為高階車型的普及鋪路,避免價格意外。車隊管理使原始設備製造商 (OEM) 能夠了解市場需求,實現準時生產並降低庫存風險。 NAVIT 等平台統一了跨國人力資源規則,加速了法國和荷蘭等勞動市場緊張地區的擴張。

採購補貼和稅收優惠

國家和地方政府的慷慨激勵措施壓低了實際價格,並提前刺激了需求。法國繼續為每輛電動自行車提供高達4000歐元(約464.6萬日元)的補貼;荷蘭允許雇主對電動自行車的成本折舊免稅額;比利時則通過工資扣除和租賃相結合的方式,提供遠低於標價的折扣。由於換代週期可預測,製造商正在調整生產計畫,以配合補貼期,從而平衡庫存並保障中價位產品的銷售。這些措施正在維持經濟成長。

與一般自行車相比,初始成本較高

電動自行車的平均價格遠高於傳統自行車,而且溢價也相當高。即使在德國降價之後,入門級車型的價格很少下降,高昂的電池更換成本進一步推高了其終身成本。東歐地區的家庭對此感受特別深刻,那裡的中位數收入較低,儘管基礎設施完善,但電動自行車的普及率仍然很低。雖然分期付款方式有所幫助,但由於文化上對消費信貸的抵觸情緒,許多買家只能等待價格下降或收入增加後再購買。

細分市場分析

預計2025年,歐洲電動式自行車市場規模將佔全球市場的77.35%。助力自行車因其操作簡單、騎行體驗熟悉而廣受歡迎,是通勤和休閒旅行的主要需求來源。在所有類別中,高速輔助自行車的複合年成長率最高,達到3.88%,這主要得益於企業對時速可達45公里/小時的通勤和高效配送的需求。

監管協調仍然是關鍵因素。如果歐盟關於統一頭盔要求和車道使用規則的立法草案得以實施,預計將會促進大規模生產並降低單位成本。 Riese & Müller即將推出的配備齒輪傳動裝置的車型表明,原始設備製造商(OEM)正致力於拓展高階高速電動式自行車。隨著保險產品的成熟和基礎設施的完善,預計動力傳動系統的構成比將逐漸轉向高功率等級。

到2025年,都市區通勤將佔歐洲電動自行車市場的73.62%。這是因為電動自行車在10公里以內的短途出行中尤為有利,而停車難和堵塞費等因素會抑制汽車的使用。配備長貨架和貨箱的貨運和實用型電動自行車正以3.84%的複合年成長率成長,這主要得益於零售商、宅配業者和年輕家庭的需求,他們希望用電動自行車取代第二輛汽車。配備雙兒童安全座椅的家庭貨運型電動自行車不僅吸引了送貨員,也吸引了更多人,例如短途汽車出行的替代者,以及注重環保的父母。此外,汽車製造商(OEM)透過重新設計車架,使電動自行車在不超過250瓦法定功率限制的情況下,能夠承載200公斤的負載容量,進一步模糊了個人用途和商業用途之間的界限。

由於車架堅固、配備雙電池和高扭矩電機,旅行自行車和山地自行車的價格居高不下,但季節性天氣和預算限制了它們的普及。市政氣候行動計畫和最後一公里配送合約正在推動有效負載容量最佳化、再生煞車和模組化配件的研發,使自行車從休閒設備轉變為商用設備。

到2025年,鋰離子電池將佔歐洲電動自行車市場99.86%的佔有率,成本降低和能量密度提高將支撐市場規模。化學成分的不斷改進以及向鎳錳鈷混合物和磷酸鋰鐵(LFP)的轉變以穩定成本,將推動市場以與整體市場相似的年均3.76%的成長率逐步擴張。

鉛酸電池將僅存在於替換市場和超低成本進口市場。採用固態電池或半固態電池組的測試車輛可望達到15-20%的充電速度提升,並在低溫環境下擁有更佳的耐久性。在固態超級工廠規模化生產之前,電池機殼設計、電池管理系統(BMS)演算法以及再生陰極材料的逐步改進將延長保固期並提升電池的轉售價值,從而確保鋰離子電池在預測期內保持主導地位。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章執行摘要主要發現

