|

市場調查報告書

商品編碼

1910503

越野車:市佔率分析、產業趨勢與統計、成長預測(2026-2031)Off-road Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

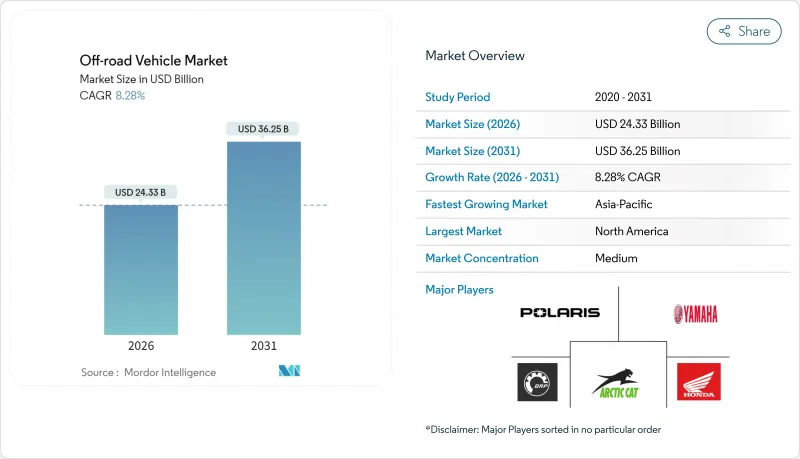

預計到 2026 年,越野車市場規模將達到 243.3 億美元,高於 2025 年的 224.7 億美元,預計到 2031 年將達到 362.5 億美元,2026 年至 2031 年的複合年成長率為 8.28%。

這一成長得益於戶外休閒參與度的提高、電氣化進程的加速以及實用應用領域的拓展,這些因素持續抵消了主要製造商的周期性收入波動。步道基礎設施建設資金的增加、精密農業的日益普及以及軍事機動性現代化項目的推進進一步擴大了市場需求,而以電動方向盤(EPS)、遠程資訊處理和先進懸吊系統為核心的技術融合,則增強了產品對消費者和商業用戶的價值提案。儘管主要供應商在 2024 年的收入有所下降,但越野車市場透過向電動車型多元化發展、獲得專業國防合約以及拓展基於訂閱的互聯服務,展現出了強大的韌性,從而鞏固了長期的收入來源。

全球越野車市場趨勢與洞察

戶外休閒旅遊激增

2024年,戶外休閒為美國GDP貢獻了1.2兆美元(國內生產總值的2.3%),並創造了大量就業機會。參與人數的增加推動了全地形車(ATV)和多用途車(UTV)的購買,用於越野騎行和長途旅行。摩托車和全地形車創造了當年大部分的經濟增加價值,證實了越野車市場的強勁需求。各州的津貼項目進一步放大了這一影響:科羅拉多的戶外休閒基金為相關計劃撥出了大量資金,而奧勒岡州的配套津貼則促進了當地製造業叢集的發展。步道系統產生了強大的溢出效應。明尼蘇達州的雪上摩托車網路全年都能帶來可觀的旅遊收入,增強了對當地經濟的乘數效應,並穩定了季節性車輛銷售。

國防部戰術全地形車/多用途車採購

國防機構正在尋求輕型機動裝備,用於邊防安全、特種作戰以及在複雜地形中的後勤保障。印度即將發布的北部邊境競標明確要求車輛具備直升機吊掛能力、四座佈局以及自主導航選項,以最大限度地提高戰術性柔軟性。芬蘭主導的歐洲FAMOUS計畫專注於北極作戰,該計畫研發的車輛能夠在攝氏零下46度的低溫下啟動,並在解凍期間具備兩棲作戰能力。美國每年都會撥出一定資金用於購買超輕型作戰車輛(ULCV),其空載重量低於4500磅,續航里程達250英里。這些項目推動了供應商開發模組化底盤,以便加裝甲套件、反無人機感測器和混合動力傳動系統。儘管民用需求有周期性波動,但累積訂單依然充足。

