|

市場調查報告書

商品編碼

1906958

北美農業機械市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)North America Agricultural Machinery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

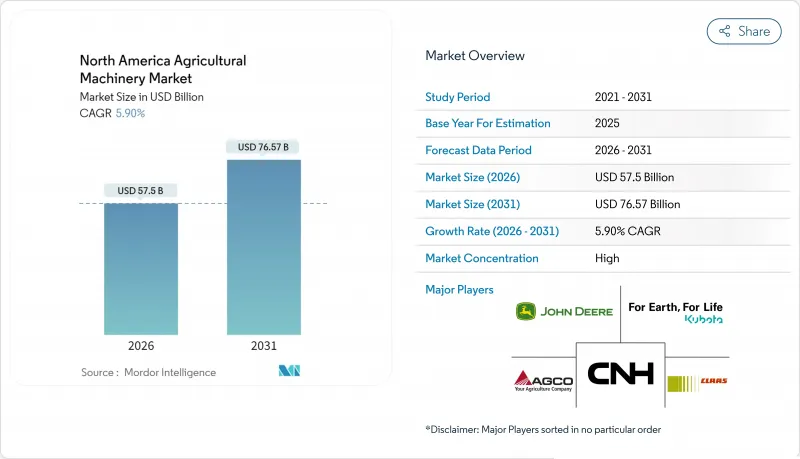

預計北美農業機械市場規模將從 2025 年的 543 億美元成長到 2026 年的 575 億美元,到 2031 年將達到 765.7 億美元,2026 年至 2031 年的複合年成長率為 5.9%。

儘管2024年高利率和大宗商品價格波動限制了資本支出,但機械化需求仍持續成長,反映出市場擴張的趨勢。結構性勞動力短缺、鼓勵設備升級的聯邦補貼計畫以及精密農業的快速普及,都繼續支撐著設備訂單。在2025年國際消費電子展(CES)上展示的自主功能,正在加速設備更早的更換週期,因為農民越來越重視軟體相容性,其重要性不亞於馬力。同時,灌溉現代化,尤其是在缺水的墨西哥,正在擴大專業設備製造商的潛在基本客群。由於主要原始設備製造商(OEM)將嵌入式金融服務、軟體訂閱和經銷商支援打包在一起,以客戶維繫並穩定收入,市場競爭仍然激烈。

北美農業機械市場趨勢與洞察

強勁的農業收入前景和補貼計劃

聯邦折舊免稅額激勵和直接津貼正在增強資本預算的韌性。光是美國農業部(USDA)的「氣候智慧型商品計畫」自2024年以來就已撥款超過30億美元,用於購買旨在減少排放和提高效率的設備。第179條法規允許每個課稅年度最高扣除116萬美元,以抵銷更高的借貸成本。中型生產商正在加快採購,以獲得補貼和稅收優惠。經銷商回饋表明,市場對配備遠端資訊處理系統以追蹤永續性。因此,北美農業機械市場擁有可預測的補貼訂單基礎,從而緩解了需求的周期性下降。

勞動力短缺和工資上漲

農村勞動參與率持續下降,迫使農場將傳統上由人工完成的工作機械化。墨西哥2024年的收成下滑凸顯了勞動力短缺可能阻礙生產。自動噴灑器和機器人收割機減少了田間勞動力,並限制了薪資成長超過整體通貨膨脹率。原始設備製造商(OEM)的演示表明,整合機器視覺可以減少農藥用量,並進一步抵消人事費用。糧倉業者也在利用人工智慧感測器提高自動化程度,使設施運作。因此,持續的勞動力短缺將繼續支持全部區域對先進設備的長期需求。

先進機械設備的高昂初始成本與維修成本

到2024年,高功率曳引機的售價將超過40萬美元,而精準改裝則需額外花費每台5萬至10萬美元。現代引擎和軟體需要專業技術人員,但這類人才仍然短缺,進一步推高了總擁有成本。約87%的經銷商難以找到合格的維修人員。延長保固和維修合約雖然可以降低不確定性,但也會使購買價格增加1.5萬至2.5萬美元。因此,許多農民選擇維修超過10年的設備,推遲技術升級,並在關鍵的農忙時期增加燃料消費量。結果,中小農場往往等到季末折扣時才購買新設備,這擠壓了經銷商的利潤空間,並延長了設備的更新週期。