第2章 報告

第3章 引言

- 研究假設和市場定義

- 調查範圍

- 調查方法

第4章 主要產業趨勢

- 年度自行車銷售額

- 平均銷售價格和價格範圍構成

- 電動自行車及零件的跨境貿易

- 電動自行車在自行車總銷量中所佔的百分比

- 5-15公里通勤共享

- 自行車和電動式自行車租賃市場規模

- 電動自行車電池組價格

- 電池化學價格比較

- 最後一公里配送量

- 受保護的自行車道(公里)

- 健行和戶外活動的參與率

- 電動自行車電池容量(瓦時)

- 都市交通壅塞指數

- 法律規範

- 身份驗證和授權

- 進出口和貿易法規

- 分類和道路法規

- 電池和充電器安全

第5章 市場情勢

- 市場概覽

- 市場促進因素

- 企業自行車租賃的蓬勃發展

- 採購補貼和稅收優惠

- 電動貨運車輛在最後一公里運輸中的成長

- 擴建自行車道

- 歐盟區域化製造地的搬遷

- 固體微型電池的進展

- 市場限制

- 與傳統自行車相比,初始成本較高

- 經銷商庫存估值降低

- 行人超速的監管灰色地帶

- 中國投入品關稅變化

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 產業間競爭

- 定價分析

第6章 市場區隔分析

- 依推進類型

- 踏板輔助

- 速度踏板

- 附油門輔助

- 透過使用

- 貨物/多用途

- 城市/都市區

- 健行/登山

- 依電池類型

- 鉛酸電池

- 鋰離子電池

- 其他

- 按下馬達安裝位置

- 輪轂(前/後)

- 中置馬達

- 透過驅動系統

- 鏈傳動

- 皮帶傳動

- 透過馬達輸出

- 小於250瓦

- 251-350 W

- 351-500 W

- 501-600 W

- 600瓦或以上

- 按價格範圍

- 低於 1000 美元

- 1,000-1,499 美元

- 1500-2499美元

- 2,500-3,499 美元

- 3,500 美元至 5,999 美元

- 超過6000美元

- 按銷售管道

- 線上

- 離線

- 按最終用途

- 商業航運

- 零售和商品分銷

- 食品和飲料配送

- 服務供應商

- 個人及家庭用途

- 對機構而言

- 其他

- 商業航運

- 按國家/地區

- 德國

- 荷蘭

- 法國

- 義大利

- 西班牙

- 英國

- 瑞士

- 奧地利

- 比利時

- 丹麥

- 瑞典

- 挪威

- 波蘭

- 捷克共和國

- 葡萄牙

- 其他歐洲地區

第7章 競爭情勢

- 關鍵策略舉措

- 市佔率分析

- 公司簡介

- Accell Group

- Pon Holdings BV

- Giant Manufacturing Co. Ltd.

- Trek Bicycle Corporation

- Riese & Muller GmbH

- Brompton Bicycle Limited

- CUBE Bikes

- Yamaha Motor Co., Ltd.

- Merida Industry Co. Ltd.

- VanMoof BV

- Volt Electric Bikes

- Pedego Electric Bikes

- KTM Fahrrad GmbH

- Fritzmeier Systems GmbH & Co. KG(M1 Sporttechnik)

第8章:CEO們需要思考的關鍵策略問題

The European e-bike market is expected to grow from USD 21.28 billion in 2025 to USD 22.08 billion in 2026 and is forecast to reach USD 26.56 billion by 2031 at 3.76% CAGR over 2026-2031.

Healthy underlying demand from corporate fleets, last-mile logistics, and commuter substitution offsets the post-pandemic inventory correction. Expansion of protected cycle networks, the five-year extension of anti-dumping duties on Chinese e-bikes, and battery technology upgrades collectively sustain pricing power and shield margins. Leasing models that convert large one-time purchases into predictable operating expenses accelerate penetration among employers, while localized EU manufacturing mitigates tariff risk and shortens lead times. Gradual regulatory alignment on speed-pedelecs, combined with solid-state micro-battery breakthroughs, is expected to widen the total addressable base for higher-performance models.

