|

市場調查報告書

商品編碼

1910640

IT服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)IT Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

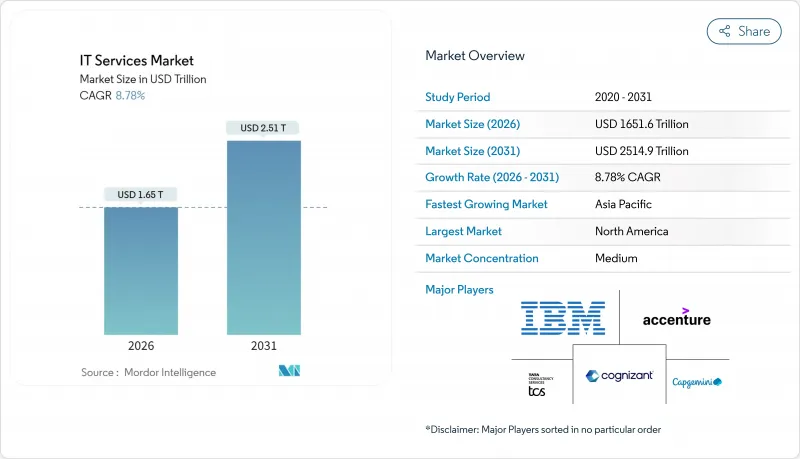

預計到 2026 年,IT 服務市場規模將達到 1,6,516 億美元,高於 2025 年的 1,5,181 億美元。

預計到 2031 年將達到 25,149 億美元,2026 年至 2031 年的複合年成長率為 8.78%。

穩健的數位轉型計劃、企業對人工智慧日益成長的採用以及不斷擴大的雲端原生遷移正在推動市場需求成長。銀行業和醫療保健產業是支出成長最強勁的產業,預計到2024年,隨著各機構對其傳統核心系統進行現代化改造,這兩個產業的支出成長率將分別達到8.7%和15%。提供基於混合雲端和人工智慧工作負載的綜合諮詢、實施和管理服務的供應商正在贏得高價值合約。同時,對價格敏感的外包協議仍然是建立大規模交付流程的基礎。不斷增加的整合活動,包括數十億美元的收購,顯示規模、垂直領域深度和差異化的智慧財產權正在成為贏得企業合約續約的關鍵因素。

全球IT服務市場趨勢與洞察

新冠疫情後加速數位轉型

多重雲端部署的企業已超過 87%,其中 51% 的企業正在投資雲端原生現代化計劃,這些項目整合了應用程式重構、人工智慧服務和資料平台。全球 IT 服務市場如今更青睞那些容器編排管理、微服務和 DevOps 的供應商,而非僅提供簡單遷移服務的供應商。 DXC Technology 的「Cloud Right」方法協助 Ocean Network Express 實現了零停機遷移,為供應商從基礎設施管理轉型為策略業務合作夥伴鋪平了道路。收入來源正轉向諮詢和託管雲端營運服務,這些服務既需要深厚的技術資質,也需要對產業有深刻的洞察。此類合約通常圍繞共用的服務等級成果 (SLA) 構建,從而提高客戶留存率和供應商的單位經濟效益。 Kubernetes、站點可靠性工程 (SRE) 和財務維 (FinOps) 等領域的技能短缺進一步推高了服務費用,也印證了雲端優先計畫對長期成長有最大正面影響的原因。

混合雲端遷移熱潮

預計2022年至2027年間,全球雲端ERP支出將成長近一倍,因為企業正在尋求工作負載可攜性和合規性。到2025年,歐洲企業在IT服務上的支出將達到4,898億歐元(5,535億美元),其中45%將用於雲端舉措。多重雲端策略有助於避免供應商鎖定,但也增加了管治的複雜性,並推動了對諮詢和最佳化服務的需求。資料主權要求促使企業需要本地化的託管基礎設施,從而擴大了近岸和在岸合約。提供認證雲端架構師和託管FinOps人才的供應商正在整個IT服務市場贏得豐厚的合約。

服務價格商品化的壓力

自動化和離岸規模化正在消除常見服務台和基礎設施任務的進入門檻,擠壓傳統外包的利潤空間。客戶越來越傾向於收費模式,迫使供應商證明其服務能帶來實際的業務影響。小規模的競爭對手透過降價來削弱服務,促使能夠交叉銷售高階諮詢和保全服務的現有企業進行整合。預計未來兩年,由此產生的市場洗牌將重塑IT服務市場的競爭格局。

