|

市場調查報告書

商品編碼

1822585

汽車市場中的生成式人工智慧機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Generative AI in Automotive Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

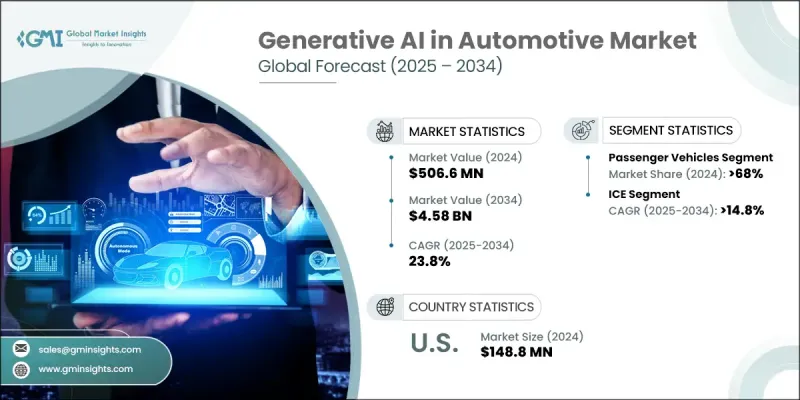

2024 年全球汽車生成人工智慧市場價值為 5.066 億美元,預計到 2034 年將以 23.8% 的複合年成長率成長至 45.8 億美元。

隨著汽車製造商擴大整合生成式人工智慧來簡化自動駕駛系統、最佳化設計工作流程並模擬關鍵駕駛場景,汽車產業正在經歷快速轉型。監管部門的鼓勵和資金支持正在推動汽車製造商、零件供應商和出行技術創新者的研發。隨著數位化進程的深入以及汽車智慧化和互聯化程度的提高,生成式人工智慧正成為汽車開發的核心。它使汽車製造商能夠複製罕見或複雜的交通事件,從而大幅縮短安全驗證所需的時間和成本。這種先進的功能正在樹立模擬精度的新標準,並有助於縮短開發週期。汽車製造商目前正在利用生成式人工智慧來增強使用者介面、預測維護需求並微調進階駕駛輔助系統。隨著汽車產業向軟體定義汽車和連網平台轉型,人工智慧不再只是一種增強功能,而是下一代出行生態系統的核心推動力。軟體公司和硬體開發商之間的合作正在建立基礎設施,以支援人工智慧在汽車環境中的無縫整合。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 5.066億美元 |

| 預測值 | 45.8億美元 |

| 複合年成長率 | 23.8% |

2024年,乘用車市場佔了68%的市場佔有率,這得益於智慧系統在車輛領域的廣泛應用。人工智慧技術如今已深深融入高級資訊娛樂、駕駛支援功能和車載安全系統等功能中。這些工具透過對話介面改善互動體驗,提供個人化洞察,並支援即時自適應回應,顯著提升了駕駛體驗。汽車製造商正專注於開發能夠增強安全性和功能性的人工智慧工具,例如主動服務通知和情境感知駕駛建議等功能。隨著感測器技術和遠端軟體更新的不斷改進,生成式人工智慧在該領域的應用預計將穩步成長。

預計2025年至2034年,內燃機 (ICE) 汽車市場的複合年成長率將達到14.8%。雖然電動車平台通常處於技術應用的前沿,但內燃機汽車也在整合人工智慧驅動的系統以保持競爭力。汽車製造商正在升級現有的內燃機車型,為其配備智慧模組,以支援更強大的診斷功能、無縫互聯和沈浸式數位體驗。這項變革的驅動力來自於高階內燃機汽車對智慧功能日益成長的需求,如今,透過無線更新和可擴展平台技術,這些汽車更容易實現基於人工智慧系統的改裝。增強型車載軟體使傳統車型無需進行大規模硬體重新設計即可受益於先進的預測功能。

