|

市場調查報告書

商品編碼

1889166

全球多式聯運市場依構成、最終用途產業及地區分類-預測至2032年Multimodal Transport Market By Configuration (Two Mode, Three Mode, Hybrid/ Others), End-use Industry (Retail, Food & Beverages, Pharmaceuticals & Healthcare, Chemicals & Materials, Manufacturing), Region - Global Forecast to 2032 |

||||||

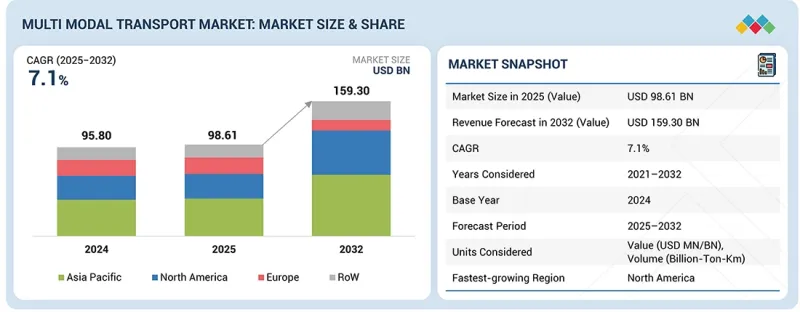

全球多式聯運市場預計將從 2025 年的 986.1 億美元成長到 2032 年的 1,593 億美元,複合年成長率為 7.1%。

市場成長的驅動力源自於日益分散的全球供應鏈中提高貨運效率的需求,以及從單一模式的公路運輸向公路、鐵路和水路一體化網路的轉變。隨著跨境配送對時間的要求越來越高,製造商和出口商越來越依賴多式聯運服務來管理不斷成長的貨運量、提高運輸計劃的可靠性並減少運輸時間的波動。

| 調查範圍 | |

|---|---|

| 調查期 | 2021-2032 |

| 基準年 | 2024 |

| 預測期 | 2025-2032 |

| 單元 | 百萬/十億美元,十億噸公里 |

| 部分 | 成分、最終用途產業、地區 |

| 目標區域 | 亞太地區、歐洲、北美和世界其他地區 |

先進的數位化平台能夠實現端到端的視覺化、自動化文件處理和動態路線最佳化,從而推動多式聯運在單一服務體系下的進一步普及。基礎設施的升級,包括新建多式聯運碼頭、港口鐵路連接、內河航道改造和多式聯運物流園區,提高了網路流動性和運力,同時減少了轉運環節。促進模式轉換和永續性的政策,例如碳減排指令和鐵路及沿海運輸激勵措施,正在加速向低排放貨運組合的轉型。地緣政治動盪、貿易路線的轉移以及近岸外包趨勢迫使企業實現運輸路線多元化,並在運輸網路中建立冗餘機制。對韌性、成本控制和可擴展運力的日益成長的需求,也促使托運人和物流供應商之間開展更緊密的合作,使多式聯運成為保障未來供應鏈的關鍵基礎。

“預計在預測期內,混合動力配置將在多式聯運市場獲得顯著需求。”

在預測期內,隨著貿易環境和網路限制的變化,企業日益尋求靈活的貨物運輸方式,混合運輸模式預計將在多式聯運市場中獲得顯著需求。與僵化的雙式聯運模式不同,混合運輸模式允許貨物根據運力可用性、路線可及性和服務優先級,在不同的運輸方式組合(例如公路-鐵路-水運或公路-航空-水運)之間靈活轉換。這種靈活的運輸結構在運輸模式波動較大的產業(例如製藥、電子產品和高價值製造業)中越來越受歡迎,因為在這些產業中,準時交貨和風險分散至關重要。跨境分銷的擴張和季節性貨運量高峰也推動了混合運輸模式的普及,這種模式可以在出現運輸中斷時將貨物重新路由至其他港口或內陸走廊。物流供應商正在透過擴大關鍵入口網站的多式聯運連接、加強承運商之間的合作以及整合支援即時模式切換的數位化工具來支持這項變革。隨著供應鏈向更靈活的營運模式轉型,混合運輸模式正成為托運人尋求連續性、客製化服務水準和增強對國際貨物流控制的關鍵選擇。

“到2024年,零售終端用戶行業將佔據多式聯運市場第二大佔有率。”

2024年,零售終端用戶產業在多式聯運市場中佔據第二大佔有率,這主要得益於消費者購買模式的快速變化以及對跨不同分銷點同步產品運輸日益成長的需求。隨著全通路模式的興起(實體店、線上平台和區域配送中心構成一個整合的網路),零售商需要能夠應對頻繁補貨、分散配送路線和訂單量波動的運輸解決方案。多式聯運使零售商能夠將遠距運輸的高效性與本地配送的靈活性相結合。大規模貨物透過海運或鐵路運輸,而對時間要求較高的出貨則透過道路運輸,運往門市和城市樞紐。生鮮電商的擴張和溫控商品的興起也推動了對綜合物流的日益依賴,尤其是在不同運輸方式轉換過程中維持產品品質。此外,高退貨率、促銷活動帶來的需求高峰以及假期季節需求的增加,都要求運輸模式能夠在不增加成本的情況下提供可預測的前置作業時間。

本報告分析了全球多式聯運市場,提供了關鍵促進因素和限制因素、競爭格局和未來趨勢的資訊。

目錄

第1章 引言

第2章調查方法

第3章執行摘要

第4章 主要發現

- 多式聯運市場對企業而言極具吸引力的機會

- 按地區分類的多式聯運市場

- 多式聯運市場構成

- 按最終用途行業分類的多式聯運市場

第5章 市場概覽

- 市場動態

- 促進要素

- 抑制因素

- 機會

- 任務

第6章:科技、專利、數位化和人工智慧應用帶來的策略顛覆

- 專利分析

- 技術分析

- 主要技術

- 互補技術

- 鄰近技術

- 技術藍圖

- 第一階段:數位化基礎、可見性(2024-2026 年)

- 第二階段:預測性、連結性和智慧化營運(2027-2030 年)

- 第三階段:自主、高度互聯、永續的生態系(2031-2035 年)

- 未來應用

- 人工智慧/生成式人工智慧的影響

- 主要應用案例和市場潛力

- 最佳實踐

- 案例研究

- 客戶對人工智慧/生成式人工智慧技術的接受程度

第7章永續性與監管環境

- 監管環境

- 監管機構、政府機構和其他組織

- 業界標準

- 對永續性的承諾

- 永續性影響和監管政策舉措

- EUROPEAN GREEN DEAL

- TRANS-EUROPEAN TRANSPORT NETWORK(TEN-T)

- PM GATI SHAKTI

- INFRASTRUCTURE INVESTMENT AND JOBS ACT(IIJA)

- 永續性影響和監管政策舉措

- 永續性勢在必行,正在改變多式聯運方式

- 企業措施旨在促進永續的多式聯運營運

- 市場影響分析

第8章 產業趨勢

- 總體經濟指標

- GDP趨勢與預測

- 多式聯運產業的全球趨勢

- 生態系分析

- 多式聯運營運商(MTO)

- 基礎設施和碼頭營運商

- 技術提供者/數位平台

- 監管和標準機構

- 最終用戶產業

- 定價分析

- 以運輸方式分類的貨運平均售價(2021-2024 年)

- 各地區公路貨運平均售價(2021-2024 年)

- 各地區鐵路貨運平均售價(2021-2024 年)

- 各地區平均航空貨運售價(2021-2024 年)

- 內河航運平均銷售價格:按地區分類(2021-2024 年)

- 影響客戶業務的趨勢與干擾因素

- 投資和資金籌措方案

- 資金籌措

- 重大會議和活動

- 案例研究分析

- 2025年美國關稅的影響

- 主要關稅稅率

- 價格影響分析

- 對國家的影響

- 對終端用戶產業的影響

9. 依服務類型分類的多式聯運市場

- 貨物運輸

- 倉儲/配送

- 運輸

- 附加價值服務

- 報關代理

第10章 多式聯運市場解決方案

- 供應鏈

- 貨物

- 運輸方式

- 宅配

- 卡車裝載

- 船運

第11章 多式聯運市場構成

- 2 方法配置

- 3種配置方法

- 混合/其他配置

- 主要發現

第12章 以最終用戶產業分類的多式聯運市場

- 零售

- 食品和飲料 (F&B)

- 化學品/材料

- 藥品和醫療保健

- 製造業

- 石油和天然氣

- 其他終端用戶產業

- 主要發現

第13章 各地區的多式聯運市場

- 亞太地區

- 宏觀經濟展望

- 中國

- 日本

- 印度

- 韓國

- 其他亞太地區

- 歐洲

- 宏觀經濟展望

- 法國

- 德國

- 西班牙

- 義大利

- 波蘭

- 其他歐洲

- 北美洲

- 宏觀經濟展望

- 美國

- 加拿大

- 墨西哥

- 其他地區

- 阿根廷

- 巴西

- 沙烏地阿拉伯

- 土耳其

- 其他

第14章 競爭格局

- 概述

- 主要參與企業的策略/優勢

- 市佔率分析(2024 年)

- 收入分析(2020-2024)

- 公司估值和財務指標

- 品牌/產品對比

- 企業評估矩陣:主要企業(2024)

- 公司評估矩陣:Start-Ups/中小企業(2024 年)

- 競爭場景

第15章:公司簡介

- 主要企業

- DSV

- DEUTSCHE POST AG

- KUEHNE+NAGEL

- NIPPON EXPRESS HOLDINGS

- AP MOLLER-MAERSK

- CMA CGM GROUP

- MARUBENI CORPORATION

- CH ROBINSON WORLDWIDE, INC.