電動動力傳動系統所需的鋰供應鏈正變得越來越緊張。

中國目前佔全球鋰精煉量五分之三以上,電池產量佔五分之四,隨著需求激增,全球原始設備製造商(OEM)面臨風險。儘管美國已根據《通貨膨脹控制法案》撥款用於國內鋰加工,但核准障礙和社區擔憂導致礦山開採延遲。電化學萃取技術新興企業承諾提供綠色解決方案,但仍處於商業化前期。在供應來源多元化之前,電池價格可能持續波動,這可能會限制總擁有成本(TCO)與傳統電池價格持平的實現,而實現這一目標將加速電動全地形車(ATV)的普及,尤其是在對價格敏感的發展中市場。

細分市場分析

多功能越野車(UTV)和並排式越野車(Side-by-side)集載客、載貨和懸吊性能於一體,預計到2025年將佔據越野車市場50.68%的佔有率。在休閒、農業和國防領域需求的推動下,該衍生市場實現了強勁成長。電動UTV目前正以8.32%的複合年成長率(CAGR)快速成長,這得益於汽車製造商(OEM)推出的15kWh電池組,這些電池組可使UTV最高時速達到80公里/小時,充電時間縮短至3小時以內。

在那些對車身寬度有嚴格限制、更適合窄底盤的地區,全地形車 (ATV) 的需求仍然強勁。同時,在氣候嚴寒的地區,兩棲車和雪上摩托車等小眾車型的需求也持續存在。差異化競爭優勢主要體現在可調式懸吊、北極星動力公司的即時閥門架構以及配備觸控螢幕 Ride Command 系統的數位化駕駛艙等。因此,我們的產品組合兼顧了傳統內燃機 (ICE) 車型的產量和新興的電氣化成長動力,從而能夠有效應對動力系統相關的不確定性。

到2025年,運動休閒領域將佔越野車市場的41.05%,這主要得益於數百萬美國人參與戶外活動,導致越野車道使用率創歷史新高。執法機關的需求預計將以8.35%的複合年成長率成長,這主要受採購機構尋求輕型戰術機動車輛(配備直升機吊掛和混合靜音監視模式)的推動。

農業和林業將採用配備動力輸出軸驅動農具的中排量多用途越野車(UTV),建設公司將採購重型車輛用於偏遠地區的後勤保障,而諸如嚮導式越野探險等新興旅遊模式將進一步拓展UTV的應用場景。因此,即使消費者可支配支出下降,多用途適應性仍將維持UTV的基本銷售。

到 2025 年,內燃機將佔非道路車輛市場佔有率的 83.05%,這得益於廣泛的燃料供應基礎設施和成熟的供應鏈;而電池電動車車型將實現最高的複合年成長率,達到 8.30%,這反映了政策激勵和電池成本的下降。

這款混合增程器將10kWh電池組與緊湊型發電機相結合,在不犧牲低速扭矩的前提下延長了運作時間,從而消除了客戶的顧慮。雖然氫燃料電池原型仍處於研發階段,但它為需要在寒冷氣候下快速加氫的重型救援車輛指明了方向。動力系統的多樣化不僅降低了監管風險,還建構了一個以電池租賃和回收為中心的新型供應商生態系統。

區域分析

2025年,北美將佔據越野車市場37.84%的佔有率,這主要得益於戶外休閒對GDP的顯著貢獻以及各州補貼的廣泛步道網路。雪帶各州每年在維護項目上投入巨資,以刺激旅遊收入。威斯康辛州和阿拉斯加州對符合條件的步道維護費用提供100%的補貼,即使在經濟低迷時期也能維持穩定的需求。經銷商融資合作關係(例如,謝菲爾德金融公司與北極星公司續約的協議)方便了買家獲得融資,並維持了展示室的周轉率。然而,加拿大省級保護區的法規帶來了營運上的複雜性,迫使汽車製造商提供更安靜的動力傳動系統和符合排放氣體的引擎,以滿足許可標準。

預計到2031年,亞太地區將以8.42%的複合年成長率實現最快增速,這主要得益於都市化的中產階級消費者對戶外生活方式品牌的青睞,以及各國政府對農村交通的大力投入。在印度,受探險旅遊行銷和農業機械化程度提高的推動,全地形車(ATV)銷量顯著成長。像CFMOTO這樣的區域性整車製造商利用其垂直整合的供應鏈,實現了價格競爭力,贏得了出口契約,並佔據了全球五分之二的市場佔有率。