細分市場分析

資安管理服務以 12.18% 的複合年成長率 (CAGR) 成長,是整個 IT 服務市場中成長最快的。企業意識到,專業服務提供者在威脅偵測和事件回應方面能夠超越內部團隊,因此擴大簽訂包含持續合規性監控的長期外包協議。 IT 外包仍佔最大的營收佔有率,達到 28.04%,這主要得益於根深蒂固的成本最佳化需求。然而,商品化工作流程中的利潤率壓縮迫使供應商將外包和諮詢服務打包,並捍衛其定價策略。雲端和平台服務正受益於混合雲端的普及。計劃通常會與 ERP 現代化和資料整合層結合,從而促進交叉銷售。

業務流程外包的需求趨勢也十分有利,其中機器人流程自動化在財務、人力資源和產業專用的後勤部門職能部門尤為突出。隨著複雜性的增加,IT諮詢收入也在成長;企業需要指導來整合人工智慧、邊緣運算和垂直雲端。提供參考架構、遷移加速工具包和特定領域解決方案的供應商正在IT服務市場中佔據越來越大的客戶支出佔有率。

到2031年,中小企業市場將以10.92%的複合年成長率成長,反映出雲端整合式ERP、CRM和網路安全解決方案的普及。付費使用制使中小企業能夠採用以前只有大型企業才能使用的功能,並將實施時間從數月縮短至數週。醫療保健和金融服務業的合規負擔促使中小企業利用外部專業知識,而不是建立內部控制機制,從而擴大了託管服務合作夥伴的潛在收入。

大型企業市場仍佔總營收的69.42%,這主要得益於其龐大的傳統資產,而這些資產需要製定長期的轉型藍圖。融合內部專業中心和外部專業知識的混合模式正變得越來越普遍,為利基供應商創造了高價值的合約機會。企業買家在其招標書中擴大要求供應商提供永續性認證和碳排放報告應對力,這為在IT服務市場中追蹤範圍3排放的供應商開闢了差異化競爭的途徑。

區域分析

2025年,北美將佔全球收入的37.05%,這主要得益於2.7兆美元的企業技術支出以及人工智慧和雲端平台的早期應用。聯邦政府強制設立人工智慧管治委員會的舉措,使得策略諮詢和實施服務的需求制度化。加拿大正在大力推動數位政府專案和自然資源自動化,而墨西哥的近岸提案則吸引尋求文化親和性和智慧財產權保護的美國公司。

至2031年,亞太地區將以11.12%的複合年成長率領先全球。中國正大力推動智慧城市試點和綠色製造發展;印度正利用其作為分銷中心的傳統優勢擴大國內需求;東南亞國協正努力彌合基礎設施差距,以支持跨境電子商務和金融科技的成長。日本和韓國正將投資重點放在先進製造業和電信領域,並大力發展5G和邊緣運算的專業諮詢服務。儘管資訊科技支出日趨成熟,澳洲和紐西蘭仍繼續將網路安全和雲端合規性作為銀行和政府機構的優先事項。

到2025年,歐洲將在IT服務領域投入4,898億歐元(約5,535億美元),其中45%將用於雲端運算專案。 GDPR、DORA和NIS2等法規結構將推動安全和合規方面的支出,確保合格供應商獲得穩定的業務機會。德國主導製造業的數位化,英國將推動金融服務業的轉型,法國、義大利和西班牙將加速採用雲端ERP系統。東歐將發展成為近岸交付中心和現代化服務需求目的地,從而深化整體IT服務市場生態系統。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 新冠疫情後加速數位轉型

- 混合雲端遷移熱潮

- 網路威脅情勢日益嚴峻

- 企業人工智慧和分析支出激增

- 產業特定雲端平台的採用情況

- 以永續性為重點的綠色IT審核

- 市場限制

- 服務價格商業化的壓力

- 全球人才短缺和離職率

- 數據主權面臨的地緣政治障礙

- 範圍 3 碳排放報告的合規成本

- 產業價值鏈分析

- 宏觀經濟因素的影響

- 關鍵法規結構評估

- 技術展望

- 波特五力分析

- 買方的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按服務類型

- IT諮詢與實施支持

- IT外包(ITO)