細分市場分析

到2025年,曳引機將維持其在北美農業機械市場47.30%的佔有率,鞏固其在整體種植的核心地位。這一領域受益於在5萬英畝土地上測試的自動駕駛技術,這些技術證明了即時運作的有效性,並逐漸消除了人們對無人耕作的疑慮。然而,在水資源短缺緩解計劃的推動下,灌溉設備預計到2031年將以13.4%的複合年成長率成長,超過所有其他設備類別。隨著墨西哥加速向中心支軸式噴灌系統轉型,預計北美灌溉設備市場規模在此期間將顯著成長。

同時,隨著精密農業技術將需求轉向變數施肥,犁和中耕機等次要類別也呈現溫和成長。在收割方面,穀物品質感測器和產量測繪技術的整合,使得傳統的六年聯合收割機更換週期提前。牧場和飼料設備受益於美國中西部北部和加拿大大平原地區酪農養殖和畜牧業的擴張。此外,「其他」類別的新興產品包括可進行除草、定點噴灑和土壤監測的自主機器人。久保田的KATR機器人就是一個多功能設計的典範,它模糊了傳統設備的界線。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 強勁的農業收入前景和補貼計劃

- 勞動力短缺加劇和薪資壓力上升

- 精密農業的引進正在加速,設備升級也不斷推進。

- 透過OEM嵌入式融資提高購買力

- 基於訂閱的機器使用模式

- 美國氣候智慧型補助促進低排放設備的發展

- 市場限制

- 先進機械設備的高昂初始成本與維修成本

- 大宗商品價格波動阻礙了資本投資週期。

- 利率主導的信貸緊縮影響了農場層面

- 電動曳引機用電池級半導體的供應受限

- 監管環境

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按類型

- 聯結機

- 不到40馬力

- 40-100馬力

- 超過100馬力

- 四驅曳引機

- 裝置

- 犁

- 光環

- 耕耘機和分蘗機

- 其他設備

- 灌溉機械

- 噴灌

- 滴灌

- 其他灌溉

- 收割機

- 結合

- 飼料收割機

- 其他收割機

- 乾草和飼料機械

- 割草機

- 打包機

- 其他乾草和飼料機械

- 其他類型

- 聯結機

- 按地區

- 美國

- 加拿大

- 墨西哥

- 北美其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Deere & Company

- CNH Industrial NV

- AGCO Corporation

- Kubota Corporation

- CLAAS KGaA mbH

- Mahindra & Mahindra Limited

- Netafim USA Inc.

- Lindsay Corporation

- Trimble Inc.

- Horsch Maschinen GmbH

- KUHN SAS

- Bernard Krone Holding SE & Co. KG

- The Toro Company

- Vermeer Corporation

- JC Bamford Excavators Ltd.

第7章 市場機會與未來展望

The North America agricultural machinery market is expected to grow from USD 54.3 billion in 2025 to USD 57.5 billion in 2026 and is forecast to reach USD 76.57 billion by 2031 at 5.9% CAGR over 2026-2031.

The expansion reflects persistent mechanization demand despite elevated interest rates and commodity price swings that limited capital spending in 2024. Structural labor shortages, federal subsidy programs that encourage fleet renewal, and rapid precision-ag adoption continue to underpin equipment orders. Autonomous capabilities showcased at Consumer Electronics Show (CES) 2025 are accelerating early replacement cycles because farms now weigh software compatibility on par with horsepower. Simultaneously, irrigation modernization, especially in water-stressed Mexico, widens the addressable base for specialized equipment makers. Competitive dynamics remain intense as leading OEMs bundle embedded finance, software subscriptions, and dealer support to retain customers and stabilize revenue.

North America Agricultural Machinery Market Trends and Insights

Robust Farm-Income Outlook and Subsidy Programs

Federal depreciation allowances and direct grants keep capital budgets resilient. The USDA Climate-Smart Commodities program alone has allocated more than USD 3 billion since 2024 for equipment that lowers emissions and improves efficiency. Section 179 rules allow deductions up to USD 1.16 million per tax year, offsetting higher borrowing costs. Mid-sized growers respond by front-loading purchases to capture both grant and tax benefits. Dealer feedback indicates stronger demand for mid-horsepower tractors equipped with telematics that document sustainability metrics required for grant compliance. As a result, the North America agricultural machinery market enjoys a predictable baseline of subsidized orders that cushions cyclical demand dips.

