|

市場調查報告書

商品編碼

2045757

休閒車市場機會、成長要素、產業趨勢分析及2026-2035年預測Recreational Vehicle Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

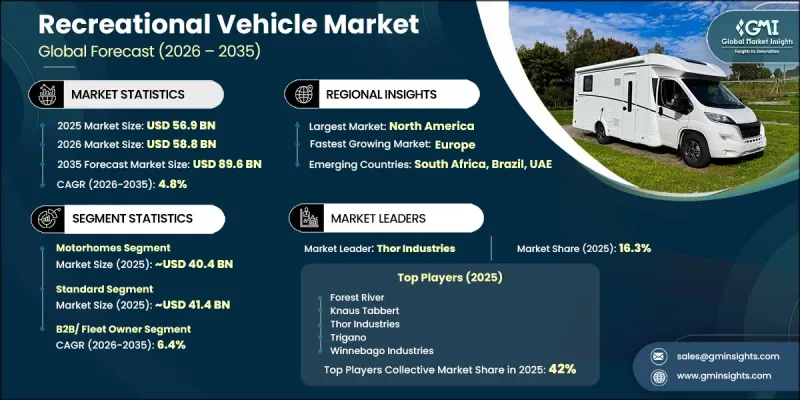

2025 年全球休閒車 (RV) 市場價值為 569 億美元,預計到 2035 年將達到 896 億美元,年複合成長率為 4.8%。

受旅行偏好轉變、戶外休閒參與度提高以及整個產業持續產品創新等因素的推動,休閒車市場正經歷穩定成長。消費者對靈活旅遊體驗和行動生活方式解決方案日益成長的興趣,持續推動全球對休閒車的需求。製造商正在推出緊湊且功能豐富的車型,這些車型配備先進的電源管理系統、太陽能整合、鋰離子電池技術和增強的互聯功能,從而推高了平均售價。人口結構的變化也在市場擴張中扮演重要角色。年輕消費者越來越傾向於短途、頻繁的旅行體驗,而年長消費者則繼續推動對豪華休閒車和高階車型的需求。租賃和點對點車輛共享平台透過鼓勵首次使用者過渡到擁有車輛,進一步擴大了客戶的選擇範圍。此外,隨著製造商探索電動休閒車方案,電氣化技術的進步,以及不斷完善的充電基礎設施和改進的電池技術,正逐步影響整個產業。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 569億美元 |

| 預計金額 | 896億美元 |

| 複合年成長率 | 4.8% |

休閒車(RV)產業正透過進一步整合數位技術、提升車輛效率以及增強旅行舒適度等方式不斷發展。隨著消費者對個人化旅行體驗和媲美轎車的便利性的需求日益成長,製造商正致力於車輛設計、駕駛性能和車載互聯系統的創新。智慧能源管理、整合導航系統、先進安全技術和升級的內裝等功能正成為不同客戶群日益重要的購買考量。同時,更便利的資金籌措和不斷擴展的經銷商網路也讓更多消費者能夠輕鬆擁有休閒車。人們對戶外旅遊的興趣日益濃厚、長途旅行的柔軟性以及行動生活方式的興起,正進一步推動著已開發市場和新興市場休閒車市場的長期成長。

預計到2025年,旅居車市佔率將達到70.9%,市場規模將達到404億美元。由於市面上車型豐富多元,能夠滿足不同消費族群的偏好,旅居車需求持續成長。追求奢華體驗的買家繼續支撐著高階旅居車的需求,而緊湊型和中型房車則因其便利性和柔軟性而受到年輕旅客和家庭的青睞。高級駕駛輔助系統(ADAS)、駕駛輔助技術和增強型互聯解決方案正擴大應用於中高階旅居車,從而提升整體駕駛體驗和消費者興趣。

預計到2025年,標準型休閒車市場規模將達到415億美元,並在2026年至2035年間以4.3%的複合年成長率成長。標準型休閒車因其實用功能、價格實惠以及可靠的季節性旅行性能而持續受到歡迎。這些車型提供必要的便利設施和耐用的結構,同時價格也適合廣大消費者。強大的經銷商網路、靈活的融資方案和豐富的產品線持續支撐著全球市場對標準型休閒車的需求。