2024年,美國汽車生成式人工智慧市場產值達1.488億美元。憑藉強大的創新格局、雄厚的研發實力以及與學術機構、技術供應商和政府機構的通力合作,美國將繼續保持領先地位。生成式人工智慧在車輛系統及其支援的數位基礎設施中的整合正在迅速推進。這些因素使美國成為生成式人工智慧解決方案開發和應用的主要樞紐,尤其是在增強即時駕駛智慧、簡化車輛設計流程和促進智慧出行解決方案方面。

積極塑造全球汽車生成人工智慧市場的關鍵參與者包括 NVIDIA、亞馬遜網路服務 (AWS)、博世、微軟、高通、Aptiv、IBM、大陸集團、英特爾和Google。為了在汽車生成人工智慧市場保持競爭優勢,主要參與者正專注於策略聯盟、技術創新和平台開發。各公司正在與汽車製造商和一級供應商建立長期合作夥伴關係,以確保跨車輛系統的無縫人工智慧整合。對先進模擬工具、即時資料處理和邊緣人工智慧運算的投資是其成長方式的核心。主要公司還透過 SDK 和 API 擴展其軟體生態系統,使開發人員能夠更快地建立人工智慧應用程式。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基礎估算與計算

- 基準年計算

- 市場評估的主要趨勢

- 初步研究和驗證

- 主要來源

- 預測模型

- 研究假設和局限性

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率分析

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 車輛設計和 ADAS 中的 AI 整合

- 電動車和連網汽車的普及率不斷提高

- 雲端和邊緣 AI 部署

- OEM科技公司合作

- 多模式人工智慧的進步

- 產業陷阱與挑戰

- 資料隱私和網路安全

- 與遺留系統整合

- 市場機會

- 軟體定義和自動駕駛汽車的擴展

- 與學術和研究機構的合作

- 亞太地區和拉丁美洲的新興市場

- 與行動服務整合

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 成本分解分析

- 專利分析

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考慮

- 用例和應用

- 車輛設計與工程應用

- 製造和生產應用

- 自動駕駛和ADAS應用

- 客戶體驗與服務應用

- 最佳情況

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 生成式人工智慧技術基礎與演進

- 生成式人工智慧技術架構與能力

- 人工智慧模型開發和培訓基礎設施

- 汽車專用AI模型開發

- 技術演進與未來路線圖

- 未來技術路線圖與創新時間表

- 生成式人工智慧技術演進(2024-2034)

- 汽車人工智慧應用發展時間表

- 技術融合與整合場景

- 顛覆性技術評估與市場影響

- 汽車產業數位轉型背景

- 汽車產業技術顛覆格局

- 數位孿生與仿真技術整合

- 數據驅動的決策與分析

- 汽車軟體和平台生態系統

- 監管環境和標準框架

- 人工智慧治理與監管格局

- 汽車安全標準和人工智慧整合

- 國際標準和協調努力

- 道德人工智慧和負責任的發展框架

- 投資前景和資金分析

- 全球人工智慧投資趨勢與汽車焦點

- 汽車業AI投資模式

- 區域投資格局與政府支持

- 新創企業生態系統與創新中心

- 網路安全與風險管理框架

- 人工智慧安全威脅與漏洞評估

- 汽車網路安全與人工智慧整合

- 透過設計和開發實踐實現安全性

- 合規性和監理安全要求

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 多邊環境協定

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估計與預測:依車型,2021 - 2034

- 搭乘用車

- 掀背車

- 轎車

- SUV

- 多功能車

- 電動乘用車

- 商用車

- 輕型商用車

- 重型商用車

第6章:市場估計與預測:以推進方式,2021 - 2034 年

- 主要趨勢

- 冰

- 純電動車

- 插電式混合動力

第7章:市場估計與預測:依技術分類,2021 - 2034 年

- 主要趨勢

- 大型語言模型(LLM)和 NLP

- 電腦視覺和圖像生成

- 多模態人工智慧與跨領域整合

- 生成式人工智慧平台和工具

- 其他

第 8 章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 自動駕駛和ADAS應用

- 車輛設計與工程

- 製造和生產最佳化

- 客戶體驗與個人化

- 供應鍊和物流最佳化

- 其他

第9章:市場估計與預測:依最終用途,2021 - 2034

- 主要趨勢

- OEM

- 一級汽車供應商

- 汽車軟體和技術公司

- 出行服務提供者和車隊營運商

第 10 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐人

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 多邊環境協定

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 11 章:公司簡介

- Global Technology Leaders

- Amazon Web Services (AWS)