- 業務流程外包(BPO)

- 資安管理服務

- 雲端平台服務

- 按最終用戶公司規模分類

- 中小企業

- 主要企業

- 按部署模式

- 陸上交付

- 近岸交付

- 離岸交付

- 按最終用戶行業分類

- BFSI

- 製造業

- 政府/公共部門

- 醫療保健和生命科學

- 零售和消費品

- 通訊與媒體

- 物流/運輸

- 能源與公共產業

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 澳洲和紐西蘭

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Accenture plc

- International Business Machines Corporation(IBM)

- Tata Consultancy Services Limited(TCS)

- Infosys Limited

- Cognizant Technology Solutions Corporation

- Capgemini SE

- Wipro Limited

- HCL Technologies Limited

- DXC Technology Company

- Atos SE

- Fujitsu Limited

- NTT DATA Corporation

- CGI Inc.

- L&T Technology Services Limited

- Tech Mahindra Limited

- EPAM Systems Inc.

- Endava plc

- Globant SA

- Mindtree Limited

- Sopra Steria Group SA

- Rackspace Technology Inc.

- Virtusa Corporation

- Persistent Systems Limited

- UST Global Inc.

第7章 市場機會與未來展望

IT services market size in 2026 is estimated at USD 1651.6 billion, growing from 2025 value of USD 1518.1 billion with 2031 projections showing USD 2514.9 billion, growing at 8.78% CAGR over 2026-2031.

Robust digital-transformation agendas, an upswing in enterprise artificial-intelligence adoption, and rising cloud-native migrations are expanding addressable demand. Spending momentum is strongest in banking and healthcare, where 2024 outlays jumped 8.7% and 15% respectively as institutions modernized legacy cores. Providers able to bundle consulting, implementation, and managed services around hybrid-cloud and AI workloads capture premium contracts, while price-sensitive outsourcing engagements continue to anchor large-scale delivery pipelines. Heightened consolidation-including multibillion-dollar acquisitions-shows that scale, vertical depth, and intellectual-property differentiation are now decisive in winning enterprise renewals.

Global IT Services Market Trends and Insights

Digital-transformation acceleration post-COVID-19

Multi-cloud adoption has crossed 87% of enterprises, while 51% are funding cloud-native modernization tracks that bundle application refactoring, AI services and data platforms. The Global IT services market now rewards providers that master container orchestration, micro-services and DevOps over simple lift-and-shift migration. DXC Technology's "Cloud Right" approach enabled Ocean Network Express to achieve zero-downtime migration, showcasing how vendors move from infrastructure caretakers to strategic business partners. Revenue pools are shifting toward advisory and managed cloud operations layers that demand both deep technical credentials and sector insight. These engagements, typically structured around shared service-level outcomes, lift provider stickiness and unit economics. Skills scarcity in Kubernetes, site reliability engineering and FinOps is further buoying service rates, underscoring why cloud-first programmes add the highest positive delta to long-run growth.

Hybrid-cloud migration boom

Global cloud-ERP outlays are on track to nearly double between 2022 and 2027 as enterprises pursue workload portability and regulatory compliance. European firms directed EUR 489.8 billion (USD 553.5 billion) to IT services in 2025, with 45% tagged for cloud initiatives. Multi-cloud strategies help organizations avert vendor lock-in, yet they impose governance complexity that drives demand for advisory and optimization services. Data sovereignty mandates heighten the need for region-specific hosting footprints, bolstering nearshore and onshore engagements. Providers offering certified cloud architects and managed FinOps talent are capturing high-margin contracts across the IT services market.

Service-price commoditization pressure

Automation and offshore scale have erased entry barriers for common help-desk and infrastructure tasks, compressing margins in traditional outsourcing. Clients increasingly demand outcome-based billing, compelling vendors to prove tangible business impact. Smaller rivals undercut pricing, which accelerates consolidation among incumbents able to cross-sell premium consulting and security offerings. The resulting shake-out is likely to realign the competitive order within the IT services market over the next two years.