美國休閒車市場預計到2025年將達到257億美元,並在2035年之前以4.7%的複合年成長率成長。憑藉其濃厚的戶外休閒文化、四通八達的公路網路和豐富的露營設施,美國仍然是全球最大、最成熟的休閒車市場之一。消費者對公路旅行、戶外旅遊和靈活住宿選擇日益成長的興趣持續支撐著美國市場的需求。此外,便利的租賃方式、遠距辦公的柔軟性以及人們對行動生活方式的日益青睞,也吸引更多年輕消費者進入這個市場。

目錄

第1章:調查方法

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 人們對體驗式旅遊和探險旅遊的興趣日益濃厚

- 千禧世代和Z世代對戶外休閒的興趣日益濃厚。

- 遠距辦公的出現使得長期房車旅行成為可能。

- 新興市場可支配所得增加

- 產業潛在風險與挑戰

- 需求季節性波動和運轉率下降

- 露營地基礎設施和停車設施不足

- 市場機遇

- 開發用於永續旅行的電動和混合動力房車

- 租賃和共享經濟平台的擴張

- 進入尚未開發的亞太市場

- 促進因素

- 技術與創新展望

- 最新科技趨勢

- GPS導航和遠端資訊處理系統

- 整合太陽能發電系統

- 新興技術

- 車輛到電網(V2G)充電系統

- 氫燃料電池推進系統

- 最新科技趨勢

- 成長潛力分析

- 價格分析

- 對過去價格趨勢的分析

- 依球員類型分類的定價策略(高級球員、超值球員、成本加成球員)

- 監理情勢

- 北美洲

- 美國-《清潔空氣法》(CAA)

- 美國 - 聯邦機動車輛安全標準 (FMVSS)

- 加拿大 - 機動車輛安全法 (MVSA)

