|

市場調查報告書

商品編碼

1690842

拉丁美洲低溫運輸物流:市場佔有率分析、產業趨勢與成長預測(2025-2030)Latin America Cold Chain Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

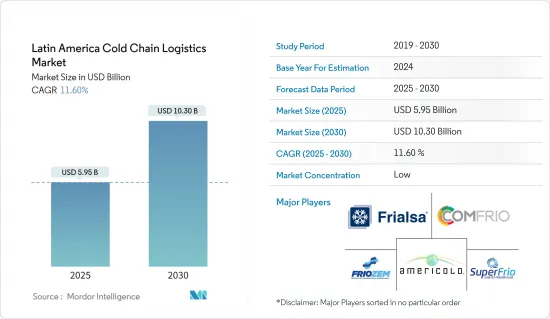

拉丁美洲低溫運輸物流市場規模預計在2025年為58.7億美元,預計到2030年將達到101.5億美元,預測期內(2025-2030年)的複合年成長率為11.60%。

拉丁美洲國家向全球出口各種各樣的產品,其中許多產品以天然、優質的狀態交付給消費者。這些產品包括肉類、魚類、水果和乳製品,高度依賴不間斷的低溫運輸。北美、歐洲甚至拉丁美洲本身都是主要的出口目的地,但某些產品也出口到非洲和南美,尤其是新冠疫苗等醫藥產品。

藥品需求激增,尤其是輝瑞/Biontech 的新冠疫苗等需要超低溫的藥品需求,正在推動拉丁美洲低溫運輸產業的創新和擴張。但勞動力短缺和基礎設施不足等挑戰依然存在,需要採取統一的政治、社會和財政應對措施。

拉丁美洲的疫苗貿易,加上對冷凍食品和乳製品日益成長的需求,對於推動市場至關重要。巴西位居榜首,其次是墨西哥、阿根廷和哥倫比亞。預計到 2025 年,加工食品銷售額將大幅成長,為低溫運輸物流和倉儲公司創造豐厚的利潤機會。預計秘魯在 2020 年至 2026 年期間的成長率將達到 15.16%,參與企業將加入該地區其他領先的低溫運輸企業。

儘管面臨勞動力短缺和倉庫爆滿等挑戰,拉丁美洲的生鮮食品供應鏈仍保持彈性。這些障礙促使該地區現有參與企業加強其技術力,以緩解該地區的冷凍空間短缺問題。

2022 年 10 月,總部位於烏拉圭蒙得維的亞的 Frigorifico Modelo (Frimosa) 宣布將其冷藏業務出售給 Emergent Cold LatAm。 Emergent Cold LatAm 是該地區主要企業,將收購 Frimosa 位於 Polo Oeste 的旗艦設施。此外,Emergent Cold LatAm 計劃在巴拉圭亞松森購買一個可容納 8,400 個托盤的倉庫。

總之,受藥品和生鮮食品需求不斷成長的推動,拉丁美洲的低溫運輸產業正在經歷強勁成長。儘管面臨勞動力短缺和基礎設施差距等挑戰,該行業仍準備透過技術進步和策略性投資實現進一步發展。 Emergent Cold LatAm 等主要企業持續的整合和擴張努力凸顯了該地區克服這些障礙和滿足不斷成長的市場需求的潛力。

拉丁美洲低溫運輸物流市場趨勢

增加對冷凍基礎設施的投資

生鮮食品國際貿易的增加使得對可靠低溫運輸的需求日益成長。在這些市場中運作的公司必須確保其產品在國際貿易中的品質和安全。生鮮食品國際貿易的成長推動了對強大低溫運輸的需求。該領域的公司必須優先考慮有效的低溫運輸管理,以確保國際運輸過程中的產品品質和安全。

為跨境客戶提供無縫的端到端連接不僅是一項策略性舉措,而且也是一個巨大的經濟優勢。這種方法簡化了供應鏈操作並提高了業務效率。從經濟角度來看,成本節約意味著盈利的提高和市場佔有率的增加,從而使公司成為更有價值的物流合作夥伴。

領先的溫控倉儲和物流供應商 Emergent Cold LatAm 在塔爾卡瓦諾開設了智利最大的冷凍食品倉庫。這一里程碑標誌著 EmergentCold 在拉丁美洲迄今為止最重要的擴張。塔爾卡瓦諾因其水產品和水果出口而聞名於世,該倉庫將在當地低溫運輸基礎設施中發揮至關重要的作用。

