|

市場調查報告書

商品編碼

1693418

氰基丙烯酸酯黏合劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Cyanoacrylate Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

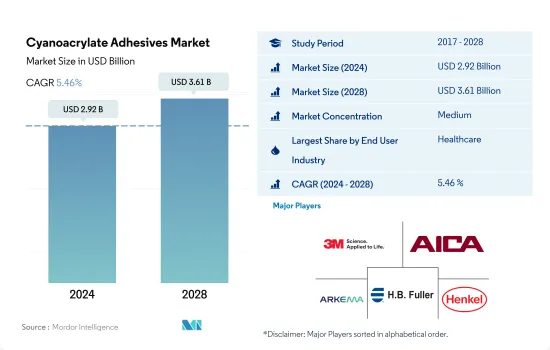

氰基丙烯酸酯黏合劑市場規模預計在 2024 年為 29.2 億美元,預計到 2028 年將達到 36.1 億美元,預測期內(2024-2028 年)的複合年成長率為 5.46%。

醫療保健產業投資的增加也將推動未來對氰基丙烯酸酯黏合劑的需求。

- 氰基丙烯酸酯黏合劑由於其獨特的性能(例如通常在室溫下快速或即時固化)而用於各種最終用戶行業。

- 氰基丙烯酸酯黏合劑用於建設產業,例如地板材料、屋頂和組裝廚房組件等。預計到 2030 年,全球建設產業的複合年成長率將達到 3.5%。在世界各國中,中國、印度、美國和印尼預計將佔全球建築業成長的 58.3%。

- 氰基丙烯酸酯黏合劑廣泛應用於汽車工業,因為它們可以應用於玻璃、金屬、塑膠和塗漆表面等表面。它用於組裝電動車電池,以及組裝車輛內飾和引擎部件。由於發展中國家的需求不斷成長,預測期內全球整體汽車產業的電動車領域預計將以 17.75% 的複合年成長率成長。預計這將在預測期內推動汽車氰基丙烯酸酯黏合劑的需求。

- 氰基丙烯酸酯黏合劑廣泛應用於電子和電氣設備的製造。用於安裝感測器和鉚接線路。全球電子產業和家用電器產業預計將分別以 2.51% 和 5.77% 的複合年成長率成長,預計在 2022-2028 年的預測期內將增加對氰基丙烯酸酯黏合劑的需求。

- 氰基丙烯酸酯黏合劑無毒且固化迅速,因此在醫療保健產業中廣泛用於組裝和醫用膠帶等應用。預測期內,全球醫療保健投資的增加將導致需求增加。

基於紫外線固化技術的氰基丙烯酸酯黏合劑正在推動全球經濟成長

- 氰基丙烯酸酯膠黏劑佔全球膠黏劑市場總量的 3%,2021 年市場規模為 547 億美元。氰基丙烯酸酯膠黏劑因其快速黏合特性而廣受歡迎。只需較少的黏合劑即可在多種基材(包括金屬、玻璃和聚合物)之間形成黏合。這些黏合劑主要用於全球汽車、電子、DIY、醫療保健和其他幾個行業。

- 2020 年氰基丙烯酸酯膠黏劑的消費量與 2019 年相比下降了 10.74%,這主要是由於新冠疫情的影響。世界各地的國家封鎖導致生產設施關閉、供應鏈中斷以及貿易交流的國際邊界關閉。然而,許多國家的經濟復甦導致2021年對氰基丙烯酸酯膠黏劑的需求增加了2,520萬公斤。

- 由於中國、日本和印度經濟的不斷成長,氰基丙烯酸酯黏合劑主要在亞太地區消費。這些瞬間黏合劑廣泛應用於該地區的汽車、DIY 和電子產業。中國是最大的汽車製造國,這些黏合劑在中國被廣泛使用。預計到 2027 年,汽車產量將達到 6,370 萬輛,高於 2021 年的 4,790 萬輛。該地區汽車產量的成長預計將在未來幾年推動對氰基丙烯酸酯黏合劑的需求。