- 歐洲

- 歐盟歐VI車輛排放氣體標準

- 歐盟通用安全法規 (GSR) 2019/2144

- 亞太地區

- 中國——中國V1排放氣體標準

- 印度 - 第六階段(BS-VI)排放氣體法規

- LATAM

- 巴西 - PROCONVE 汽車排放氣體控制計劃

- 智利 - 汽車排放氣體標準 DS No. 211

- 中東和非洲

- 阿拉伯聯合大公國-阿拉伯聯合大公國汽車安全法規

- 沙烏地阿拉伯 - SASO燃油經濟性標準

- 北美洲

- 波特的分析

- PESTLE分析

- 貿易數據分析

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- 生產能力和生產情況

- 設備產能:按地區和主要生產商分類

- 運轉率和擴張計劃

- 成本細分分析

- 原料和零件成本

- 製造和組裝成本

- 動力傳動系統和能源系統的成本

- 內裝和舒適性配置的成本

- 分銷和物流成本

- 專利分析

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 考慮碳足跡

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 按細分市場分類的生成式人工智慧用例和部署藍圖

- 風險、限制和監管考量

- 從所有權經濟轉向租賃經濟的轉變

- 按車輛類型和地區分類的租賃市場滲透率

- 透過P2P租賃平台實現轉型

- 傳統所有製模式衰落的機制

- 預測假設和情境分析

- 基本案例:驅動複合年成長率的關鍵宏觀經濟與產業變量

- 樂觀情境:宏觀經濟與產業的順風

- 悲觀情景:宏觀經濟放緩或產業逆風

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- LATAM

- 中東和非洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃及資金籌措

- 按公司規模進行基準測試

- 排名分類標準與遴選標準

- 按銷售額、地區和創新能力分類的層級定位矩陣。

第5章 市場估價與預測:依車輛類型分類,2022-2035年

- 露營車

- 班級

- A級

- B級

- C級

- 燃料

- 汽油

- 柴油引擎

- 電池式電動車

- 混合

- 班級

- 拖曳式房車

- 折疊式/露營拖車

- 卡車露營車

- 第五輪拖車

- 旅行拖車

第6章 市場估計與預測:依價格區間分類,2022-2035年

- 標準

- 奢華

第7章 市場估計與預測:依應用領域分類,2022-2035年

- B2C/個人

- B2B/車隊車主

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 瑞典

- 挪威

- 瑞士

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 泰國

- 印尼

- 馬來西亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 智利

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第9章:公司簡介

- 世界公司

- Thor Industries

- Forest River

- Winnebago Industries

- REV Group

- Trigano

- Knaus Tabbert

- Hymer

- Wildax Motorhomes

- Dethleffs

- Burstner

- Hobby Caravan

- Groupe Pilote

- 當地公司

- Triple E RV

- Adria Mobil

- Swift Leisure

- Fendt Caravan

- Bailey of Bristol

- Zone RV

- Giottiline

- 新興企業

- Sportsmobile

- Kimberley Kampers

- Tonke Campers

The Global Recreational Vehicle Market was valued at USD 56.9 billion in 2025 and is estimated to grow at a CAGR of 4.8% to reach USD 89.6 billion by 2035.

The market is witnessing stable growth supported by changing travel preferences, rising participation in outdoor recreation, and ongoing product innovation across the industry. Increasing consumer interest in flexible travel experiences and mobile living solutions continues to drive demand for recreational vehicles worldwide. Manufacturers are introducing compact yet feature-rich models equipped with advanced power management systems, solar integration, lithium battery technologies, and enhanced connectivity features, which are contributing to higher average selling prices. Demographic shifts are also playing a major role in market expansion as younger consumers increasingly prefer shorter and more frequent travel experiences, while older consumers continue to support demand for luxury recreational vehicles and premium models. Rental and peer-to-peer vehicle sharing platforms are further broadening customer accessibility by encouraging first-time users to transition toward ownership. In addition, advancements in electrification technologies are gradually influencing the industry as manufacturers explore electric recreational vehicle options supported by evolving charging infrastructure and battery technology improvements.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $56.9 Billion |

| Forecast Value | $89.6 Billion |

| CAGR | 4.8% |

The recreational vehicle industry is continuing to evolve through stronger integration of digital technologies, improved vehicle efficiency, and enhanced travel comfort features. Consumer demand for personalized travel experiences and automotive-grade convenience is encouraging manufacturers to focus on innovation across vehicle design, drivability, and onboard connectivity systems. Features such as intelligent energy management, integrated navigation systems, enhanced safety technologies, and improved interior functionality are becoming increasingly important purchasing factors across multiple customer groups. At the same time, financing accessibility and expanding dealership networks are making recreational vehicles more attainable for a wider customer base. Growing interest in outdoor tourism, remote travel flexibility, and mobile lifestyles is further supporting long-term market growth across developed and emerging regions.

The motorhomes segment held a 70.9% share, generating USD 40.4 billion in 2025. Demand for motorhomes continues to rise due to the availability of multiple vehicle formats designed to meet the preferences of different consumer groups. Luxury-oriented buyers continue to support demand for high-end motorhomes, while compact and mid-sized models are gaining popularity among younger travelers and families seeking convenience and flexibility. Advanced safety systems, driver-assistance technologies, and enhanced connectivity solutions are increasingly being integrated into mid-range and premium motorhomes, improving overall driving experience and consumer appeal.

The standard applications segment generated USD 41.5 billion in 2025 and is anticipated to grow at a CAGR of 4.3% from 2026 to 2035. Standard recreational vehicles remain popular due to their practical functionality, accessible pricing structure, and dependable performance for seasonal travel use. These models offer essential amenities and durable construction while maintaining affordability for a broad consumer base. Strong dealership networks, flexible financing options, and diverse product availability continue to support demand for standard recreational vehicles across global markets.

U.S. Recreational Vehicle Market reached USD 25.7 billion in 2025 and is projected to grow at a CAGR of 4.7% through 2035. The country remains one of the largest and most mature recreational vehicle markets globally due to its strong outdoor recreation culture, extensive road transportation network, and broad availability of camping facilities. Increasing consumer interest in road travel, outdoor tourism, and flexible accommodation options continues to support demand across the United States. Younger consumers are also entering the market in greater numbers, encouraged by rental accessibility, remote work flexibility, and growing interest in mobile travel lifestyles.

