|

市場調查報告書

商品編碼

1906861

拉丁美洲工廠自動化和工業控制:市場佔有率分析、行業趨勢、統計數據和成長預測(2026-2031 年)Latin America Factory Automation And Industrial Controls - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

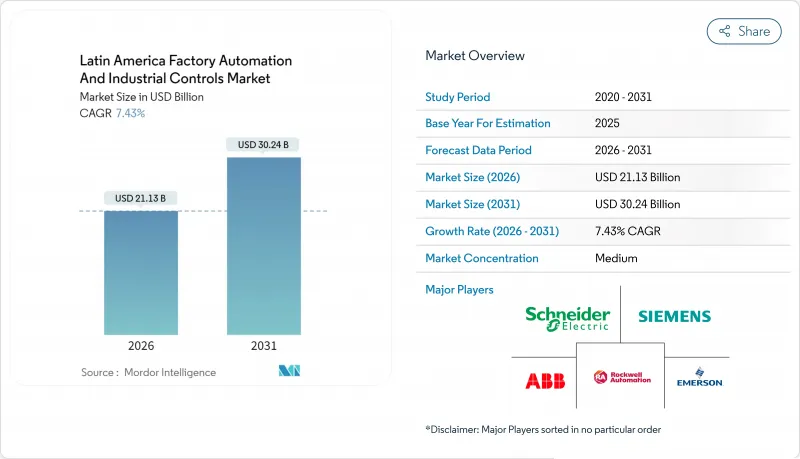

2025年拉丁美洲工廠自動化和工業控制市場價值為196.7億美元,預計到2031年將達到302.4億美元,高於2026年的211.3億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 7.43%。

數位轉型加速、近岸外包活動日益增多以及政府激勵措施,正持續推動對端到端自動化解決方案的需求。各行各業的製造商都在優先考慮即時分析、預測性維護和靈活的生產線,以減少停機時間並達到出口導向的品質標準。供應商的策略重點在於在地化生產、附加價值服務和利基夥伴關係關係,以降低匯率波動和供應鏈中斷的影響。隨著工廠對其傳統資產進行現代化改造,該地區也正在快速採用協作機器人、人工智慧驅動的數位雙胞胎和基於雲端的監控系統。

拉丁美洲工廠自動化與工業控制市場趨勢及洞察

製造業對工業4.0和工業物聯網的採用日益成長

預計到2028年,巴西在工業4.0領域的支出將成長兩倍,這將推動企業範圍內的感測器應用和邊緣分析。阿卡大陸集團(Arca Continental)正在利用雲端平台連接其遍布四個國家的45家工廠和1.25億消費者,從而實現即時效能儀錶板。製造商正從月度指標轉向近乎即時的關鍵績效指標(KPI),以提高應對力並消除生產瓶頸。水泥巨頭沃托蘭廷水泥公司(Votorantim Cimentos)利用預測分析,將每個工廠的糾正性維護成本降低了2,300萬雷亞爾(約460萬美元),並將資產可靠性提高了6%。因此,拉丁美洲的工廠自動化和工業控制市場,無論是在離散製造業或製程工業,都在持續推動智慧感測器網路和數據驅動型工作流程的應用。

政府獎勵計畫加速了智慧工廠投資

巴西已累計1866億雷亞爾(約373億美元)用於工業設施現代化改造,而墨西哥在2024年前七個月新增製造業投資達480億美元,其中超過一半將用於自動化舉措。針對中小企業的定向補貼、稅額扣抵和工程師安置計劃降低了其採用新技術的門檻,而中小企業正是拉丁美洲工廠自動化和工業控制市場的重要組成部分。光是WEG一家公司就計劃投資1.22億美元用於雙邊產能擴張項目,該項目將整合機器人揀選、搬運和製造執行系統(MES)平台。阿根廷的礦業政策也為先進控制系統提供關稅豁免,鞏固了該國作為該地區技術應用最快國家之一的地位。這些激勵措施透過整合公共和私人資本產生協同效應,加速了科技的應用。