該設施的儲存容量為 294,000 立方米,可容納 37,000 個托盤,將創造 150 個直接就業機會和約 500 個間接就業機會,從而增強當地經濟。

在本地和國際投資者的支持下,該地區已經建立了專門的投資工具。從歷史上看,拉丁美洲並沒有統一的倉庫網路,只有巴西和墨西哥有一些例外。主要目標是建立一個跨境、泛拉丁美洲網路,提供全面的食品供應鏈解決方案。

受不斷成長的市場需求、技術進步以及對更高效、更廣泛的低溫運輸物流網路的迫切需求的推動,巴西是拉丁美洲冷資料儲存投資激增的領頭羊。

總之,以 Emergent Cold LatAm 新工廠為代表的拉丁美洲低溫運輸基礎設施的擴張凸顯了該地區在全球生鮮食品市場中日益成長的重要性。隨著投資的持續,該地區有望成為溫控物流的重要樞紐,確保生鮮產品跨境安全且有效率地運輸。

巴西在低溫運輸物流市場佔據主導地位。

近年來,巴西低溫運輸物流市場大幅擴張,主要得益於生鮮產品購買力的增強和製藥業的快速成長。值得注意的是,巴西的冷凍食品產業受到上層和中產階級消費者的購買所推動。

這些消費者表現出明顯的購買模式,其中25%的人每月購買冷凍食品4-5次,30%的人每月至少購買兩次,40%的人每月至少購買一次冷凍食品。女性在這一市場佔據主導地位,佔冷凍食品購買量的 73%。在冷凍食品中,肉類(39%)、披薩(33%)和千層麵(10%)最受歡迎。

此市場主要由中上階層(42%)和中下階層(29%)所構成。巴西中產階級的崛起,加上雙收入家庭面臨的時間限制,是支持冷凍食品市場成長的關鍵因素。

巴西冷凍食品產業由 700 多家冷凍食品公司組成,其中大多數(超過 90%)都是小型企業。巴西是冷凍肉類出口國中的重要角色,提供多種多樣的產品,包括冷凍牛肚、牛裡肌和各種牛肉切塊。

儘管巴西在冷凍食品領域佔據主導地位,但該國目前冷藏儲存能力僅600萬立方米,缺口約30%。此次短缺將對冷凍食品市場產生重大影響。冷藏和運輸設施不足會造成大量產品浪費,並影響冷凍食品的供應和價格。

為了滿足不斷成長的需求,巴西必須優先投資擴大其低溫運輸基礎設施。巴西的成長前景看好,尤其是在全球肉類市場,因為它是水果、肉類、糖和大豆的主要出口國。

巴西低溫運輸市場可望加速成長。這是由於多種因素造成的,包括該國冷藏產品出口的增加、現代技術和自動化的快速採用、對肉類、水產品、水果和蔬菜的需求不斷成長以及基礎設施的顯著改善。此外,隨著此類基礎設施的發展,冷藏運輸的市場佔有率預計會增加。

總之,受生鮮產品需求增加和基礎設施進步的推動,巴西低溫運輸物流市場呈現強勁成長動能。為了維持這種成長,重要的是解決當前冷資料儲存容量短缺的問題並利用現代技術。隨著巴西在全球市場,尤其是肉類出口領域的作用不斷擴大,低溫運輸物流領域將在確保貨物高效安全運輸方面發揮至關重要的作用。

拉丁美洲低溫運輸物流產業概況

拉丁美洲低溫運輸物流產業高度分散,既有本地參與者,也有全球參與企業。這種多樣性顯示競爭環境非常激烈,沒有一家公司能夠獨佔鰲頭。該領域的主要競爭對手包括Fralsa Frigorificos SA、Comfrio Solucoes Logisticas、Friozem Armazens Frigorificos、Superfrio Armazens Gerais 和 Americold Logistics。

這些公司正在轉向物聯網、RFID、雲端儲存和電子資料交換等最尖端科技,以提高低溫運輸物流的效率。為了鞏固市場結構,企業間的併購也增加。例如,Emergent Cold Latin America 收購 Frigorifico Modelo 在烏拉圭的業務以及在巴拉圭的新倉庫就凸顯了這一趨勢。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態與洞察

- 市場概況(低溫運輸物流市場現況)

- 市場動態

- 驅動程式

- 電子商務的成長

- 醫療領域佔市場主導地位

- 限制因素

- 供應鏈中斷

- 缺乏溫控倉庫

- 機會

- 技術創新

- 驅動程式

- 政府法規(冷藏儲存和運輸)