Rising Labor Scarcity and Wage Inflation

Rural workforce participation keeps falling, which pushes farms to mechanize tasks once handled manually. Mexico's crop yield setbacks in 2024 underscore how labor shortages can throttle production. Autonomous sprayers and robotic harvest aids reduce field crews and curb escalating wages that now outstrip general inflation. OEM demonstrations prove that integrated machine-vision lowers chemical use, which further offsets labor costs. Grain-elevator operators also automate with AI-enabled sensors that let facilities run at night without staff oversight. Persistent worker scarcity, therefore, sustains long-term demand for advanced equipment across the region.

High Upfront and Maintenance Costs of Advanced Machinery

A high-horsepower tractor exceeded USD 400,000 in 2024, while precision retrofits add USD 50,000-100,000 per unit. Total ownership costs climb further because modern engines and software demand specialized technicians that remain scarce. Nearly 87% of dealers struggle to hire qualified service staff. Extended warranties and service contracts ease uncertainty, yet they add another USD 15,000-25,000 to the purchase price. Many producers, therefore, refurbish decade-old machines, which postpones technology upgrades and raises fuel consumption during critical field windows. As a result, small and mid-sized farms often delay purchases until late-season discounting emerges, compressing dealer margins and extending replacement cycles.

Other drivers and restraints analyzed in the detailed report include:

- Precision-Agriculture Adoption Accelerating Equipment Replacement

- USDA Climate-Smart Grants Driving Low-Emission Equipment

- Volatile Commodity Prices Curbing CAPEX Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tractors maintained a 47.30% share of the North America agricultural machinery market in 2025, underscoring their central role across crop operations. The segment benefits from autonomous retrofits tested on 50,000 acres, validating real-world uptime and lowering skepticism about driverless tillage. Yet irrigation machinery, supported by water-scarcity mitigation projects, is projected to register a 13.4% CAGR through 2031, outpacing every other equipment class. The North America agricultural machinery market size for irrigation equipment is forecast to show a significant growth during the period as center-pivot conversions accelerate in Mexico.

Secondary categories such as plows and cultivators grow modestly because precision tech shifts demand toward variable-rate applications. In harvesting, integrated grain-quality sensors and yield mapping push farms to upgrade combines earlier than the traditional 6-year cycle. Haying and forage machinery benefits from dairy and beef expansion in the Upper Midwest and Canadian Prairies, while the other types bucket now covers autonomous robots that perform weeding, spot spraying, and soil monitoring. Kubota's KATR robot exemplifies a multifunctional design that blurs traditional equipment lines.

The North America Agricultural Machinery Market Report is Segmented by Type (Tractor, Equipment, Irrigation Machinery, Harvesting Machinery, Haying and Forage Machinery, Other Types) and Geography (United States, Canada, Mexico, Rest of North America). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Deere & Company

- CNH Industrial N.V.

- AGCO Corporation

- Kubota Corporation

- CLAAS KGaA mbH

- Mahindra & Mahindra Limited

- Netafim USA Inc.

- Lindsay Corporation

- Trimble Inc.

- Horsch Maschinen GmbH

- KUHN SAS

- Bernard Krone Holding SE & Co. KG

- The Toro Company

- Vermeer Corporation

- J.C. Bamford Excavators Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Robust farm-income outlook and subsidy programs

- 4.2.2 Rising labor scarcity and wage inflation

- 4.2.3 Precision-ag adoption accelerating equipment replacement

- 4.2.4 OEM embedded-finance boosting purchasing power

- 4.2.5 Subscription-based machinery access models (under-reported)

- 4.2.6 USDA Climate-Smart grants driving low-emission equipment (under-reported)

- 4.3 Market Restraints

- 4.3.1 High upfront and maintenance costs of advanced machinery

- 4.3.2 Volatile commodity prices curbing CAPEX cycles

- 4.3.3 Interest-rate-driven credit tightening at farm level

- 4.3.4 Battery-grade semiconductor supply constraints for e-tractors (under-reported)