中小企業面臨初始資本投入高、投資報酬率不確定性等問題。

調查數據顯示,巴西中小企業在自動化應用方面落後大型企業近兩倍,資金籌措和技術知識不足是主要障礙。協作機器人縮小了這一差距,其實施成本比傳統機器人低20-30%,且投資回收期短。然而,總投資額仍會對資本預算帶來壓力。雖然租賃模式和廠商主導的培訓可以降低部分風險,但拉丁美洲工廠自動化和工業控制市場仍需進一步調整資金籌措結構,以釋放中小企業的潛力。像SENAI這樣的公共機構提供低成本的模擬研討會,幫助企業在購買設備前檢驗投資報酬率。

細分市場分析

2025年,工業控制系統(ICS)將佔據拉丁美洲工廠自動化和工業控制市場30.38%的佔有率,這主要得益於石油天然氣、採礦和食品工廠對PLC、SCADA和DCS的廣泛應用。巴西石油公司(Petrobras)正利用預測分析技術最佳化其煉油廠,而墨西哥國家石油公司(Pemex)則在全部區域部署SCADA系統,用於管道洩漏檢測和流量控制。系統升級通常會整合製造執行系統(MES)和人機介面(HMI)層,使操作人員能夠簡化批次排序和監管報告流程。隨著流程工業更新老化的控制設備並加強網路安全措施,該領域的成長保持穩定。

在拉丁美洲,現場設備正以8.46%的複合年成長率成長,成為工廠自動化和工業控制市場中成長最快的領域,這主要得益於機器人應用的激增和智慧感測器改裝的普及。 2021年,巴西新增安裝工業機器人1,595台,其中協作機器人(cobot)的普及率是傳統機器人的四倍。用於品質檢測的視覺系統和用於內部物流的自動導引運輸車(AGV)在電子、金屬和製藥行業正變得越來越普遍。節能驅動裝置也幫助製造商滿足永續性要求,降低每千瓦時的電力消耗量和維護成本。

受大型計劃(例如價值 50 億美元的 Squilio 造紙廠)的推動,硬體設備(需要各種感測器、致動器和開關設備)將在 2025 年繼續佔據拉丁美洲工廠自動化和工業控制市場 30.25% 的佔有率。然而,由於全球供應鏈調整和外匯波動,零件利潤率正在下降。

服務板塊正以 8.07% 的複合年成長率快速成長,客戶對承包整合、培訓和預測性維護的需求日益成長,這使得供應商能夠獲得持續的收入來源。以績效為基礎的合約十分普遍,例如 Votorantim Cimentos 公司支付的服務費與避免停機時間掛鉤。軟體約佔市場佔有率的四分之一,透過提供以資產為中心的分析和多站點可視性來支援這些模式。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 製造業對工業4.0和工業物聯網的採用日益成長

- 政府獎勵計畫加速了智慧工廠投資

- 成本壓力和最佳化生產力的需要

- 將電力轉移至巴西用於低碳可再生能源生產

- 墨西哥加工出口區相關近岸外包業務的激增正在推動該國的自動化需求。

- 人工智慧驅動的數位雙胞胎在現有工廠的試點部署取得了快速進展

- 市場限制

- 中小企業面臨初始資本投入高、投資報酬率不確定性等問題。

- 在高度自動化的世界裡,技術純熟勞工嚴重短缺。

- 該地貨幣波動阻礙了長期投資

- 針對工業控制系統的網實整合攻擊日益增多

- 產業價值鏈分析

- 監管環境

- 技術展望

- 宏觀經濟因素的影響

- 波特五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 依產品類型

- 工業控制系統

- 分散式控制系統(DCS)

- 可程式邏輯控制器(PLC)

- 監控與數據採集(SCADA)

- 製造執行系統(MES)

- 產品生命週期管理(PLM)

- 人機介面(HMI)

- 企業資源規劃(ERP)

- 現場設備

- 機器視覺

- 工業機器人

- 感測器和發射器

- 馬達和驅動器

- 繼電器和開關

- 工業控制系統

- 依組件類型

- 硬體

- 軟體

- 服務

- 按最終用戶行業分類

- 車

- 食品/飲料

- 石油和天然氣

- 化工/石油化工

- 電力/公共產業

- 製藥

- 電子電器設備

- 採礦和金屬

- 其他終端用戶產業

- 透過部署模式

- 本地部署

- 雲

- 混合

- 按國家/地區

- 巴西

- 墨西哥

- 阿根廷

- 智利

- 哥倫比亞

- 其他拉丁美洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Siemens AG

- ABB Ltd

- Rockwell Automation Inc.