- IBM

- Intel

- Microsoft

- NVIDIA

- OpenAI

- Qualcomm

- Automotive Technology Specialists

- Aptiv

- Bosch

- Continental

- DENSO

- Magna International

- Mobileye

- Valeo

- Waymo

- ZF Friedrichshafen

- Emerging AI Specialists and Startups

- Argo AI

- Aurora Innovation

- Cruise

- DeepRoute.ai

- Einride

- Ghost Autonomy

- Innoviz Technologies

- Motional

- Plus

- Pony.ai

- Scale AI

- WeRide

- Zoox

The Global Generative AI in Automotive Market was valued at USD 506.6 million in 2024 and is estimated to grow at a CAGR of 23.8% to reach USD 4.58 billion by 2034.

The industry is witnessing rapid transformation as automotive manufacturers increasingly integrate generative artificial intelligence to streamline autonomous systems, optimize design workflows, and simulate critical driving scenarios. Regulatory encouragement and supportive funding are fueling development across automakers, component suppliers, and mobility tech innovators. As digitalization deepens and vehicles become more intelligent and interconnected, generative AI is becoming central to vehicle development. It enables automakers to replicate rare or complex traffic events, drastically cutting the time and costs associated with safety verification. This advanced capability is creating new standards in simulation accuracy and contributing to faster development timelines. Automakers are now leveraging generative AI to enhance user interfaces, predict maintenance requirements, and fine-tune advanced driving assistance systems. As the automotive industry transitions to software-defined vehicles and connected platforms, AI is no longer an enhancement but a core enabler of next-gen mobility ecosystems. Collaborations between software firms and hardware developers are creating foundational infrastructure that supports seamless integration of AI across automotive environments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $506.6 Million |

| Forecast Value | $4.58 Billion |

| CAGR | 23.8% |

In 2024, the passenger vehicle segment generated a 68% share driven by the widespread implementation of intelligent systems across vehicles. AI-enabled technologies are now deeply embedded in functions such as advanced infotainment, driver support features, and in-car safety systems. These tools are significantly elevating the driving experience by improving interaction through conversational interfaces, delivering personalized insights, and powering adaptive responses in real time. Automakers are focusing on AI tools that enhance safety and functionality, with features like proactive service notifications and context-aware driving suggestions. With ongoing enhancements in sensor technology and remote software updates, the application of generative AI in this segment is expected to rise steadily.

The internal combustion engine (ICE) vehicle segment is expected to grow at a CAGR of 14.8% from 2025 to 2034. While electric vehicle platforms are often at the forefront of technological adoption, ICE-powered cars are also integrating AI-driven systems to stay competitive. Automakers are upgrading existing ICE models with intelligent modules that support improved diagnostics, seamless connectivity, and immersive digital experiences. This evolution is being driven by the rising demand for smart functionality in premium ICE vehicles, where retrofitting with AI-based systems is now more accessible through over-the-air updates and scalable platform technologies. Enhanced onboard software allows traditional vehicle categories to benefit from advanced predictive capabilities without requiring major hardware redesigns.

United States Generative AI in Automotive Market generated USD 148.8 million in 2024. The US continues to hold a leadership position due to its strong innovation landscape, vast R&D capabilities, and collaborative efforts spanning academic institutions, technology providers, and government agencies. The integration of generative AI is advancing rapidly across both vehicle systems and the digital infrastructure supporting them. These factors position the US as a primary hub for the development and adoption of generative AI solutions, particularly in enhancing real-time driving intelligence, streamlining vehicle design processes, and facilitating smart mobility solutions.