Europe E-Bike Market Trends and Insights

Corporate Bike-Leasing Boom

Tax-advantaged leasing turns e-bikes into employee benefits rather than discretionary buys. Payroll deductions cut effective outlay by 30-50% and open premium tiers without sticker shock. Fleets give OEMs volume visibility, enabling just-in-time production and lower inventory risk. Platforms like NAVIT unify cross-border HR rules, accelerating rollouts in France and the Netherlands under tight labor markets.

Purchase Subsidies and Tax Incentives

Generous national and municipal incentives compress effective prices and pull demand forward. France still grants up to EUR 4,000 (~USD 4,646) per unit, the Netherlands lets employers depreciate e-bike costs, and Belgium couples payroll credits with leases, slicing significant savings from sticker prices. Because renewals follow predictable cycles, manufacturers time production runs to subsidy windows, smoothing inventories and protecting mid-range volume tiers. These measures sustain growth.

High Upfront Cost vs Acoustic Bikes

Average prices are significantly higher, commanding a substantial premium over conventional bicycles. Even after a German price retreat, entry models rarely dip, while high battery replacements add lifetime expense. Eastern European households, with lower median wages, feel the gap most, slowing mainstream adoption despite better infrastructure. Financing helps, yet cultural resistance to consumer credit leaves many buyers waiting for price cuts or income growth.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Last-Mile E-Cargo Fleets

- Protected Bicycle-Lane Expansion

- Dealer Inventory Write-Downs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The European e-bike market size for pedal-assist propulsion accounted for 77.35% share in 2025. Pedal-assist thrives on regulatory simplicity and a familiar ride feel, anchoring commuter and leisure volumes. Speed-pedelecs outpaced all categories at 3.88% CAGR, leveraging commuter appetite for 45 km/h capability and fleet demand for quicker deliveries.

Regulatory convergence remains the swing factor: draft EU proposals aiming to synchronize helmet and path-access rules could unlock scale manufacturing and lower unit costs. Riese & Muller's forthcoming Pinion-equipped models reflect OEM bets on premium speed-pedelec expansion . As insurance products mature and infrastructure adapts, the propulsion mix is likely to tilt gradually toward higher-power classes.

City/urban commuting generated 73.62% of the European e-bike market share in 2025, because e-bikes excel on sub-10 km trips where parking scarcity and congestion charges penalize cars. Cargo/utility formats, purpose-built with long racks or boxes, expand at a 3.84% CAGR as retailers, couriers, and young families replace second cars. Family cargo variants with dual-child seating broaden the appeal beyond couriers, substituting short car trips and capturing sustainability-minded parents. OEMs redesign frames for 200 kg payloads without exceeding 250 W legal limits, further blurring lines between personal and commercial use.

Trekking and mountain bikes command premium ASPs through rugged frames, dual batteries, and high-torque motors, but remain limited by discretionary budgets and seasonal weather. Municipal climate plans and last-mile contracts tilt R&D toward payload optimization, regenerative braking, and modular accessories that transform bikes from leisure gear into professional equipment.

Lithium-ion holds 99.86% of the European e-bike market share in 2025, anchoring market size through cost erosion and energy-density gains. Continuous chemistry tweaks, shift toward nickel-manganese-cobalt blends or LFP for cost stability, drive incremental 3.76% CAGR, mirroring total market.

Lead-acid survives only in replacement sales and ultra-budget imports. Pilot fleets with lithium-carbon or semi-solid packs promise 15-20% faster charging and better low-temperature resilience. Until solid-state gigafactories scale, incremental gains in housing design, BMS algorithms, and recycled-content cathodes will lengthen warranties and lift resale values, keeping lithium-ion unchallenged during the forecast window.

The Europe E-Bike Market Report is Segmented by Propulsion Type (Pedal Assisted, Speed Pedelec, and More), Application Type (Cargo/Utility, City/Urban, and More), Battery Type (Lead-Acid Battery, Lithium-Ion Battery, and More), Motor Placement (Hub (Front/Rear), Mid-Drive), Drive Systems, Motor Power, Price Band, Sales Channel, End Use, and Country. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

List of Companies Covered in this Report:

- Accell Group

- Pon Holdings B.V.

- Giant Manufacturing Co. Ltd.