- 冷媒和包裝材料洞察

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 地緣政治與疫情將如何影響市場

第5章市場區隔

- 按服務

- 冷藏/冷凍倉庫

- 冷藏運輸

- 附加價值服務(訂單管理、冷凍、貼標、庫存管理等)

- 按溫度

- 冷藏

- 《冷凍》

- 常溫

- 按最終用戶

- 水果和蔬菜

- 乳製品(牛奶、奶油、起司、冰淇淋等)

- 魚、肉和水產品

- 加工食品

- 製藥

- 烘焙和糖果零食

- 其他

- 按國家

- 墨西哥

- 巴西

- 智利

- 哥倫比亞

- 其他拉丁美洲

第6章 競爭格局

- 市場集中度概覽

- 公司簡介

- Frialsa Frigorificos SA

- Comfrio Solucoes Logisticas

- Friozem Armazens Frigorificos Ltda

- Superfrio Armazens Gerais Ltda

- Americold Logistics

- Brasfrigo

- Arfrio Armazens Gerais Frigorificos

- Ransa Comercial SA

- Localfrio

- Qualianz*

- 其他公司(關鍵資訊/概述)

第7章:市場的未來

第 8 章 附錄

- 宏觀經濟因素

- 對外貿易統計

The Latin America Cold Chain Logistics Market size is estimated at USD 5.87 billion in 2025, and is expected to reach USD 10.15 billion by 2030, at a CAGR of 11.60% during the forecast period (2025-2030).

Latin American nations export a diverse range of products globally, with many reaching consumers in their natural state, emphasizing quality. These products, including meat, fish, fruits, and dairy, rely heavily on an uninterrupted cold chain. While North America, Europe, and even Latin America itself are primary destinations, certain products, notably pharmaceuticals like the Covid-19 vaccines, have found their way to Africa and South America.

The surge in demand for medicines, notably those requiring ultra-low temperatures like Pfizer/Biontech's Covid-19 vaccine, has propelled the cold chain sector in Latin America to innovate and expand. Yet, challenges persist, with labor shortages and inadequate infrastructure necessitating a unified political, social, and financial effort.

Latin America's vaccine trade, coupled with a rising appetite for frozen foods and dairy, has been pivotal in propelling the market. Brazil leads the pack, trailed by Mexico, Argentina, and Colombia. Projections suggest a significant uptick in processed food sales until 2025, presenting a lucrative opportunity for cold chain logistics and warehousing firms. Peru, poised for a 15.16% growth rate from 2020 to 2026, is set to join the region's leading cold chain players.

Despite challenges like workforce shortages and full-capacity warehouses, Latin America's perishable food supply chain remains resilient. These hurdles are prompting established regional players to bolster their technological prowess, aiming to combat the region's refrigerated space deficit.

In a notable move in October 2022, Uruguay's Montevideo-based Frigorifico Modelo (Frimosa) announced the sale of its cold storage operations to Emergent Cold Latin America (Emergent Cold LatAm). Emergent Cold LatAm, a key player in refrigerated storage and logistics in the region, will acquire Frimosa's primary facility in Polo Oeste, boasting 22,000 cold storage pallets, a bonded warehouse, and ample room for expansion. Additionally, Emergent Cold LatAm is set to purchase an 8,400-pallet warehouse in Asuncion, Paraguay.

In conclusion, the cold chain sector in Latin America is experiencing significant growth driven by increased demand for pharmaceuticals and perishable foods. Despite facing challenges such as labor shortages and infrastructure gaps, the sector is poised for further development through technological advancements and strategic investments. The ongoing consolidation and expansion efforts by key players like Emergent Cold LatAm highlight the region's potential to overcome these obstacles and meet the growing market demands.

Latin America Cold Chain Logistics Market Trends

Increasing investment in cold storage infrastructure

The increase in international trade in fresh food has led to an increase in the need for reliable cold chains. Companies operating in these markets must ensure the quality and safety of their products during internationaThe rise in global trade of fresh food has heightened the demand for robust cold chains. Companies in this space must prioritize effective cold chain management to guarantee product quality and safety during international transit.

Enabling seamless end-to-end connections for customers across nations is not just a strategic move but also a significant economic advantage. This approach streamlines supply chain operations, enhancing operational efficiency. Economically, it can lead to heightened profitability through cost savings and an expanded market share, positioning the company as a more valuable logistics partner.