- GEODIS

- XPO, INC.

- NYK LINE

- EXPEDITORS INTERNATIONAL OF WASHINGTON, INC.

- UNITED PARCEL SERVICE OF AMERICA, INC.

- HAPAG-LLOYD AG

- KLN LOGISTICS GROUP LIMITED

- 其他公司

- C & S TRANSPORTATION SERVICES, LLC.

- BDP INTERNATIONAL INC.

- CROWLEY

- DACHSER

- JB HUNT TRANSPORT, INC.

- RHENUS LOGISTICS SE & CO. KG.

- RYDER SYSTEM, INC.

- DP WORLD

- CJ LOGISTICS CORPORATION

- LOGISTEED, LTD.

第16章附錄

The multimodal transport market is projected to reach USD 159.30 billion by 2032 from USD 98.61 billion in 2025 at a CAGR of 7.1%. Market growth is fueled by the need to streamline freight movement across increasingly fragmented global supply chains and the shift from single-mode trucking to integrated road-rail-waterway networks. Manufacturers and exporters are increasingly relying on multimodal services to manage rising shipment volumes, improve schedule reliability, and reduce transit variability, particularly as cross-border distribution becomes more time-sensitive.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Units Considered | Value (USD Million/Billion), Volume (Billion-Ton-Km) |

| Segments | By Configuration, End-use Industry, Region |

| Regions covered | Asia Pacific, Europe, North America, and Rest of the World |

Advanced digital platforms enabling end-to-end visibility, automated documentation, and dynamic route optimization, supporting greater adoption of coordinated transport under a single service umbrella. Infrastructure upgrades, including new intermodal terminals, port-rail links, the revival of inland waterways, and multimodal logistics parks, are enhancing network fluidity and enabling higher throughput with fewer handoffs. Policy measures promoting modal shift and sustainability, such as carbon-reduction mandates and incentives for rail and coastal shipping, are accelerating the transition toward lower-emission freight combinations. Geopolitical disruptions, shifting trade lanes, and nearshoring trends are prompting companies to diversify routing options and build redundancy into transport networks. The rising demand for resilience, cost discipline, and scalable capacity is also driving closer collaboration between shippers and logistics providers, positioning multimodal transport as a critical enabler of future-ready supply chains.

"Hybrid-mode configurations are expected to witness significant demand in the multimodal transport market during the forecast period."

Hybrid-mode configurations are expected to experience notable demand in the multimodal transport market during the forecast period, as companies increasingly require flexible movement of freight across changing trade conditions and network constraints. Unlike fixed two-mode arrangements, hybrid setups enable cargo to shift between different transport combinations, such as road-rail-waterways or road-air-waterways, based on capacity availability, route accessibility, and service priorities. This adaptable structure is gaining traction among industries with variable shipment patterns, including pharmaceuticals, electronics, and high-value manufacturing, where delivery timing and risk diversification are critical. Growth in cross-border distribution and seasonal volume surges is also encouraging the adoption of hybrid movements that can reroute cargo through alternative ports or inland corridors when disruptions occur. Logistics providers are supporting this shift by expanding multimodal connectivity at key gateways, enhancing coordination across carriers, and integrating digital tools that enable real-time mode switching. As supply chains shift toward more agile operating models, hybrid-mode configurations are emerging as a crucial option for shippers seeking continuity, tailored service levels, and enhanced control over international freight flows.

"The retail end-use industry held the second-largest share of the multimodal transport market in 2024."

The retail end-use industry accounted for the second-largest share of the multimodal transport market in 2024, driven by the rapid evolution of consumer buying patterns and the increasing need for synchronized product movement across diverse distribution points. With the rise of omnichannel models, where physical stores, online platforms, and regional fulfillment centers operate as a unified network, retailers require transport solutions that can handle frequent restocking, dispersed delivery routes, and fluctuating order volumes. Multimodal setups enable retailers to combine long-haul efficiency with flexible regional distribution, using sea or rail for bulk inbound flows and road for time-sensitive outbound movements to stores and urban hubs. The expansion of grocery e-commerce and temperature-controlled product lines is also creating greater reliance on integrated logistics, particularly for maintaining product integrity during transfers between modes. Additionally, high return rates, promotional spikes, and holiday-season surges demand transport models that offer predictable lead times without increasing cost burdens.

" Asia Pacific held the largest share of the multimodal transport market in 2024."

The Asia Pacific accounted for the largest share of the multimodal transport market in 2024, driven by its dominant position in global manufacturing, export-oriented production, and rapidly expanding regional trade flows. The presence of major industrial hubs across China, India, Japan, and Southeast Asia has created dense freight corridors that link factories, inland logistics zones, and maritime gateways, resulting in a high reliance on integrated road-rail-sea combinations for both domestic distribution and international shipment cycles. The region's extensive port network, including major transshipment centers such as Singapore, Shanghai, and Busan, enhances connectivity to North America, Europe, and the Middle East. The rising intra-Asia trade is increasing demand for shorter, multimodal routes between emerging consumer markets. Large-scale infrastructure programs, such as China's Belt and Road Initiative, India's multimodal logistics parks, and Southeast Asia's rail expansion projects, are improving capacity, reducing transfer bottlenecks, and enabling faster modal transitions. Additionally, rapid growth in e-commerce, urban consumption, and contract manufacturing is driving higher freight volumes that require coordinated transport solutions. As companies prioritize cost efficiency, resilience, and regional supply-chain integration, the Asia Pacific is expected to retain its leading position throughout the forecast period.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and technology directors, and executives from various key organizations operating in this market.

- By Company Type: MNC 90% and Tier I - 10%

- By Designation: C- Level 45%, Director-Level- 30%, and Others - 25%

- By Region: Asia Pacific - 35%, North America - 40%, and Europe - 25%

The multi-modal transport market is dominated by major players, including DSV (Denmark), Deutsche Post AG (Germany), Kuehne+Nagel (Switzerland), NIPPON EXPRESS HOLDINGS (Japan), and A.P. Moller - Maersk (Denmark). These companies are expanding their portfolios to strengthen their multimodal transport market position.

Research Coverage:

The report covers the multimodal transport market in terms of configuration type (two-mode, three-mode, and hybrid/others), end-use industry (retail, manufacturing, healthcare & pharmaceuticals, food & beverages, chemicals & materials, oil & gas, and others), and region. It covers the competitive landscape and company profiles of the significant multimodal transport market players.

The study also includes an in-depth competitive analysis of the key market players, their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Key Benefits of Buying the Report:

- The report will help market leaders/new entrants with information on the closest approximations of revenue numbers for the multimodal transport market and its subsegments.

- This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies.

- The report will also help stakeholders understand the market pulse and provide information on key market drivers, restraints, challenges, and opportunities.

- The report will also help stakeholders understand the current and future pricing trends of the multimodal transport market.

- The report will help market leaders/new entrants with information on various trends in the multimodal transport market based on configuration type, end-use industry, and region.