Other drivers and restraints analyzed in the detailed report include:

- Escalating cyber-threat landscape

- Enterprise AI and analytics spend surge

- Global talent shortage and attrition

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Managed Security Services is growing at a 12.18% CAGR, the steepest rate across the IT services market. Enterprises accept that specialized providers outperform internal teams in threat detection and incident response, prompting long-term outsourcing contracts that include continuous compliance monitoring. IT Outsourcing retains the largest 28.04% revenue position due to entrenched cost-optimization mandates. However, margin compression in commoditized workstreams is pushing vendors to package outsourcing with consulting to protect pricing. Cloud and Platform Services benefit from surging hybrid-cloud adoption; projects frequently bundle ERP modernization with data-integration layers, supporting cross-selling momentum.

Demand dynamics also favor Business Process Outsourcing, especially in finance, HR, and industry-specific back-office workflows where robotic process automation amplifies efficiency gains. IT Consulting revenues rise on complexity: organizations need guidance to harmonize AI, edge computing, and vertical clouds. Vendors that deliver reference architectures, accelerated migration toolkits, and domain-centric solutions increase wallet share across the IT services market.

Small and Medium Enterprises register an 10.92% CAGR through 2031, reflecting democratized access to cloud-delivered ERP, CRM, and cybersecurity bundles. Consumption-based pricing allows SMEs to deploy capabilities historically reserved for large corporations, compressing deployment timelines from months to weeks. Compliance burdens in healthcare and financial services incentivize SMEs to engage external specialists rather than build in-house controls, expanding addressable revenue for managed-service partners.

Large Enterprises still command 69.42% revenue, underpinned by sprawling legacy estates that demand long-duration transformation roadmaps. Hybrid models blending internal centers of excellence with targeted external expertise prevail, securing high-value contracts for niche providers. Enterprise buyers increasingly list sustainability credentials and carbon-reporting readiness in RFPs, offering differentiation avenues for providers that track Scope-3 emissions across the IT services market.

The IT Services Market Report is Segmented by Service Type (IT Consulting and Implementation, and More), End-User Enterprise Size (Small and Medium Enterprises, and More), Deployment Model (Onshore, Nearshore, and More), End-User Vertical (BFSI, Manufacturing, and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America represents 37.05% of 2025 revenue, steered by USD 2.7 trillion in enterprise tech spending and early-adopter behavior toward AI and cloud platforms. Federal mandates requiring AI governance boards have institutionalized demand for strategic advisory and implementation services. Canada advances digital-government programs and natural-resource automation, whereas Mexico's nearshore proposition attracts U.S. firms seeking cultural affinity and IP protection.

Asia-Pacific records the highest 11.12% CAGR through 2031. China scales smart-city pilots and green-manufacturing upgrades, India leverages its delivery-hub heritage while expanding domestic demand, and ASEAN economies close infrastructure gaps to support cross-border e-commerce and fintech growth. Japan and South Korea funnel investments into advanced manufacturing and telecom, spurring niche consulting around 5G and edge computing. Australia and New Zealand, despite mature IT spend, continue prioritizing cybersecurity and cloud compliance in banking and government.

Europe allocates EUR 489.8 billion (USD 553.5 billion) to IT services in 2025, 45% of which funds cloud programs. Regulatory frameworks-GDPR, DORA, and NIS2-propel security and compliance spend, ensuring consistent engagement pipelines for qualified providers. Germany spearheads manufacturing digitization, the United Kingdom leads in financial services transformation, and France, Italy, and Spain scale cloud-ERP rollouts. Eastern Europe develops as both a nearshore delivery basin and a consumer of modernization services, strengthening ecosystem depth across the IT services market.

- Accenture plc

- International Business Machines Corporation (IBM)

- Tata Consultancy Services Limited (TCS)

- Infosys Limited

- Cognizant Technology Solutions Corporation

- Capgemini SE

- Wipro Limited

- HCL Technologies Limited

- DXC Technology Company

- Atos SE

- Fujitsu Limited

- NTT DATA Corporation

- CGI Inc.

- L&T Technology Services Limited

- Tech Mahindra Limited

- EPAM Systems Inc.

- Endava plc

- Globant S.A.

- Mindtree Limited

- Sopra Steria Group SA

- Rackspace Technology Inc.