Major companies operating in the Global Recreational Vehicle Market include Adria Mobil, Forest River, Hobby Caravan, Hymer, Knaus Tabbert, REV Group, Swift Leisure, Thor Industries, Trigano, and Winnebago Industries. Companies operating in the recreational vehicle market are focusing on product innovation, strategic partnerships, and digital transformation initiatives to strengthen their market position and expand customer reach. Leading manufacturers are investing in lightweight materials, advanced power management systems, lithium battery integration, and smart connectivity features to improve vehicle performance and enhance customer experience. Many companies are also expanding compact and luxury model portfolios to address changing consumer preferences across multiple demographic groups. Strategic collaborations with rental platforms and dealership networks are helping businesses increase brand visibility and convert first-time renters into long-term owners. In addition, manufacturers are prioritizing sustainability initiatives by exploring electric recreational vehicle technologies, energy-efficient systems, and eco-friendly manufacturing processes. Enhanced financing solutions, aftermarket services, and customization options are also supporting stronger customer retention and long-term market growth.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Price Point

- 2.2.4 Application

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Preference for Experiential Travel & Adventure Tourism

- 3.2.1.2 Growing Millennial & Gen Z Interest in Outdoor Recreation

- 3.2.1.3 Remote Work Normalization Enabling Extended RV Travel

- 3.2.1.4 Increasing Disposable Income in Emerging Markets

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Seasonal Demand Fluctuation & Low Utilization Rates

- 3.2.2.2 Limited Campground Infrastructure & Parking Facilities

- 3.2.3 Market opportunities

- 3.2.3.1 Electric & Hybrid RV Development for Sustainable Travel

- 3.2.3.2 Rental & Sharing Economy Platform Expansion

- 3.2.3.3 Expansion into Underpenetrated Asia-Pacific Markets

- 3.2.1 Growth drivers

- 3.3 Technology and innovation landscape

- 3.3.1 Current technological trends

- 3.3.1.1 GPS Navigation and Telematics Systems

- 3.3.1.2 Solar Power Integration Systems

- 3.3.2 Emerging technologies

- 3.3.2.1 Vehicle-to-Grid (V2G) Charging Systems

- 3.3.2.2 Hydrogen Fuel Cell Propulsion Systems

- 3.3.1 Current technological trends

- 3.4 Growth potential analysis

- 3.5 Pricing Analysis (Driven by Primary Research)

- 3.5.1 Historical Price Trend Analysis

- 3.5.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 US - U.S. Clean Air Act (CAA)

- 3.6.1.2 US - Federal Motor Vehicle Safety Standards (FMVSS)

- 3.6.1.3 Canada - Motor Vehicle Safety Act (MVSA)

- 3.6.2 Europe

- 3.6.2.1 EU - Euro VI Vehicle Emission Standards

- 3.6.2.2 EU - General Safety Regulation (GSR) 2019/2144

- 3.6.3 Asia Pacific

- 3.6.3.1 China - China VI Emission Standards

- 3.6.3.2 India - Bharat Stage VI (BS-VI) Emission Norms

- 3.6.4 LATAM

- 3.6.4.1 Brazil - PROCONVE Vehicle Emission Control Program

- 3.6.4.2 Chile - Vehicle Emission Standard DS No. 211

- 3.6.5 MEA

- 3.6.5.1 UAE - UAE Vehicle Safety Regulations

- 3.6.5.2 Saudi Arabia - SASO Fuel Economy Standards

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Trade Data Analysis (Driven by Paid Database)

- 3.9.1 Import/Export Volume & Value Trends

- 3.9.2 Key Trade Corridors & Tariff Impact

- 3.10 Capacity & Production Landscape (Driven by Primary Research)

- 3.10.1 Installed Capacity by Region & Key Producer

- 3.10.2 Capacity Utilization Rates & Expansion Pipelines

- 3.11 Cost breakdown analysis

- 3.11.1 Raw materials & components costs

- 3.11.2 Manufacturing and assembly costs

- 3.11.3 Powertrain and energy system costs

- 3.11.4 Interior and comfort feature costs

- 3.11.5 Distribution and logistics costs

- 3.12 Patent analysis (Driven by Primary Research)

