|

市場調查報告書

商品編碼

1693415

亞太地區環氧膠黏劑:市場佔有率分析、產業趨勢和成長預測(2025-2030)Asia-Pacific Epoxy Adhesive - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

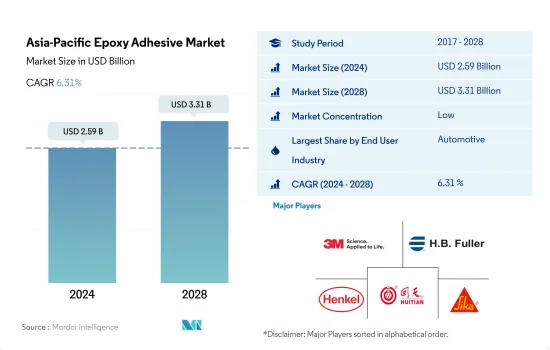

亞太地區環氧膠黏劑市場規模預計在 2024 年為 25.9 億美元,預計到 2028 年將達到 33.1 億美元,預測期內(2024-2028 年)的複合年成長率為 6.31%。

該地區汽車產量不斷成長,預計到 2028 年將達到 6,600 萬輛,這將推動對環氧膠黏劑的需求。

- 環氧樹脂膠黏劑是熱固性樹脂,固化後具有高強度和低收縮性。這些黏合劑堅韌且耐化學性和環境損害。環氧樹脂膠黏劑具有對多種基材優異的黏合性、優異的耐溶劑性和良好的電絕緣性能。此外,環氧膠黏劑的黏合硬度高達 80 肖氏硬度以上。

- 2020年環氧膠黏劑的消費量與2019年相比下降了9.66%,這主要是由於包括中國、印度、日本和韓國在內的許多國家受到新冠疫情的影響。全國範圍的封鎖、供應鏈中斷和經濟放緩導致大多數國家的生產陷入停滯,導致環氧膠的消費下降。 2021年受各國經濟復甦影響,環氧膠合劑產量增加,新增3,680萬單位。

- 中國是該地區環氧膠黏劑的主要市場,其次是日本和印度。 2021年中國對環氧膠黏劑的需求約為12億美元。汽車和建築是使用環氧膠黏劑進行各種應用的主要終端使用產業。

- 由於該國生產的汽車數量不斷增加,汽車產業已成為該地區最大的環氧膠黏劑消費產業。環氧樹脂膠黏劑主要用於結構應用,是用於黏合金屬、玻璃和塑膠的所有樹脂基膠黏劑中抗張強度最高的,約為 35-41N/mm2。該地區的汽車產量預計將從 2021 年的 4,790 萬輛增至 2028 年的 6,600 萬輛。預計汽車產量的成長將在未來幾年推動對環氧膠黏劑的需求。

汽車電子元件需求的不斷成長可能會增加對環氧膠黏劑的需求

- 在評估環氧膠黏劑的效率時,查看其組成化學物質的整體成分很有用。兩種初始成分(樹脂和硬化劑)的混合物聚合產生環氧樹脂。當樹脂與特定催化劑結合時,固化就開始了。環氧樹脂膠黏劑可黏合多種材料,其品質取決於系統的化學性質和可用的交聯類型。出色的耐化學性和耐熱性、良好的附著力和耐水性、令人滿意的機械和電氣絕緣性能是最重要的性能參數。

- 環氧樹脂膠黏劑是最常用的結構型膠合劑,通常為單組分或雙組分體系。單組分環氧膠黏劑通常在 250-300°F 的溫度範圍內固化,從而產生強度高、對金屬黏合力強、耐環境和耐化學性優異的產品。

- 在所有終端使用領域中,汽車是全球環氧樹脂的最大消費者,約佔 35.7% 的佔有率,其次是建築、醫療、木工和航太,分別約佔 19.4%、6.3%、4.7% 和 2.1% 的佔有率。其他終端用途產業的佔有率約為31.1%。在整個汽車產業,人們越來越重視永續性,預計亞太地區的電動車產量將會增加。為此,新興國家紛紛採取措施抑制汽車產業對傳統能源的消耗。這項因素將會增加對汽車電子元件的需求,從而促進全部區域對環氧膠黏劑的消費。

亞太環氧膠黏劑市場趨勢

電動車的普及正在推動該產業

- 由於汽車銷售強勁成長,亞太汽車產業成為領先的市場領域之一。在所有國家中,中國是最大的汽車生產國,佔該地區汽車產量的57%左右,其次是日本(17%)、印度(10%)和韓國(8%)。