- Virtusa Corporation

- Persistent Systems Limited

- UST Global Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Digital-transformation acceleration post-COVID-19

- 4.2.2 Hybrid-cloud migration boom

- 4.2.3 Escalating cyber-threat landscape

- 4.2.4 Enterprise AI and analytics spend surge

- 4.2.5 Vertical-specific cloud platforms adoption

- 4.2.6 Sustainability-driven Green-IT audits

- 4.3 Market Restraints

- 4.3.1 Service-price commoditization pressure

- 4.3.2 Global talent shortage and attrition

- 4.3.3 Data-sovereignty geopolitical barriers

- 4.3.4 Scope-3 carbon-reporting compliance costs

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors

- 4.6 Evaluation of Critical Regulatory Framework

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 IT Consulting and Implementation

- 5.1.2 IT Outsourcing (ITO)

- 5.1.3 Business Process Outsourcing (BPO)

- 5.1.4 Managed Security Services

- 5.1.5 Cloud and Platform Services

- 5.2 By End-User Enterprise Size

- 5.2.1 Small and Medium Enterprises (SMEs)

- 5.2.2 Large Enterprises

- 5.3 By Deployment Model

- 5.3.1 Onshore Delivery

- 5.3.2 Nearshore Delivery

- 5.3.3 Offshore Delivery

- 5.4 By End-user Vertical

- 5.4.1 BFSI

- 5.4.2 Manufacturing

- 5.4.3 Government and Public Sector

- 5.4.4 Healthcare and Life-Sciences

- 5.4.5 Retail and Consumer Goods

- 5.4.6 Telecom and Media

- 5.4.7 Logistics and Transport

- 5.4.8 Energy and Utilities

- 5.4.9 Other End-user Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Australia and New Zealand

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 International Business Machines Corporation (IBM)

- 6.4.3 Tata Consultancy Services Limited (TCS)

- 6.4.4 Infosys Limited

- 6.4.5 Cognizant Technology Solutions Corporation

- 6.4.6 Capgemini SE

- 6.4.7 Wipro Limited

- 6.4.8 HCL Technologies Limited

- 6.4.9 DXC Technology Company

- 6.4.10 Atos SE

- 6.4.11 Fujitsu Limited

- 6.4.12 NTT DATA Corporation

- 6.4.13 CGI Inc.

- 6.4.14 L&T Technology Services Limited

- 6.4.15 Tech Mahindra Limited

- 6.4.16 EPAM Systems Inc.

- 6.4.17 Endava plc

- 6.4.18 Globant S.A.

- 6.4.19 Mindtree Limited

- 6.4.20 Sopra Steria Group SA

- 6.4.21 Rackspace Technology Inc.

- 6.4.22 Virtusa Corporation

- 6.4.23 Persistent Systems Limited

- 6.4.24 UST Global Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

大型通訊業者業務與IT服務:全球市場預測(2025-2030)

大型通訊業者業務與IT服務:全球市場預測(2025-2030) 2026年全球網路部署服務市場報告

2026年全球網路部署服務市場報告 IT 服務市場:2026-2032 年全球市場預測(按服務類型、合約模式、最終用戶、組織規模和部署方式分類)2026年全球5G網路部署服務市場報告2026年全球IT服務市場報告2026年全球硬體支援服務市場報告

IT 服務市場:2026-2032 年全球市場預測(按服務類型、合約模式、最終用戶、組織規模和部署方式分類)2026年全球5G網路部署服務市場報告2026年全球IT服務市場報告2026年全球硬體支援服務市場報告 IT 服務市場規模、佔有率和趨勢分析報告:按方法、類型、應用、技術、部署、企業規模、最終用途、地區和細分市場進行預測(2026-2033 年)

IT 服務市場規模、佔有率和趨勢分析報告:按方法、類型、應用、技術、部署、企業規模、最終用途、地區和細分市場進行預測(2026-2033 年) IT 服務市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和解決方案分類Oracle服務市場分析及預測(至 2035 年):依類型、產品類型、服務、技術、元件、應用、部署類型、終端使用者、功能及解決方案分類

IT 服務市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和解決方案分類Oracle服務市場分析及預測(至 2035 年):依類型、產品類型、服務、技術、元件、應用、部署類型、終端使用者、功能及解決方案分類 美國IT服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

美國IT服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)