歐洲的成長雖然緩慢,但監管要求與電氣化進程相契合。針對非道路機械的第五階段排放氣體法規增加了後處理裝置和替代動力傳動系統的研發投入,間接推動了混合動力和燃料電池技術的創新。將於2028年生效的新NRMM法規設定了70輛的小規模生產門檻,為新興電動車製造商更容易獲得認證鋪平了道路。北歐國家已推出長期步道維護補助以促進旅遊業發展,德國和奧地利也考慮在其阿爾卑斯山區採取類似措施。因此,儘管監管負擔將在短期內抑制銷量,但長期需求將轉向低排放車型,使歐洲供應商能夠透過溢價收回投資。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 戶外休閒旅遊激增

- 國防部戰術全地形車/多用途車採購

- 中型農場的快速機械化

- 採用先進的電動方向盤(EPS)和遠端資訊處理技術

- 無人機拍攝對低噪音電動全地形車的需求

- 北歐越野滑雪道維護補助金擴大了騎乘網路

- 市場限制

- 高昂的初始成本和生命週期成本

- 電動動力傳動系統所需的鋰供應鏈十分緊張。

- 加強傷害賠償法規並引入速度限制

- 在保護區內禁止使用

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模及成長預測(價值(美元)及銷售量(單位))

- 按車輛類型

- 全地形車(ATV)

- 多用途作業車輛(UTV)/並排式全地形車

- 越野摩托車

- 雪上摩托車

- 兩棲特種越野車

- 透過使用

- 運動與休閒

- 農業和林業

- 工業與建築

- 軍事和執法機關

- 其他商業活動(旅遊、搜救)

- 依推進類型

- 內燃機(汽油/柴油)

- 混合

- 電池式電動車

- 氫燃料電池

- 按引擎排氣量(cc)

- 排氣量低於400cc

- 400-800 cc

- 超過800cc

- 按輸出功率(千瓦)

- 小於50千瓦

- 50~100 kW

- 100千瓦或以上

- 按驅動類型

- 兩輪驅動

- 四輪驅動/全輪驅動

- 按座位數

- 1人

- 2人

- 3 位或以上客人

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 亞太其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 埃及

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Polaris Inc.

- Bombardier Recreational Products Inc.(Can-Am)

- Yamaha Motor Corp.

- Textron Inc.(Arctic Cat)

- Kawasaki Heavy Industries Ltd.

- Suzuki Motor Corp.

- Honda Motor Co. Ltd.

- CFMOTO Powersports Inc.

- Kwang Yang Motor Co. Ltd.(Kymco)

- American LandMaster

- Tracker Off-Road(Bass Pro Shops)

- Kubota Corp.(RTV)

- John Deere(Gator)

- Mahindra & Mahindra Ltd.

- Segway Powersports

- Hisun Motors Corp.

- Linhai Group

- TGB(Taiwan Golden Bee)

- DRR USA

第7章 市場機會與未來展望

Off-road Vehicle Market size in 2026 is estimated at USD 24.33 billion, growing from 2025 value of USD 22.47 billion with 2031 projections showing USD 36.25 billion, growing at 8.28% CAGR over 2026-2031.

This growth arises from a confluence of rising outdoor recreation participation, accelerating electrification, and expanding utility applications that continue to offset cyclical revenue fluctuations among leading manufacturers. Growing trail infrastructure funding, precision-farming uptake, and military mobility modernization programs further widen demand pools, while technology convergence around electronic power steering (EPS), telematics, and advanced suspension systems enhances value propositions for both consumer and commercial buyers. Even with revenue contractions at major suppliers during 2024, the off-road vehicle market shows resilience through diversification into electric variants, specialty defense contracts, and subscription-based connectivity services that solidify long-term revenue streams.

Global Off-road Vehicle Market Trends and Insights

Surge In Outdoor Recreational Tourism

Outdoor recreation contributed USD 1.2 trillion to U.S. GDP in 2024, equal to 2.3% of national output and supporting multiple jobs. Participation increased, spurring ATV and UTV purchases for trail riding and overlanding. In 2024, motorcycling and ATVing generated a large share of value-added economic output, underscoring strong demand in the off-road vehicle market. State grant programs amplify the effect: Colorado's Outdoor Recreation Fund distributed a massive amount to access projects, while Oregon's matching grants nurtured rural manufacturing clusters. Trail systems create powerful spillovers; Minnesota's snowmobile network generates significant annual tourism revenue, reinforcing the sector's multiplier effect on local economies and stabilizing seasonal vehicle sales.