Emergent Cold Latin America (Emergent Cold LatAm), the leading provider of temperature-controlled storage and logistics in the region, unveiled Chile's largest frozen food warehouse in Talcahuano. This milestone marks Emergent Cold's most substantial expansion in Latin America. Given Talcahuano's global reputation for seafood and fruit exports, this warehouse stands as a pivotal addition to the local cold chain infrastructure.

Boasting a storage capacity of 294,000 m3 and 37,000 pallets, this facility is set to create 150 direct jobs and an estimated 500 indirect job opportunities, bolstering the regional economy.

Backed by both local and international investors, a dedicated investment vehicle was established for the region. Historically, Latin America, barring a few exceptions in Brazil and Mexico, lacked a unified warehouse network. The primary aim was to create a pan-Latin American network, transcending individual borders, and offering a holistic food supply chain solution.

Brazil spearheads the surge in cold storage investments across Latin America, driven by rising market demands, technological progress, and the pressing need for more efficient and expansive cold chain logistics networks.

In conclusion, the expansion of cold chain infrastructure in Latin America, exemplified by Emergent Cold LatAm's new facility, highlights the region's growing importance in the global fresh food market. As investments continue to pour in, the region is poised to become a critical hub for temperature-controlled logistics, ensuring the safe and efficient transport of perishable goods across borders.

The cold chain logistics market is dominated by Brazil.

In recent years, the Brazil cold chain logistics market has seen notable expansion, primarily fueled by a rising appetite for perishable goods and the burgeoning pharmaceutical sector. Notably, Brazil's frozen food sector is buoyed by the purchases of its upper and middle-class consumers.

These consumers exhibit a noteworthy buying pattern: 25% purchase frozen food 4-5 times a month, 30% do so at least twice, and 40% make the purchase at least once monthly. Women, in particular, dominate this market, accounting for 73% of frozen food purchases. Among the frozen food offerings, meat (39%), pizzas (33%), and lasagnas (10%) stand out as the most favored.

The market is largely shaped by the high middle class (42%) and the low middle class (29%). The rise of Brazil's middle class, combined with the time constraints faced by working families, is a key driver behind the frozen food market's growth.

The industry boasts over 700 frozen food businesses in operation, with the majority (over 90%) classified as small enterprises. Brazil's role as a frozen meat exporter is substantial, offering a diverse range that includes frozen beef tripe, tenderloins, and various beef cuts.

Despite its prominence in the frozen food arena, Brazil's current cold storage capacity of 6 million cubic meters falls short by about 30%. This shortfall bears significant consequences for the frozen food market. Inadequate cold storage and transportation facilities can result in substantial product wastage, potentially affecting the supply and affordability of frozen foods.

To meet the escalating demand, Brazil must prioritize investments in expanding its cold chain infrastructure. Given its status as a leading exporter of fruits, meat, sugar, and soybeans, Brazil holds promising growth prospects, particularly in the global meat market.

The Brazil cold chain market is poised for accelerated growth. This is attributed to several factors, including the country's increased exports of refrigerated products, a surge in the adoption of modern technologies and automation, a rising appetite for meat, seafood, fruits, and vegetables, and notable improvements in infrastructure facilities. Furthermore, the market share of cold transport is expected to witness a rise, thanks to these enhanced infrastructure facilities.

In conclusion, the Brazil cold chain logistics market is on a robust growth trajectory, driven by the increasing demand for perishable goods and advancements in infrastructure. Addressing the current shortfall in cold storage capacity and leveraging modern technologies will be crucial for sustaining this growth. As Brazil continues to expand its role in the global market, particularly in meat exports, the cold chain logistics sector will play a pivotal role in ensuring the efficient and safe transportation of goods.

Latin America Cold Chain Logistics Industry Overview

In Latin America, the cold chain logistics sector stands out for its fragmentation, hosting a mix of local and global players. This diversity underlines a fiercely competitive landscape, where no single entity reigns supreme. Key contenders in this arena include Frialsa Frigorificos SA, Comfrio Solucoes Logisticas, Friozem Armazens Frigorificos, Superfrio Armazens Gerais, and Americold Logistics.