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable Practices

- 3.13.2 Waste Reduction Strategies

- 3.13.3 Energy Efficiency in Production

- 3.13.4 Eco-friendly Initiatives

- 3.13.5 Carbon Footprint Considerations

- 3.14 Impact of AI & generative AI on the market

- 3.14.1 AI-driven disruption of existing business models

- 3.14.2 GenAI use cases & adoption roadmap by segment

- 3.14.3 Risks, limitations & regulatory considerations

- 3.15 Ownership vs rental economy shift

- 3.15.1 Rental market penetration by vehicle type & geography

- 3.15.2 Peer-to-peer rental platform disruption

- 3.15.3 Traditional ownership model erosion dynamics

- 3.16 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.16.1 Base Case- Key Macro & Industry Variables Driving CAGR

- 3.16.2 Optimistic Scenarios- Favorable macro and industry tailwinds

- 3.16.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates and Forecast, By Vehicle, 2022 - 2035 ($ Mn, Units)

- 5.1 Key trends

- 5.2 Motorhomes

- 5.2.1 Class

- 5.2.1.1 Class A

- 5.2.1.2 Class B

- 5.2.1.3 Class C

- 5.2.2 Fuel

- 5.2.2.1 Gasoline

- 5.2.2.2 Diesel

- 5.2.2.3 Battery-Electric

- 5.2.2.4 Hybrid

- 5.2.1 Class

- 5.3 Towable RVs

- 5.3.1 Folding/Camping Trailers

- 5.3.2 Truck Campers

- 5.3.3 Fifth Wheeler

- 5.3.4 Travel Trailers

Chapter 6 Market Estimates and Forecast, By Price Point, 2022 - 2035 ($ Mn, Units)

- 6.1 Key trends

- 6.2 Standard

- 6.3 Luxury

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn, Units)

- 7.1 Key trends

- 7.2 B2C/individual

- 7.3 B2B/ Fleet owner

Chapter 8 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 US

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.3.7 Sweden

- 8.3.8 Norway

- 8.3.9 Switzerland

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 South Korea

- 8.4.4 India

- 8.4.5 Thailand

- 8.4.6 Indonesia

- 8.4.7 Malaysia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Chile

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global players

- 9.1.1 Thor Industries

- 9.1.2 Forest River

- 9.1.3 Winnebago Industries

- 9.1.4 REV Group

- 9.1.5 Trigano

- 9.1.6 Knaus Tabbert

- 9.1.7 Hymer

- 9.1.8 Wildax Motorhomes

- 9.1.9 Dethleffs

- 9.1.10 Burstner

- 9.1.11 Hobby Caravan

- 9.1.12 Groupe Pilote

- 9.2 Regional players

- 9.2.1 Triple E RV

- 9.2.2 Adria Mobil

- 9.2.3 Swift Leisure

- 9.2.4 Fendt Caravan

- 9.2.5 Bailey of Bristol

- 9.2.6 Zone RV

- 9.2.7 Giottiline

- 9.3 Emerging players

- 9.3.1 Sportsmobile

- 9.3.2 Kimberley Kampers

- 9.3.3 Tonke Campers

休閒車市場-2026-2032年全球市場預測

休閒車市場-2026-2032年全球市場預測 休閒車市場分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、材料類型、最終用戶、安裝配置

休閒車市場分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、材料類型、最終用戶、安裝配置 全球休閒車市場

全球休閒車市場 休閒車輛:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

休閒車輛:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026-2030年全球休閒車(RV)市場

2026-2030年全球休閒車(RV)市場 露營車(RV)市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測

露營車(RV)市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測 休閒車市場規模、佔有率和成長分析(按地區分類)-2026-2033年產業預測北美休閒車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)歐洲休閒車:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

休閒車市場規模、佔有率和成長分析(按地區分類)-2026-2033年產業預測北美休閒車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)歐洲休閒車:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球休閒車市場:依類型、應用和地區劃分 - 市場規模、行業趨勢、機會分析和預測(2025-2033 年)

全球休閒車市場:依類型、應用和地區劃分 - 市場規模、行業趨勢、機會分析和預測(2025-2033 年)