The report provides insight into the following points:

- Analysis of key drivers (electrification to dominate the freight movement globally, cost efficiency through optimization and dynamic mode routing), restraints (dominance of road transport due to its flexibility and reliability, hindering modal shifts, limited adoption among SMEs due to complexity and resource constraints), opportunities (market access and entry into new trade routes, reduction of trade barriers fosters smoother cross-border movement of goods), and challenges (regulatory and legal barriers, including varying policies across regions)

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product launches in the multimodal transport market

- Market Development: Comprehensive information about lucrative markets (the report analyzes the multimodal transport market across varied regions)

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the multimodal transport market

- Competitive Assessment: In-depth assessment of shares, growth strategies, and service offerings of leading players, such as DSV (Denmark), Deutsche Post AG (Germany), Kuehne+Nagel (Switzerland), NIPPON EXPRESS HOLDINGS (Japan), and A.P. Moller - Maersk (Denmark), in the multimodal transport market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SNAPSHOT

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key secondary sources

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Primary participants

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- 2.3 DATA TRIANGULATION

- 2.4 RESEARCH LIMITATIONS

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

- 3.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 3.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 3.3 DISRUPTIVE TRENDS SHAPING MARKET

- 3.4 HIGH-GROWTH SEGMENTS AND EMERGING FRONTIERS

- 3.5 MNM INSIGHTS INTO MULTIMODAL TRANSPORT

- 3.6 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN MULTIMODAL TRANSPORT MARKET

- 4.2 MULTIMODAL TRANSPORT MARKET, BY REGION

- 4.3 MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION

- 4.4 MULTIMODAL TRANSPORT MARKET, BY END-USE INDUSTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Shift from conventional diesel-powered trucks to electric vehicles in logistics sector

- 5.2.1.1.1 Growth in electric truck sales

- 5.2.1.1.2 Policy and regulatory frameworks favoring electric truck adoption

- 5.2.1.2 Rise of sustainable fuels in transportation

- 5.2.1.3 Cost efficiency through optimization and dynamic mode routing

- 5.2.1.1 Shift from conventional diesel-powered trucks to electric vehicles in logistics sector

- 5.2.2 RESTRAINTS

- 5.2.2.1 Dominance of road transport due to its flexibility and reliability

- 5.2.2.2 Limited adoption among SMEs due to complexity and resource constraints

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Market access and entry into new trade routes

- 5.2.3.2 Reduction of trade barriers for smoother cross-border movement of goods

- 5.2.4 CHALLENGES

- 5.2.4.1 Regulatory and legal barriers

- 5.2.1 DRIVERS

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTION

- 6.1 PATENT ANALYSIS

- 6.1.1 LIST OF PATENTS

- 6.2 TECHNOLOGY ANALYSIS

- 6.2.1 KEY TECHNOLOGIES

- 6.2.1.1 Digital twins for transport networks

- 6.2.1.2 Multimodal transport management systems (TMS 2.0)

- 6.2.1.3 Blockchain

- 6.2.1.4 Autonomous & connected freight systems

- 6.2.1.5 Robotics & high-automation warehousing

- 6.2.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.2.1 Cybersecurity & secure access systems

- 6.2.2.2 RFID, NFC, and smart labeling

- 6.2.2.3 Power AR/VR for training and operations

- 6.2.3 ADJACENT TECHNOLOGIES

- 6.2.3.1 Holographic navigation interfaces

- 6.2.3.2 Urban and autonomous last-mile delivery

- 6.2.1 KEY TECHNOLOGIES

- 6.3 TECHNOLOGY ROADMAP

- 6.3.1 INTRODUCTION

- 6.3.2 PHASE 1 (2024-2026): DIGITAL FOUNDATION & VISIBILITY

- 6.3.3 PHASE 2 (2027-2030): PREDICTIVE, CONNECTED, AND INTELLIGENT OPERATIONS

- 6.3.4 PHASE 3 (2031-2035): AUTONOMOUS, HYPERCONNECTED, AND SUSTAINABLE ECOSYSTEMS

- 6.4 FUTURE APPLICATIONS

- 6.5 IMPACT OF AI/GEN AI

- 6.5.1 TOP USE CASES AND MARKET POTENTIAL

- 6.5.2 BEST PRACTICES

- 6.5.3 CASE STUDIES

- 6.5.4 CLIENTS' READINESS TO ADOPT AI/GEN AI

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGULATORY LANDSCAPE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.3.1 EUROPEAN GREEN DEAL

- 7.3.2 TRANS-EUROPEAN TRANSPORT NETWORK (TEN-T)

- 7.3.3 PM GATI SHAKTI

- 7.3.4 INFRASTRUCTURE INVESTMENT AND JOBS ACT (IIJA)

- 7.4 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4.1 SUSTAINABILITY IMPERATIVES TRANSFORMING MULTIMODAL TRANSPORT

- 7.4.1.1 Modal shift for emission reduction

- 7.4.1.2 Electrification & alternative fuels

- 7.4.1.3 Green corridors & eco-efficient hubs

- 7.4.2 CORPORATE INITIATIVES DRIVING SUSTAINABLE MULTIMODAL OPERATIONS

- 7.4.2.1 Digital optimization & AI

- 7.4.2.2 Green warehousing & intermodal terminals

- 7.4.3 MARKET IMPACT ANALYSIS

- 7.4.1 SUSTAINABILITY IMPERATIVES TRANSFORMING MULTIMODAL TRANSPORT

8 INDUSTRY TRENDS

- 8.1 MACROECONOMIC INDICATORS

- 8.1.1 INTRODUCTION

- 8.1.2 GDP TRENDS AND FORECAST

- 8.1.3 TRENDS IN GLOBAL MULTIMODAL TRANSPORT INDUSTRY

- 8.2 ECOSYSTEM ANALYSIS

- 8.2.1 MULTIMODAL TRANSPORT OPERATORS (MTOS)

- 8.2.2 INFRASTRUCTURE & TERMINAL OPERATORS

- 8.2.3 TECHNOLOGY PROVIDERS & DIGITAL PLATFORMS

- 8.2.4 REGULATORY BODIES & STANDARDS ORGANIZATIONS

- 8.2.5 END-USE INDUSTRIES

- 8.3 PRICING ANALYSIS

- 8.3.1 AVERAGE SELLING PRICE OF FREIGHT TRANSPORT, BY MODE, 2021-2024

- 8.3.2 AVERAGE SELLING PRICE OF ROAD FREIGHT, BY REGION, 2021-2024

- 8.3.3 AVERAGE SELLING PRICE OF RAIL FREIGHT, BY REGION, 2021-2024

- 8.3.4 AVERAGE SELLING PRICE OF AIR FREIGHT, BY REGION, 2021-2024

- 8.3.5 AVERAGE SELLING PRICE, INLAND WATERWAYS, BY REGION, 2021-2024

- 8.4 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 8.5 INVESTMENT AND FUNDING SCENARIO

- 8.6 FUNDING, BY USE CASE

- 8.7 KEY CONFERENCES AND EVENTS

- 8.8 CASE STUDY ANALYSIS

- 8.8.1 NOKIA ACHIEVED MAJOR EMISSION SAVINGS THROUGH DHL'S MULTIMODAL SOLUTION

- 8.8.2 DSV ENABLED ALLBIRDS TO SCALE UK E-COMMERCE AND RETAIL FULFILMENT WITH TAILORED LOGISTICS SUPPORT

- 8.8.3 C.H. ROBINSON HELPED LEADING US RETAILER ACHIEVE 98 % ON-TIME DELIVERY AND SAVE 12,000 LABOR HOURS THROUGH CONSOLIDATION-LED SUPPLY-CHAIN PROGRAM

- 8.8.4 XPO LOGISTICS IMPLEMENTED RIVER-BASED MULTIMODAL DELIVERY SOLUTION TO SERVE SHOPS IN PARIS

- 8.8.5 UPS BUILT END-TO-END SUPPLY CHAIN AND FREIGHT STRATEGY TO SERVE GLOBAL MARKETS

- 8.9 IMPACT OF US 2025 TARIFFS

- 8.9.1 INTRODUCTION

- 8.9.2 KEY TARIFF RATES

- 8.9.3 PRICE IMPACT ANALYSIS

- 8.9.4 IMPACT ON COUNTRIES/REGIONS

- 8.9.5 IMPACT ON END-USE INDUSTRIES

9 MULTIMODAL TRANSPORT MARKET, BY SERVICE TYPE

- 9.1 INTRODUCTION

- 9.2 FREIGHT FORWARDING

- 9.2.1 DIGITAL TRANSFORMATION AND AI-DRIVEN ORCHESTRATION RESHAPING GLOBAL FREIGHT FORWARDING SERVICE

- 9.3 WAREHOUSING & DISTRIBUTION

- 9.3.1 DIGITAL WAREHOUSING AND INTEGRATED DISTRIBUTION NETWORKS REDEFINING MULTIMODAL LOGISTICS PERFORMANCE

- 9.4 TRANSPORTATION

- 9.4.1 OPTIMIZING END-TO-END FREIGHT MOVEMENT WITH INTEGRATED, DATA-DRIVEN TRANSPORT NETWORKS

- 9.5 VALUE-ADDED SERVICES

- 9.5.1 ELEVATING CUSTOMER EXPERIENCE THROUGH ADVANCED, CUSTOMIZED VALUE-ADDED LOGISTICS SERVICES

- 9.6 CUSTOMS BROKERAGE

- 9.6.1 STREAMLINING GLOBAL TRADE FLOWS WITH INTEGRATED, HIGH-EFFICIENCY CUSTOMS BROKERAGE SOLUTIONS

10 MULTIMODAL TRANSPORT MARKET, BY SOLUTION

- 10.1 INTRODUCTION

- 10.2 SUPPLY CHAIN

- 10.2.1 RISING INVESTMENTS AND DIGITAL INTEGRATION TRANSFORMING MULTIMODAL SUPPLY CHAIN SOLUTIONS GLOBALLY

- 10.3 CARGO

- 10.3.1 GLOBAL INITIATIVES AND DIGITAL ADVANCEMENTS ACCELERATING CARGO SOLUTIONS IN MULTIMODAL TRANSPORT NETWORKS

- 10.4 CARRIAGE MODE

- 10.4.1 ADVANCED CARRIAGE NETWORKS AND STRATEGIC INVESTMENTS ENHANCING EFFICIENCY ACROSS GLOBAL MULTIMODAL TRANSPORT SYSTEMS