- Schneider Electric SE

- Emerson Electric Co.

- Honeywell International Inc.

- Mitsubishi Electric Corporation

- General Electric Co.

- Dassault Systemes SE

- Autodesk Inc.

- Aspen Technology Inc.

- Bosch Rexroth AG

- Yokogawa Electric Corporation

- Omron Corporation

- FANUC Corporation

- Yaskawa Electric Corporation

- KUKA AG

- Festo SE and Co. KG

- Endress+Hauser Group Services AG

- WEG Industrias SA

第7章 市場機會與未來展望

The Latin America factory automation and industrial controls market was valued at USD 19.67 billion in 2025 and estimated to grow from USD 21.13 billion in 2026 to reach USD 30.24 billion by 2031, at a CAGR of 7.43% during the forecast period (2026-2031).

Accelerated digital transformation, growing nearshoring activity, and government incentives are creating sustained demand for end-to-end automation solutions. Manufacturers across diverse sectors are prioritizing real-time analytics, predictive maintenance, and flexible production lines to reduce downtime and meet export-oriented quality standards. Vendor strategies emphasize localized production, value-added services, and domain-specific partnerships to mitigate currency volatility and supply chain disruptions. The region is also witnessing rapid uptake of collaborative robots, AI-enabled digital twins, and cloud-based supervisory systems as plants modernize legacy assets.

Latin America Factory Automation And Industrial Controls Market Trends and Insights

Rising Industry 4.0 and IIoT Adoption Across Manufacturing

Brazil's Industry 4.0 spending is forecast to triple by 2028, catalyzing enterprise-wide sensor rollouts and edge analytics. Arca Continental uses a cloud-based platform to connect 45 plants and serve 125 million consumers across four countries, enabling real-time performance dashboards. Manufacturers are shifting from monthly metrics to near-instant KPIs, elevating responsiveness and trimming production bottlenecks. Cement major Votorantim Cimentos reduced corrective maintenance costs by BRL 23 million (USD 4.6 million) per site through the use of predictive analytics, improving asset reliability by 6%. As a result, the Latin America factory automation and industrial controls market continues to embed smart-sensor networks and data-driven workflows across both discrete and process industries.

Government Incentive Programs Accelerating Smart-Factory Investments

Brazil earmarked BRL 186.6 billion (USD 37.3 billion) for modernizing industrial facilities, while Mexico reported USD 48 billion in new manufacturing commitments during the first seven months of 2024, over half of which was tied to automation initiatives. Targeted subsidies, tax credits, and technical residencies lower adoption barriers for small and mid-sized enterprises, a priority segment for the Latin America factory automation and industrial controls market. WEG alone plans USD 122 million in dual-country capacity expansions that integrate robotic picking, conveyance, and MES platforms. Argentina's mining policy also grants duty exemptions on advanced controls, supporting its position as the region's fastest-growing adopter. These incentives deliver a multiplier effect by blending public finance with private capital, thereby accelerating the diffusion of technology.

High Upfront Capex and ROI Uncertainty for SMEs

Survey data show that Brazilian SMEs lag behind large firms by as much as 2 times in automation adoption, constrained by access to finance and technical know-how. Collaborative robots narrow this gap, costing 20-30% less to deploy than traditional robots and offering quick paybacks, yet total investment still stretches capital budgets. Leasing models and vendor-led training mitigate some risk, but the Latin America factory automation and industrial controls market must further adapt financing structures to unlock SME potential. Public institutions, such as SENAI, offer low-cost simulation workshops that enable companies to validate ROI scenarios before committing to equipment purchases.