These companies are pivoting towards cutting-edge technologies like IoT, RFID, cloud storage, and electronic data interchange, amplifying the efficiency of their cold chain logistics. Mergers and acquisitions are on the rise, as firms seek to bolster their market foothold. For instance, Emergent Cold Latin America's acquisition of Frigorifico Modelo's operations in Uruguay and a new warehouse in Paraguay underscores this trend.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Market Overview (Current Scenario of the Cold Chain Logistics Market)

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Growth in E-commerce

- 4.2.1.2 Healthcare Sector is the market

- 4.2.2 Restraints

- 4.2.2.1 Supply Chain Disruptions

- 4.2.2.2 Lack of Temperature- Controlled Warehouses

- 4.2.3 Opportunities

- 4.2.3.1 Technological Innovations

- 4.2.1 Drivers

- 4.3 Government Regulations (Related to Cold Storage and Transport)

- 4.4 Insights into Refrigerants and Packaging Materials

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Impact of Geopolitics and Pandemic on the Market

5 MARKET SEGMENTATION

- 5.1 By Service

- 5.1.1 Cold Storage/Refrigerated Warehousing

- 5.1.2 Refrigerated Transportation

- 5.1.3 Value-added Services (Order Management, Blast Freezing, Labeling, Inventory Management, etc.)

- 5.2 By Temperature

- 5.2.1 Chilled

- 5.2.2 Frozen

- 5.2.3 Ambient

- 5.3 By End User

- 5.3.1 Fruits and Vegetables

- 5.3.2 Dairy Products (Milk, Butter, Cheese, Ice Cream, etc.)

- 5.3.3 Fish, Meat, and Seafood

- 5.3.4 Processed Food

- 5.3.5 Pharmaceutical (Includes Biopharma)

- 5.3.6 Bakery and Confectionery

- 5.3.7 Other End Users

- 5.4 By Country

- 5.4.1 Mexico

- 5.4.2 Brazil

- 5.4.3 Chile

- 5.4.4 Colombia

- 5.4.5 Rest of Latin America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Frialsa Frigorificos SA

- 6.2.2 Comfrio Solucoes Logisticas

- 6.2.3 Friozem Armazens Frigorificos Ltda

- 6.2.4 Superfrio Armazens Gerais Ltda

- 6.2.5 Americold Logistics

- 6.2.6 Brasfrigo

- 6.2.7 Arfrio Armazens Gerais Frigorificos

- 6.2.8 Ransa Comercial SA

- 6.2.9 Localfrio

- 6.2.10 Qualianz*

- 6.3 Other Companies (Key Information/Overview)

7 FUTURE OF THE MARKET

8 APPENDIX

- 8.1 Macroeconomic Factors

- 8.2 External Trade Statistics

RAP冷藏貨櫃市場:依貨櫃類型、冷卻系統類型、隔熱材料、容量、溫度範圍、應用、最終用戶分類,全球預測,2026-2032年

RAP冷藏貨櫃市場:依貨櫃類型、冷卻系統類型、隔熱材料、容量、溫度範圍、應用、最終用戶分類,全球預測,2026-2032年 2026-2030年全球低溫運輸市場

2026-2030年全球低溫運輸市場 低溫運輸市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、設備、解決方案、最終用戶分類

低溫運輸市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、設備、解決方案、最終用戶分類 亞太地區低溫運輸物流:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)西班牙低溫運輸物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

亞太地區低溫運輸物流:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)西班牙低溫運輸物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026-2034年全球低溫運輸物流市場規模、佔有率、趨勢及成長分析報告

2026-2034年全球低溫運輸物流市場規模、佔有率、趨勢及成長分析報告 日本低溫運輸運輸市場:規模、佔有率、趨勢和預測:按類型、應用、設備和地區分類,2026-2034年

日本低溫運輸運輸市場:規模、佔有率、趨勢和預測:按類型、應用、設備和地區分類,2026-2034年 低溫運輸物流市場-全球產業規模、佔有率、趨勢、機會與預測:按服務類型、應用、溫度類型、技術、地區和競爭格局分類,2021-2031年血漿分餾低溫運輸產品市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用戶、地區和競爭格局分類,2021-2031年低溫運輸物流車輛市場依運輸方式、溫度範圍、冷凍技術及終端用戶產業分類-2026-2032年全球預測

低溫運輸物流市場-全球產業規模、佔有率、趨勢、機會與預測:按服務類型、應用、溫度類型、技術、地區和競爭格局分類,2021-2031年血漿分餾低溫運輸產品市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用戶、地區和競爭格局分類,2021-2031年低溫運輸物流車輛市場依運輸方式、溫度範圍、冷凍技術及終端用戶產業分類-2026-2032年全球預測