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Tractor

- 5.1.1.1 Less Than 40 HP

- 5.1.1.2 40 to 100 HP

- 5.1.1.3 More than 100 HP

- 5.1.1.4 4WD Tractors

- 5.1.2 Equipment

- 5.1.2.1 Plows

- 5.1.2.2 Harrows

- 5.1.2.3 Cultivators and Tillers

- 5.1.2.4 Other Equipment

- 5.1.3 Irrigation Machinery

- 5.1.3.1 Sprinkler

- 5.1.3.2 Drip

- 5.1.3.3 Other Irrigation

- 5.1.4 Harvesting Machinery

- 5.1.4.1 Combine Harvesters

- 5.1.4.2 Forage Harvesters

- 5.1.4.3 Other Harvesting

- 5.1.5 Haying and Forage Machinery

- 5.1.5.1 Mowers

- 5.1.5.2 Balers

- 5.1.5.3 Other Haying and Forage

- 5.1.6 Other Types

- 5.1.1 Tractor

- 5.2 By Geography

- 5.2.1 United States

- 5.2.2 Canada

- 5.2.3 Mexico

- 5.2.4 Rest of North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.4.1 Deere & Company

- 6.4.2 CNH Industrial N.V.

- 6.4.3 AGCO Corporation

- 6.4.4 Kubota Corporation

- 6.4.5 CLAAS KGaA mbH

- 6.4.6 Mahindra & Mahindra Limited

- 6.4.7 Netafim USA Inc.

- 6.4.8 Lindsay Corporation

- 6.4.9 Trimble Inc.

- 6.4.10 Horsch Maschinen GmbH

- 6.4.11 KUHN SAS

- 6.4.12 Bernard Krone Holding SE & Co. KG

- 6.4.13 The Toro Company

- 6.4.14 Vermeer Corporation

- 6.4.15 J.C. Bamford Excavators Ltd.

7 Market Opportunities and Future Outlook

除草機器人市場:按組件、類型、運作方式、銷售管道、應用和最終用途分類-2026-2032年全球市場預測農作物殘渣處理機械市場:按類型、機械化程度、動力來源、應用、最終用途和分銷管道分類-2026-2032年全球市場預測

除草機器人市場:按組件、類型、運作方式、銷售管道、應用和最終用途分類-2026-2032年全球市場預測農作物殘渣處理機械市場:按類型、機械化程度、動力來源、應用、最終用途和分銷管道分類-2026-2032年全球市場預測 2026年全球自主作物殘茬管理機器人市場報告農業橡膠履帶市場:2026-2032年全球市場預測(依應用程式、銷售管道、履頻寬度、橡膠配方類型、履帶長度及最終用戶類型分類)

2026年全球自主作物殘茬管理機器人市場報告農業橡膠履帶市場:2026-2032年全球市場預測(依應用程式、銷售管道、履頻寬度、橡膠配方類型、履帶長度及最終用戶類型分類) 自主農業車輛市場:策略性洞察與預測(2026-2031年)溶離設備市場:2026-2032年全球市場預測(依設備類型、自動化程度、技術、應用、最終用戶及銷售管道)農業和施工機械市場:按產品類型、功率範圍、引擎類型、應用、最終用戶和分銷管道分類——2026-2032年全球預測穀物螺旋輸送機市場:按類型、動力來源、容量、應用、最終用戶和分銷管道分類-2026-2032年全球預測紅外線瀝青加熱器市場:按產品類型、電源、移動性、應用、最終用戶、分銷管道分類,全球預測(2026-2032年)

自主農業車輛市場:策略性洞察與預測(2026-2031年)溶離設備市場:2026-2032年全球市場預測(依設備類型、自動化程度、技術、應用、最終用戶及銷售管道)農業和施工機械市場:按產品類型、功率範圍、引擎類型、應用、最終用戶和分銷管道分類——2026-2032年全球預測穀物螺旋輸送機市場:按類型、動力來源、容量、應用、最終用戶和分銷管道分類-2026-2032年全球預測紅外線瀝青加熱器市場:按產品類型、電源、移動性、應用、最終用戶、分銷管道分類,全球預測(2026-2032年) 農業設備市場規模、佔有率、趨勢和預測:按設備類型、應用、銷售管道和地區分類,2026-2034年

農業設備市場規模、佔有率、趨勢和預測:按設備類型、應用、銷售管道和地區分類,2026-2034年