- 氰基丙烯酸酯黏合劑用於反應性和紫外線固化技術。紫外線固化技術是全球成長最快的技術,預計在 2022-2028 年預測期內,其產量複合年成長率將達到 4.83%。

氰基丙烯酸酯黏合劑的全球趨勢

政府推行的電動車優惠政策將推動汽車產業

- 預計 2021 年後全球汽車產業將穩定成長,但成長速度將放緩,因為消費者對擁有個人汽車的偏好降低,而對共用出行的偏好。預計預測期內全球汽車產業將以每年 2% 的速度成長,總收益增加價值將達到 1.5 兆美元。

- 2020年,受新冠疫情影響,汽車銷量下滑,但2021年卻迅速回升。汽車市場通常對GDP貢獻巨大,因此世界各國政府紛紛推出措施支持經濟。汽車銷量從2019年的9000萬輛下降到2020年的7800萬輛。

- 由於電動車能源成本低廉、環境友善且移動性高效,其在全球範圍內的普及對全球汽車市場的總收益做出了重大貢獻。各種政府政策和標準也在推動電動車產量的成長。例如,歐盟二氧化碳排放標準在2021年增加了對電動車的需求。根據國際能源總署的永續情景,到2030年將需要2.3億輛電動車取代燃油汽車。 2021年,最大的電動車製造商特斯拉的電動車產量增加了157%。預計預測期內(2022-2028 年),消費者對電動車的偏好將進一步成長。

家居和辦公家具需求成長推動產業成長

- 雖然IKEA仍然是全球家具市場最大的線下零售商,但近年來出現了像 Wayfair 這樣的電子商務巨頭。全球消費者對網上家具購物的接受度正在不斷提高,其在整個家具市場的佔有率預計將從 2017 年的 15% 成長到 2021 年的 18%。由於家具的便利性和易於安裝,這一趨勢隨後推動了對家具的需求。美國是家具銷售額最高的國家,2021年達2,292億美元。

- 全球木製家具市場可分為臥室家具、客廳家具、戶外家具和餐廳家具。其中,客廳家具板塊佔據了最高的收益佔有率,自2020年新冠疫情期間居家辦公文化興起以來,客廳家具板塊佔整個家具市場的近40%。疫情導致2020-2021年對客廳或家庭辦公家具的需求增加,該板塊全球整體市場價值達到2,271億美元。

- 在預測期內(2022-2028 年),市場預計將穩定成長,因為人均家具支出增加,從 2017 年的 72.85 美元上升到 2021 年的 89.30 美元,儘管 2020 年受到疫情影響,但在此期間下降至 80.43 美元。人均家具支出的增加可以歸因於人們生活水準的提高。

氰基丙烯酸酯膠黏劑產業概況

氰基丙烯酸酯黏合劑市場適度整合,前五大公司佔據43.97%的市場佔有率。該市場的主要企業有:3M、Aica Kogyo、阿科瑪集團、HB Fuller Company 和 Henkel AG & Co. KGaA(按字母順序排列)

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 最終用戶趨勢

- 航太

- 車

- 建築與施工

- 鞋類和皮革

- 木製品和配件

- 法律規範

- 阿根廷

- 澳洲

- 巴西

- 加拿大

- 中國

- EU

- 印度

- 印尼

- 日本

- 馬來西亞

- 墨西哥

- 俄羅斯

- 沙烏地阿拉伯

- 新加坡

- 南非

- 韓國

- 泰國

- 美國

- 價值鍊和通路分析

第5章市場區隔

- 最終用戶產業

- 航太

- 車

- 建築與施工

- 鞋類和皮革

- 衛生保健

- 木製品和配件

- 其他最終用戶產業

- 科技

- 反應性

- 紫外線固化膠合劑

- 地區

- 亞太地區

- 澳洲

- 中國

- 印度

- 印尼

- 日本

- 馬來西亞

- 新加坡

- 韓國

- 泰國

- 其他亞太地區

- 歐洲

- 法國

- 德國

- 義大利

- 俄羅斯

- 西班牙

- 英國

- 其他歐洲國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 北美洲

- 加拿大

- 墨西哥

- 美國

- 北美其他地區

- 南美洲

- 阿根廷

- 巴西

- 南美洲其他地區

- 亞太地區

第6章競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介.