- 該地區的汽車銷售和產量均大幅下降,影響了黏合劑的使用。 2017- 與前一年同期比較變動為-1.8%,而2018-19年度則進一步下降-6.4%。 2019-20年度,受新冠疫情影響,該地區產量再次受到負面影響,較去年同期與前一年同期比較10.2%。由於製造工廠停工和供應鏈中斷,汽車零件短缺,生產水準受到限制。然而,預計汽車需求將在 2021 年再次增加並持續成長,從而導致預測期內全部區域的黏合劑使用量增加。

- 亞太電動車市場為黏合劑市場帶來了另一個成長機會。電動和混合動力汽車的產量和採用率的不斷提高,推動了汽車電子組裝中黏合劑的使用量。中國是世界上最大的電動車生產國,也是全部區域最大的電動車生產國。 2016年至2021年間,商用電動車數量從562,603輛增加到1,116,382輛,成長率約98%。預計這些因素將增加對黏合劑的需求,有助於預測期內的市場成長。

加大基礎建設投資將擴大產業規模

- 亞太地區受中國、日本和印度等世界主要經濟體推動。中國正處於持續都市化進程中,2030年都市化率目標達到70%。都市化加快將增加都市區生活空間需求,鼓勵都市區中等收入者追求更好的居住條件,這將對住宅市場產生影響,從而增加全國的住宅建設。

- 非住宅基礎設施可能會大幅擴張。 2019年,中國政府核准了26個基礎建設計劃,總價值約1420億美元,預計2023年完工。中國擁有全球最大的建築市場,佔全球建築投資的20%。到2030年,政府計劃在建設方面投資超過13兆美元。因此,預計預測期內(2022-2028 年)建築市場的複合年成長率為 4.48%。

- 建築業是亞太地區最大的產業之一,2019 年取得了可喜的成長。由於該地區包括越南、馬來西亞、印尼、泰國和其他南亞國家等許多新興國家,該產業持續成長。然而,受新冠疫情影響,全部區域政府實施封鎖,建築業大幅下滑,嚴重影響了包括印度、中國、日本和東南亞國協在內的開發中國家。

- 亞太地區建築領域也越來越受到國際投資者的興趣。隨著發展中國家為投資者提供更好的利益和機會,建築開發領域的外國直接投資(FDI)正在增加。

亞太環氧膠黏劑產業概況

亞太地區環氧膠黏劑市場細分化,前五大公司佔22.42%。該市場的主要企業包括 3M、HB Fuller Company、漢高股份公司、湖北迴天新材料、西卡股份公司等。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 最終用戶趨勢

- 航太

- 車

- 建築與施工

- 鞋類皮革

- 包裝

- 木製品和配件

- 法律規範

- 澳洲

- 中國

- 印度

- 印尼

- 日本

- 馬來西亞

- 新加坡

- 韓國

- 泰國

- 價值鍊和通路分析

第5章市場區隔

- 最終用戶產業

- 航太

- 車

- 建築與施工

- 鞋類和皮革

- 醫療保健

- 包裝

- 木製品和配件

- 其他

- 科技

- 反應性

- 溶劑型

- 紫外線固化膠合劑

- 水性

- 國家

- 澳洲

- 中國

- 印度

- 印尼

- 日本

- 馬來西亞

- 新加坡

- 韓國

- 泰國

- 其他亞太地區

第6章競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介

- 3M

- Arkema Group

- HB Fuller Company

- Henkel AG & Co. KGaA

- Hubei Huitian New Materials Co. Ltd

- Huntsman International LLC

- Kangda New Materials(Group)Co., Ltd.

- NANPAO RESINS CHEMICAL GROUP

- Pidilite Industries Ltd.

- Sika AG

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 全球黏合劑和密封劑產業概況

- 概述

- 五力分析框架(產業吸引力分析)

- 全球價值鏈分析

- 促進因素、限制因素和機會

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 數據包

- 詞彙表

簡介目錄

Product Code: 92474

The Asia-Pacific Epoxy Adhesive Market size is estimated at 2.59 billion USD in 2024, and is expected to reach 3.31 billion USD by 2028, growing at a CAGR of 6.31% during the forecast period (2024-2028).

Increasing vehicle production which is expected to reach 66 million units by 2028 in the region is likely to drive the demand for epoxy adhesives

- Epoxy adhesives are thermosetting resins that demonstrate high strength and low shrinkage during curing. These adhesives are tough and resistant to chemicals and environmental damage. Epoxy adhesives offer excellent adhesion to various substrates, superior resistance solvents, and good electrical insulation. In addition, epoxy adhesives offer high hardness to the bond, which is more than 80 shore.