Key players actively shaping Global Generative AI in Automotive Market include NVIDIA, Amazon Web Services (AWS), Bosch, Microsoft, Qualcomm, Aptiv, IBM, Continental, Intel, and Google. To maintain a competitive edge in the generative AI in automotive market, major players are focusing on strategic alliances, technological innovation, and platform development. Companies are forming long-term partnerships with automakers and tier-one suppliers to ensure seamless AI integration across vehicle systems. Investment in advanced simulation tools, real-time data processing, and edge AI computing is central to their growth approach. Key firms are also expanding their software ecosystems through SDKs and APIs, allowing developers to build AI-powered applications faster.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Propulsion

- 2.2.4 Technology

- 2.2.5 Application

- 2.2.6 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 AI integration in vehicle design and ADAS

- 3.2.1.2 Increasing adoption of electric and connected vehicles

- 3.2.1.3 Cloud and edge AI deployment

- 3.2.1.4 OEM-tech company collaborations

- 3.2.1.5 Advancements in multimodal AI

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Data privacy and cybersecurity

- 3.2.2.2 Integration with legacy systems

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of software-defined and autonomous vehicles

- 3.2.3.2 Collaborations with academic and research institutes

- 3.2.3.3 Emerging markets in Asia-Pacific and Latin America

- 3.2.3.4 Integration with mobility services

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Cost breakdown analysis

- 3.8 Patent analysis

- 3.9 Sustainability and environmental aspects

- 3.9.1 Sustainable practices

- 3.9.2 Waste reduction strategies

- 3.9.3 Energy efficiency in production

- 3.9.4 Eco-friendly Initiatives

- 3.9.5 Carbon footprint considerations

- 3.10 Use cases and Applications

- 3.10.1 Vehicle design and engineering applications

- 3.10.2 Manufacturing and production applications

- 3.10.3 Autonomous driving and ADAS applications

- 3.10.4 Customer experience and service applications

- 3.11 Best-case scenario

- 3.12 Technology and Innovation landscape

- 3.12.1 Current technological trends

- 3.12.2 Emerging technologies

- 3.13 Generative AI technology foundation and evolution

- 3.13.1 Generative AI technology architecture and capabilities

- 3.13.2 Ai model development and training infrastructure

- 3.13.3 Automotive-specific AI model development

- 3.13.4 Technology evolution and future roadmap

- 3.14 Future technology roadmap and innovation timeline

- 3.14.1 Generative AI technology evolution (2024-2034)

- 3.14.2 Automotive AI application development timeline

- 3.14.3 Technology convergence and integration scenarios

- 3.14.4 Disruptive technology assessment and market impact

- 3.15 Automotive industry digital transformation context

- 3.15.1 Automotive industry technology disruption landscape

- 3.15.2 Digital twin and simulation technology integration

- 3.15.3 Data-driven decision making and analytics

- 3.15.4 Automotive software and platform ecosystem

- 3.16 Regulatory environment and standards framework

- 3.16.1 AI governance and regulatory landscape

- 3.16.2 Automotive safety standards and AI integration

- 3.16.3 International standards and harmonization efforts

- 3.16.4 Ethical AI and responsible development framework

- 3.17 Investment landscape and funding analysis

- 3.17.1 Global AI investment trends and automotive focus

- 3.17.2 Automotive industry AI investment patterns

- 3.17.3 Regional investment landscape and government support

- 3.17.4 Startup ecosystem and innovation hubs

- 3.18 Cybersecurity and risk management framework

- 3.18.1 AI security threats and vulnerability assessment

- 3.18.2 Automotive cybersecurity and AI integration

- 3.18.3 Security by design and development practices

- 3.18.4 Compliance and regulatory security requirements

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn)

- 5.1 Passenger vehicles

- 5.1.1 Hatchback

- 5.1.2 Sedan

- 5.1.3 SUV

- 5.1.4 MPV

- 5.1.5 Electric passenger cars

- 5.2 Commercial vehicles

- 5.2.1 Light commercial vehicles

- 5.2.2 Heavy commercial vehicles

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 ICE

- 6.3 BEV

- 6.4 PHEV

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Large language models (LLMs) and NLP