Tactical ATV/UTV Procurement By Defense Forces

Defense agencies seek light mobility assets for border patrol, special operations, and logistics in difficult terrain. India's upcoming northern-border tender specifies helicopter-sling capability, four-seat layouts, and autonomous navigation options to maximize tactical flexibility. Europe's FAMOUS program, coordinated by Finland, focuses on Arctic operability with vehicles tolerating -46 °C start-up and amphibious functionality for thaw periods. The United States allocates some amount annually to acquire Ultra-Light Combat Vehicles with 4,500-pound curb-weight caps and 250-mile range requirements. Such multi-program momentum encourages vendors to develop modular chassis that accept armor kits, counter-drone sensors, and hybrid powertrains, strengthening order backlogs despite civilian cyclical swings.

Lithium Supply-Chain Crunch For E-Powertrains

China currently refines more than three-fifths of global lithium and fabricates four-fifths of batteries, creating exposure for global OEMs as demand surges. The United States allocated funding under the Inflation Reduction Act for domestic processing, but permitting hurdles and community concerns are delaying mine openings. Electro-chemical extraction startups promise lower-impact solutions yet remain pre-commercial. Until diversified supply materializes, battery prices may remain volatile, constraining the total-cost parity that accelerates electric ATV adoption, particularly in price-sensitive developing markets.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Mechanization Of Midsize Farms

- Adoption Of Advanced EPS & Telematics

- Rising Injury-Related Regulations & Speed Caps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

UTVs and side-by-sides captured 50.68% of the off-road vehicle market share in 2025 by blending passenger capacity, cargo utility, and suspension sophistication. The segment reached a robust level of off-road vehicle market size, buoyed by recreation, agriculture, and defense orders. Electric UTV derivatives now post the fastest 8.32% CAGR as OEMs introduce 15 kWh battery packs delivering 80 km/h top speed and sub-3-hour recharge cycles.

Demand for all-terrain vehicles (ATVs) remains robust in regions with strict width restrictions that favor narrower chassis. In contrast, niche demand for amphibious and snowmobile platforms persists where climatic extremes prevail. Competitive differentiation hinges on adjustable suspension, Polaris's DYNAMIX live valve architecture, and cabin digitization through touchscreen ride-command systems. The vehicle-type portfolio, therefore, balances legacy ICE volumes against emerging electric growth vectors, enabling OEMs to hedge against propulsion uncertainty.

Sports and recreation account for 41.05% of the off-road vehicle market in 2025, benefiting from record trail participation as millions of Americans venture outdoors. Military and law enforcement demand will escalate at an 8.35% CAGR as procurement agencies seek light tactical mobility with helicopter-sling compatibility and hybrid silent-watch modes.

Agriculture and forestry absorb mid-displacement UTVs outfitted with PTO-driven implements, while construction firms requisition high-payload units for remote-site logistics. Emerging tourism concepts such as guided overlanding expeditions further widen commercial use cases. Multi-role adaptability, therefore, sustains baseline volumes even when consumer discretionary spending dips.

Internal-combustion engines commanded 83.05% of the off-road vehicle market share in 2025, backed by ubiquitous fueling infrastructure and mature supply chains. Battery-electric models, however, record the steepest 8.30% CAGR, reflecting policy push and falling cell costs.

Hybrid range-extender concepts bridge customer anxiety by pairing 10 kWh packs with compact generators, extending runtime without compromising low-speed torque. Hydrogen fuel-cell prototypes remain R&D efforts but signal pathways for heavy-duty rescue fleets requiring rapid cold-weather refueling. Propulsion diversification mitigates regulatory risks while inviting new supplier ecosystems around battery leasing and recycling.