- 10.5 COURIER

- 10.5.1 DRIVING HIGH-SPEED FREIGHT MOVEMENT WITH UNIFIED, TECHNOLOGY-ENABLED COURIER SERVICES

- 10.6 TRUCK LOADING

- 10.6.1 BOOSTING MULTIMODAL EFFICIENCY WITH AGILE, DIGITALLY ENABLED TRUCK LOADING OPERATIONS

- 10.7 SHIPPING

- 10.7.1 BOOSTING MULTIMODAL EFFICIENCY WITH AGILE, DIGITALLY ENABLED TRUCK-LOADING OPERATIONS

11 MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION

- 11.1 INTRODUCTION

- 11.2 TWO-MODE CONFIGURATION

- 11.2.1 STRENGTHENING GLOBAL LOGISTICS THROUGH EXPANDING DOMINANCE OF TWO-MODE MULTIMODAL CONFIGURATIONS

- 11.3 THREE-MODE CONFIGURATION

- 11.3.1 ENHANCING GLOBAL TRADE CONNECTIVITY THROUGH STRATEGIC INVESTMENTS IN THREE-MODE TRANSPORT INFRASTRUCTURE

- 11.4 HYBRID/OTHER CONFIGURATIONS

- 11.4.1 HIGHER LEVEL OF AUTONOMY AND HIGH-SPEED IN-VEHICLE NETWORKS TO DRIVE MARKET

- 11.5 PRIMARY INSIGHTS

12 MULTIMODAL TRANSPORT MARKET, BY END-USE INDUSTRY

- 12.1 INTRODUCTION

- 12.2 RETAIL

- 12.2.1 EXPANDING INTERMODAL TERMINALS, UPGRADED INLAND PORTS, AND NEW TRADE CORRIDORS TO DRIVE MARKET

- 12.3 FOOD & BEVERAGES (F&B)

- 12.3.1 EXPANDING AGRICULTURAL AND FOOD COMMODITY TRADE TO DRIVE MARKET

- 12.4 CHEMICALS & MATERIALS

- 12.4.1 GROWTH OF FREIGHT VOLUMES ASSOCIATED WITH BASIC, SPECIALTY, AND HIGH-VALUE CHEMICAL SHIPMENTS TO DRIVE MARKET

- 12.5 PHARMACEUTICALS & HEALTHCARE

- 12.5.1 HIGH PRODUCT VALUE, TIME SENSITIVITY, AND STRINGENT HANDLING REQUIREMENTS TO DRIVE MARKET

- 12.6 MANUFACTURING

- 12.6.1 LARGE-SCALE MOVEMENT OF RAW MATERIALS AND FINISHED GOODS TO DRIVE MARKET

- 12.7 OIL & GAS

- 12.7.1 RISING GLOBAL OIL SUPPLY TO INTENSIFY MULTIMODAL LOGISTICS DEMAND ACROSS COMPLEX ENERGY VALUE CHAINS

- 12.8 OTHER END-USE INDUSTRIES

- 12.9 PRIMARY INSIGHTS

13 MULTIMODAL TRANSPORT MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 ASIA PACIFIC

- 13.2.1 MACROECONOMIC OUTLOOK

- 13.2.2 CHINA

- 13.2.2.1 Focus on integrated logistics, trade expansion, and green transportation to drive market

- 13.2.3 JAPAN

- 13.2.3.1 Modal shifts from road to rail and coastal shipping to reduce carbon emissions to drive market

- 13.2.4 INDIA

- 13.2.4.1 Emphasis on integrated logistics ecosystem that connects road, rail, air, and waterways to drive market

- 13.2.5 SOUTH KOREA

- 13.2.5.1 Rise in logistics infrastructure investments to drive market

- 13.2.6 REST OF ASIA PACIFIC

- 13.3 EUROPE

- 13.3.1 MACROECONOMIC OUTLOOK

- 13.3.2 FRANCE

- 13.3.2.1 Several targeted financial aid schemes to strengthen first- and last-mile connections to drive market

- 13.3.3 GERMANY

- 13.3.3.1 Goal of increasing rail freight's modal share to 25% by 2030

- 13.3.4 SPAIN

- 13.3.4.1 Investments in intermodal terminals, rail infrastructure upgrades, and acquisition of low-emission locomotives to drive market

- 13.3.5 ITALY

- 13.3.5.1 Investments in port-rail interfaces, multimodal terminal upgrades, and digital freight management systems to drive market

- 13.3.6 POLAND

- 13.3.6.1 Infrastructure modernization to enhance rail, road, and sea connectivity to drive market

- 13.3.7 REST OF EUROPE

- 13.4 NORTH AMERICA

- 13.4.1 MACROECONOMIC OUTLOOK

- 13.4.2 US

- 13.4.2.1 Government programs to promote zero-emission vehicles to drive growth

- 13.4.3 CANADA

- 13.4.3.1 Logistics modernization, digital documentation, and streamlined customs procedures to drive market

- 13.4.4 MEXICO

- 13.4.4.1 Upgrades to key ports, expanded highways, and industrial park developments to drive market

- 13.5 REST OF THE WORLD

- 13.5.1 ARGENTINA

- 13.5.2 BRAZIL

- 13.5.3 SAUDI ARABIA

- 13.5.4 TURKEY

- 13.5.5 OTHERS

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 14.3 MARKET SHARE ANALYSIS, 2024

- 14.4 REVENUE ANALYSIS, 2020-2024

- 14.5 COMPANY VALUATION AND FINANCIAL METRICS

- 14.5.1 COMPANY VALUATION

- 14.5.2 FINANCIAL METRICS

- 14.6 BRAND/PRODUCT COMPARISON

- 14.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT

- 14.7.5.1 Company footprint

- 14.7.5.2 Region footprint

- 14.7.5.3 End-use industry footprint

- 14.7.5.4 Service type footprint

- 14.7.5.5 Solution footprint

- 14.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING

- 14.8.5.1 List of startups/SMEs

- 14.8.5.2 Competitive benchmarking of startups/SMEs

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 SERVICE LAUNCHES

- 14.9.2 DEALS

- 14.9.3 EXPANSIONS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 DSV

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions/Services offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Service launches

- 15.1.1.3.2 Deals

- 15.1.1.4 MnM view

- 15.1.1.4.1 Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 DEUTSCHE POST AG

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions/Services offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Deals

- 15.1.2.4 MnM view

- 15.1.2.4.1 Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses and competitive threats

- 15.1.3 KUEHNE+NAGEL

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions/Services offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Deals

- 15.1.3.4 MnM view

- 15.1.3.4.1 Right to win

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses and competitive threats

- 15.1.4 NIPPON EXPRESS HOLDINGS

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions/Services offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Service launches

- 15.1.4.3.2 Deals

- 15.1.4.4 MnM view

- 15.1.4.4.1 Right to win

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses and competitive threats

- 15.1.5 A.P. MOLLER - MAERSK

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Deals

- 15.1.5.4 MnM view

- 15.1.5.4.1 Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 CMA CGM GROUP

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Deals

- 15.1.6.3.2 Expansions

- 15.1.6.3.3 Others

- 15.1.7 MARUBENI CORPORATION

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions/Services offered

- 15.1.8 C.H. ROBINSON WORLDWIDE, INC.

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions/Services offered

- 15.1.9 GEODIS

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Deals

- 15.1.9.3.2 Expansions

- 15.1.10 XPO, INC.

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.11 NYK LINE

- 15.1.11.1 Business overview

- 15.1.11.2 Products/Solutions/Services offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Service launches

- 15.1.11.3.2 Deals

- 15.1.12 EXPEDITORS INTERNATIONAL OF WASHINGTON, INC.

- 15.1.12.1 Business overview

- 15.1.12.2 Products/Solutions/Services offered

- 15.1.13 UNITED PARCEL SERVICE OF AMERICA, INC.

- 15.1.13.1 Business overview

- 15.1.13.2 Products/Solutions/Services offered

- 15.1.13.3 Recent developments

- 15.1.13.3.1 Deals

- 15.1.14 HAPAG-LLOYD AG

- 15.1.14.1 Business overview

- 15.1.14.2 Products/Solutions/Services offered

- 15.1.14.3 Recent developments

- 15.1.14.3.1 Service launches

- 15.1.14.3.2 Deals

- 15.1.15 KLN LOGISTICS GROUP LIMITED

- 15.1.15.1 Business overview

- 15.1.15.2 Products/Solutions/Services offered

- 15.1.15.3 Recent developments

- 15.1.15.3.1 Deals

- 15.1.1 DSV

- 15.2 OTHER PLAYERS

- 15.2.1 C & S TRANSPORTATION SERVICES, LLC.