- The consumption of epoxy adhesives shrunk by 9.66% in 2020 compared to 2019, mainly due to the impact of the COVID-19 pandemic in many countries, including China, India, Japan, and South Korea. Production stopped in most countries due to nationwide lockdowns, supply chain disruptions, and economic slowdowns, which resulted in a decline in the consumption of epoxy adhesives. In 2021, the economic recovery in the countries caused a rise in the production of epoxy adhesives, which registered a growth of 36.8 million in volume.

- China is the major market for epoxy adhesives in the region, followed by Japan and India. China's demand for epoxy adhesives was nearly USD 1.2 billion in 2021. Automotive and construction are the major end-user industries that use epoxy adhesives for different applications.

- Automotive is the region's largest consumer industry for epoxy adhesives, owing to the rising vehicle production in the country. Epoxy adhesive is mainly used in structural applications and offers the highest tensile strength, around 35-41 N/mm2, among all other resin-based adhesives to bond metal, glass, and plastic. It is expected that vehicle production will reach 66 million units in the region in 2028 from 47.9 million units in 2021. Rising vehicle production is expected to drive the demand for epoxy adhesives over the coming years.

Increasing demand for electronic components for vehicles is likely to boost the demand for epoxy adhesives

- When evaluating the efficiency of an epoxy adhesive, it is beneficial to examine the general composition of the chemicals that comprise it. Polymerization of a mixture of two initial components, the resin and the hardener, produces epoxy. Curing begins when the resin is combined with a specific catalyst. Epoxy adhesives stick to a wide range of materials, and their qualities are determined by the system's chemistry and the type of cross-linking available. Exceptional chemical and heat resistance, great adhesion and water resistance, and satisfactory mechanical and electrical insulating qualities are among the most significant performance parameters.

- Epoxy adhesives, the most generally used structural type adhesive, are commonly available as one-component or two-component systems. One-component epoxy adhesives are typically cured at temperatures ranging from 250 to 300°F, resulting in a product with great strength, strong adherence to metals, and exceptional environmental and harsh chemical resistance.

- Across all the end-use sectors, automotive is the leading consumer of epoxy globally, holding a share of about 35.7%, followed by building and construction, healthcare, woodworking, and aerospace, with shares of approximately 19.4%, 6.3%, 4.7%, and 2.1%, respectively. The other end-use industries hold about 31.1%%. Across the automotive industry, the rising adoption of sustainability is expected to increase EV production across the Asia-Pacific region. Owing to this reason, emerging nations are moving toward limiting the consumption of conventional energy in the automotive industry. The factor tends to increase the demand for electronic components for vehicles and, thus, boost the consumption of epoxy adhesives across the region.

Asia-Pacific Epoxy Adhesive Market Trends

Increasing adoption of electric vehicles to drive the industry

- The Asia-Pacific automotive industry is one of the leading industries in the market, as the sales of automotive vehicles are largely increasing. Among all the countries, China is the largest automotive producer, accounting for about 57% of the regional production, followed by Japan with 17%, India with 10%, and South Korea with 8%.

- Vehicle sales in the region have majorly declined along with production, owing to which the utilization of adhesives has been impacted. While the Y-o-Y variation in 2017-18 was -1.8%, it fell further by -6.4% in 2018-19. In 2019-20, regional production was again impacted negatively and recorded a -10.2% decline from the previous year due to the COVID-19 pandemic. The shutdown of manufacturing facilities and the shortage of vehicle components due to disruptions in the supply chain constrained the production level. However, in 2021, the demand for automobiles rose again and is expected to continue, thereby increasing the utilization of adhesives across the region over the forecast period.

- The EV market in Asia-Pacific offers another opportunity for the adhesives market to grow. The rising production and adoption of EVs and hybrid vehicles are boosting the usage of adhesives for electronic component assembly in vehicles. China is the largest producer of EVs globally as well as across the region. From 2016 to 2021, the volume of commercial electric vehicles increased from 562,603 to 1,116,382 units, recording a growth rate of about 98%. These factors are expected to increase the demand for adhesives and result in the higher market growth over the forecast period.

Raising investment to expand infrastructural activities will augment the industry size

- Asia-Pacific is driven by the world's major economies, such as China, Japan, and India. China is promoting and undergoing a process of continuous urbanization, with a target rate of 70% for 2030. The increased living spaces required in the urban areas resulting from increasing urbanization and the desire of middle-income urban residents to improve their living conditions may impact the housing market and, thereby, increase the residential constructions in the country.

- Non-residential infrastructure is likely to expand significantly. The Chinese government approved 26 infrastructure projects worth approximately USD 142 billion in 2019, with completion due in 2023. The country has the largest construction market globally, accounting for 20% of all worldwide construction investments. By 2030, the government plans to spend over USD 13 trillion on construction. Thus, the construction market is expected to register a 4.48% CAGR during the forecast period (2022-2028).