The Off-Road Vehicle Market Report is Segmented by Vehicle Type (All-Terrain Vehicles and More), Application (Sports & Recreation and More), Propulsion Type (Internal-Combustion and More), Engine Displacement (Less Than 400 Cc and More), Power Output (Less Than 50 KW and More), Drive Type (2-Wheel Drive and More), Seating Capacity, and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

North America secured 37.84% of off-road vehicle market share in 2025, underpinned by the outdoor recreation GDP contribution and extensive trail networks subsidized by state grants. Snowbelt states invested huge amount annually in grooming programs that stimulated in tourism receipts, while Wisconsin and Alaska reimbursed 100% of eligible trail maintenance costs, anchoring steady demand even during economic slowdowns. Dealer financing partnerships, such as Sheffield Financial's renewal with Polaris, ease credit access for buyers and sustain showroom turnover. Nevertheless, conservation-area restrictions across Canadian provinces introduce operational complexity, nudging OEMs to supply quieter powertrains and emission-compliant engines to satisfy permitting criteria.

Asia-Pacific delivers the fastest 8.42% CAGR through 2031 as urbanizing middle-class consumers embrace outdoor lifestyle brands and governments fund rural connectivity. India's ATV sales grew drastically which was supported by adventure-tourism marketing and agricultural mechanization drives. Regional OEMs such as CFMOTO leverage vertically integrated supply chains to offer competitive pricing, enabling them to capture export contracts and reach two-fifth global market share.

Europe's growth lags but regulatory thrust aligns with electrification imperatives. Stage V emission norms for non-road machinery elevate R&D spending on after-treatment and alternative powertrains, indirectly spurring innovation in hybrid and fuel-cell concepts. New NRMM rules effective 2028 set small-series thresholds of 70 units, granting boutique electric startups manageable certification pathways. Nordic countries deploy long-run trail-maintenance subsidies to catalyze tourism, a template that Germany and Austria now evaluate for alpine regions. Consequently, although compliance burdens restrain short-term volumes, long-term demand will pivot toward low-emission models, allowing European suppliers to recoup investments through premium pricing.

- Polaris Inc.

- Bombardier Recreational Products Inc. (Can-Am)

- Yamaha Motor Corp.

- Textron Inc. (Arctic Cat)

- Kawasaki Heavy Industries Ltd.

- Suzuki Motor Corp.

- Honda Motor Co. Ltd.

- CFMOTO Powersports Inc.

- Kwang Yang Motor Co. Ltd. (Kymco)

- American LandMaster

- Tracker Off-Road (Bass Pro Shops)

- Kubota Corp. (RTV)

- John Deere (Gator)

- Mahindra & Mahindra Ltd.

- Segway Powersports

- Hisun Motors Corp.

- Linhai Group

- TGB (Taiwan Golden Bee)

- DRR USA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge In Outdoor Recreational Tourism

- 4.2.2 Tactical ATV/UTV Procurement By Defense Forces

- 4.2.3 Rapid Mechanization Of Midsize Farms

- 4.2.4 Adoption Of Advanced EPS & Telematics

- 4.2.5 Demand For Low-Noise E-Atvs For Drone Cinematography

- 4.2.6 Nordic Trail-Maintenance Subsidies Expanding Riding Networks

- 4.3 Market Restraints

- 4.3.1 High Upfront & Lifecycle Costs

- 4.3.2 Lithium Supply-Chain Crunch For E-Powertrains

- 4.3.3 Rising Injury-Related Regulations & Speed Caps

- 4.3.4 Conservation-Area Usage Bans

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Vehicle Type

- 5.1.1 All-Terrain Vehicles (ATV)

- 5.1.2 Utility Task Vehicles (UTV) / Side-by-Sides

- 5.1.3 Dirt / Off-road Motorcycles

- 5.1.4 Snowmobiles

- 5.1.5 Amphibious & Specialty ORVs

- 5.2 By Application

- 5.2.1 Sports & Recreation

- 5.2.2 Agriculture & Forestry

- 5.2.3 Industrial & Construction

- 5.2.4 Military & Law-Enforcement

- 5.2.5 Other Commercial (tourism, search-and-rescue)

- 5.3 By Propulsion Type

- 5.3.1 Internal-Combustion (Gasoline / Diesel)

- 5.3.2 Hybrid

- 5.3.3 Battery-Electric

- 5.3.4 Hydrogen Fuel-Cell

- 5.4 By Engine Displacement (cc)

- 5.4.1 Less than 400 cc

- 5.4.2 400 - 800 cc

- 5.4.3 More than 800 cc

- 5.5 By Power Output (kW)