Other drivers and restraints analyzed in the detailed report include:

- Cost-Reduction Pressure and Productivity Optimization Mandates

- Rapid Uptake of AI-Enabled Digital-Twin Pilots in Brownfield Plants

- Acute Skilled-Labor Shortage for Advanced Automation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Industrial Control Systems (ICS) represented 30.38% of the Latin America factory automation and industrial controls market in 2025, underpinned by deployments of PLC, SCADA, and DCS across oil and gas, mining, and food plants. Petrobras leverages predictive analytics to optimize refineries, while PEMEX employs region-wide pipeline SCADA for leak detection and flow control. Upgrades frequently bundle MES and HMI layers, enabling operators to streamline batch sequencing and regulatory reporting. The segment's growth remains steady as process industries refresh aging controllers and expand cybersecurity safeguards.

Field Devices are advancing at an 8.46% CAGR, the fastest pace within the Latin America factory automation and industrial controls market, propelled by surging robot installations and smart-sensor retrofits. Brazil added 1,595 new industrial robots in 2021, with cobots outpacing conventional units by a factor of four. Vision systems for quality inspection and autonomous guided vehicles for intralogistics are gaining traction in the electronics, metals, and pharmaceutical industries. Energy-efficient drives also support sustainability mandates, as manufacturers target lower kilowatt-hour intensity and reduced maintenance bills.

Hardware retained a 30.25% share of the Latin America factory automation and industrial controls market size in 2025, supported by mega-projects such as the USD 5 billion Sucuriu pulp mill that requires extensive sensors, actuators, and switchgear. However, component margins are tightening due to global supply chain rebalancing and currency fluctuations.

Services are expanding at 8.07% CAGR as clients demand turnkey integration, training, and predictive maintenance, positioning vendors for recurring revenue streams. Outcome-based contracts are common, with Votorantim Cimentos paying service fees tied to the avoidance of downtime. Software, at roughly one-quarter market share, anchors these models by providing asset-centric analytics and multi-site visibility.

The Latin America Factory Automation and Industrial Controls Market Report is Segmented by Product Type (Industrial Control Systems, Field Devices), Component Type (Hardware, Software, Services), End-User Industry (Automotive, Food and Beverages, and More), Deployment Mode (On-Premise, Cloud, Hybrid), and Country (Brazil, Mexico, Argentina, Chile, Colombia, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Siemens AG

- ABB Ltd

- Rockwell Automation Inc.

- Schneider Electric SE

- Emerson Electric Co.

- Honeywell International Inc.

- Mitsubishi Electric Corporation

- General Electric Co.

- Dassault Systemes SE

- Autodesk Inc.

- Aspen Technology Inc.

- Bosch Rexroth AG

- Yokogawa Electric Corporation

- Omron Corporation

- FANUC Corporation

- Yaskawa Electric Corporation

- KUKA AG

- Festo SE and Co. KG

- Endress+Hauser Group Services AG

- WEG Industrias S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Industry 4.0 and IIoT adoption across manufacturing

- 4.2.2 Government incentive programmes accelerating smart-factory investments

- 4.2.3 Cost-reduction pressure and productivity optimisation mandates

- 4.2.4 Powershoring to Brazil for low-carbon renewable-energy manufacturing

- 4.2.5 Maquiladora-linked near-shoring surge driving automation demand in Mexico

- 4.2.6 Rapid uptake of AI-enabled digital-twin pilots in brownfield plants

- 4.3 Market Restraints

- 4.3.1 High upfront capex and ROI uncertainty for SMEs

- 4.3.2 Acute skilled-labour shortage for advanced automation

- 4.3.3 Local-currency volatility stalling long-cycle investments

- 4.3.4 Escalating cyber-physical attacks on industrial control systems

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Industrial Control Systems

- 5.1.1.1 Distributed Control System (DCS)

- 5.1.1.2 Programmable Logic Controller (PLC)

- 5.1.1.3 Supervisory Control AND Data Acquisition (SCADA)

- 5.1.1.4 Manufacturing Execution System (MES)

- 5.1.1.5 Product Lifecycle Management (PLM)

- 5.1.1.6 Human Machine Interface (HMI)