- 15.2.2 BDP INTERNATIONAL INC.

- 15.2.3 CROWLEY

- 15.2.4 DACHSER

- 15.2.5 J.B. HUNT TRANSPORT, INC.

- 15.2.6 RHENUS LOGISTICS SE & CO. KG.

- 15.2.7 RYDER SYSTEM, INC.

- 15.2.8 DP WORLD

- 15.2.9 CJ LOGISTICS CORPORATION

- 15.2.10 LOGISTEED, LTD.

16 APPENDIX

- 16.1 KEY INSIGHTS OF INDUSTRY EXPERTS

- 16.2 DISCUSSION GUIDE

- 16.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.4 CUSTOMIZATION OPTIONS

- 16.4.1 MULTIMODAL TRANSPORT MARKET, BY CONTAINER FREIGHT, AT REGIONAL LEVEL

- 16.5 RELATED REPORTS

- 16.6 AUTHOR DETAILS

List of Tables

- TABLE 1 EXCHANGE RATE, 2021-2024

- TABLE 2 TRADE AGREEMENTS IN EMERGING MARKETS

- TABLE 3 RECENT BILATERAL & REGIONAL AGREEMENTS ENHANCING CROSS-BORDER TRADE

- TABLE 4 PATENTS GRANTED, 2022-2024

- TABLE 5 CURRENT STATUS AND SHORT/MID/LONG-TERM PROSPECTS OF TECHNOLOGIES IN MULTIMODAL TRANSPORT MARKET

- TABLE 6 TOP USE CASES AND MARKET POTENTIAL

- TABLE 7 COMPANIES IMPLEMENTING AI/GENERATIVE AI

- TABLE 8 CASE STUDIES OF AI/GENERATIVE AI IMPLEMENTATION IN MULTIMODAL TRANSPORT MARKET

- TABLE 9 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 10 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 11 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 12 REST OF WORLD: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 13 GLOBAL INDUSTRY STANDARDS

- TABLE 14 GDP PERCENTAGE CHANGE, BY COUNTRY, 2021-2030

- TABLE 15 ROLE OF COMPANIES IN ECOSYSTEM

- TABLE 16 AVERAGE SELLING PRICE OF FREIGHT TRANSPORT, BY MODE, 2021-2024 (USD/-TON-KM)

- TABLE 17 AVERAGE SELLING PRICE OF ROAD FREIGHT, BY REGION, 2021-2024 (USD/-TON-KM)

- TABLE 18 AVERAGE SELLING PRICE OF RAIL FREIGHT, BY REGION, 2021-2024 (USD/-TON-KM)

- TABLE 19 AVERAGE SELLING PRICE OF AIR FREIGHT, BY REGION, 2021-2024 (USD/-TON-KM)

- TABLE 20 AVERAGE SELLING PRICE, INLAND WATERWAYS, BY REGION, 2021-2024 (USD/-TON-KM)

- TABLE 21 KEY CONFERENCES AND EVENTS, 2025-2026

- TABLE 22 KEY TRENDS IMPACTING TRANSPORTATION SERVICE SEGMENT

- TABLE 23 MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (BILLION-TON-KM)

- TABLE 24 MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (BILLION-TON-KM)

- TABLE 25 MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (USD BILLION)

- TABLE 26 MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (USD BILLION)

- TABLE 27 TWO-MODE CONFIGURATION: MULTIMODAL TRANSPORT MARKET, BY REGION, 2021-2024 (BILLION-TON-KM)

- TABLE 28 TWO-MODE CONFIGURATION: MULTIMODAL TRANSPORT MARKET, BY REGION, 2025-2032 (BILLION-TON-KM)

- TABLE 29 TWO-MODE CONFIGURATION: MULTIMODAL TRANSPORT MARKET, BY REGION, 2021-2024 (USD BILLION)

- TABLE 30 TWO-MODE CONFIGURATION: MULTIMODAL TRANSPORT MARKET, BY REGION, 2025-2032 (USD BILLION)

- TABLE 31 THREE-MODE CONFIGURATION: MULTIMODAL TRANSPORT MARKET, BY REGION, 2021-2024 (BILLION-TON-KM)

- TABLE 32 THREE-MODE CONFIGURATION: MULTIMODAL TRANSPORT MARKET, BY REGION, 2025-2032 (BILLION-TON-KM)

- TABLE 33 THREE-MODE CONFIGURATION: MULTIMODAL TRANSPORT MARKET, BY REGION, 2021-2024 (USD BILLION)

- TABLE 34 THREE-MODE CONFIGURATION: MULTIMODAL TRANSPORT MARKET, BY REGION, 2025-2032 (USD BILLION)

- TABLE 35 HYBRID/OTHER CONFIGURATIONS: MULTIMODAL TRANSPORT MARKET, BY REGION, 2021-2024 (BILLION-TON-KM)

- TABLE 36 HYBRID/OTHER CONFIGURATIONS: MULTIMODAL TRANSPORT MARKET, BY REGION, 2025-2032 (BILLION-TON-KM)

- TABLE 37 HYBRID/OTHER CONFIGURATIONS: MULTIMODAL TRANSPORT MARKET, BY REGION, 2021-2024 (USD BILLION)

- TABLE 38 HYBRID/OTHER CONFIGURATIONS: MULTIMODAL TRANSPORT MARKET, BY REGION, 2025-2032 (USD BILLION)

- TABLE 39 MULTIMODAL TRANSPORT MARKET, BY END-USE INDUSTRY, 2021-2024 (BILLION-TON-KM)

- TABLE 40 MULTIMODAL TRANSPORT MARKET, BY END-USE INDUSTRY, 2025-2032 (BILLION-TON-KM)

- TABLE 41 MULTIMODAL TRANSPORT MARKET, BY END-USE INDUSTRY, 2021-2024 (USD BILLION)

- TABLE 42 MULTIMODAL TRANSPORT MARKET, BY END-USE INDUSTRY, 2025-2032 (USD BILLION)

- TABLE 43 RETAIL: MULTIMODAL TRANSPORT MARKET, BY REGION, 2021-2024 (BILLION-TON-KM)

- TABLE 44 RETAIL: MULTIMODAL TRANSPORT MARKET, BY REGION, 2025-2032 (BILLION-TON-KM)

- TABLE 45 RETAIL: MULTIMODAL TRANSPORT MARKET, BY REGION, 2021-2024 (USD BILLION)

- TABLE 46 RETAIL: MULTIMODAL TRANSPORT MARKET, BY REGION, 2025-2032 (USD BILLION)

- TABLE 47 FOOD & BEVERAGES INDUSTRY: MULTIMODAL TRANSPORT MARKET, BY REGION, 2021-2024 (BILLION-TON-KM)

- TABLE 48 FOOD & BEVERAGES INDUSTRY: MULTIMODAL TRANSPORT MARKET, BY REGION, 2025-2032 (BILLION-TON-KM)

- TABLE 49 FOOD & BEVERAGES INDUSTRY: MULTIMODAL TRANSPORT MARKET, BY REGION, 2021-2024 (USD BILLION)

- TABLE 50 FOOD & BEVERAGES INDUSTRY: MULTIMODAL TRANSPORT MARKET, BY REGION, 2025-2032 (USD BILLION)

- TABLE 51 CHEMICALS & MATERIALS INDUSTRY: MULTIMODAL TRANSPORT MARKET, BY REGION, 2021-2024 (BILLION-TON-KM)

- TABLE 52 CHEMICALS & MATERIALS INDUSTRY: MULTIMODAL TRANSPORT MARKET, BY REGION, 2025-2032 (BILLION-TON-KM)

- TABLE 53 CHEMICALS & MATERIALS INDUSTRY: MULTIMODAL TRANSPORT MARKET, BY REGION, 2021-2024 (USD BILLION)

- TABLE 54 CHEMICALS & MATERIALS INDUSTRY: MULTIMODAL TRANSPORT MARKET, BY REGION, 2025-2032 (USD BILLION)

- TABLE 55 PHARMACEUTICALS & HEALTHCARE INDUSTRY: MULTIMODAL TRANSPORT MARKET, BY REGION, 2021-2024 (BILLION-TON-KM)

- TABLE 56 PHARMACEUTICALS & HEALTHCARE INDUSTRY: MULTIMODAL TRANSPORT MARKET, BY REGION, 2025-2032 (BILLION-TON-KM)

- TABLE 57 PHARMACEUTICALS & HEALTHCARE INDUSTRY: MULTIMODAL TRANSPORT MARKET, BY REGION, 2021-2024 (USD BILLION)