- The construction industry is one of the largest industries in Asia-Pacific and recorded promising growth in 2019. The industry continues to grow as the region constitutes many developing countries such as Vietnam, Malaysia, Indonesia, Thailand, and other South Asian countries. However, due to the COVID-19 pandemic, the construction sector witnessed a significant decline owing to lockdowns by governments across the region, which severely affected developing countries, including India, China, Japan, and ASEAN countries.

- The Asia-Pacific region is also witnessing significant interest from international investors in the construction space. Foreign Direct Investment (FDI) in the construction development sector is increasing as developing countries provide better returns and opportunities for investors.

Asia-Pacific Epoxy Adhesive Industry Overview

The Asia-Pacific Epoxy Adhesive Market is fragmented, with the top five companies occupying 22.42%. The major players in this market are 3M, H.B. Fuller Company, Henkel AG & Co. KGaA, Hubei Huitian New Materials Co. Ltd and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Footwear and Leather

- 4.1.5 Packaging

- 4.1.6 Woodworking and Joinery

- 4.2 Regulatory Framework

- 4.2.1 Australia

- 4.2.2 China

- 4.2.3 India

- 4.2.4 Indonesia

- 4.2.5 Japan

- 4.2.6 Malaysia

- 4.2.7 Singapore

- 4.2.8 South Korea

- 4.2.9 Thailand

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Footwear and Leather

- 5.1.5 Healthcare

- 5.1.6 Packaging

- 5.1.7 Woodworking and Joinery

- 5.1.8 Other End-user Industries

- 5.2 Technology

- 5.2.1 Reactive

- 5.2.2 Solvent-borne

- 5.2.3 UV Cured Adhesives

- 5.2.4 Water-borne

- 5.3 Country

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Malaysia

- 5.3.7 Singapore

- 5.3.8 South Korea

- 5.3.9 Thailand

- 5.3.10 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 H.B. Fuller Company

- 6.4.4 Henkel AG & Co. KGaA

- 6.4.5 Hubei Huitian New Materials Co. Ltd

- 6.4.6 Huntsman International LLC

- 6.4.7 Kangda New Materials (Group) Co., Ltd.

- 6.4.8 NANPAO RESINS CHEMICAL GROUP

- 6.4.9 Pidilite Industries Ltd.

- 6.4.10 Sika AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

環氧樹脂黏合劑市場:全球市場預測(依樹脂類型、技術、形態、應用和最終用途產業分類)-2026-2032年可注射錨固環氧樹脂市場(按最終用戶、應用和產品形式分類),全球預測,2026-2032年

環氧樹脂黏合劑市場:全球市場預測(依樹脂類型、技術、形態、應用和最終用途產業分類)-2026-2032年可注射錨固環氧樹脂市場(按最終用戶、應用和產品形式分類),全球預測,2026-2032年 全球雙組分環氧樹脂粘合劑市場規模、佔有率、趨勢及成長分析報告(2026-2034)

全球雙組分環氧樹脂粘合劑市場規模、佔有率、趨勢及成長分析報告(2026-2034) 2026年全球環氧樹脂粘合劑市場報告2026年全球純環氧樹脂注射式化學錨定劑市場報告2026年全球高強度環氧樹脂黏合劑市場報告環氧彩色砂漿市場按包裝類型、最終用途產業、應用和分銷管道分類-2026-2032年全球預測環氧樹脂抗衝擊黏合劑市場按樹脂類型、固化技術、產品形式、最終用途產業、應用和分銷管道分類,全球預測(2026-2032年)

2026年全球環氧樹脂粘合劑市場報告2026年全球純環氧樹脂注射式化學錨定劑市場報告2026年全球高強度環氧樹脂黏合劑市場報告環氧彩色砂漿市場按包裝類型、最終用途產業、應用和分銷管道分類-2026-2032年全球預測環氧樹脂抗衝擊黏合劑市場按樹脂類型、固化技術、產品形式、最終用途產業、應用和分銷管道分類,全球預測(2026-2032年) 環氧膠黏劑市場-全球產業規模、佔有率、趨勢、機會及預測,依技術、應用、區域及競爭細分,2020-2030 年

環氧膠黏劑市場-全球產業規模、佔有率、趨勢、機會及預測,依技術、應用、區域及競爭細分,2020-2030 年 2025-2033年環氧膠黏劑市場報告(依產品類型、配銷通路、最終用途產業和地區)

2025-2033年環氧膠黏劑市場報告(依產品類型、配銷通路、最終用途產業和地區)

▼