- 5.5.1 Less than 50 kW

- 5.5.2 50 - 100 kW

- 5.5.3 More than 100 kW

- 5.6 By Drive Type

- 5.6.1 2-Wheel Drive

- 5.6.2 4-Wheel / All-Wheel Drive

- 5.7 By Seating Capacity

- 5.7.1 1 Rider

- 5.7.2 2 Riders

- 5.7.3 More than or equal to 3 Passengers

- 5.8 By Geography

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Rest of North America

- 5.8.2 South America

- 5.8.2.1 Brazil

- 5.8.2.2 Argentina

- 5.8.2.3 Rest of South America

- 5.8.3 Europe

- 5.8.3.1 Germany

- 5.8.3.2 France

- 5.8.3.3 United Kingdom

- 5.8.3.4 Italy

- 5.8.3.5 Spain

- 5.8.3.6 Russia

- 5.8.3.7 Rest of Europe

- 5.8.4 Asia-Pacific

- 5.8.4.1 China

- 5.8.4.2 Japan

- 5.8.4.3 India

- 5.8.4.4 South Korea

- 5.8.4.5 Australia

- 5.8.4.6 Rest of Asia-Pacific

- 5.8.5 Middle East and Africa

- 5.8.5.1 United Arab Emirates

- 5.8.5.2 Saudi Arabia

- 5.8.5.3 Turkey

- 5.8.5.4 Egypt

- 5.8.5.5 South Africa

- 5.8.5.6 Rest of Middle East and Africa

- 5.8.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Polaris Inc.

- 6.4.2 Bombardier Recreational Products Inc. (Can-Am)

- 6.4.3 Yamaha Motor Corp.

- 6.4.4 Textron Inc. (Arctic Cat)

- 6.4.5 Kawasaki Heavy Industries Ltd.

- 6.4.6 Suzuki Motor Corp.

- 6.4.7 Honda Motor Co. Ltd.

- 6.4.8 CFMOTO Powersports Inc.

- 6.4.9 Kwang Yang Motor Co. Ltd. (Kymco)

- 6.4.10 American LandMaster

- 6.4.11 Tracker Off-Road (Bass Pro Shops)

- 6.4.12 Kubota Corp. (RTV)

- 6.4.13 John Deere (Gator)

- 6.4.14 Mahindra & Mahindra Ltd.

- 6.4.15 Segway Powersports

- 6.4.16 Hisun Motors Corp.

- 6.4.17 Linhai Group

- 6.4.18 TGB (Taiwan Golden Bee)

- 6.4.19 DRR USA

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

非公路用車輛照明市場-2026-2032年全球市場預測

非公路用車輛照明市場-2026-2032年全球市場預測 全球越野車市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球越野車市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球休閒越野車市場報告2026年全球越野車市場報告2026年全球非公路用車輛照明市場報告

2026年全球休閒越野車市場報告2026年全球越野車市場報告2026年全球非公路用車輛照明市場報告 全球非公路用塑膠市場:依材料類型、製程類型、最終用戶和地區分類-預測(至2030年)

全球非公路用塑膠市場:依材料類型、製程類型、最終用戶和地區分類-預測(至2030年) 日本越野車市場規模、佔有率、趨勢和預測:按產品、地區分類,2026-2034年非公路用電氣設備市場按產品類型、推進類型、功率輸出、應用和分銷管道分類 - 全球預測(2026-2032 年)

日本越野車市場規模、佔有率、趨勢和預測:按產品、地區分類,2026-2034年非公路用電氣設備市場按產品類型、推進類型、功率輸出、應用和分銷管道分類 - 全球預測(2026-2032 年) 越野車市場-全球產業規模、佔有率、趨勢、機會及預測(按車輛類型(全地形車和多用途車)、應用類型、地區和競爭格局分類,2021-2031年預測)

越野車市場-全球產業規模、佔有率、趨勢、機會及預測(按車輛類型(全地形車和多用途車)、應用類型、地區和競爭格局分類,2021-2031年預測) 越野車市場規模、佔有率及成長分析(按車輛類型、動力方式、應用領域及地區分類)-2026-2033年產業預測

越野車市場規模、佔有率及成長分析(按車輛類型、動力方式、應用領域及地區分類)-2026-2033年產業預測