- TABLE 58 PHARMACEUTICALS & HEALTHCARE INDUSTRY: MULTIMODAL TRANSPORT MARKET, BY REGION, 2025-2032 (USD BILLION)

- TABLE 59 MANUFACTURING INDUSTRY: MULTIMODAL TRANSPORT MARKET, BY REGION, 2021-2024 (BILLION-TON-KM)

- TABLE 60 MANUFACTURING INDUSTRY: MULTIMODAL TRANSPORT MARKET, BY REGION, 2025-2032 (BILLION-TON-KM)

- TABLE 61 MANUFACTURING INDUSTRY: MULTIMODAL TRANSPORT MARKET, BY REGION, 2021-2024 (USD BILLION)

- TABLE 62 MANUFACTURING INDUSTRY: MULTIMODAL TRANSPORT MARKET, BY REGION, 2025-2032 (USD BILLION)

- TABLE 63 OIL & GAS INDUSTRY: MULTIMODAL TRANSPORT MARKET, BY REGION, 2021-2024 (BILLION-TON-KM)

- TABLE 64 OIL & GAS INDUSTRY: MULTIMODAL TRANSPORT MARKET, BY REGION, 2025-2032 (BILLION-TON-KM)

- TABLE 65 OIL & GAS INDUSTRY: MULTIMODAL TRANSPORT MARKET, BY REGION, 2021-2024 (USD BILLION)

- TABLE 66 OIL & GAS INDUSTRY: MULTIMODAL TRANSPORT MARKET, BY REGION, 2025-2032 (USD BILLION)

- TABLE 67 OTHER END-USE INDUSTRIES: MULTIMODAL TRANSPORT MARKET, BY REGION, 2021-2024 (BILLION-TON-KM)

- TABLE 68 OTHER END-USE INDUSTRIES: MULTIMODAL TRANSPORT MARKET, BY REGION, 2025-2032 (BILLION-TON-KM)

- TABLE 69 OTHER END-USE INDUSTRIES: MULTIMODAL TRANSPORT MARKET, BY REGION, 2021-2024 (USD BILLION)

- TABLE 70 OTHER END-USE INDUSTRIES: MULTIMODAL TRANSPORT MARKET, BY REGION, 2025-2032 (USD BILLION)

- TABLE 71 MULTIMODAL TRANSPORT MARKET, BY REGION, 2021-2024 (BILLION-TON-KM)

- TABLE 72 MULTIMODAL TRANSPORT MARKET, BY REGION, 2025-2032 (BILLION-TON-KM)

- TABLE 73 MULTIMODAL TRANSPORT MARKET, BY REGION, 2021-2024 (USD BILLION)

- TABLE 74 MULTIMODAL TRANSPORT MARKET, BY REGION, 2025-2032 (USD BILLION)

- TABLE 75 ASIA PACIFIC: MULTIMODAL TRANSPORT MARKET, BY COUNTRY, 2021-2024 (BILLION-TON-KM)

- TABLE 76 ASIA PACIFIC: MULTIMODAL TRANSPORT MARKET, BY COUNTRY, 2025-2032 (BILLION-TON-KM)

- TABLE 77 ASIA PACIFIC: MULTIMODAL TRANSPORT MARKET, BY COUNTRY, 2021-2024 (USD BILLION)

- TABLE 78 ASIA PACIFIC: MULTIMODAL TRANSPORT MARKET, BY COUNTRY, 2025-2032 (USD BILLION)

- TABLE 79 ASIA PACIFIC: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (BILLION-TON-KM)

- TABLE 80 ASIA PACIFIC: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (BILLION-TON-KM)

- TABLE 81 ASIA PACIFIC: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (USD BILLION)

- TABLE 82 ASIA PACIFIC: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (USD BILLION)

- TABLE 83 CHINA: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (BILLION-TON-KM)

- TABLE 84 CHINA: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (BILLION-TON-KM)

- TABLE 85 CHINA: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (USD BILLION)

- TABLE 86 CHINA: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (USD BILLION)

- TABLE 87 JAPAN: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (BILLION-TON-KM)

- TABLE 88 JAPAN: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (BILLION-TON-KM)

- TABLE 89 JAPAN: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (USD BILLION)

- TABLE 90 JAPAN: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (USD BILLION)

- TABLE 91 INDIA: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (BILLION-TON-KM)

- TABLE 92 INDIA: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (BILLION-TON-KM)

- TABLE 93 INDIA: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (USD BILLION)

- TABLE 94 INDIA: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (USD BILLION)

- TABLE 95 SOUTH KOREA: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (BILLION-TON-KM)

- TABLE 96 SOUTH KOREA: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (BILLION-TON-KM)

- TABLE 97 SOUTH KOREA: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (USD BILLION)

- TABLE 98 SOUTH KOREA: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (USD BILLION)

- TABLE 99 REST OF ASIA PACIFIC: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (BILLION-TON-KM)

- TABLE 100 REST OF ASIA PACIFIC: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (BILLION-TON-KM)

- TABLE 101 REST OF ASIA PACIFIC: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (USD BILLION)

- TABLE 102 REST OF ASIA PACIFIC: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (USD BILLION)

- TABLE 103 EUROPE: MULTIMODAL TRANSPORT MARKET, BY COUNTRY, 2021-2024 (BILLION-TON-KM)

- TABLE 104 EUROPE: MULTIMODAL TRANSPORT MARKET, BY COUNTRY, 2025-2032 (BILLION-TON-KM)

- TABLE 105 EUROPE: MULTIMODAL TRANSPORT MARKET, BY COUNTRY, 2021-2024 (USD BILLION)

- TABLE 106 EUROPE: MULTIMODAL TRANSPORT MARKET, BY COUNTRY, 2025-2032 (USD BILLION)

- TABLE 107 EUROPE: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (BILLION-TON-KM)

- TABLE 108 EUROPE: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (BILLION-TON-KM)

- TABLE 109 EUROPE: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (USD BILLION)

- TABLE 110 EUROPE: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (USD BILLION)

- TABLE 111 FRANCE: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (BILLION-TON-KM)

- TABLE 112 FRANCE: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (BILLION-TON-KM)

- TABLE 113 FRANCE: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (USD BILLION)

- TABLE 114 FRANCE: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (USD BILLION)

- TABLE 115 GERMANY: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (BILLION-TON-KM)

- TABLE 116 GERMANY: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (BILLION-TON-KM)

- TABLE 117 GERMANY: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (USD BILLION)

- TABLE 118 GERMANY: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (USD BILLION)

- TABLE 119 SPAIN: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (BILLION-TON-KM)

- TABLE 120 SPAIN: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (BILLION-TON-KM)

- TABLE 121 SPAIN: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (USD BILLION)

- TABLE 122 SPAIN: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (USD BILLION)

- TABLE 123 ITALY: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (BILLION-TON-KM)

- TABLE 124 ITALY: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (BILLION-TON-KM)

- TABLE 125 ITALY: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (USD BILLION)

- TABLE 126 ITALY: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (USD BILLION)

- TABLE 127 POLAND: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (BILLION-TON-KM)

- TABLE 128 POLAND: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (BILLION-TON-KM)

- TABLE 129 POLAND: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (USD BILLION)

- TABLE 130 POLAND: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (USD BILLION)

- TABLE 131 REST OF EUROPE: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (BILLION-TON-KM)

- TABLE 132 REST OF EUROPE: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (BILLION-TON-KM)

- TABLE 133 REST OF EUROPE: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (USD BILLION)

- TABLE 134 REST OF EUROPE: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (USD BILLION)

- TABLE 135 NORTH AMERICA: MULTIMODAL TRANSPORT MARKET, BY COUNTRY, 2021-2024 (BILLION-TON-KM)

- TABLE 136 NORTH AMERICA: MULTIMODAL TRANSPORT MARKET, BY COUNTRY, 2025-2032 (BILLION-TON-KM)

- TABLE 137 NORTH AMERICA: MULTIMODAL TRANSPORT MARKET, BY COUNTRY, 2021-2024 (USD BILLION)

- TABLE 138 NORTH AMERICA: MULTIMODAL TRANSPORT MARKET, BY COUNTRY, 2025-2032 (USD BILLION)

- TABLE 139 NORTH AMERICA: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (BILLION-TON-KM)

- TABLE 140 NORTH AMERICA: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (BILLION-TON-KM)

- TABLE 141 NORTH AMERICA: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (USD BILLION)

- TABLE 142 NORTH AMERICA: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (USD BILLION)

- TABLE 143 US: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (BILLION-TON-KM)

- TABLE 144 US: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (BILLION-TON-KM)

- TABLE 145 US: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (USD BILLION)

- TABLE 146 US: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (USD BILLION)

- TABLE 147 CANADA: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (BILLION-TON-KM)

- TABLE 148 CANADA: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (BILLION-TON-KM)