- 3M

- Aica Kogyo Co..Ltd.

- Arkema Group

- DELO Industrie Klebstoffe GmbH & Co. KGaA

- HB Fuller Company

- Henkel AG & Co. KGaA

- Hubei Huitian New Materials Co. Ltd

- Illinois Tool Works Inc.

- Jowat SE

- Kangda New Materials(Group)Co., Ltd.

- NANPAO RESINS CHEMICAL GROUP

- Permabond LLC.

- Pidilite Industries Ltd.

- Soudal Holding NV

- ThreeBond Holdings Co., Ltd.

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 全球黏合劑和密封劑產業概況

- 概述

- 五力分析框架(產業吸引力分析)

- 全球價值鏈分析

- 促進因素、限制因素和機會

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 92477

The Cyanoacrylate Adhesives Market size is estimated at 2.92 billion USD in 2024, and is expected to reach 3.61 billion USD by 2028, growing at a CAGR of 5.46% during the forecast period (2024-2028).

Rising investments in the healthcare industry to also drive the demand for cyanoacrylate adhesives in the future

- Cyanoacrylate adhesives are used in different end-user industries because of their unique properties, such as quick or instant curing, usually at room temperature.

- Cyanoacrylate adhesives are used in the construction industry for their applications, such as flooring, roofing, and kitchen component assembly. The construction industry is expected to grow globally with a 3.5% CAGR up to 2030. Among the nations of the world, China, India, the United States, and Indonesia are expected to account for 58.3% of the global construction growth.

- Cyanoacrylate adhesives are widely used in the automotive industry because of their applicability to surfaces such as glass, metal, plastic, and painted surfaces. They are used to assemble body interiors and engine components, such as battery assembly in electric vehicles. The electric vehicles segment of the automotive industry is expected to record a 17.75% CAGR globally in the forecast period because of the increase in demand for the same in growing economies. This is expected to boost the demand for automotive cyanoacrylate adhesives in the forecast period.

- Cyanoacrylate adhesives are widely used in electronics and electrical equipment manufacturing. They are used for attaching sensors and tacking off wires. The global electronics and household appliances industries are expected to record CAGRs of 2.51% and 5.77%, respectively, which is expected to increase demand for cyanoacrylate adhesives in the forecast period 2022-2028.

- Cyanoacrylate adhesives are used in the healthcare industry for applications such as assembling and medical tapes because of their non-toxic nature and instant curing. The increase in healthcare investments worldwide will lead to a rise in their demand in the forecast period.

Cyanoacrylate adhesives based on the UV-cured technology leading the growth rates at the global scale

- Cyanoacrylate adhesives account for 3% of the total adhesives market worldwide, valued at USD 54.7 billion in 2021. Cyanoacrylate adhesives are popular because of their quick bonding properties. It requires less adhesive to form a bond between various substrates, including metals, glass, and polymers. These adhesives are majorly consumed in automotive, electronics, DIY, healthcare, and a few other industries across the globe.

- The consumption of cyanoacrylate adhesives declined in 2020 by 10.74% compared to 2019, mainly due to the COVID-19 pandemic. Nationwide lockdowns globally resulted in the shutdown of production facilities, supply chain disruptions, and sealed international borders for trade exchange. However, the economic recovery in many countries resulted in a growth in demand for cyanoacrylate adhesives by 25.2 million kg in 2021.