- 7.3 Computer vision and image generation

- 7.4 Multimodal AI and cross-domain integration

- 7.5 Generative AI platforms and tools

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 Autonomous Driving and ADAS Applications

- 8.3 Vehicle Design and Engineering

- 8.4 Manufacturing and production optimization

- 8.5 Customer experience and personalization

- 8.6 Supply chain and logistics optimization

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Tier 1 automotive suppliers

- 9.4 Automotive software and technology companies

- 9.5 Mobility service providers and fleet operators

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Technology Leaders

- 11.1.1 Amazon Web Services (AWS)

- 11.1.2 Google

- 11.1.3 IBM

- 11.1.4 Intel

- 11.1.5 Microsoft

- 11.1.6 NVIDIA

- 11.1.7 OpenAI

- 11.1.8 Qualcomm

- 11.2 Automotive Technology Specialists

- 11.2.1 Aptiv

- 11.2.2 Bosch

- 11.2.3 Continental

- 11.2.4 DENSO

- 11.2.5 Magna International

- 11.2.6 Mobileye

- 11.2.7 Valeo

- 11.2.8 Waymo

- 11.2.9 ZF Friedrichshafen

- 11.3 Emerging AI Specialists and Startups

- 11.3.1 Argo AI

- 11.3.2 Aurora Innovation

- 11.3.3 Cruise

- 11.3.4 DeepRoute.ai

- 11.3.5 Einride

- 11.3.6 Ghost Autonomy

- 11.3.7 Innoviz Technologies

- 11.3.8 Motional

- 11.3.9 Plus

- 11.3.10 Pony.ai

- 11.3.11 Scale AI

- 11.3.12 WeRide

- 11.3.13 Zoox

汽車人工智慧 (AI) 軟體市場分析及預測(至 2035 年):按類型、產品、服務、技術、組件、應用、部署、最終用戶、功能和解決方案分類

汽車人工智慧 (AI) 軟體市場分析及預測(至 2035 年):按類型、產品、服務、技術、組件、應用、部署、最終用戶、功能和解決方案分類 2026年全球汽車人工智慧市場報告

2026年全球汽車人工智慧市場報告 2026-2030年全球汽車技術市場

2026-2030年全球汽車技術市場 汽車人工智慧:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

汽車人工智慧:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026-2034年全球汽車人工智慧市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球汽車人工智慧市場規模、佔有率、趨勢和成長分析報告 汽車人工智慧(AI)市場-全球產業規模、佔有率、趨勢、機會及預測(按組件、技術、工藝、應用、車輛類型、需求類別、地區和競爭格局分類,2021-2031)車輛智慧系統市場-全球產業規模、佔有率、趨勢、機會與預測:按道路場景理解、車輛類型、進階駕駛輔助與監控、地區和競爭格局分類,2021-2031年

汽車人工智慧(AI)市場-全球產業規模、佔有率、趨勢、機會及預測(按組件、技術、工藝、應用、車輛類型、需求類別、地區和競爭格局分類,2021-2031)車輛智慧系統市場-全球產業規模、佔有率、趨勢、機會與預測:按道路場景理解、車輛類型、進階駕駛輔助與監控、地區和競爭格局分類,2021-2031年 汽車人工智慧模擬與合成資料生成市場機會、成長要素、產業趨勢分析及2026年至2035年預測

汽車人工智慧模擬與合成資料生成市場機會、成長要素、產業趨勢分析及2026年至2035年預測 汽車語音AI助理市場規模、佔有率及預測:依AI引擎(自然語言理解、自然語言處理)、語言支援、整合類型(原生、雲端連接)及功能(導航、媒體、車輛控制)劃分-全球預測至2036年

汽車語音AI助理市場規模、佔有率及預測:依AI引擎(自然語言理解、自然語言處理)、語言支援、整合類型(原生、雲端連接)及功能(導航、媒體、車輛控制)劃分-全球預測至2036年 AIGC平台模型市場:2026-2032年全球預測(按模型類型、部署格式、應用和產業分類)

AIGC平台模型市場:2026-2032年全球預測(按模型類型、部署格式、應用和產業分類)