- Trek Bicycle Corporation

- Riese & Muller GmbH

- Brompton Bicycle Limited

- CUBE Bikes

- Yamaha Motor Co., Ltd.

- Merida Industry Co. Ltd.

- VanMoof BV

- Volt Electric Bikes

- Pedego Electric Bikes

- KTM Fahrrad GmbH

- Fritzmeier Systems GmbH & Co. KG (M1 Sporttechnik)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Executive Summary & Key Findings

2 Report Offers

3 Introduction

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 Key Industry Trends

- 4.1 Annual Bicycle Sales

- 4.2 Average Selling Price & Price-Band Mix

- 4.3 Cross-Border Trade in E-Bikes & Parts

- 4.4 E-Bike Share of Total Bicycle Sales

- 4.5 5-15 km Commuter Share

- 4.6 Bicycle/E-Bike Rental Market Size

- 4.7 E-Bike Battery Pack Price

- 4.8 Battery Chemistry Price Comparison

- 4.9 Last-Mile Delivery Volume

- 4.10 Protected Bicycle Lanes (km)

- 4.11 Trekking/Outdoor Activity Participation

- 4.12 E-Bike Battery Capacity (Wh)

- 4.13 Urban Traffic Congestion Index

- 4.14 Regulatory Framework

- 4.14.1 Homologation & Certification

- 4.14.2 Export-Import & Trade Rules

- 4.14.3 Classification & Road-Access Rules

- 4.14.4 Battery & Charger Safety

5 Market Landscape

- 5.1 Market Overview

- 5.2 Market Drivers

- 5.2.1 Corporate Bike-Leasing Boom

- 5.2.2 Purchase Subsidies and Tax Incentives

- 5.2.3 Growth of Last-Mile E-Cargo Fleets

- 5.2.4 Protected Bicycle-Lane Expansion

- 5.2.5 Regionalized EU Manufacturing Shift

- 5.2.6 Solid-State Micro-Battery Advances

- 5.3 Market Restraints

- 5.3.1 High Upfront Cost vs Acoustic Bikes

- 5.3.2 Dealer Inventory Write-Downs

- 5.3.3 Speed-Pedelec Regulatory Grey-Zones

- 5.3.4 Tariff Volatility on Chinese Inputs

- 5.4 Value / Supply-Chain Analysis

- 5.5 Regulatory Landscape

- 5.6 Technological Outlook

- 5.7 Porter's Five Forces

- 5.7.1 Threat of New Entrants

- 5.7.2 Bargaining Power of Suppliers

- 5.7.3 Bargaining Power of Buyers

- 5.7.4 Threat of Substitutes

- 5.7.5 Industry Rivalry

- 5.8 Pricing Analysis

6 Market Segmentation Analysis (Market Size & Growth Forecasts -Value (USD) and Volume (Units))

- 6.1 By Propulsion Type

- 6.1.1 Pedal Assisted

- 6.1.2 Speed Pedelec

- 6.1.3 Throttle Assisted

- 6.2 By Application Type

- 6.2.1 Cargo / Utility

- 6.2.2 City / Urban

- 6.2.3 Trekking / Mountain

- 6.3 By Battery Type

- 6.3.1 Lead-Acid Battery

- 6.3.2 Lithium-ion Battery

- 6.3.3 Others

- 6.4 By Motor Placement

- 6.4.1 Hub (Front / Rear)