- Cyanoacrylate adhesives are consumed mainly in the Asia-Pacific region owing to growing economies such as China, Japan, and India. These instant adhesives are widely used in the region's automotive, DIY, and electronics industries. China is the largest country for automotive production, and these adhesives are used more in the country. Automotive production is expected to reach 63.7 million units by 2027 from 47.9 million units in 2021. The rising automotive production in the region is expected to drive the demand for cyanoacrylate adhesives over the coming years.

- Cyanoacrylate adhesives are used with reactive and UV-cured technology. UV-cured technology is the fastest-growing technology in the world and is expected to record a CAGR of 4.83% in volume terms in the forecast period 2022-2028.

Global Cyanoacrylate Adhesives Market Trends

Favorable government policies to promote electric vehicles will propel automotive industry

- Since 2021, the global automotive industry has been expected to grow steadily but at a slower pace because of the decline in consumers' preferences for individual ownership of passenger vehicles and their increased preference for shared mobility in transportation. The global automotive industry is expected to experience a growth rate of 2% annually, with an expected value addition of USD 1.5 trillion in total revenue during the forecast period.

- In 2020, due to the impact of the COVID-19 pandemic, vehicle sales declined but recovered rapidly in 2021 because the governments of various countries took measures to support their economies, as automotive markets usually contribute majorly to their GDP. Vehicle sales declined from 90 million units of passenger vehicles in 2019 to 78 million units in 2020.

- The introduction of electric vehicles worldwide has contributed significantly to the overall revenue of the global automotive market because of their cheaper energy costs, environmentally benign nature, and efficient mobility features. Various government policies and standards also work as driving factors to increase EV production. For instance, the EU standards for CO2 emissions increased the demand for electric vehicles in 2021. As per the IEA's Sustainable Scenario, 230 million electric vehicles are required to replace combustion fuel-based vehicles by 2030. In 2021, Tesla, the largest EV manufacturer, recorded a rise of 157% in the number of electric vehicles manufactured. This growing trend of consumers preferring electric vehicles is expected to rise further during the forecast period (2022-2028).

Rising demand for home & office furniture to aid the growth of the industry

- While IKEA is the largest offline retail player in the global furniture market, there has been a rise in e-commerce giants, such as Wayfair, in recent years. The adoption of online furniture shopping by consumers is gaining momentum globally, and its share in the overall furniture market increased from 15% in 2017 to 18% in 2021. This trend is subsequently boosting the demand for furniture due to its convenience and easy installation. The highest sales revenue for furniture was generated in the United States, with USD 229.2 billion, in 2021.

- The global wooden furniture market can be segmented into bedroom, living room, outdoor, and dining furniture. Among these, the living room furniture segment held the highest revenue share, accounting for nearly 40% of the overall furniture market since the increase in the work-from-home culture during the COVID-19 outbreak in 2020. The pandemic led to an increase in demand for living room or home office furniture in 2020-2021, and the segment registered a market value of USD 227.10 billion globally.

- The market is expected to witness steady growth during the forecast period (2022-2028) due to the increasing per capita expenditure on furniture, which rose from USD 72.85 in 2017 to USD 89.30 in 2021 despite the pandemic in 2020, during which it dipped to USD 80.43. This increasing per capita expenditure on furniture could be due to the improving living standards of people.