- 5.1.1.7 Enterprise Resource Planning (ERP)

- 5.1.2 Field Devices

- 5.1.2.1 Machine Vision

- 5.1.2.2 Robotics (Industrial)

- 5.1.2.3 Sensors and Transmitters

- 5.1.2.4 Motors and Drives

- 5.1.2.5 Relays and Switches

- 5.1.1 Industrial Control Systems

- 5.2 By Component Type

- 5.2.1 Hardware

- 5.2.2 Software

- 5.2.3 Services

- 5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.2 Food and Beverages

- 5.3.3 Oil and Gas

- 5.3.4 Chemical and Petrochemical

- 5.3.5 Power and Utilities

- 5.3.6 Pharmaceutical

- 5.3.7 Electronics and Electrical

- 5.3.8 Mining and Metals

- 5.3.9 Other End-user Industries

- 5.4 By Deployment Mode

- 5.4.1 On-premise

- 5.4.2 Cloud

- 5.4.3 Hybrid

- 5.5 By Country

- 5.5.1 Brazil

- 5.5.2 Mexico

- 5.5.3 Argentina

- 5.5.4 Chile

- 5.5.5 Colombia

- 5.5.6 Rest of Latin America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Siemens AG

- 6.4.2 ABB Ltd

- 6.4.3 Rockwell Automation Inc.

- 6.4.4 Schneider Electric SE

- 6.4.5 Emerson Electric Co.

- 6.4.6 Honeywell International Inc.

- 6.4.7 Mitsubishi Electric Corporation

- 6.4.8 General Electric Co.

- 6.4.9 Dassault Systemes SE

- 6.4.10 Autodesk Inc.

- 6.4.11 Aspen Technology Inc.

- 6.4.12 Bosch Rexroth AG

- 6.4.13 Yokogawa Electric Corporation

- 6.4.14 Omron Corporation

- 6.4.15 FANUC Corporation

- 6.4.16 Yaskawa Electric Corporation

- 6.4.17 KUKA AG

- 6.4.18 Festo SE and Co. KG

- 6.4.19 Endress+Hauser Group Services AG

- 6.4.20 WEG Industrias S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

工業鍵盤和觸控板市場:按產品類型、連接方式、開關技術、背光、最終用途產業和分銷管道分類,全球預測,2026-2032年鋰電池工業除塵器市場:按類型、過濾材料、工作模式、風量和最終用途行業分類,全球預測,2026-2032年

工業鍵盤和觸控板市場:按產品類型、連接方式、開關技術、背光、最終用途產業和分銷管道分類,全球預測,2026-2032年鋰電池工業除塵器市場:按類型、過濾材料、工作模式、風量和最終用途行業分類,全球預測,2026-2032年 美國工廠自動化和工業控制:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)中國工廠自動化與工業控制:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)亞太地區工廠自動化和工業控制:市場佔有率分析、產業趨勢和成長預測(2025-2030)北美工廠自動化和工業控制:市場佔有率分析、行業趨勢和成長預測(2025-2030)日本工廠自動化與工業控制設備:市場佔有率分析、產業趨勢、統計、成長預測(2025-2030)歐洲工廠自動化與工業控制:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)法國工廠自動化和工業控制設備:市場佔有率分析、行業趨勢、統計和成長預測(2025-2030)

美國工廠自動化和工業控制:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)中國工廠自動化與工業控制:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)亞太地區工廠自動化和工業控制:市場佔有率分析、產業趨勢和成長預測(2025-2030)北美工廠自動化和工業控制:市場佔有率分析、行業趨勢和成長預測(2025-2030)日本工廠自動化與工業控制設備:市場佔有率分析、產業趨勢、統計、成長預測(2025-2030)歐洲工廠自動化與工業控制:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)法國工廠自動化和工業控制設備:市場佔有率分析、行業趨勢、統計和成長預測(2025-2030) 2025-2033 年日本工廠自動化和工業控制市場報告(按類型、最終用途行業和地區)

2025-2033 年日本工廠自動化和工業控制市場報告(按類型、最終用途行業和地區)