- 6.4.2 Mid-Drive

- 6.5 By Drive Systems

- 6.5.1 Chain Drive

- 6.5.2 Belt Drive

- 6.6 By Motor Power

- 6.6.1 Below 250 W

- 6.6.2 251-350 W

- 6.6.3 351-500 W

- 6.6.4 501-600 W

- 6.6.5 Above 600 W

- 6.7 By Price Band

- 6.7.1 Less than/Equals USD 1,000

- 6.7.2 USD 1,000-1,499

- 6.7.3 USD 1,500-2,499

- 6.7.4 USD 2,500-3,499

- 6.7.5 USD 3,500-5,999

- 6.7.6 Greater than/Equals USD 6,000

- 6.8 By Sales Channel

- 6.8.1 Online

- 6.8.2 Offline

- 6.9 By End Use

- 6.9.1 Commercial Delivery

- 6.9.1.1 Retail and Goods Delivery

- 6.9.1.2 Food and Beverage Delivery

- 6.9.2 Service Providers

- 6.9.3 Personal and Family Use

- 6.9.4 Institutional

- 6.9.5 Others

- 6.9.1 Commercial Delivery

- 6.10 By Country

- 6.10.1 Germany

- 6.10.2 Netherlands

- 6.10.3 France

- 6.10.4 Italy

- 6.10.5 Spain

- 6.10.6 United Kingdom

- 6.10.7 Switzerland

- 6.10.8 Austria

- 6.10.9 Belgium

- 6.10.10 Denmark

- 6.10.11 Sweden

- 6.10.12 Norway

- 6.10.13 Poland

- 6.10.14 Czech Republic

- 6.10.15 Portugal

- 6.10.16 Rest of Europe

7 Competitive Landscape

- 7.1 Key Strategic Moves

- 7.2 Market Share Analysis

- 7.3 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 7.3.1 Accell Group

- 7.3.2 Pon Holdings B.V.

- 7.3.3 Giant Manufacturing Co. Ltd.

- 7.3.4 Trek Bicycle Corporation

- 7.3.5 Riese & Muller GmbH

- 7.3.6 Brompton Bicycle Limited

- 7.3.7 CUBE Bikes

- 7.3.8 Yamaha Motor Co., Ltd.

- 7.3.9 Merida Industry Co. Ltd.

- 7.3.10 VanMoof BV

- 7.3.11 Volt Electric Bikes

- 7.3.12 Pedego Electric Bikes

- 7.3.13 KTM Fahrrad GmbH

- 7.3.14 Fritzmeier Systems GmbH & Co. KG (M1 Sporttechnik)

8 Key Strategic Questions for E-Bikes CEOs

折疊式電動車市場報告:按車型、電池類型、銷售管道、用戶年齡層和地區分類(2026-2034 年)

折疊式電動車市場報告:按車型、電池類型、銷售管道、用戶年齡層和地區分類(2026-2034 年) 全球電動自行車市場:按類別、電池、馬達、系統、應用、速度、電池容量、組件和地區分類-預測(至2035年)

全球電動自行車市場:按類別、電池、馬達、系統、應用、速度、電池容量、組件和地區分類-預測(至2035年) 全球電動自行車市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球電動自行車市場規模、佔有率、趨勢和成長分析報告(2026-2034) 電動自行車市場:2026-2032年全球市場預測(依產品類型、等級、電池類型、馬達類型、功率輸出、車架材料、應用和銷售管道)電動自行車市場:2026-2032年全球市場預測(依產品類型、電池類型、驅動系統、功率輸出、速度類型、應用和銷售管道)折疊式電動自行車市場:依使用者類型、馬達功率、驅動系統和銷售管道分類-2026-2032年全球市場預測

電動自行車市場:2026-2032年全球市場預測(依產品類型、等級、電池類型、馬達類型、功率輸出、車架材料、應用和銷售管道)電動自行車市場:2026-2032年全球市場預測(依產品類型、電池類型、驅動系統、功率輸出、速度類型、應用和銷售管道)折疊式電動自行車市場:依使用者類型、馬達功率、驅動系統和銷售管道分類-2026-2032年全球市場預測 2026-2030年全球折疊式電動自行車市場專業電動自行車市場:依馬達配置、電池容量、價格範圍、應用和分銷管道分類-2026-2032年全球預測電動式自行車市場規模、佔有率、成長率及全球市場分析:按類型、應用和地區的洞察,2026-2034年的預測高階電動自行車市場:2026 年至 2032 年全球預測,按自行車類型、價格範圍、應用、電池容量、通路和馬達功率分類。

2026-2030年全球折疊式電動自行車市場專業電動自行車市場:依馬達配置、電池容量、價格範圍、應用和分銷管道分類-2026-2032年全球預測電動式自行車市場規模、佔有率、成長率及全球市場分析:按類型、應用和地區的洞察,2026-2034年的預測高階電動自行車市場:2026 年至 2032 年全球預測,按自行車類型、價格範圍、應用、電池容量、通路和馬達功率分類。