Cyanoacrylate Adhesives Industry Overview

The Cyanoacrylate Adhesives Market is moderately consolidated, with the top five companies occupying 43.97%. The major players in this market are 3M, Aica Kogyo Co..Ltd., Arkema Group, H.B. Fuller Company and Henkel AG & Co. KGaA (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Footwear and Leather

- 4.1.5 Woodworking and Joinery

- 4.2 Regulatory Framework

- 4.2.1 Argentina

- 4.2.2 Australia

- 4.2.3 Brazil

- 4.2.4 Canada

- 4.2.5 China

- 4.2.6 EU

- 4.2.7 India

- 4.2.8 Indonesia

- 4.2.9 Japan

- 4.2.10 Malaysia

- 4.2.11 Mexico

- 4.2.12 Russia

- 4.2.13 Saudi Arabia

- 4.2.14 Singapore

- 4.2.15 South Africa

- 4.2.16 South Korea

- 4.2.17 Thailand

- 4.2.18 United States

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Footwear and Leather

- 5.1.5 Healthcare

- 5.1.6 Woodworking and Joinery

- 5.1.7 Other End-user Industries

- 5.2 Technology

- 5.2.1 Reactive

- 5.2.2 UV Cured Adhesives

- 5.3 Region

- 5.3.1 Asia-Pacific

- 5.3.1.1 Australia

- 5.3.1.2 China

- 5.3.1.3 India

- 5.3.1.4 Indonesia

- 5.3.1.5 Japan

- 5.3.1.6 Malaysia

- 5.3.1.7 Singapore

- 5.3.1.8 South Korea

- 5.3.1.9 Thailand

- 5.3.1.10 Rest of Asia-Pacific

- 5.3.2 Europe

- 5.3.2.1 France

- 5.3.2.2 Germany

- 5.3.2.3 Italy

- 5.3.2.4 Russia

- 5.3.2.5 Spain

- 5.3.2.6 United Kingdom

- 5.3.2.7 Rest of Europe

- 5.3.3 Middle East & Africa

- 5.3.3.1 Saudi Arabia

- 5.3.3.2 South Africa

- 5.3.3.3 Rest of Middle East & Africa

- 5.3.4 North America

- 5.3.4.1 Canada

- 5.3.4.2 Mexico

- 5.3.4.3 United States

- 5.3.4.4 Rest of North America

- 5.3.5 South America

- 5.3.5.1 Argentina

- 5.3.5.2 Brazil

- 5.3.5.3 Rest of South America

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Aica Kogyo Co..Ltd.

- 6.4.3 Arkema Group

- 6.4.4 DELO Industrie Klebstoffe GmbH & Co. KGaA

- 6.4.5 H.B. Fuller Company

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 Hubei Huitian New Materials Co. Ltd

- 6.4.8 Illinois Tool Works Inc.

- 6.4.9 Jowat SE

- 6.4.10 Kangda New Materials (Group) Co., Ltd.

- 6.4.11 NANPAO RESINS CHEMICAL GROUP

- 6.4.12 Permabond LLC.

- 6.4.13 Pidilite Industries Ltd.

- 6.4.14 Soudal Holding N.V.

- 6.4.15 ThreeBond Holdings Co., Ltd.

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

氰基丙烯酸黏合劑市場:全球市場預測,2026-2032年

氰基丙烯酸黏合劑市場:全球市場預測,2026-2032年 亞太地區氰基丙烯酸黏合劑:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)歐洲氰基丙烯酸黏合劑:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)

亞太地區氰基丙烯酸黏合劑:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)歐洲氰基丙烯酸黏合劑:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年) 2026年全球氰基丙烯酸黏合劑市場報告

2026年全球氰基丙烯酸黏合劑市場報告 全球氰基丙烯酸黏合劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)北美氰基丙烯酸酯黏合劑:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)

全球氰基丙烯酸黏合劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)北美氰基丙烯酸酯黏合劑:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年) 到 2030 年氰基丙烯酸黏劑市場預測:按產品類型、最終用戶和地區分類的全球分析

到 2030 年氰基丙烯酸黏劑市場預測:按產品類型、最終用戶和地區分類的全球分析 氰基丙烯酸黏劑市場:按化學、按固化工藝、按應用、按最終用途行業、按地區 - 預測至 2029 年

氰基丙烯酸黏劑市場:按化學、按固化工藝、按應用、按最終用途行業、按地區 - 預測至 2029 年