- TABLE 149 CANADA: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (USD BILLION)

- TABLE 150 CANADA: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (USD BILLION)

- TABLE 151 MEXICO: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (BILLION-TON-KM)

- TABLE 152 MEXICO: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (BILLION-TON-KM)

- TABLE 153 MEXICO: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (USD BILLION)

- TABLE 154 MEXICO: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (USD BILLION)

- TABLE 155 REST OF WORLD: MULTIMODAL TRANSPORT MARKET, BY COUNTRY, 2021-2024 (BILLION-TON-KM)

- TABLE 156 REST OF WORLD: MULTIMODAL TRANSPORT MARKET, BY COUNTRY, 2025-2032 (BILLION-TON-KM)

- TABLE 157 REST OF WORLD: MULTIMODAL TRANSPORT MARKET, BY COUNTRY, 2021-2024 (USD BILLION)

- TABLE 158 REST OF WORLD: MULTIMODAL TRANSPORT MARKET, BY COUNTRY, 2025-2032 (USD BILLION)

- TABLE 159 REST OF WORLD: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (BILLION-TON-KM)

- TABLE 160 REST OF WORLD: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (BILLION-TON-KM)

- TABLE 161 REST OF WORLD: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (USD BILLION)

- TABLE 162 REST OF WORLD: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (USD BILLION)

- TABLE 163 ARGENTINA: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (BILLION-TON-KM)

- TABLE 164 ARGENTINA: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (BILLION-TON-KM)

- TABLE 165 ARGENTINA: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (USD BILLION)

- TABLE 166 ARGENTINA: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (USD BILLION)

- TABLE 167 BRAZIL: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (BILLION-TON-KM)

- TABLE 168 BRAZIL: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (BILLION-TON-KM)

- TABLE 169 BRAZIL: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (USD BILLION)

- TABLE 170 BRAZIL: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (USD BILLION)

- TABLE 171 SAUDI ARABIA: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (BILLION-TON-KM)

- TABLE 172 SAUDI ARABIA: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (BILLION-TON-KM)

- TABLE 173 SAUDI ARABIA: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (USD BILLION)

- TABLE 174 SAUDI ARABIA: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (USD BILLION)

- TABLE 175 TURKEY: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (BILLION-TON-KM)

- TABLE 176 TURKEY: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (BILLION-TON-KM)

- TABLE 177 TURKEY: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (USD BILLION)

- TABLE 178 TURKEY: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (USD BILLION)

- TABLE 179 OTHERS: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (BILLION-TON-KM)

- TABLE 180 OTHERS: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (BILLION-TON-KM)

- TABLE 181 OTHERS: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2021-2024 (USD BILLION)

- TABLE 182 OTHERS: MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025-2032 (USD BILLION)

- TABLE 183 KEY PLAYER STRATEGIES/RIGHT TO WIN, JANUARY 2021-SEPTEMBER 2025

- TABLE 184 DEGREE OF COMPETITION IN MULTIMODAL TRANSPORT MARKET, 2024

- TABLE 185 MULTIMODAL TRANSPORT MARKET: REGION FOOTPRINT, 2024

- TABLE 186 MULTIMODAL TRANSPORT MARKET: END-USE INDUSTRY FOOTPRINT, 2024

- TABLE 187 MULTIMODAL TRANSPORT MARKET: SERVICE TYPE FOOTPRINT, 2024

- TABLE 188 MULTIMODAL TRANSPORT MARKET: SOLUTION FOOTPRINT, 2024

- TABLE 189 MULTIMODAL TRANSPORT MARKET: LIST OF STARTUPS/SMES

- TABLE 190 MULTIMODAL TRANSPORT MARKET: COMPETITIVE BENCHMARKING OF STARTUPS/SMES, 2024

- TABLE 191 MULTIMODAL TRANSPORT MARKET: SERVICE LAUNCHES, JANUARY 2021-SEPTEMBER 2025

- TABLE 192 MULTIMODAL TRANSPORT MARKET: DEALS, JANUARY 2021-SEPTEMBER 2025

- TABLE 193 MULTIMODAL TRANSPORT MARKET: EXPANSIONS, JANUARY 2021-SEPTEMBER 2025

- TABLE 194 DSV: COMPANY OVERVIEW

- TABLE 195 DSV: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 196 DSV: SERVICE LAUNCHES

- TABLE 197 DSV: DEALS

- TABLE 198 DEUTSCHE POST AG: COMPANY OVERVIEW

- TABLE 199 DEUTSCHE POST AG: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 200 DEUTSCHE POST AG: DEALS

- TABLE 201 KUEHNE+NAGEL: COMPANY OVERVIEW

- TABLE 202 KUEHNE+NAGEL: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 203 KUEHNE+NAGEL: DEALS

- TABLE 204 NIPPON EXPRESS HOLDINGS: COMPANY OVERVIEW

- TABLE 205 NIPPON EXPRESS HOLDINGS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 206 NIPPON EXPRESS HOLDINGS: SERVICE LAUNCHES

- TABLE 207 NIPPON EXPRESS HOLDINGS: DEALS

- TABLE 208 A.P. MOLLER - MAERSK: COMPANY OVERVIEW

- TABLE 209 A.P. MOLLER - MAERSK: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 210 A.P. MOLLER - MAERSK: DEALS

- TABLE 211 CMA CGM GROUP: COMPANY OVERVIEW

- TABLE 212 CMA CGM GROUP: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 213 CMA CGM GROUP: DEALS

- TABLE 214 CMA CGM GROUP: EXPANSIONS

- TABLE 215 CMA CGM GROUP: OTHERS

- TABLE 216 MARUBENI CORPORATION: COMPANY OVERVIEW

- TABLE 217 MARUBENI CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 218 C.H. ROBINSON WORLDWIDE, INC.: COMPANY OVERVIEW

- TABLE 219 C.H. ROBINSON WORLDWIDE, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 220 GEODIS: COMPANY OVERVIEW

- TABLE 221 GEODIS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 222 GEODIS: DEALS

- TABLE 223 GEODIS: EXPANSIONS

- TABLE 224 XPO, INC.: COMPANY OVERVIEW

- TABLE 225 XPO, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 226 NYK LINE: COMPANY OVERVIEW

- TABLE 227 NYK LINE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 228 NYK LINE: SERVICE LAUNCHES

- TABLE 229 NYK LINE: DEALS

- TABLE 230 EXPEDITORS INTERNATIONAL OF WASHINGTON, INC.: COMPANY OVERVIEW

- TABLE 231 EXPEDITORS INTERNATIONAL OF WASHINGTON, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 232 UNITED PARCEL SERVICE OF AMERICA, INC.: COMPANY OVERVIEW

- TABLE 233 UNITED PARCEL SERVICE OF AMERICA, INC.: PRODUCTS/SOLUTIONS/ SERVICES OFFERED

- TABLE 234 UNITED PARCEL SERVICE OF AMERICA, INC.: DEALS

- TABLE 235 HAPAG-LLOYD AG: COMPANY OVERVIEW

- TABLE 236 HAPAG-LLOYD AG: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 237 HAPAG-LLOYD AG: SERVICE LAUNCHES

- TABLE 238 HAPAG-LLOYD AG: DEALS

- TABLE 239 KLN LOGISTICS GROUP LIMITED: COMPANY OVERVIEW

- TABLE 240 KLN LOGISTICS GROUP LIMITED: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 241 KLN LOGISTICS GROUP LIMITED: DEALS

List of Figures

- FIGURE 1 RESEARCH DESIGN

- FIGURE 2 RESEARCH DESIGN MODEL

- FIGURE 3 BREAKDOWN OF PRIMARY INTERVIEWS

- FIGURE 4 RESEARCH METHODOLOGY: HYPOTHESIS BUILDING

- FIGURE 5 BOTTOM-UP APPROACH

- FIGURE 6 TOP-DOWN APPROACH

- FIGURE 7 DATA TRIANGULATION

- FIGURE 8 KEY INSIGHTS AND MARKET HIGHLIGHTS

- FIGURE 9 STRATEGIC DEVELOPMENTS BY KEY PLAYERS IN MULTIMODAL TRANSPORT MARKET

- FIGURE 10 DISRUPTIVE TRENDS IMPACTING MULTIMODAL TRANSPORT MARKET

- FIGURE 11 TWO-MODE CONFIGURATION TO BE LEADING CONFIGURATION SEGMENT DURING FORECAST PERIOD

- FIGURE 12 NEW VALUE STREAMS FOR STAKEHOLDERS IN MULTIMODAL TRANSPORT MARKET

- FIGURE 13 NORTH AMERICA TO RECORD FASTEST GROWTH DURING FORECAST PERIOD

- FIGURE 14 SUPPORTIVE GOVERNMENT POLICIES, E-COMMERCE GROWTH, AND BOOMING EXPORTS TO DRIVE MARKET

- FIGURE 15 ASIA PACIFIC TO BE LARGEST MARKET FOR MULTIMODAL TRANSPORT IN 2025

- FIGURE 16 TWO-MODE CONFIGURATION TO BE DOMINANT DURING FORECAST PERIOD

- FIGURE 17 MANUFACTURING END-USE INDUSTRY TO SECURE LEADING POSITION DURING FORECAST PERIOD

- FIGURE 18 MULTIMODAL TRANSPORT MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, CHALLENGES

- FIGURE 19 REGION-WISE ADOPTION OF ELECTRIC TRUCKS

- FIGURE 20 RESTRAINTS FOR SMES IN ADOPTING MULTIMODAL SERVICES

- FIGURE 21 PATENT ANALYSIS, 2015-2024

- FIGURE 22 ECOSYSTEM ANALYSIS

- FIGURE 23 AVERAGE SELLING PRICE OF FREIGHT TRANSPORT, BY MODE, 2021-2024 (USD/-TON-KM)

- FIGURE 24 AVERAGE SELLING PRICE OF ROAD FREIGHT, BY REGION, 2021-2024 (USD/-TON-KM)

- FIGURE 25 AVERAGE SELLING PRICE OF RAIL FREIGHT, BY REGION, 2021-2024 (USD/-TON-KM)

- FIGURE 26 AVERAGE SELLING PRICE OF AIR FREIGHT, BY REGION, 2021-2024 (USD/-TON-KM)

- FIGURE 27 AVERAGE SELLING PRICE, INLAND WATERWAYS, BY REGION, 2021-2024 (USD/-TON-KM)

- FIGURE 28 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 29 INVESTMENT AND FUNDING SCENARIO, 2020-2024 (USD BILLION)

- FIGURE 30 MULTIMODAL TRANSPORT MARKET, BY SERVICE TYPE

- FIGURE 31 FREIGHT FORWARDING: MULTIMODAL TRANSPORT MARKET

- FIGURE 32 VALUE-ADDED SERVICES IN MULTIMODAL TRANSPORT MARKET

- FIGURE 33 MULTIMODAL TRANSPORT MARKET, BY SOLUTION

- FIGURE 34 SUPPLY CHAIN SOLUTIONS IN MULTIMODAL TRANSPORT MARKET

- FIGURE 35 SHIPPING SOLUTIONS IN MULTIMODAL TRANSPORT MARKET

- FIGURE 36 MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION

- FIGURE 37 MULTIMODAL TRANSPORT MARKET, BY CONFIGURATION, 2025 VS. 2032 (USD BILLION)

- FIGURE 38 MULTIMODAL TRANSPORT MARKET: BY END-USE INDUSTRY

- FIGURE 39 MULTIMODAL TRANSPORT MARKET, BY END-USE INDUSTRY, 2025 VS. 2032 (USD BILLION)

- FIGURE 40 MULTIMODAL TRANSPORT MARKET, BY REGION, 2025 VS. 2032 (USD BILLION)

- FIGURE 41 ASIA PACIFIC: REAL GDP GROWTH RATE, BY COUNTRY, 2024-2026

- FIGURE 42 ASIA PACIFIC: GDP PER CAPITA, BY COUNTRY, 2024-2026

- FIGURE 43 ASIA PACIFIC: INFLATION RATE AVERAGE CONSUMER PRICES, BY COUNTRY, 2024-2026

- FIGURE 44 ASIA PACIFIC: MANUFACTURING INDUSTRY'S CONTRIBUTION TO GDP, 2024

- FIGURE 45 ASIA PACIFIC: MULTIMODAL TRANSPORT MARKET SNAPSHOT

- FIGURE 46 EUROPE: REAL GDP GROWTH RATE, BY COUNTRY, 2024-2026

- FIGURE 47 EUROPE: GDP PER CAPITA, BY COUNTRY, 2024-2026

- FIGURE 48 EUROPE: INFLATION RATE AVERAGE CONSUMER PRICES, BY COUNTRY, 2024-2026

- FIGURE 49 EUROPE MANUFACTURING INDUSTRY'S CONTRIBUTION TO GDP, 2024

- FIGURE 50 EUROPE: MULTIMODAL TRANSPORT MARKET SNAPSHOT

- FIGURE 51 NORTH AMERICA: REAL GDP GROWTH RATE, BY COUNTRY, 2024-2026

- FIGURE 52 NORTH AMERICA: GDP PER CAPITA, BY COUNTRY, 2024-2026

- FIGURE 53 NORTH AMERICA: CPI INFLATION RATE, BY COUNTRY, 2024-2026

- FIGURE 54 NORTH AMERICA: MANUFACTURING INDUSTRY'S CONTRIBUTION TO GDP, 2024

- FIGURE 55 NORTH AMERICA: MULTIMODAL TRANSPORT MARKET SNAPSHOT

- FIGURE 56 REST OF THE WORLD: MULTIMODAL TRANSPORT MARKET SNAPSHOT

- FIGURE 57 MULTIMODAL TRANSPORT MARKET SHARE ANALYSIS, 2024

- FIGURE 58 MULTIMODAL TRANSPORT MARKET: REVENUE ANALYSIS OF TOP LISTED PLAYERS, 2020-2024

- FIGURE 59 COMPANY VALUATION OF KEY PLAYERS, OCTOBER 2025 (USD BILLION)

- FIGURE 60 FINANCIAL METRICS OF KEY PLAYERS, OCTOBER 2025 (EV/EBITDA)

- FIGURE 61 MULTIMODAL TRANSPORT MARKET: BRAND/PRODUCT COMPARISON

- FIGURE 62 COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

- FIGURE 63 MULTIMODAL TRANSPORT MARKET: COMPANY FOOTPRINT, 2024

- FIGURE 64 MULTIMODAL TRANSPORT MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

- FIGURE 65 DSV: COMPANY SNAPSHOT

- FIGURE 66 DEUTSCHE POST AG: COMPANY SNAPSHOT

- FIGURE 67 KUEHNE+NAGEL: COMPANY SNAPSHOT

- FIGURE 68 NIPPON EXPRESS HOLDINGS: COMPANY SNAPSHOT

- FIGURE 69 A.P. MOLLER - MAERSK: COMPANY SNAPSHOT

- FIGURE 70 CMA CGM GROUP: COMPANY SNAPSHOT

- FIGURE 71 MARUBENI CORPORATION: COMPANY SNAPSHOT

- FIGURE 72 C.H. ROBINSON WORLDWIDE, INC.: COMPANY SNAPSHOT

- FIGURE 73 GEODIS: COMPANY SNAPSHOT

- FIGURE 74 XPO, INC.: COMPANY SNAPSHOT

- FIGURE 75 NYK LINE: COMPANY SNAPSHOT

- FIGURE 76 EXPEDITORS INTERNATIONAL OF WASHINGTON, INC.: COMPANY SNAPSHOT

- FIGURE 77 UNITED PARCEL SERVICE OF AMERICA, INC.: COMPANY SNAPSHOT

- FIGURE 78 HAPAG-LLOYD AG: COMPANY SNAPSHOT

- FIGURE 79 KLN LOGISTICS GROUP LIMITED: COMPANY SNAPSHOT

汽車人工智慧市場:2026-2032年全球市場預測(按交付方式、核心技術、車輛類型、應用和最終用戶分類)

汽車人工智慧市場:2026-2032年全球市場預測(按交付方式、核心技術、車輛類型、應用和最終用戶分類) 汽車人工智慧處理器市場預測至2034年——按處理器類型、車輛類型、部署等級、應用和地區分類的全球分析

汽車人工智慧處理器市場預測至2034年——按處理器類型、車輛類型、部署等級、應用和地區分類的全球分析 汽車技術研究展望:2025

汽車技術研究展望:2025 遙感器市場報告:趨勢、預測及競爭分析(至2035年)

遙感器市場報告:趨勢、預測及競爭分析(至2035年) 2026年全球汽車元宇宙宇宙市場報告2026年全球汽車與交通運輸人工智慧市場報告2026年全球車載人工智慧助理市場報告

2026年全球汽車元宇宙宇宙市場報告2026年全球汽車與交通運輸人工智慧市場報告2026年全球車載人工智慧助理市場報告 汽車奈米技術市場-策略性洞察與預測(2026-2031年)

汽車奈米技術市場-策略性洞察與預測(2026-2031年) 汽車人工智慧 (AI) 軟體市場分析及預測(至 2035 年):按類型、產品、服務、技術、組件、應用、部署、最終用戶、功能和解決方案分類2026年全球遙感探測設備(RSD)與車輛智慧系統市場報告

汽車人工智慧 (AI) 軟體市場分析及預測(至 2035 年):按類型、產品、服務、技術、組件、應用、部署、最終用戶、功能和解決方案分類2026年全球遙感探測設備(RSD)與車輛智慧系統市場報告